RVTTY - Sega Sammy: Pachinko Optimism But Gaming IPs Are Solid Beyond Sonic

2023-11-23 08:00:00 ET

Summary

- Sega Sammy has strong gaming IPs, including Total War, Football Manager, Sonic, Yakuza, and Persona - recently also Angry Birds through the Rovio acquisition.

- The company trades at a steep discount compared to peers as Sonic in particular is viewed as being a fallen angel of an IP, which is not that inaccurate.

- The Pachinko business is rebounding with the loosening of regulations and the introduction of smart machines, which are seeing an uptake in parlours, driving growth.

- Over the years, we expect them to get involved in US online gambling growth and to benefit from more convention, entertainment, and gambling activity at their resorts with the end of the pandemic.

- We think that it's reasonable that they hit forecasts which defends them in the short term, and that they have a lot of resources to generate sustainable growth. Earnings direction and absolute valuation are positives here.

Sega Sammy ( SGAMF )( SGAMY ) looks pretty interesting. It has some pretty strong gaming IPs. Total War, Football Manager through SI Games, obviously Sonic, and also the Yakuza games and Persona. Some of these are really at the forefront in their categories. The main ailing IP is Sonic, and that is only in a relative sense compared to the 90s, where Sonic Frontiers last year was a megahit.

The reality is that it trades at a steep discount to reasonable peers in a blended multiple of both their games business as well as Pachinko, which is undergoing an upcycle in terms of regulatory considerations. Also, we think Football Manager 2024, probably not Sonic Superstars, gets us to the forecasts. Also, the business is family-controlled by the Satomis, who owned Sammy and now have power over the Sega IPs. While the direction seems better than before, the lack of expressive shareholder pressure is a possible concern, even though there isn't much demonstrating this as a problem at this point.

Businesses

Entertainment

Sega Sammy makes videogames , a very high multiple market with consumer staple status and high margins. One of the best possible businesses to be in as far as market appraisal goes. This is definitely the crown jewel and establishes the underlying quality of the Sega Sammy profile.

In addition to the obvious IP of Sonic , which Sega originated, they also have other really good subsidiaries that make very established titles such as Creative Assembly, a European studio that works on the Total War franchise , which also makes use of the Warhammer Fantasy IP.

In their stable are also the Yakuza games, which have a strong cult following, as well as the Persona series which is very mainstream. They also own Sports Interactive Limited, which is the company with the Football Manager franchise and database.

