SIGI - Selective Insurance: Overcoming Market Disruptions Quite Overvalued But Still A Great Stock

Summary

- Selective Insurance Group, Inc. maintained a solid performance amidst market disruptions.

- Its stellar balance sheet is one of its cornerstones.

- Macroeconomic headwinds persist, but opportunities are present in the market.

- Dividend payments are constantly increasing, but yields are low.

- The stock price is moving sideways, but not cheap.

Selective Insurance Group, Inc. (SIGI) operates in a high-demand market. But given its location, operational risks are more present and intense. We saw how Hurricane Ian led to a substantial increase in claims. Despite this, the company proves it can withstand headwinds and disruptions. Revenue growth was impeccable, while margins remained stable. Even better, it maintains a stellar Balance Sheet. With that, SIGI can cover its operating capacity without increasing its financial leverage.

Meanwhile, dividend payments continue to increase while remaining well-covered. However, yields are unexciting, showing that SIGI stock price may be too high. This assumption can be logical, given the sharp stock price uptrend in 4Q 2022. Now, price metrics show that it is overvalued. But actual investor returns are consistent with company earnings.

Company Performance

The past two years have been challenging and disruptive for most industries. But for many companies in the financial sector, these have become a stepping stone to reaching more customers. The same was applicable to the insurance industry. The pandemic and increased frequency of natural calamities highlighted the importance of having insurance. Today, the P&C insurance industry is one of the primary components of climate finance. With that, we must see how companies coped with macroeconomic headwinds and natural disasters. It is a crucial factor for companies in the states along the Atlantic Coastline. And Selective Insurance Group, Inc. is one of them. Thankfully, it had a stable performance amidst the unprecedented events last year.

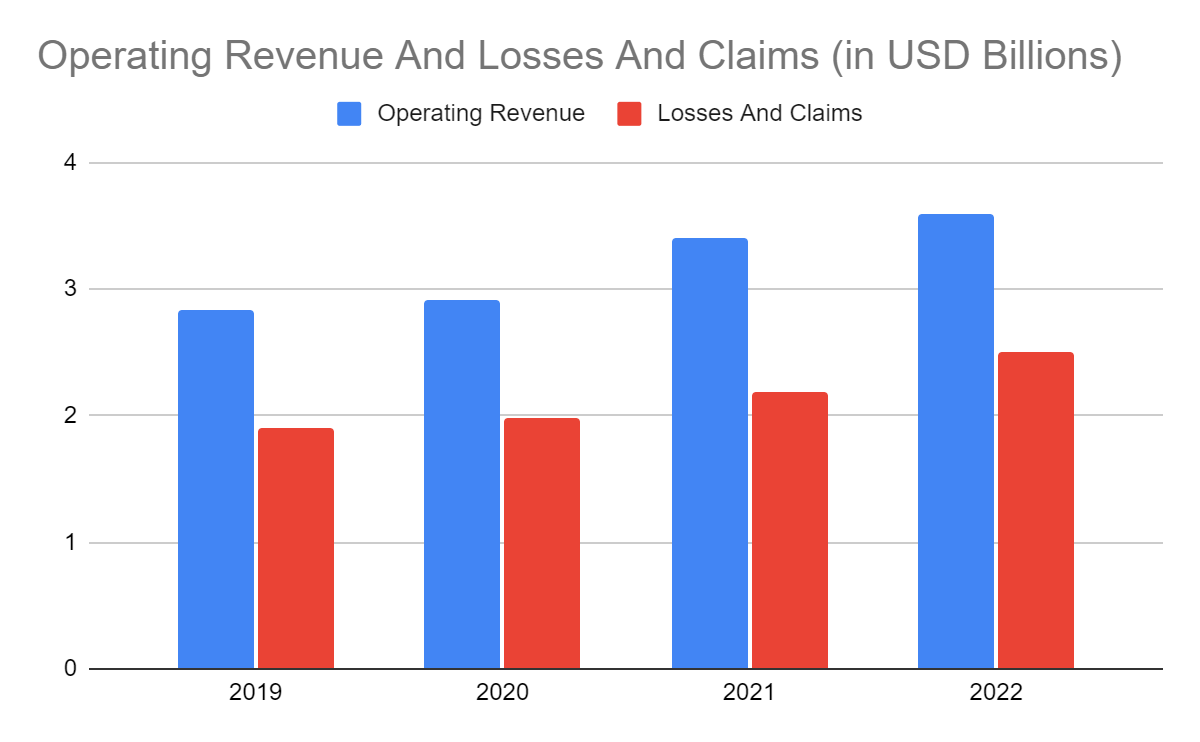

The operating revenue of the company amounted to $3.6 billion , a 6% year-over-year growth. During 4Q 2022, it amounted to $949 million, a 9% year-over-year growth. Indeed, the results proved its ability to navigate a volatile market. It is risky for this NJ-based company due to several natural calamities I will discuss later. We can attribute this decent revenue growth to several factors. First, it maintains an effective underwriting discipline. Its premium rate increases remained favorable for the company and policyholders. For example, its Standard Commercial Lines Segment had a 5.4% policy renewal pure price increases on net premiums written. It was a substantial yet acceptable growth rate compared to 5.3% in 2021.

