LANDO - Sell Alert: 2 REITs To Sell Before 2023

Summary

- I invest 50% of my net worth in REITs.

- But not all REITs are worth buying.

- I highlight two REITs that I wouldn't buy today.

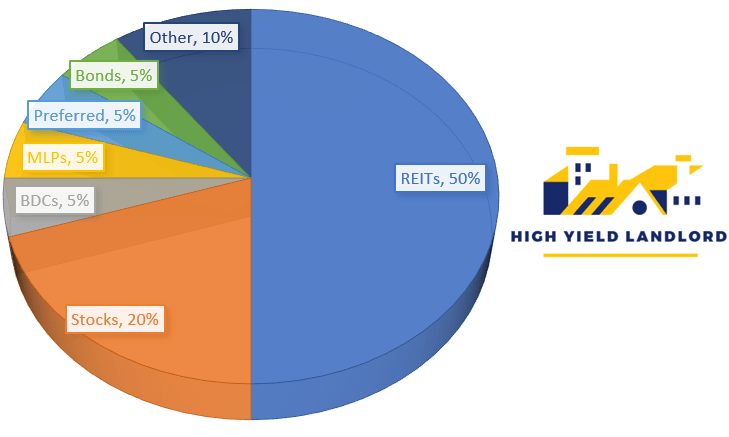

I invest about 50% of my portfolio in REITs, so needless to say I am very bullish on them.

{kind=link}

I invest so heavily in them because there are lots of REITs that are heavily discounted following the recent market correction and they essentially allow you to buy real estate at 50 cents on the dollar.

To give you an example: BSR REIT ( OTCPK:BSRTF )'s latest net asset value per share is $22.35, but you can buy its shares today at just $13. This may lead you to think that there must be something wrong with BSR, but that isn't the case, and there are surprisingly many such opportunities in the REIT market right now. Off the top of my head: Mid-America ( MAA ), Simon Property ( SPG ), and SL Green ( SLG )... all trade at historically large discounts to their net asset values:

But just because most REITs are discounted does not mean that all of them are. In fact, there are quite a few REITs that still remain expensive even after the recent market correction, and that's why it is very important to be selective.

In what follows, we highlight two REITs that we wouldn't buy because they continue to trade at high valuations:

Gladstone Land ( LAND )

I am a big fan of farmland investments. I explain why in a recent article entitled " Billionaire investors buy farmland and you should too ":

Farmland Partners

But unfortunately, there are only two farmland REITs out there and those are Farmland Partners ( FPI ) and Gladstone Land ( LAND ).

LAND is the most popular of the two because it pays a higher dividend yield:

But REIT investors often forget that the dividend yield itself says nothing about the valuation.

The dividend is just a capital allocation decision and a higher yield is not necessarily the result of a low valuation. It may simply be the result of a higher payout ratio, more leverage, or investments in higher-cap properties that enjoy lower growth potential.

And that's the case here as well.

LAND's latest net asset value is $16.56, but it currently trades at $19, which means that you are paying a 20% premium to its net asset value.

In comparison, FPI's latest net asset value per share is estimated to be $16, but it trades at just $12 at the moment, representing a 20% discount.

This implies that FPI is a lower-quality REIT but we think that it is actually the opposite.

Gladstone Land is externally managed, which results in greater conflicts of interest.

It also owns mainly permanent / specialty crop farmland, which comes at a higher yield, but enjoys lower growth potential.

Finally, unlike FPI, it does not have additional businesses like asset management and brokerage services.

So all in all, we think that LAND is a lower quality REIT but it is today priced at a higher valuation, and for this reason, we are not interested in buying it.

FPI has better assets with faster growth prospects, a better-aligned management team, and it is also developing other capital-light businesses with high growth potential, and yet, it is priced at a materially lower valuation.