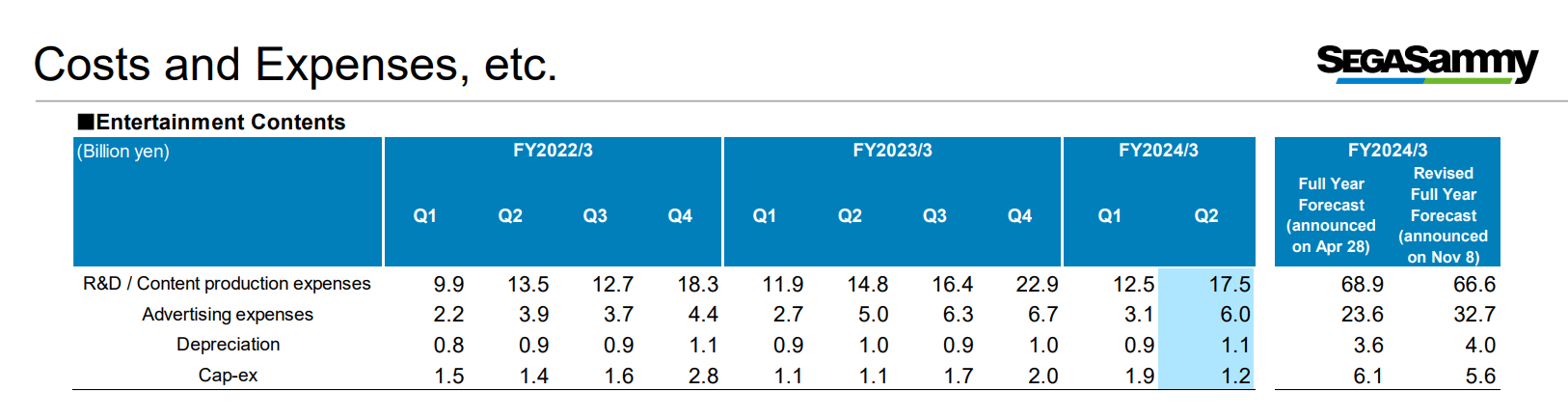

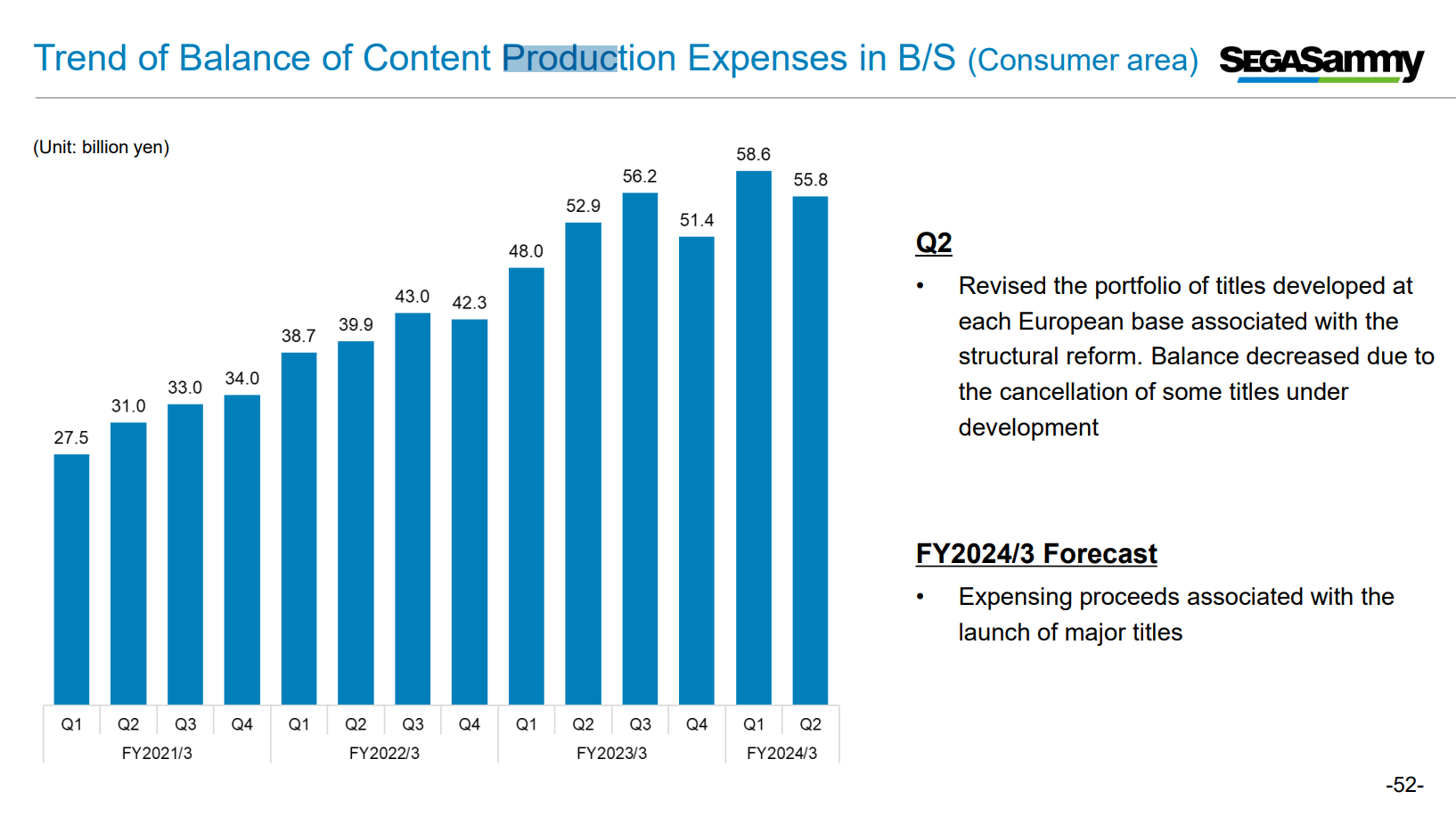

There are some troubles in this business though, beginning with the expense bloat, which is related to the big, negative news of the HYENAS cancellation.

Expenses (Q2 Pres) Production Costs (Q2 Pres)

{kind=link}

{kind=link}

What happened here is that Creative Assembly was working on HYENAS, which was supposed to be a live service F2P shooter. It looked decent; it was a long-time-to-kill shooter with some heist elements. There was a closed Beta, and people seemed to like it but market commentators had some concerns including the general saturation of F2P shooters. The game looked ready to go, so the fact that they cancelled the whole project was a real punch in the teeth as they had already spent everything they needed to spend to launch this game. The fact that they didn't think it was still worth launching on the increment is very telling of the F2P saturation and the fact that Sega probably couldn't pull off an F2P launch considering its history with single-player titles and franchises.

There are some knock-on effects here that we believe are responsible for the come-down in price of Sega Sammy. They are doing a structural reform, resulting in write-downs from cancelled projects, including HYENAS but also some other unannounced ones focused on the fact that profitability in European businesses is tough to improve. They are also eliminating backend redundancy by combining some of the backends they use for publishing games overseas, merging US and European publishing. So narrowing lineups at their studios as well as reducing fixed costs, and also trying to get regrowth by continuing to leverage IPs and now to challenge the mobile gaming market with Rovio ( ROVVF ).

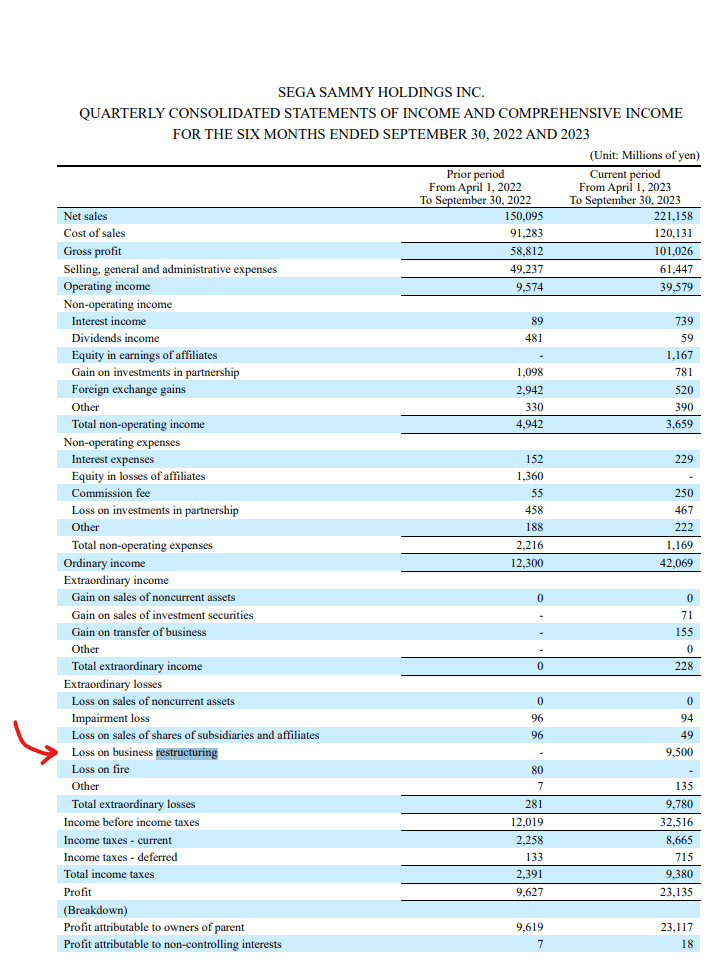

The restructuring losses are meaningful and can be seen below.