Operating Revenue (MarketWatch)

{kind=link}

Operating Revenue (MarketWatch)

{kind=link}

Second, it has a solid customer base. Thanks to its strong distribution relations and efficient underwriting tools. This attribute allows the company to cater to policyholders with improved efficiency.

Third, its investment portfolio diversification remains prudent. It covers a wide range from mortgage-backed securities and corporate bonds to collateralized loans. But what I liked about its investments is that 20% are government-backed securities. These are more suitable in a high-interest environment due to their inflation-linked nature. It may have to improve its diversification by increasing its concentration on government securities. Doing so can help it generate more stable yields and lower valuation losses.

Its high concentration on commercial lines is helpful. Policy renewals are more fixed or stable since it negotiates with businesses. Also, these have lower risks than personal lines. Again, New Jersey is more exposed to natural calamities due to its location. Personal lines may incur more claims due to home structures. Potential abuses like roofing scams are more present in personal lines.

Likewise, claims and losses also rose dramatically in the last year. It was logical, given the Midwest weather in 2Q 2022 and Winter Storm Elliott in 4Q 2022. However, the massive bulk of claims happened in 3Q 2022 when Hurricane Ian struck the Atlantic Coast. Claims amounted to $651 million , an 8% increase from 3Q 2021. Other operating expenses also increased by 13% due to inflation. Given all these, they offset revenue growth, leading to a lower operating income. The operating margin dropped from 15% in 2021 to 10% in 2022. Despite this, we can see a substantial improvement in 4Q 2022. It was lower at 12% versus 15% in 4Q 2022 but higher than in 2Q at 8% and 3Q at 7%. Overall, Selective sustained its revenue growth while stabilizing claims and expenses amidst inflation and more frequent natural disasters. It remained viable, allowing it to sustain its operations without touching its cash reserves or increasing borrowings.

Operating Margin (MarketWatch)

{kind=link}

Operating Margin (MarketWatch)

{kind=link}

This year, I expect challenges to persist, mainly due to inflation. Although it continues to relax, it may take some time for individuals and companies to adjust. But I am optimistic about Selective Insurance Group, Inc. Revenues and expenses may be affected but will still fare well. Selective may capitalize on its flexible insurance rates. Today, it is one of the cheapest home and auto insurance providers. Its home insurance rate is only $519 , way lower than the NJ and National average of $942 and $1,784. Meanwhile, its car insurance is $1,800-2,900 , depending on the coverage and age of the vehicle. It is way cheaper than the state average of $2,809. With that, Selective has more room to adjust its prices to stabilize its premiums and policy retention.

How Selective Insurance Group May Fare This Year

The P&C insurance industry may still fare well this year. But market prospects are less robust than in 2021-2022. It is logical amidst moderating demand and macroeconomic headwinds. Some expectations from industry analysts are higher reinsurance costs and M&A slowdowns. I adhere to the near-term impact of inflationary headwinds. But insurance companies may cope with it in the second half. Today, inflation is only 6.4% , 29% lower than the 2022 peak.

Also, property value continues to appreciate despite the cooling sales and prices. I disagree with suppositions of a recession and a real estate market crash. After all, industry trends these days are way different from the Great Recession. Property inventory levels remain low, which we can attribute to builders not ramping up over the past decade. Even better, the labor market conditions are manageable. No speculative mania and unethical borrowing and lending can be seen in the market. Given all these, the real estate market may still be stable. In turn, P&C insurance may remain a staple for commercial and residential property owners.

