ILPT - Sell Alert: 3 REITs That Likely Will Cut Their Dividends

Summary

- A few real estate investment trusts cut their dividends recently.

- I think that we will see a few more dividend cuts in 2023.

- I highlight 3 REITs that will likely cut their dividends and present some red flags to watch out for.

There have been quite a few real estate investment trust ("REIT") dividend cuts lately.

Just to give you a few examples:

Broadmark Realty Capital Inc. ( BRMK ) halved its dividend in November 2022.

Then SL Green Realty Corp. ( SLG ) also cut its dividend by 13% in December 2022.

And finally, the most recent cut came from Gladstone Commercial ( GOOD ), which broke its near-20-year track record of dividend growth as it cut its dividend by 20%.

Here's how these three dividend cutters have performed over the past year:

Understandably, this has led a lot of REIT investors to wonder:

When are my REITs going to cut their dividend as well...

Is this a sector-wide issue? Or are these isolated cases?

And if so, who are the next in-line to cut their dividend?

To answer these questions, we need to first understand why these REITs cut their dividends in the first place:

BRMK's dividend cut wasn't really a surprise to anyone. It had long overpaid what it really earned, and its fundamentals have recently gotten worse as more of its borrowers defaulted on their loans.

SLG's cut came more as a surprise because it had actually hiked its dividend in 2021 and the commentary of the management had been mostly positive. But even here, the cut is quite understandable when you consider that SLG is an office REIT that's mainly invested in NYC. Its market is the worst impacted by the shift to hybrid/remote work and it needs to preserve liquidity to pay off debt.

Finally, GOOD had also been overpaying its earnings potential, and it happens to own a lot of single-tenant office buildings, which will likely suffer significant pain in the coming years as leases expire and tenants move out or demand rent cuts/tenant improvements.

So in all three cases, it appears that the REITs were overpaying and had to cut because their underlying assets were suffering and/or they had to retain liquidity to pay off debt.

Is this a broad issue in the REIT sector?

The short answer is no.

REIT cash flows rose significantly in 2022 because most property sectors are performing very well:

{kind=link}

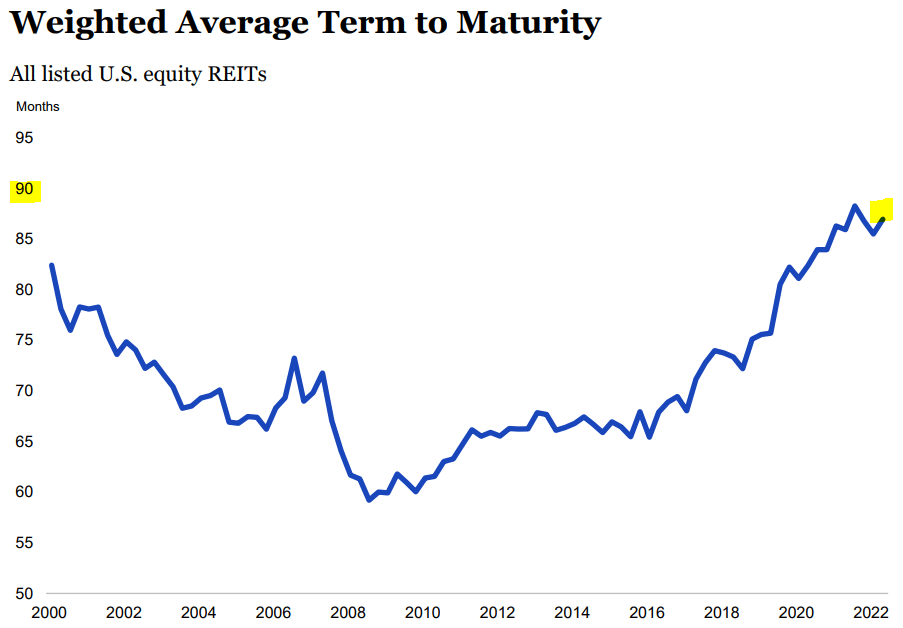

REIT balance sheets are also the strongest they have ever been, with low debt and long debt maturities, so the impact of rising interest rates is not significant:

NAREIT

And finally, REIT payout ratios are also historically low at around 75%, so we can confidently say that REITs aren't overpaying in most cases:

{kind=link}

Therefore, I think that these dividend cuts were isolated cases. The vast majority of REITs actually hiked their dividend in 2022. Just to give you a few examples:

- EastGroup Properties ( EGP ) hiked its dividend by 13.6%.