{kind=link}

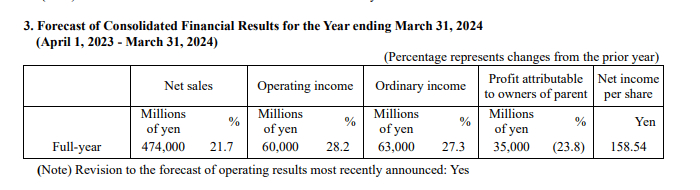

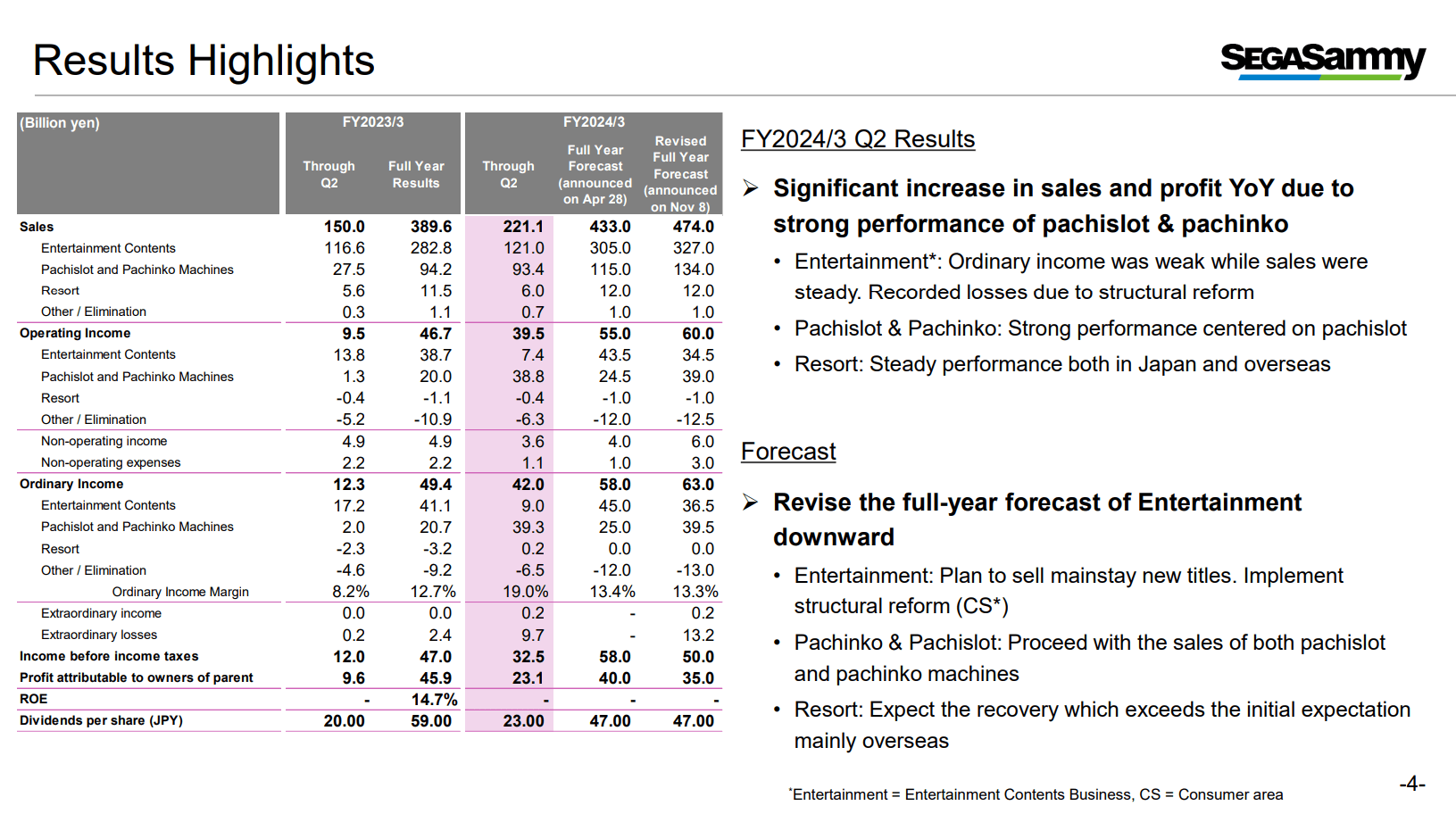

It will badly affect bottom line forecasts for the FY due to below-the-line restructuring, but also some of the lost revenue is bringing down the segment forecasts for gaming.