Public Storage ( PSA )

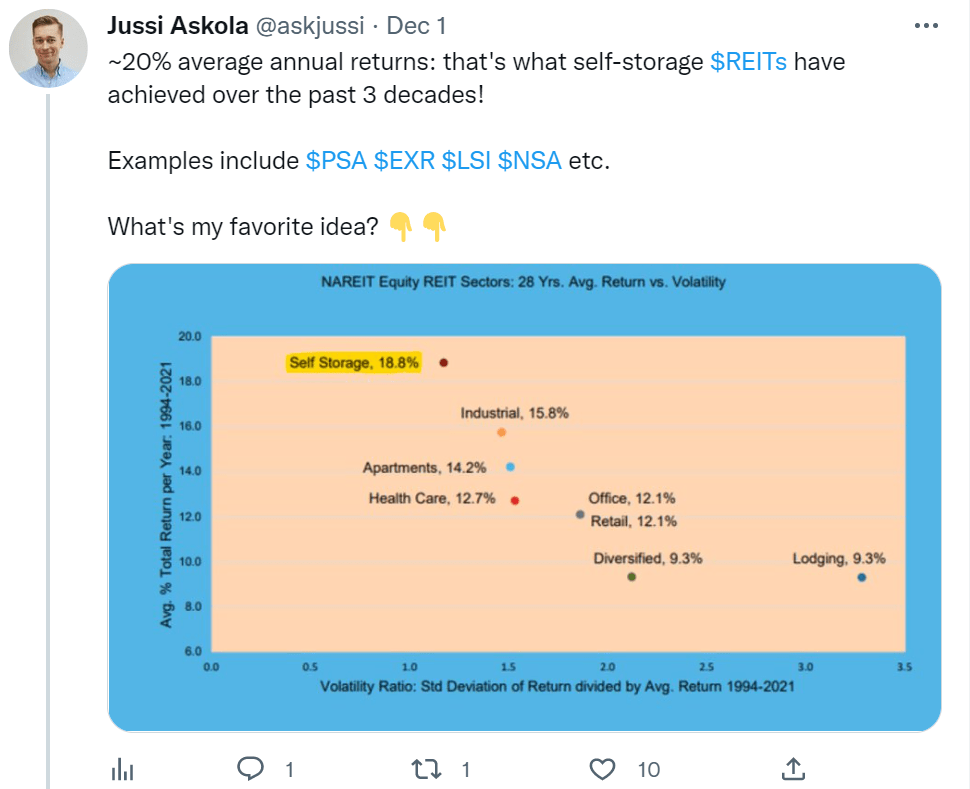

Self-storage REITs have been one of the best-performing asset classes of all time:

{kind=link}

And yet, we are not buying any of the US self-storage REITs.

Public Storage ( PSA ) is the leader in the space, it has a fantastic track record and an A-rated balance sheet.

So why aren't we buying it?

We fear that the past returns of the self-storage sector are a poor indicator of their future potential.

Public Storage

Today, the self-storage space is very competitive with many large REITs including ExtraSpace ( EXR ) CubeSmart ( CUBE ), Life Storage ( LSI ), and lots of private sophisticated owners. As a result, there is a lot of competition for properties, and cap rates have compressed. The management of these properties has also become a lot more professional and so most new acquisitions have less value-add potential than in the past.

Moreover, developers have witnessed the large returns of the past decade and built new properties on every busy street corner. As a result, most external growth opportunities appear to have been exhausted in the US as there is now 10 square feet of storage space for every person, compared to just 1 in the UK for example.

This is happening just as people are increasingly favoring experiences over things, and the sharing economy makes it more efficient for people to rent than buy things.

Finally, I also fear that some of the gains of the pandemic were just temporary. The pandemic caused a lot of people to move around, and a lot of older people to die, and it also led to a surge in sales of things like RVs and boats. All these things led to a surge in demand for storage space and since it takes time for new supply to hit the market, self-storage owners were able to rapidly bump up rental rates.

But are those new rental rates sustainable? How will they be affected by a new wave of supply hitting the market?

PSA is priced for the rapid growth to continue but I am not so sure that it will and for this reason, I would stay away.

If you want to invest in self-storage, there are better opportunities abroad at the moment. My favorite is Big Yellow ( OTCPK:BYLOF ). It is the leader in the UK, where the self-storage concept is still relatively new and opportunities are abundant.

It has great assets, a large pipeline, and access to cheap capital. It is still just getting started and already has a strong track record:

Big Yellow

I think that it is set to replicate the success of US self-storage REITs over the decades ahead and offers far better risk-to-reward than PSA at today's valuations.

Bottom Line

Not all REITs are equally attractive.

I aim to buy solid high cash-flowing REITs at large discounts to their net asset value because this allows me to earn income all while I patiently wait for long-term upside. I also believe that it reduces risks because the lower valuation provides a margin of safety.

This explains why I am not buying LAND or PSA, for example. There are better opportunities out there.

For further details see:

Sell Alert: 2 REITs To Sell Before 2023