- Farmland Partners ( FPI ) hiked its dividend by 20%.

- UMH Properties ( UMH ) just hiked its dividend by another 2.5% this week.

- Simon Property Group ( SPG ) also hiked it by 3% in late 2022...

But despite that, I expect a number of REITs to still cut their dividend in 2023. It is important to remember that the REIT market is vast and versatile with over 200 companies and lots of different property sectors.

How do you identify those that are the most likely to cut their dividend?

I believe that there are three primary red flags to look for:

Red flag #1: the management quality

This is perhaps the most important. Lots of REITs that are poorly managed will overpay their dividend in an attempt to lure in unsophisticated investors with their highly enticing dividend yield.

But this almost never works out in the long run.

I would avoid most REITs that are externally managed because the external management structure creates a lot of conflicts. I discuss this topic in a recent video on YouTube.

A good example to avoid today would be Global Net Lease ( GNL ). It offers a mouth-watering 11.5% dividend yield, but the payout ratio is too high at 93% and leaves no room for error. The company has cut its dividend in the past, and I think that it is very likely that it will cut it again in the near future.

Red flag #2: the balance sheet

Most REIT balance sheets are strong today.

But some individual REITs played with fire ahead and they are paying the consequences. The best example is Industrial Logistics Properties Trust ( ILPT ), which took on significant debt to close a big acquisition in 2021, just to eliminate its dividend shortly after. It is at risk of bankruptcy.

Another example that hasn't cut its dividend just yet is Necessity Retail REIT ( RTL ). It offers a 13% dividend yield but it has a 55% LTV, which is quite high in today's environment for retail real estate. Its payout ratio is also quite high at 88%, leaving little cash flow to pay back debt. I think that a dividend cut is very likely.

Red flag #3: the underlying asset class

Finally, not all property types are created equal.

Today, office buildings are suffering great pain from the growth of hybrid/remote work, and this pain will only get worse if we enter a recession.

Another property sector that I am avoiding is outlet centers. I fear that the growth of Amazon ( AMZN ) and T.J. Maxx ( TJX ) pose a big risk to them because they are typically located in more remote areas, focus mainly on fashion, and their layouts are difficult to adapt to non-retail uses.

Tanger Outlet ( SKT ) is the only REIT that specializes in this sector, and its payout ratio appears low at right around 50%, but this is based on funds from operations ("FFO"), which does not take capex into account. If, like me, you think that outlets will suffer in the coming years, then SKT will be forced to reinvest heavily in its properties, and this could trigger a dividend cut. CBL ( CBL ), Pennsylvania REIT ( PRET ), and other mall REITs were in a similar situation years back. Their payout ratios were low, and most investors (including myself!) thought that their dividend was sustainable. But we greatly underestimated the need to reinvest in capex, and this forced them to eventually cut their dividend.

I discuss this topic in more detail in this video.

Bottom Line

Overall, it is unlikely that we see a large wave of REIT dividend cuts. Cash flows are rising, balance sheets are strong, payout ratios are low... and so I would actually expect a lot more dividend hikes than cuts in the coming years.

However, there are exceptions. Some property sectors are suffering. Some REITs are poorly managed. And others are overleveraged.

If you can steer clear of those REITs, you will save yourself a lot of headaches and increase your chances of outperforming the REIT market indexes ( VNQ ).

For further details see:

Sell Alert: 3 REITs That Likely Will Cut Their Dividends