MPW - Sell Medical Properties Trust And Buy These 10%-Yielding Blue Chips Instead

2023-11-22 07:15:00 ET

Summary

- Medical Properties Trust, Inc.'s fundamentals continue to deteriorate, with rising risk of a dividend cut and bankruptcy risk.

- If interest rates return to record low rates, its interest costs will double in the coming years. Medical Properties Trust might have to refinance at 3X higher interest if they don't.

- The risk of another dividend cut is approximately 17%, the same as the risk of the stock going to zero.

- That's about 15 times higher risk than these 10% yielding sleep well at night blue chips.

- We look at blue chips whose current dividends alone are enough to likely outperform Medical Properties Trust, whose growth outlook has collapsed to -5% annual growth.

A few of our members asked for an update on Medical Properties Trust, Inc. ( MPW ), which slashed its dividend by 50% on August 21st.

For several months prior to that, starting in March with the S&P downgrade from BBB- to BB+, we'd been downgrading MPW's fundamental dividend safety as the wheels steadily came off the bus.

Not one but two of its largest tenants, representing 38% of adjusted funds from operations, or AFFO, ran into trouble, and in a rising rate environment, its interest costs soared.

{kind=link}

The fundamentals kept falling, and our Investing Group kept on hacking away at MPW's fundamental safety and quality score.

{kind=link}

However, to use MPW as a teachable moment, let's quickly examine what's happened since the dividend cut and why investors should stay clear of this low-quality, speculative yield trap.

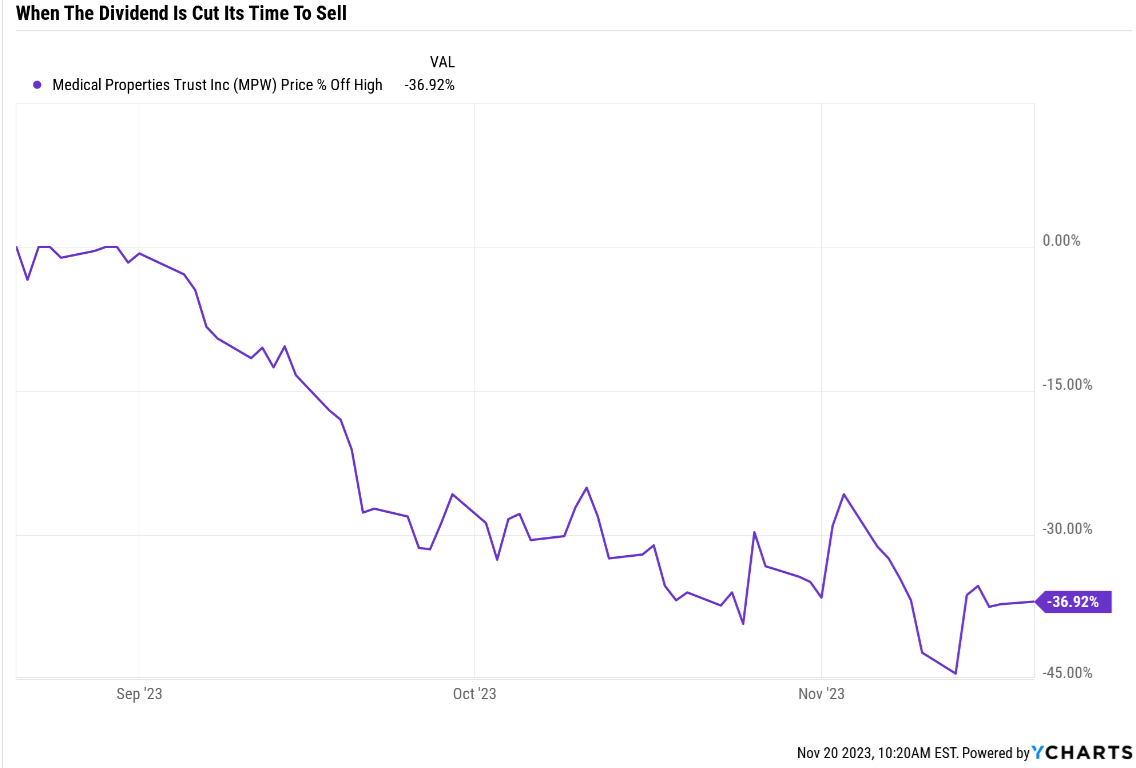

When The Dividend Is Cut Its Time To Sell

I keep making this point because nothing is absolute, and there are always examples of a dividend cutter that soared to new heights.

