UMH - Sell Alert: 2 REITs Getting Risky

2024-01-16 08:05:00 ET

Summary

- I am very bullish on most REITs following their recent crash.

- But not all REITs are worth buying.

- Here are two risky REITs that I would consider selling.

I have about 50% of my portfolio invested in REITs ( VNQ ).

So needless to say I am very bullish on REITs. Many of you would probably describe me as a "cheerleader for REITs".

But you will note that I regularly also write articles on REITs that I would sell.

While I am bullish on the sector as a whole, I am still objective enough to recognize that not all glitter is gold, and there are lots of REITs that aren't worthy of your dollars.

In what follows, I will highlight two REITs that I would consider selling if I owned them today:

Easterly Government Properties ( DEA )

DEA is a REIT that owns mostly single-tenant office buildings, and this is the single worst property sector in my opinion.

Already in my private equity days, we would avoid these assets.

They commonly offer a nice cap rate and long lease term, but once the lease is over, the risk of value destruction is very significant. The tenant knows that if they move out, it would be a nightmare for the landlord to release the building. It would lead to significant remodeling costs, leasing expenses, holding costs, and in some cases, releasing the property may not even be possible, causing the asset to turn into a liability.

This is especially true in the post-pandemic world.

Before the pandemic, tenants would sign long leases for these large single-tenant office buildings, thinking that their needs for office space wouldn't change drastically for a long time to come.

But their needs changed with the pandemic. To this day, the physical occupancy of office buildings is still stagnating at 50%, and it is likely even lower for these older single-tenant office buildings that are stuck in long-term leases. People have switched to working remotely at least a few days each week and as a result, there is no need for so much office space anymore.

This puts all single-tenant office buildings at significant risk of vacancy and the cost of remodeling and releasing the building may often exceed the current value of the equity.

Add to that the recent surge in interest rates, and a tighter lending environment for offices, and you have a perfect recipe for disaster.

As a result, valuations for these assets are crashing down, and the Twitter profile "Triple Net Investor" has done a great job documenting this value destruction with recent market transactions.

Here are two recent examples:

A 339k sq ft office tower in the Washington DC area (Bethesda) just sold for $30 million or $88 per SF The seller acquired the building for $134 million in 2019, taking a ~80% haircut in 4 yrs. But this isn't the worst of it... The seller also spent $21 million renovating the building during their ownership. It will be interesting to see how much worse the US office meltdown gets but it's certainly one of the biggest stories to keep an eye on in 2024.

X - Triple Net Investor

A 195k sq ft office complex in Fairfax Virginia just sold for $9.5 million or $48 sq ft. The seller acquired it in 2020 for $31 million, taking a massive 70% loss. But this isn't the end of the story. The seller also spent millions renovating the building during their ownership so the 'discount' is meaningfully higher than 70%. The timing of the seller's purchase in 2020 could not have been any worse...

X - Triple Net Investor

This recently pushed Office Properties Income Trust ( OPI ) to almost fully eliminate its dividend, and other REITs that own similar properties ( ONL , NLOP , etc.) have all crashed in value and trade at just 3-5x their FFO:

DEA is the exception.

It has not dropped nearly as much and as a result, it continues to trade at a relatively high 12x FFO.

| Single tenant office REITs |

| DEA |

| FFO Multiple |

| 3-5x |

| 11.85x |

The reason why it has been so much more resilient is that it focuses mainly on single-tenant office buildings that are leased to government agencies.

The market appears to think that this will protect DEA from the risks that we mentioned earlier, but I strongly disagree.

A recent study showed that the physical occupancy rate of office buildings leased to government agencies is even lower than that of corporate tenants at just around 25% in many cases.

This is likely because government agencies may not care as much about the productivity of their workers as for-profit companies, but they still care about the cost, especially as budgets get squeezed.

The issue for DEA is that government tenants hold even greater bargaining power than corporate tenants at the time of lease renewals. That's because they know that if they vacate the property, the result would be devastating to the landlord. Often, the properties may have been built specifically for the government agency with some unique characteristics. This means that in case of a vacancy, the remodeling and leasing costs would be very significant. Moreover, properties leased to government agencies tend to trade at lower cap rates, meaning that even if they managed to release the property to a company, it would now trade at a higher cap rate, resulting in a lower valuation.

This puts DEA in a very tough spot.

As leases gradually expire, these government agencies will hold all the cards. Their needs have changed and they know that there are plenty of office buildings that are now sitting vacant and a lot of landlords would gladly inject significant capital to redevelop their properties if that allowed them to secure them as a tenant.

At best, DEA will need to heavily reinvest in its properties. At worst, it will deal with significant vacancies. The base case scenario is likely a mix of the two.

That puts the company's dividend at risk given that the payout ratio is already very high and leaves no room for error. That's a big problem because most shareholders of the company own it for the dividend.

Just recently, OPI cuts its dividend, and its share price crashed by ~40% in a single day:

I think that paying 12x for DEA is too much when you consider these risks and for this reason, I have no interest in owning it today.

UMH Properties ( UMH )

UMH is a very different story.

The REIT owns assets that I like. It owns mostly manufactured housing communities, and most of them are performing very well:

UMH Properties

However, the problem that I have with UMH is its capital allocation strategy.

The REIT has massively underperformed its close peers, Sun Communities ( SUI ) and Equity LifeStyle ( ELS ) over the long run, and that's despite taking more risks by using greater leverage and following a riskier value-add strategy:

Why has it done so much worse for its shareholders?

I think that the management is not giving enough consideration to its cost of capital when making new investments, and this has diluted its performance on a per-share basis.

