SEGXF - SEGRO: Exiting The Penalty Box

2023-09-22 16:41:43 ET

Summary

- SEGRO has sold off alongside the rest of the European property.

- Yet, its high-quality portfolio and resilient balance sheet are shining through.

- With the stock now on offer at a steep discount to book, there’s plenty of value on offer.

A lot has changed since I last covered UK/EU-based property investment and development company SEGRO ( SEGXF ). Having initially been upbeat about its best-in-class European portfolios, spanning the office and industrial spaces (e.g., logistics, data centers, and warehouses), an extended rate hike cycle has penalized valuations across the board. On a relative basis, though, management deserves credit for limiting the damage, with the H1 portfolio correction markedly slowing after the deep contraction in H2 2022.

From here, diversification should continue to help - having built a quality platform across different sectors and ex-UK geographies, SEGRO is well-positioned to capitalize on secular rental demand growth. Also helping is the well-insulated balance sheet and continued rental pass-throughs, both of which underpinned another round of dividend hikes in the last half-year. Alongside rental income optionality from the land bank, SEGRO's current ~20% book value discount seems excessive, particularly with the UK/EU rate hike cycle finally at an end.

Ongoing Rental Uplifts Underpin Resilience Through the Downcycle

SEGRO kicked off the year strongly, with H1 adjusted earnings coming in at a resilient +1.9% YoY to 15.9p/share on the back of rental values matching overall inflation on an annual basis. At the group level, like-for-like net rental income growth was +5.1% YoY (+4.3% YoY in the UK; +6.4% YoY in Continental Europe), only slightly down from the +6.7% last year. Within the rental income component, rental uplifts were the key positive driver at +20% (+26% in the UK), helped by rent reviews and renewals, along with incremental contributions from completed developments. The fact that vacancy rates have been relatively low through this downcycle (only up ~50bps in H1 2023) also stands out, a testament to the high-quality platform SEGRO’s management has built through the years.

{kind=link}

SEGRO

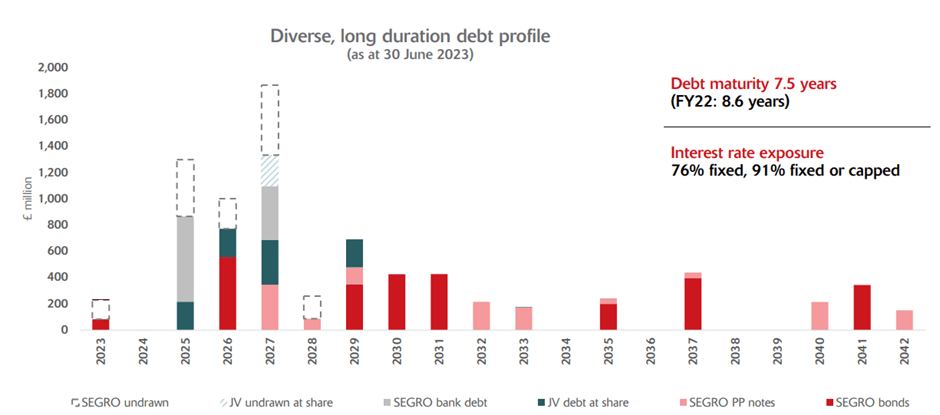

The main detractor from H1 earnings was higher funding costs, as reflected in the overall weighted average debt costs rising to 2.9% (up ~130bps from H1 last year). This isn’t all that surprising, given the pace of the UK/EU rate hike cycle and SEGRO’s rich growth pipeline, which still needs to be financed with more expensive new debt. The more pertinent thing here, in my view, is the well-insulated balance sheet, which has not only been termed out pre-tightening (no major maturities through 2025/2026) but also has limited variable rate exposure (91% fixed or capped). In turn, this gives the company headroom to shield its P&L from sharply higher financial expenses. For income investors, a strong balance sheet also means intact capital returns; the high-single-digits interim dividend hike to a 3-4% yield (at current prices) is a case in point.