- Occidental Petroleum (OXY) in the Pandemic cut, and it's now Buffett's favorite oil company

- All but 17 real estate investment trusts, or REITs, cut their dividends in the Great Recession.

But while exceptions are always available for any rule, the prudent long-term investor, like a champion poker player, goes with the math.

{kind=link}

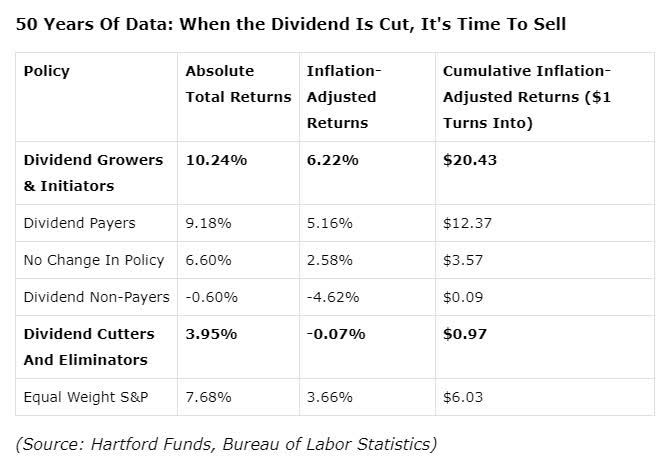

50 years with zero returns, absolutely horrific.

Here is why I use dividends as my canary in the coal mine.

{kind=link}

Note how the average dividend cut in recessions outside of the Great Recession was just 0.5%.

U.S. companies don't cut their dividends until absolutely necessary.

REITs and other high-yield sectors like utilities or midstream are even more so.

As I like to say, stock price is vanity, cash flow is sanity, and dividends are reality.

Here's why pulling the chute on a broken company is so important.

{kind=link}

Usually, if a stock falls 70+%, there is a roughly 50% chance it will never, ever, ever return to a new record high.

{kind=link}

General Electric (GE) cut its dividend, on an annual basis, five times on the road to a 65% inflation-adjusted loss over 23 years.

How about another famous broken aristocrat, Lumen Technologies (LUMN), formerly CenturyLink? They not only cut their dividend several times, they eliminated it entirely.

{kind=link}

How about V.F. Corp (VFC)? A 52-year streak dividend king that broke?