Forecasts (Q2 PR) Highlights (Q2 Pres)

{kind=link}

{kind=link}

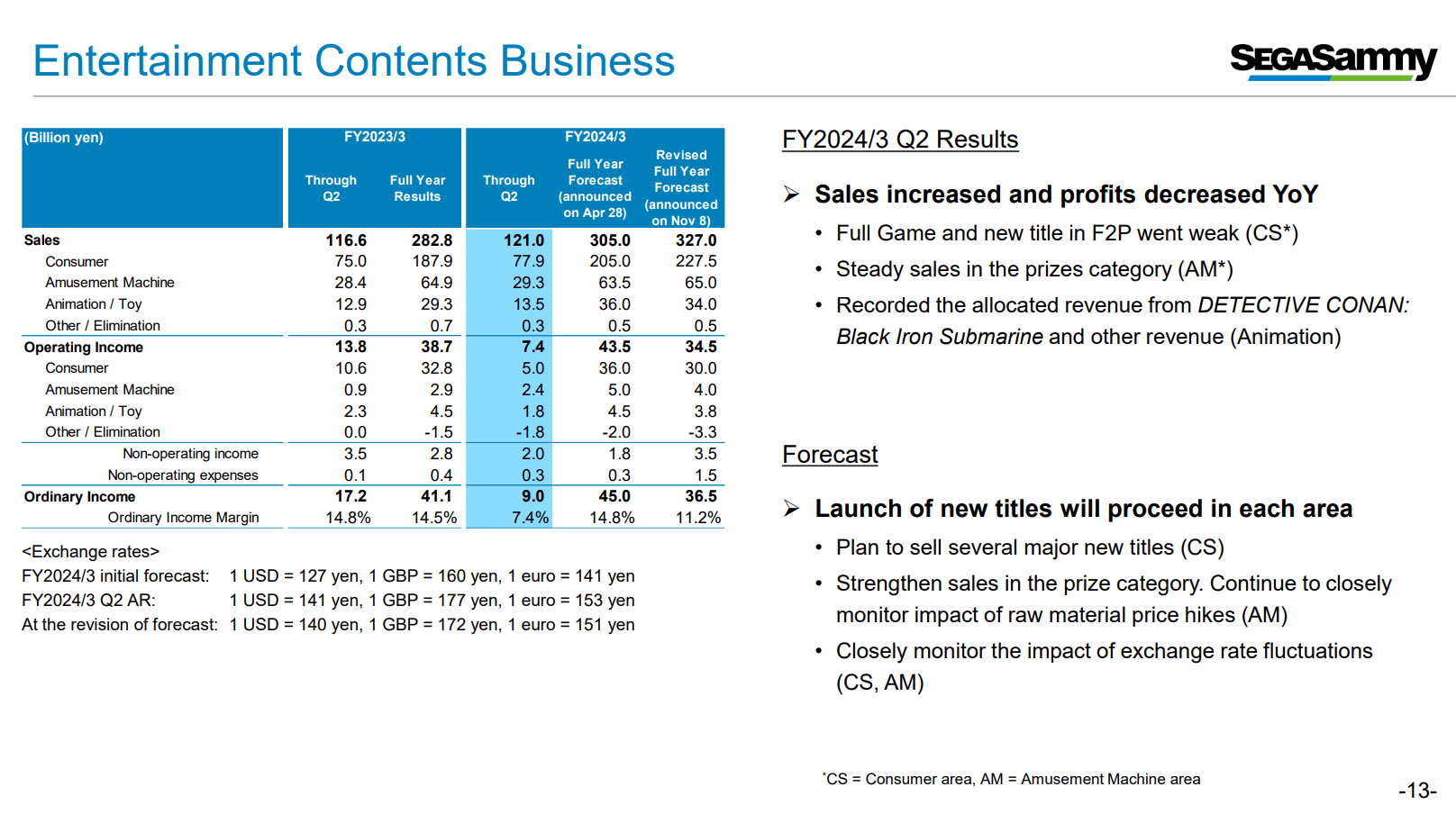

There have been some new releases: classic style side-scrolling Sonic Superstars which came out in mid-October. There are also new launches of Persona spinoffs and some remasters, as well as another title in connection with the Yakuza series which came out on November 8th which started off with "overwhelmingly positive" reviews on Steam. Another Yakuza-related title comes out in January next year. Games sales look good, it's just that the screw-ups in development productivity are dragging on operating income, but sales will grow and the full consolidation of Rovio that began in August will start giving some power to results and a new IP platform. The Angry Birds movies tripled their budgets in box office receipts and the games continue to sell well.

{kind=link}

Having a look at SteamDB , we can look at the potential value of the new titles in terms of sales contribution over the next two quarters, composing the rest of the FY. We used the distribution of sales data from this paper to estimate total revenue from current counts. Current counts have been scaled up as Steam figures (all estimates by the way) are only for PC, and most of these releases are multi-platform . Rovio probably adds about 20 billion Yen over an annualised figure for existing titles over the next two quarters, and the new titles we calculate may add another 25 billion Yen. 40 billion Yen seems to be the threshold needed over the existing titles to meet expectations, so that looks pretty good.

New Title VTS Forecasts (VTS)

There are a couple of elements outside of the gaming space, which is consumer. There are amusement machines, which are things like crane games . This market has rebounded post-COVID. Pretty stable market domestically, and they are planning on trying to expand to foreign markets, but it's doubtful that it will work.

In animation, they have great underlying IPs; Lupin the 3rd, Detective Conan, Anpanman among others. Detective Conan movie was a nice addition for the year, and the animation business lets them complete their multimedia offering and monetise their properties as much as possible. This is quite evergreen.