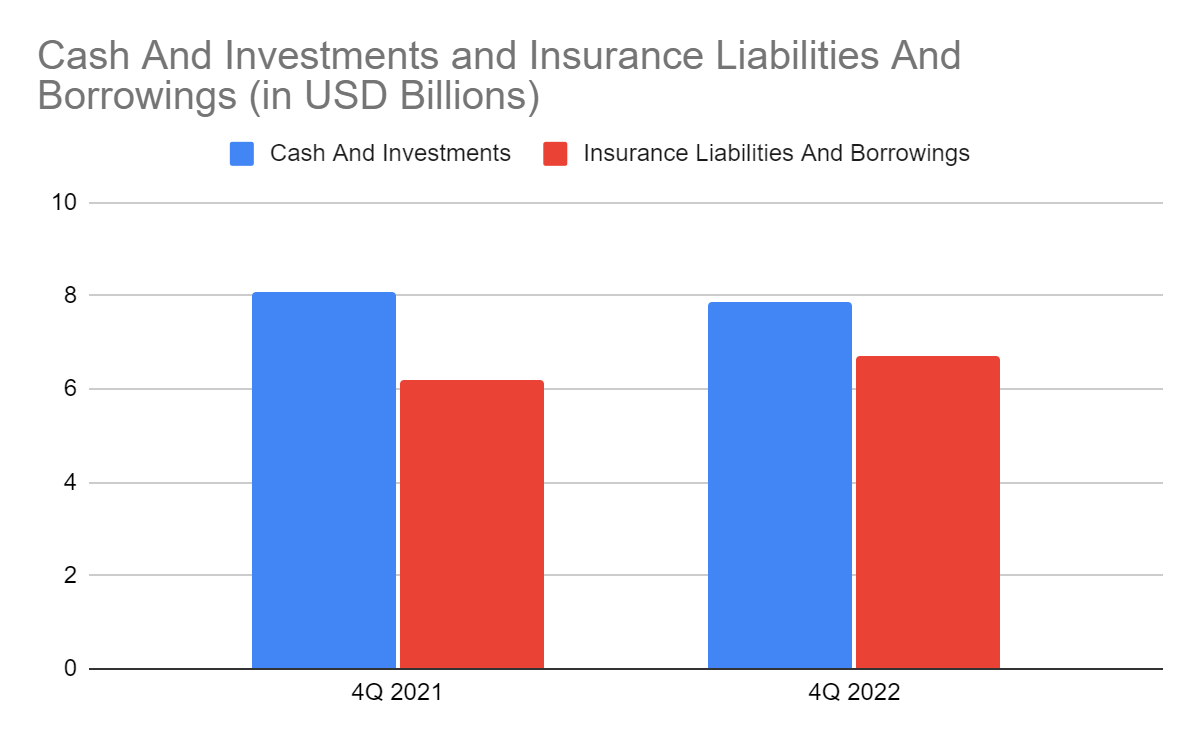

What makes Selective Insurance Group, Inc. a solid company is its stellar Balance Sheet. It has adequate liquid assets to cover its insurance liabilities and borrowings. As such, it can sustain its capacity without increasing its borrowings. Cash levels are rebounding after compensating for claims in 3Q 2022. Also, the Net Debt/EBITDA Ratio of 1.42x shows that SIGI earns enough to pay borrowings. We can confirm its impressive liquidity with its FCF/Sales Ratio of 22%. Hence, SIGI maintains the consistency between its viability and liquidity.

Cash And Investments And Insurance Liabilities And Borrowings (MarketWatch)

{kind=link}

Stock Price Assessment

The stock price of Selective Insurance Group, Inc. has been in a sustained uptrend in the last three years. But it has become sharper in the last year. At $100, the stock price is already 22% higher than last year’s value. With this massive increase, the stock price appears to have already exceeded its intrinsic value. The PB Ratio shows that the current BVPS of 41.89 gives a ratio of 2.24x. It is higher than the average of 2.12x. If we multiply the current BVPS by the average PB Ratio, the target price will be $88.8. Despite this, the EV Model disagrees with it, given the target price of ($6.80 B EV - $0.54 B Net Debt) / 60,340,000 shares = $103.41.

Meanwhile, dividend payments of the company are increasing. But dividend yields are only 1.17%, the same as the S&P 400 average but lower than the NASDAQ average of 1.43%. These remain well-covered since the dividend payout ratio is 32%. To assess the stock price better, we will use the DCF Model.

FCFF $283,000,000

Cash $25,200,000

Borrowings $549,000,000

Perpetual Growth Rate 4.8%

WACC 9.9%

Common Shares Outstanding 60,340,000

Stock Price $100

Derived Value $98.02

The derived value adheres to the potential overvaluation of the stock price. There may be a 2% downside in the next 12-18 months. So, investors may have to rethink their plans for buying shares. But I like its reasonable investor returns over the years. We can compare the cumulative retained earnings of $14.62 to the 2019-2022 price change of $15.16. It shows that for every $1 increase in retained earnings, the stock price increased by $1.04. The actual investor returns using these two figures show that the company remains an earning stock.

Bottom Line

Selective Insurance Group, Inc. should still be considered a durable P&C insurance company. It maintains stable revenue growth and margins amidst the volatile market. Also, its stellar Balance Sheet shows it can sustain its capacity and borrowings without raising its financial leverage. Moreover, dividends keep increasing despite the low yields. Meanwhile, the stock price appears overvalued for the intrinsic value of the company. But it is still a promising stock, given its continued uptrend and ideal investor returns. The recommendation, for now, is that Selective Insurance Group, Inc. is a hold.

For further details see:

Selective Insurance: Overcoming Market Disruptions, Quite Overvalued But Still A Great Stock