{kind=link}

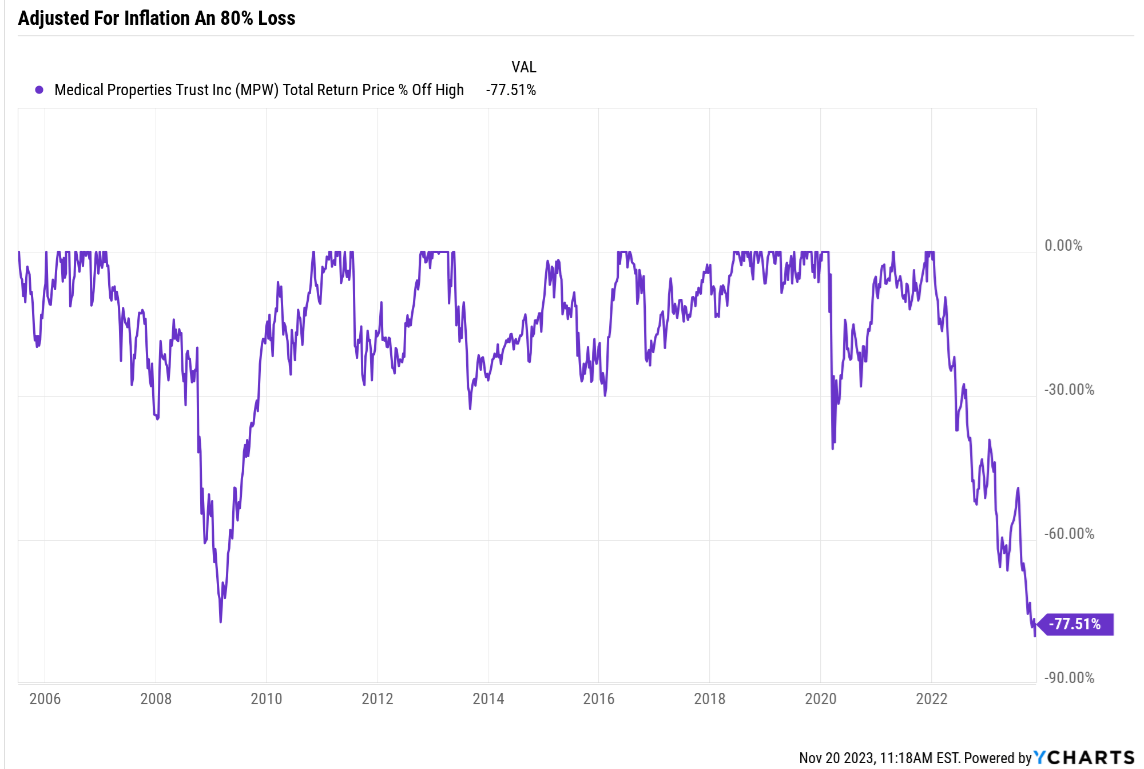

So, what does MPW look like?

{kind=link}

OK, so the charts are ugly, but isn't MPW cheap?

Cheap For A Reason

{kind=link}

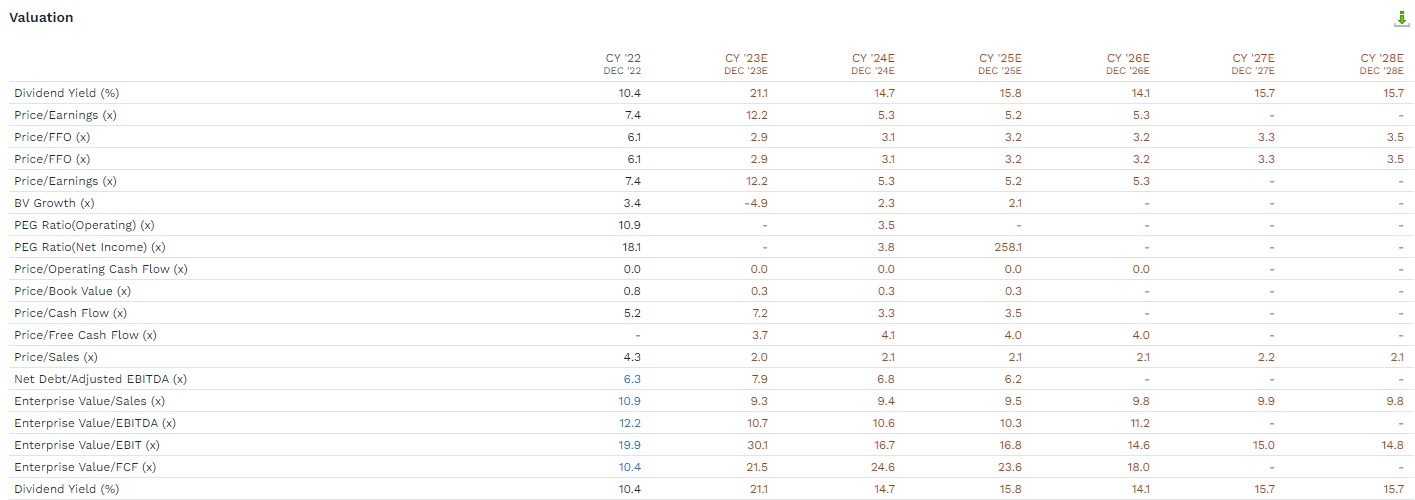

Whether you're looking at the 13% yield or the 3X FFO or 4X AFFO, MPW is cheap, cheap, cheap.

And here's why.

{kind=link}

AFFO is the REIT equivalent of free cash flow. Look at the trend.

2022: $1.92 and $1.92 dividend

2024: $1.58 and $0.92 dividend

2028: $1.37 and $0.99 dividend.

So, another dividend cut (our model agrees) and -5.5% annual growth in AFFO through 2028 is expected.

What about after 2028?

{kind=link}

A month ago that growth outlook was -3.2% and now it's approaching -5%.

And the balance sheet ?

Balance Sheet Is A Mess: If Rates Go To Zero, MPW Is Still In Trouble

In September, S&P downgraded MPW again to BB negative outlook, indicating a 33% chance it would downgrade to at least BB-.