They will commonly issue new common equity at a large discount to their net asset value, as well as preferred equity with a high yield to make new investments, but the returns of these investments often won't cover the cost of capital in year 1, resulting in dilution.

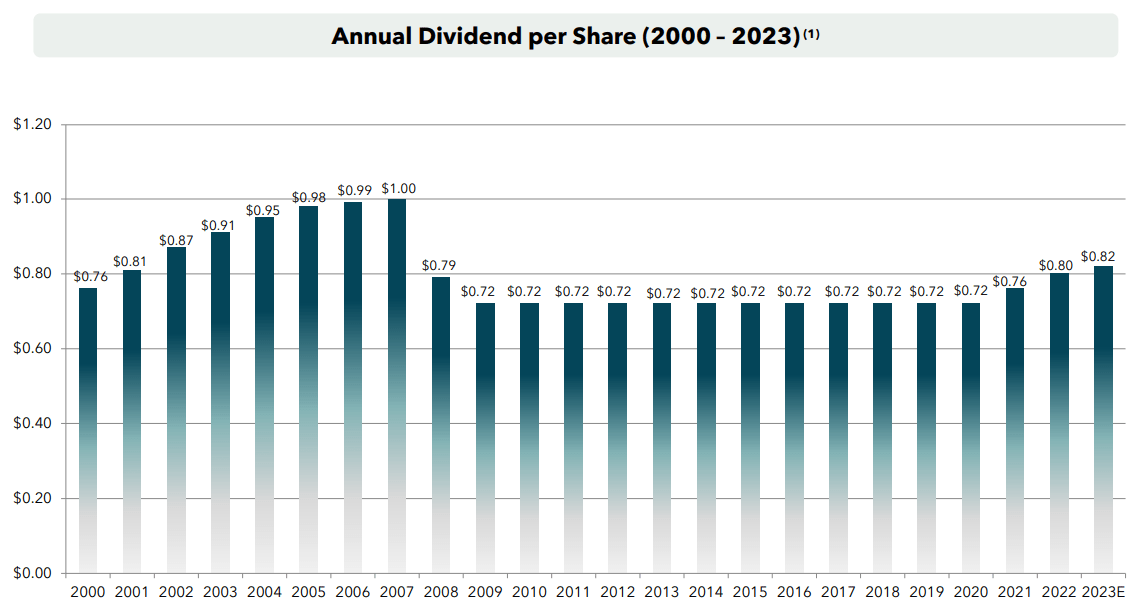

The management asserts that the dilution will turn into accretion down the line, but their track record of dividend growth on a per-share basis tells a different story.

Their dividend per share is today still smaller than 20 years ago and that's despite significant rent growth since then:

{kind=link}

UMH Properties

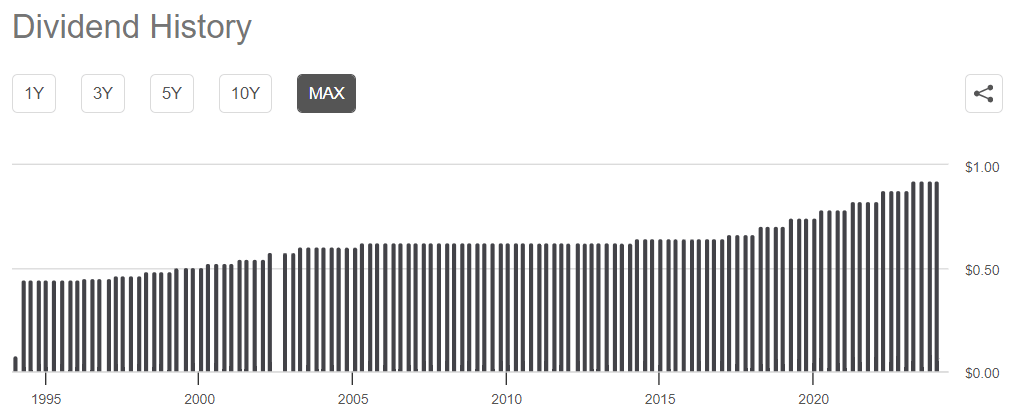

Now compare that to the dividend growth of its close peer, SUI:

{kind=link}

Seeking Alpha

UMH has previously also invested in the shares of other REITs and those investments have been rather disappointing. I don't really care about the performance of these securities because they are a minor part of the portfolio, but I care about the signal that this sends to the market.

The market does not want REITs to start playing the role of a hedge fund manager and therefore, these investments are likely to hurt UMH's market sentiment and cost of capital. I suspect that if the REIT just sold all its securities and reinvested the proceeds into more manufactured housing communities, the market would reward UMH with a higher valuation. Yet, they refuse to do so, possibly because they don't want to admit that buying these securities was a mistake in the first place.

Finally, I would point out that they have a slide on their investor deck that's meant to show investors that their common equity is deeply undervalued relative to private market valuations. But despite that, they keep issuing more shares at these levels:

{kind=link}

UMH Properties

I cannot make sense of that. If your equity is truly discounted, then you probably should consider buying back shares. You sure shouldn't be issuing more of them.

I just don't trust the capital allocation skills of the management and for this reason, I have no interest in owning UMH. We used to own a position for many years, but we finally threw in the towel and reallocated into SUI in late 2023. I am not bearish on UMH, but there are better options out there in my opinion.

Closing Note

REIT valuations are low today, but that does not mean that all REITs are worth buying.

Some own assets that are struggling.

Others are overleveraged.

And some are mismanaged.

Therefore, it is very important to be selective when investing in REITs.

For further details see:

Sell Alert: 2 REITs Getting Risky