{kind=link}

SEGRO

Portfolio Quality Stems the Valuation Decline

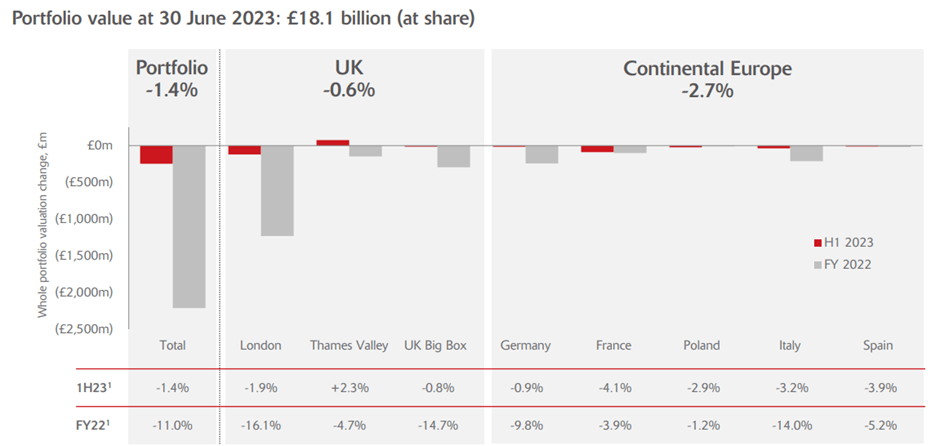

In line with the rest of the European property sector, SEGRO has seen its portfolio value decline through the rate hike cycle. But if H1 2023 was any indication, the headwinds are slowing – valuations were only down by 1.4% for the half-year (vs. a high-teens decline in H2 2022), with a stable UK (-0.6%) offsetting wider declines in Continental Europe (-2.7%) and keeping the overall portfolio value at GBP18.1bn. Relative to resilient market rental values (+3.7%) as well, the portfolio has seen an overall ~30bps yield expansion, taking the blended equivalent yield to 5.1%.

{kind=link}

SEGRO

As a result, the adjusted net asset value is down by a modest 3% to 937p/share as of H1 2023; at current market prices, this implies SEGRO stock is on offer at a steep ~20% discount to NAV. Given the company’s quality operating platform and established track record of capital recycling (mainly into new prime warehouse locations) via developments and acquisitions, this seems a step too far, in my view. Plus, inflation pressures are starting to ease across the UK/EU, and as central banks inch back on tightening, SEGRO’s attractive fundamentals should help the stock re-rate.

Robust Transaction Pipeline Offers Long-Term Optionality

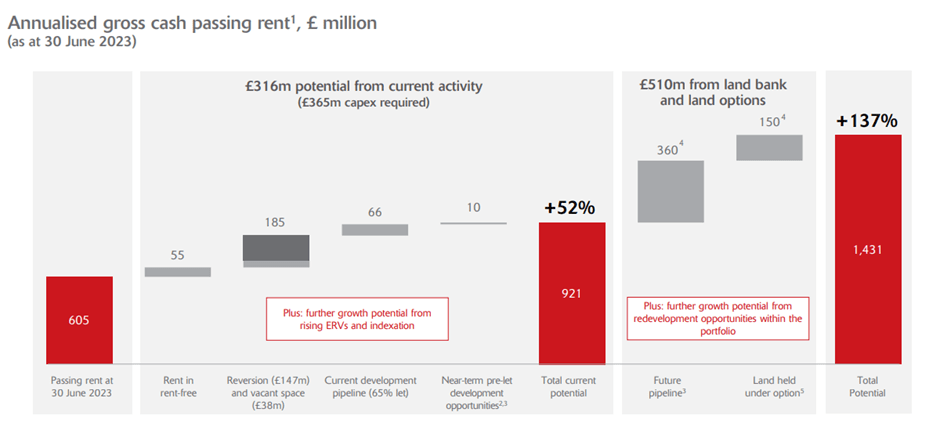

In addition to protecting its downside, SEGRO’s balance sheet advantage also gives it headroom to ramp up transaction activity amid cheaper valuations. The H1 report confirmed as much, with Q2 activity already improving on Q1 levels. Most of the outlay is understandably focused on acquisitions (GBP326m through H1), specifically ‘super prime’ land opportunities to boost the development pipeline. Also on the agenda are accelerated development completions (GBP299m allocated through H1) on the path to a GBP600m target for the full year. While activity here won’t hit the P&L anytime soon, plans to expand, develop, and monetize its extensive land bank underpin long-term earnings optionality (assuming management executes) that likely isn’t priced into the stock yet.

{kind=link}

SEGRO

Exiting the Penalty Box

European real estate has been a torrid place to be over the last year, but with the extended UK/EU monetary tightening reaching its conclusion, a long-overdue relief rally may be on the horizon for higher-quality names like SEGRO. As H1 2023 showed, the company has seen its assets revalued lower, though at a much slower -1.4% pace than its peers and vs. its own correction in the back half of last year. Unlike many of its peers, SEGRO’s portfolio skews further toward the prime end of the market; as this sector continues to benefit from rising rents, a key source of support for real estate value, the company has enjoyed relative outperformance.

Its biggest strength in the face of a higher for longer rate environment, though, is its rock-solid balance sheet (>90% of the debt stack is fixed), which, combined with the company’s credit rating, has limited much of the ongoing funding headwinds. From here, the prime industrial logistics-focused operating platform presents steady upside through the cycles, as occupier demand continues to gain traction across Europe. The development pipeline is nothing to scoff at either - SEGRO’s land bank and ability to recycle capital accretively mean there's significant long-term optionality on top of a 2-6%/year status quo rental growth trajectory. Few of these positives seem to be priced in at a discounted 0.8x P/B. As the cycle turns, however, expect SEGRO to re-rate; investors get a well-covered 3-4% yield in the meantime.

For further details see:

SEGRO: Exiting The Penalty Box