S&P

S&P estimates a 17% chance that MPW will default on its debt entirely and declare bankruptcy. That would effectively make its stock worth $0.

If current trends continue, S&P will increase that estimate to 21% to 25%, and anyone buying MPW today will lose 100% of their money.

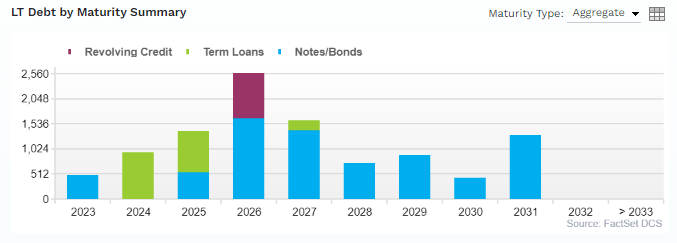

Material upcoming debt maturities threaten to pressure Medical Properties Trust's liquidity position. Starting in 2025, it has more than $1.4 billion of debt due in each of the next three years through 2027. While the company's current liquidity position is adequate due to more modest debt maturities in 2023 and 2024, with proceeds from asset sales earmarked for debt repayment, it may come under significant pressure beginning in 2025." - S&P (emphasis added).

{kind=link}

How many bond investors will buy bonds maturing longer than seven years? None. MPW has no such bonds, and we can't confirm that bond investors think it will still exist beyond 2031.

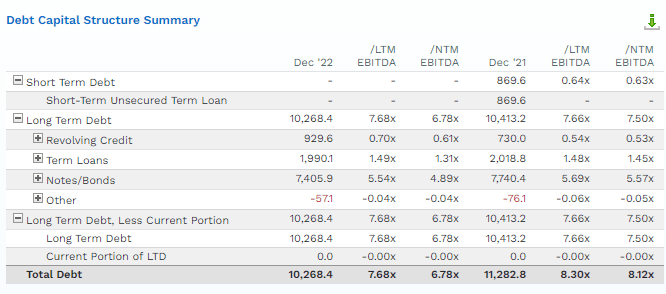

6X or less debt/EBITDA is the ratio rating agencies consider safe for investment-grade REITs.

MPW hit 8.3X in the last year, and even by the end of 2024 is expected to be close to 7X.

And as S&P points out, it has mountains of bonds maturing in the coming years.

{kind=link}

OK, but what if interest rates come down quickly?

Unless they go back to zero in the next year or two, MPW is in for a rough time.

- 4.1% average interest rate on its debt.

What are the current yields on MPW's BB negative outlook-rated bonds?

- MPW borrowed at 4% to 5% during the Pandemic

- now 12% to 13% is the yield on its bonds.

MPW's business is now so speculative, and bond investors are so worried about its ability to repay debt that even if the Fed cut 5% back to zero and 10-year yields went back to a record low of 0.5%, MPW would be likely facing 8% refinancing costs.

- if rates go back to the lowest levels in history, MPW's interest costs will double

- if they don't, they will triple.

Isn't it worth taking a flyer for a 13% yield and 4X AFFO REIT?

What if we take 1% of our money and take a complete punt on MPW? Just in case it doesn't cut its dividend? Might that not be an incredible opportunity?

Fundamentals Summary

- yield: 13% - very unsafe

- dividend safety: 17% very unsafe (17+% dividend cut risk)

- overall quality: 41% low-risk Ultra SWAN dividend aristocrat

- credit rating: BB Negative (17% 30-year bankruptcy risk)

- S&P LT Risk management global percentile: 30 = high risk (good risk management)

- long-term growth consensus: -4.7%

- long-term total return potential: 8.3% vs 10.2% S&P 500.

How many stocks can deliver better than 8.3% long-term returns? Most good defensive sectors like utilities REITs and midstream offer 9% or more.

Anyone buying MPW today is making a relatively high-risk speculative gamble that MPW will stop the fundamental slide (somehow), and the dividend will remain intact.

Why take this risk to earn 8% long-term returns when you can buy 8% yielding SWANs and Ultra SWANs that can match or beat MPW on yield alone?

Finding 10%-Yielding SWAN Alternatives To MPW

Here is how I have used our DK Zen Research Terminal to find the best 8% yielding alternatives to MPW. The kinds of dependable dividend stocks that can beat MPW's total returns on yield alone, never mind modest growth.