Resorts and Gaming

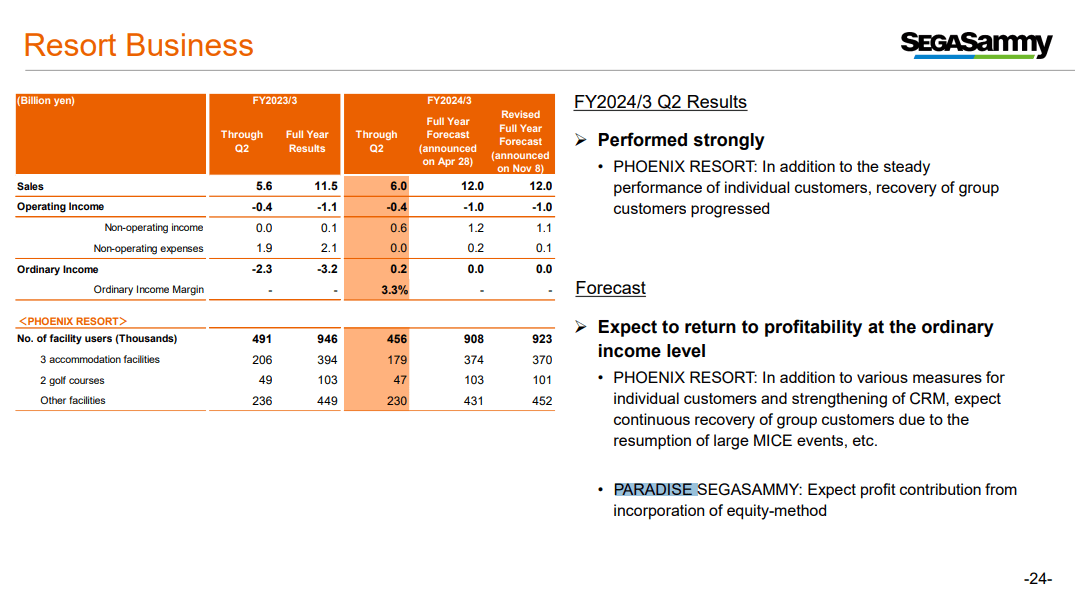

The resorts business consists of the Phoenix Resort (non-gambling) in Japan, as well as the equity-accounted affiliate business of Paradise City in Korea which does have a casino and would be similar to the sort of resorts typical of the Vegas entertainment majors in the US. Both are benefiting from the return of convention activity and general recovery in mobility as the pandemic is now completely a thing of the past, and in gaming, the drop amounts of Japanese VIPs that are going abroad to game are rising dramatically in a rebound.

{kind=link}

It's quite a small segment currently, but there are some actions being undertaken, specifically the acquisition of GAN Limited ( GAN ) which is of some interest and will be the platform for more investment into gaming exposures outside of resorts and Pachinko, which is quite demographically and geographically particular.

Gan does SaaS for casino operators and has its own B2C business of online gambling. There are a lot of approvals that need to come through so the acquisition won't close before March 2025, but it will give them a platform to position themselves as B2B players in the US gambling space, which is a growing arena.

Pachinko and Pachislot

Otherwise, Sega Sammy makes Pachinko machines and Pachislot machines. The difference between this and slots in the US is that there is a legitimate skill-based component to these games. Gambling is also generally illegal in Japan although the first casinos are being approved now and built, but Pachinko and Pachislot have been able to get around this in various arcane ways, but it is true that these games require reaction time and other dexterity to succeed at them. Pachislot is more similar to slots, while Pachinko is its own type of minigame, but again both have skill-based components.

