SEGXF - SEGRO: A Quality Play On The U.K. Property Recovery

Summary

- SEGRO further builds out its data center presence via the GBP120m acquisition of Bath Road Shopping Park.

- Supported by a UK property market that has likely troughed and a best-in-class balance sheet, SEGRO is well-positioned to weather a recession scenario.

- At the current book value discount, the stock offers investors a compelling entry point into a long-term compounding story.

UK-based property company SEGRO ( SEGXF ) has seen its stock price re-rate since I last covered the stock; while UK property data remains in decline, emerging recovery signs bode well for a better year ahead. While macro uncertainty remains and rates are set to remain higher for longer, SEGRO's strong balance sheet and relatively low leverage keep it well-positioned to withstand any further turbulence ahead. Supported by a robust development pipeline and accretive acquisitions in the fast-growing data center space, the company also stands to benefit from significant rental-driven upside potential in the coming years. With the stock still on offer at a ~30% book value discount, SEGRO's compounding potential remains undervalued, in my view.

Building out Data Center Presence via Accretive Acquisitions

Earlier this month, SEGRO announced the GBP120m acquisition of Bath Road Shopping Park from Royal London Asset Management. The acquired site covers ~11 acres, implying a valuation of ~GBP10.5m/acre, and boasts a vacancy rate of >30%, presenting ample optionality from a development perspective. Given the proximity to the Slough Trading Estate, one of the few availability zones for data centers in the UK, the acquisition likely marks another step in SEGRO's efforts to build out a more significant data center presence. I view this as a positive - data center demand has been strong in recent times and offers uniquely accretive development opportunities. For instance, the lack of rent differential across data center property floors allows for significantly increased land intensity via multi-level builds vs. other sources of demand.

At this stage, the lack of disclosures on the financing involved means gauging the post-deal accretion is challenging. While the acquisition will drive a higher net debt/equity ratio near term, the relatively small deal size means any change in the overall gearing won't be too material. Clearly, management is comfortable with its balance sheet capacity, and with interest coverage likely to ease as the macro headwinds subside, expect SEGRO to capitalize on the rate-driven valuation reset with more accretive development opportunities ahead. In particular, I would keep an eye on more acquisitions in the data center space - relative to the <10% contribution to overall rents, the company has ample runway to expand its exposure via more acquisitions and subsequent multi-level developments.

Green Shoots of Recovery

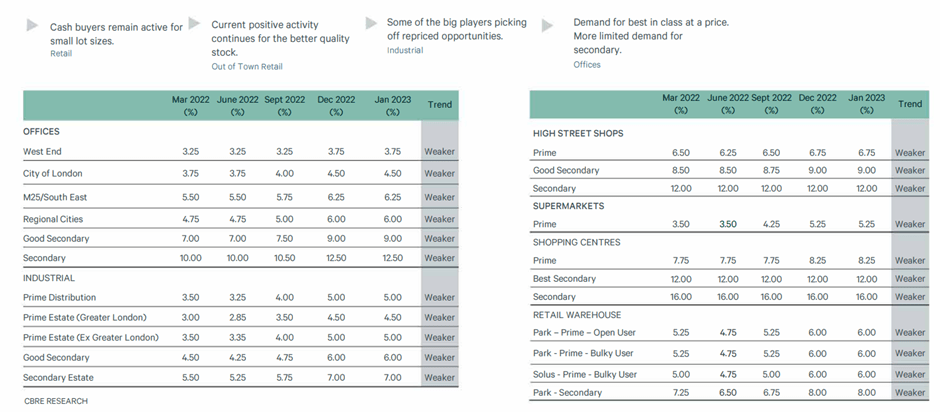

After a record month of weakness in October, UK real estate price data for November and December have seen more price declines amid higher interest rates. That said, the negative valuation and NAV implications are well-understood at this point, and the market has reacted accordingly, with SEGRO and its peers now trading well below book value (post-revaluation). The latest January data from CBRE, particularly relevant for SEGRO given the broker provides its UK and Europe valuations, indicated more of the same, with yield expansion on pause for now across asset types.

{kind=link}

That said, the yield sheet offered a glimmer of hope going forward, noting that the market is starting up for FY23 as major players begin to capitalize on repriced opportunities, particularly for industrial property. With central banks also set to slow down their pace of rate hikes, I expect a gradual recovery and yield expansion across SEGRO's high-quality portfolio through FY23.

Well-Capitalized Balance Sheet Offers Insulation from Rate Headwinds

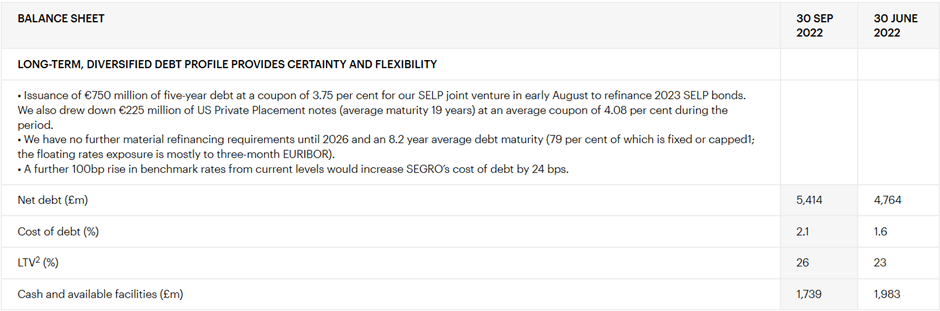

In the face of higher for longer rates and the risk for real estate valuations to further adjust downwards (although mid-term rate expectations seem to have softened, as proxied by the 10y gilts), investors will find shelter in SEGRO's balance sheet. While the company maintains a net debt position, its financial obligations are manageable. At a >30% net debt to equity and ~6x interest coverage (backed by a high-quality rental income stream), SEGRO has sufficient safety margin to weather a worst-case recession scenario.

Perhaps more importantly, the debt stack has been termed out at a ~9-year average debt maturity (well ahead of the sector), keeping the company well insulated from the ongoing rate hike cycle. Recent efforts indicate management's focus on preserving the balance sheet resilience - the November GBP350m debt issuance not only increased its average debt maturity but also raised the overall fixed debt exposure to 86% (from 79% prior). All in all, the strong fundamentals allow for a best-in-class ~2% all-in cost of debt and, by extension, value-accretive development activity through the cycles.

{kind=link}

A Quality Play on the UK Property Recovery

While SEGRO's re-rating in recent months has narrowed the book value discount, the thesis remains intact, in my view. With UK property prices showing signs of a recovery, the low-risk balance sheet offers investors a safer way to gain exposure while maintaining insulation against the worst of a potential recession in FY23. In addition, the strong development pipeline and the M&A capacity allow the company to expand into new growth areas, in turn supporting strong rent-driven upside potential over time. At a ~30% discount to book, the stock remains attractively priced relative to its quality fundamentals and earnings growth runway.

For further details see:

SEGRO: A Quality Play On The U.K. Property Recovery