All in one minute, thanks to the DK Zen Research Terminal. This is how I find all my investment ideas.

| Screening Criteria |

| Companies Remaining |

| % Of Master List |

| 1 |

| SWAN Quality (11, 12, and 13 quality scores) |

| 254 |

| 50.80% |

| 2 |

| BHS Rating "reasonable buy, good buy, strong buy, very strong buy, ultra value buy" |

| 194 |

| 38.80% |

| 3 |

| Non-Speculative (No Turnaround Stocks, investment grade) |

| 158 |

| 31.60% |

| 4 |

| 8% Yield |

| 3 |

| 0.60% |

| Total Time |

| 1 minute |

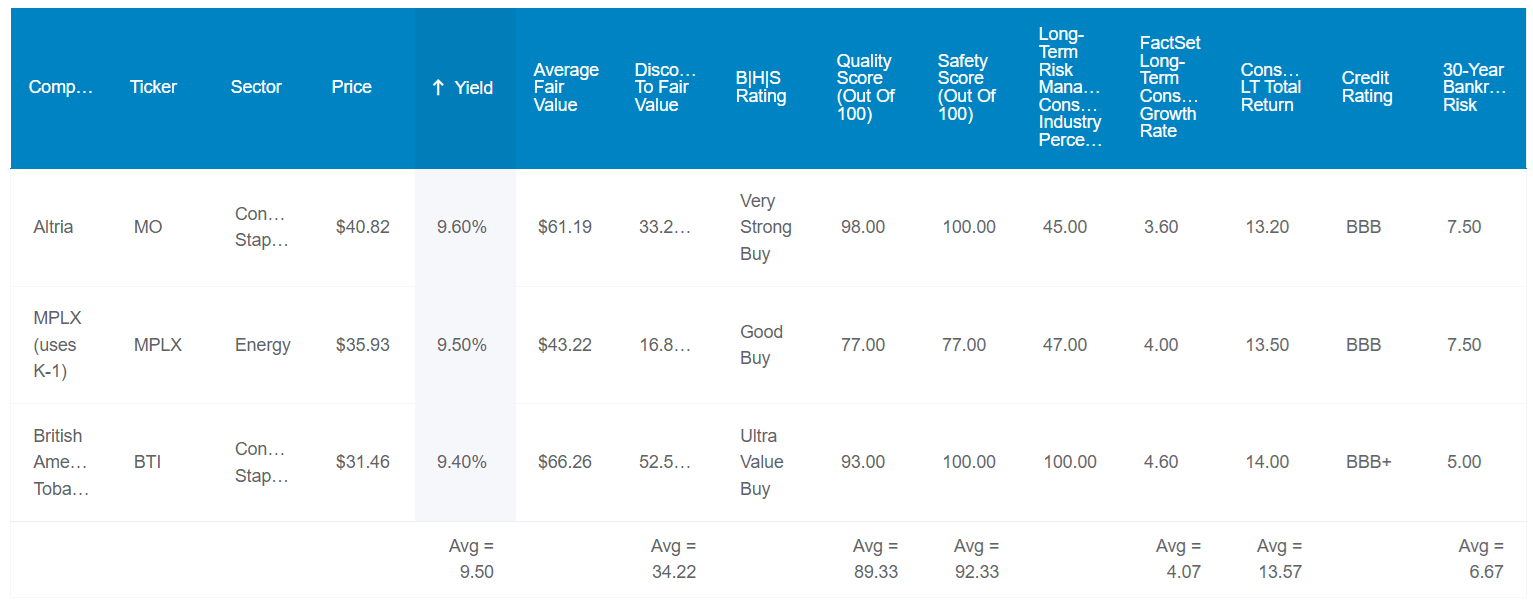

10% Yielding SWANs For A Rich Retirement

Here's the bottom line up front

Fundamentals Summary

- yield: 9.5% (6X S&P 500 and more than 2X SCHD)

- dividend safety: 92% very safe (1.4% dividend cut risk)

- overall quality: 89% low-risk Ultra SWAN dividend aristocrat

- credit rating: BBB+ stable (6.67% 30-year bankruptcy risk)

- S&P LT Risk management global percentile: 63rd = low risk (good risk management)

- long-term growth consensus: 4.1%

- long-term total return potential: 13.6% vs 10.2% S&P 500

- discount to fair value: 34% discount (potential very strong buy) vs 11% overvaluation on S&P

- 10-year valuation boost: 4.2% annually

- 10-year consensus total return potential: 9.5% yield + 4.1% growth + 4.2% valuation boost = 17.8% vs 9% S&P

- 10-year consensus total return potential: = 415 % vs 134% S&P 500.