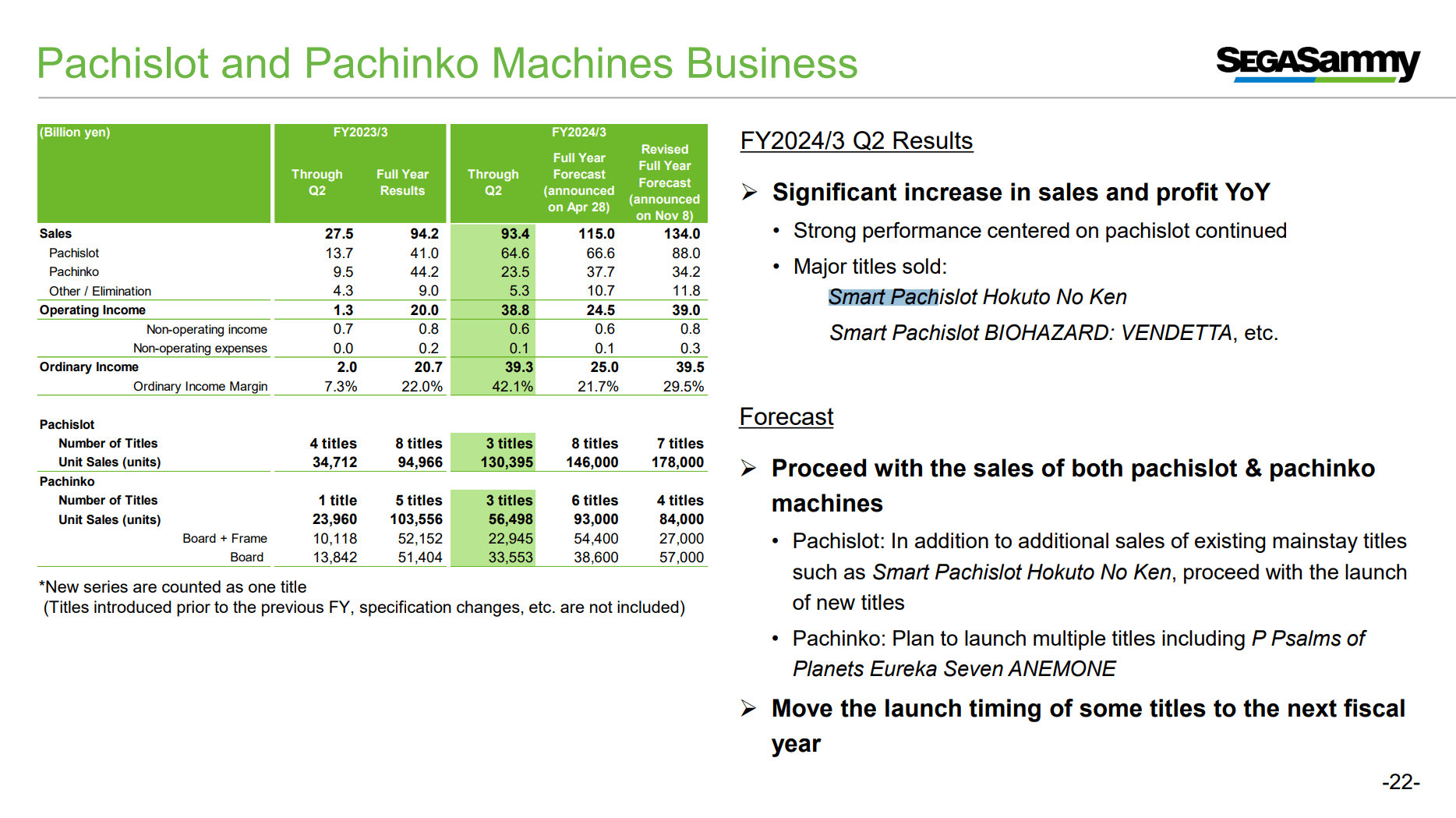

Pachinko was a bit of a dying market due to demographic factors and also expensive underlying regulations that force frequent upgrades and replacement of these machines at a minimum every two years, but it was compounded in 2016 by laws around gambling addiction, that were enacted into law not because of the Pachinko industry but because of the recent legalisation of casinos - Pachinko got caught in the crossfire. The industry has been shrinking since re-regulation till now by about 5% per year driven by parlour closures. Payouts from the machines were reduced and so was excitement, and advertising curbs also limited growth. But rules have loosened recently, specifically allowing more latitude for Pachinko advertising but also around Pachinko machine features, and analysts in the sector typically see the regulatory cycles playing out over a decade before turning again. This is going to be good for smaller Pachinko operators that have been under a lot of pressure from both higher utility costs and the inability to run profitably with all the regulation, who have otherwise been leaving the market in droves over the last decade. The end of the pandemic has also helped. Although, the market is still generally on a downtrend, especially on general inflation .

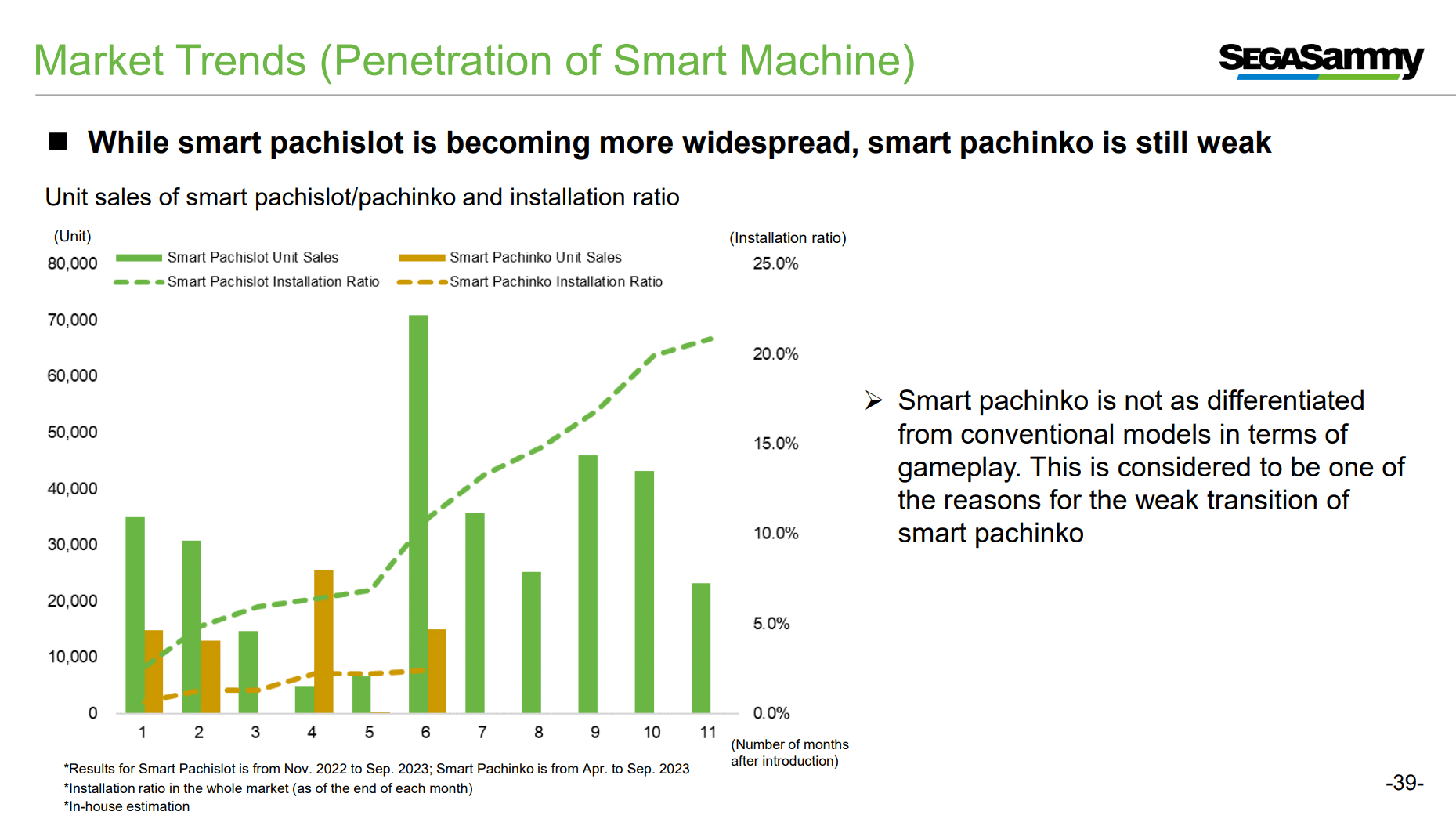

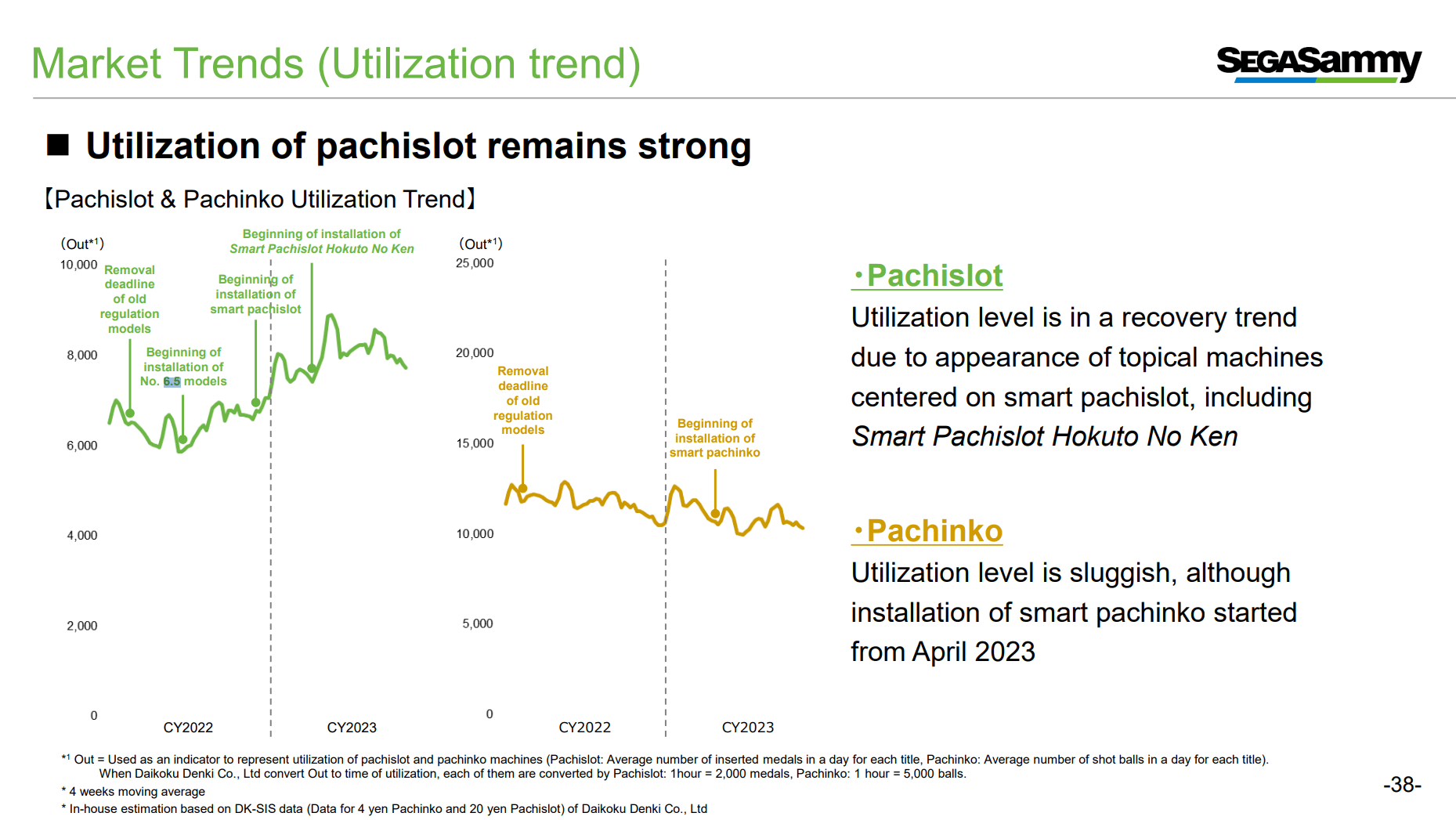

There are more trends to be aware of. There are now Smart Pachislot and Smart Pachinko machines that are easier to manage because they don't shoot out medals or coins associated with their slot machine-like jackpots. These are really expensive machines, and only really make sense for high profile parlours to buy. The good thing is Sega Sammy is highly exposed to these sorts of machines and high quality customers, and ordering for these units has wholly beaten expectations and puts them ahead of less sophisticated competitors. This is also why Pachislot grew but Pachinko not as much - Pachislot is younger and the smart machines drive more of the mix there, while Pachinko is still waiting for the smart products to grow in the mix. Utilisation rates are also growing faster on Pachislot compared to Pachinko, driving upgrades. Sega Sammy, as well as competitor Universal Entertainment ( OTCPK:UETMF ), have also both been benefiting from the periodic need of parlours to upgrade machines to comply with gambling standards, now getting lots of orders for the 6.5th generation Pachislot machines, and also orders for Smart Pachinko machines too although smartification hasn't been as successful in Pachinko compared to Pachislot with interest from parlours pretty low for now - a hit title will be needed in the future to drive penetration . Universal has seen orders spike, and Sega Sammy has already been able to make deliveries as customer parlours upgrade.

Smart Penetration (Q2 Pres) Pachinko Segment (Q2 Pres)

{kind=link}

{kind=link}

The Sega Sammy Pachinko business is rocketing driven by pachislot although Pachinko is looking more resilient on the sales front in forecasts from November compared to April. This upward revision is nice to see. Also, they are coming out with new titles in both. Remember also that period replacement is mandated in the industry. As investors, we just need to hope that parlours can run profitably and won't close. But these new titles are being put out till they can be released in the next fiscal year also with more features, as new possible features are coming to market thanks again to regulation loosening. In general, Pachinko is actually looking like a decent market now.

{kind=link}

Management Plan

The plan is straightforward: use the platforms to grow the consumer business organically and look for opportunities in integrated resorts and gaming. For Pachinko and Pachislot, keep things stable.

They are also doing buybacks. Their outstanding programme for this year is for a 2.5% buyback, which is nothing to scoff at, and they want to stably increase dividends offering a minimum 50% payout ratio including buybacks. Minimum 3% return of book value of equity annually in dividends .

The capital structure is pretty normalised, so despite the ownership situation in the company, there aren't a lot of reasons for why they wouldn't stick to this. Moreover, their businesses offer a fair bit of reinvestment opportunities.

Valuation

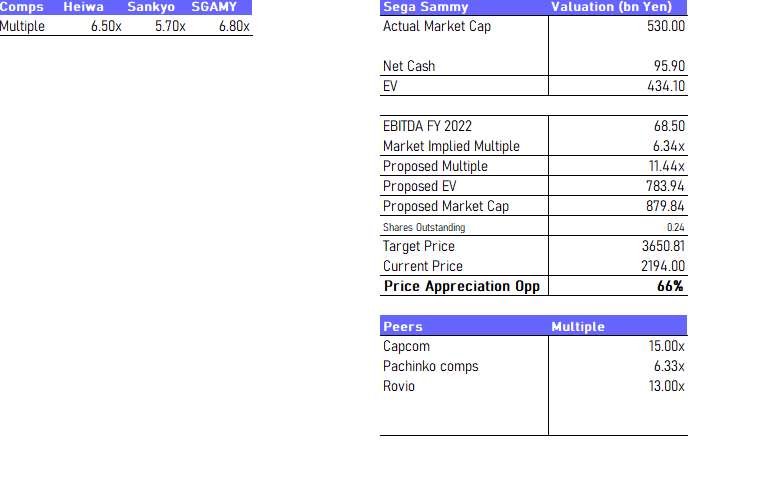

For valuation, we do a blended multiple weighted towards gaming peers since that has traditionally been most of their operating income, and the remainder of the blend is towards Pachinko peers. While the forecasts show that there should be closer to a 50:50 split between the segments the upside remains substantial.

{kind=link}

Conclusions

Ultimately, it's pretty likely that they'll keep growing earnings. Pachinko and Pachislot are in a regulatory uptrend, and there is still a way to go with smart Pachinko machines. The economics are highly recurring.

In consumer, income is being hit, but portfolio normalisation and one-offs related to restructuring should tilt up the income. Also, they had a big hit with IPs beginning last year that we hope to see continue. A lot of great titles are still being released. But they could realistically cause some disappointment. These markets get saturated with releases, and multiple from the same franchise may not work out.

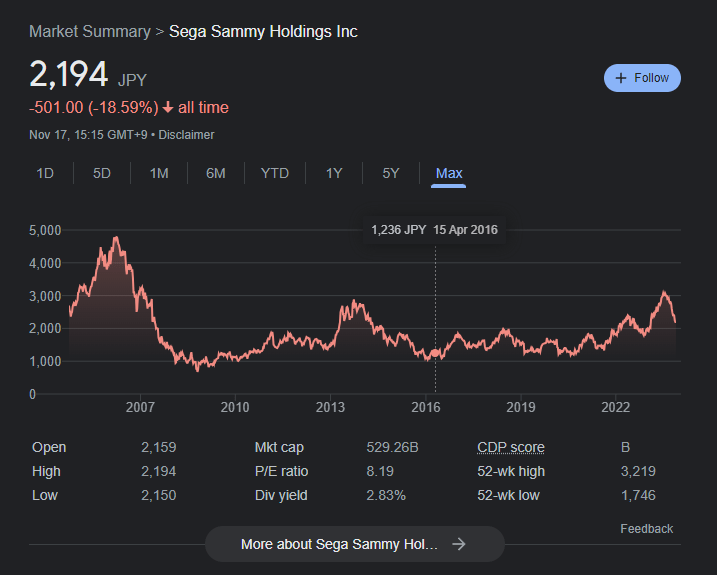

Performance of Domestic Listing (Google Finance)

{kind=link}

The stock also happens to be on a pretty steep downtrend. It has made no YTD progress. Could be a buying moment at a 10x PE on a normalised basis and a low EV/EBITDA gives that margin of safety, especially considering Nintendo is at above 15x PE and other gaming multiples all lie clearly above twice the EV/EBITDA multiple of Sega Sammy.

We also like that there is decent remuneration, around 2.8% in dividend, as well as an ongoing 2.5% buyback programme for this year.

Our only concerns are longer-term earnings disappointments and the effects that a tighter consumer wallet might have on Sega titles, especially F2P titles, which incidentally interact with the growing exposure to those games through the Rovio acquisition. They have pretty good IPs, way above average and more likely to be a cash cow than something newly created, but when even Nintendo can disappoint and with a terrible record over the last decade of handling IPs by Sega, we are inclined to understand market action and do wonder if we'd want to maybe see some more declines first, even if we think the current forecasts will be reached.

Finally, there are risks with Japan. While not terribly likely, if the BoJ pivots to save the Yen despite possible impacts that a tighter environment will have on the economy, we may see quite the rotation from Japanese equities. Thankfully, Sega has a fair bit of foreign exposure, and it grew with the Rovio acquisition.

However, Pachinko is a bit of a definite grower over the next year which gives a really strong basis for the underlying direction, and they are growing in the mix. Leaning heavily towards buy.

For further details see:

Sega Sammy: Pachinko Optimism, But Gaming IPs Are Solid Beyond Sonic