$1 today could be $5.15 in 10 years, 3X better than the S&P's expected returns.

Now, here are the incredible 10% yielding SWANs worth buying today.

{kind=link}

Consensus Total Return Potential Through 2025

- if and only if each company grows as analysts expect

- and returns to historical market-determined fair value

- this is what you will make.

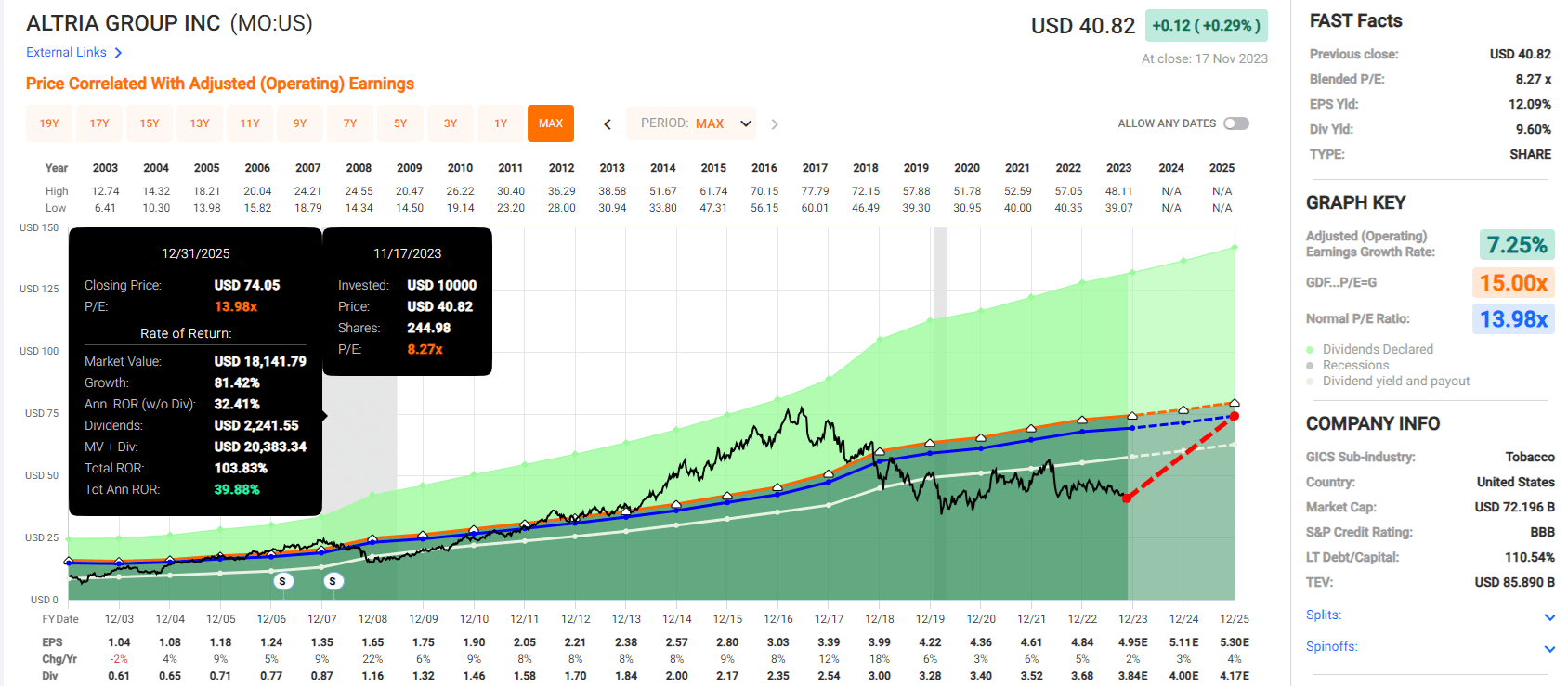

Altria

{kind=link}

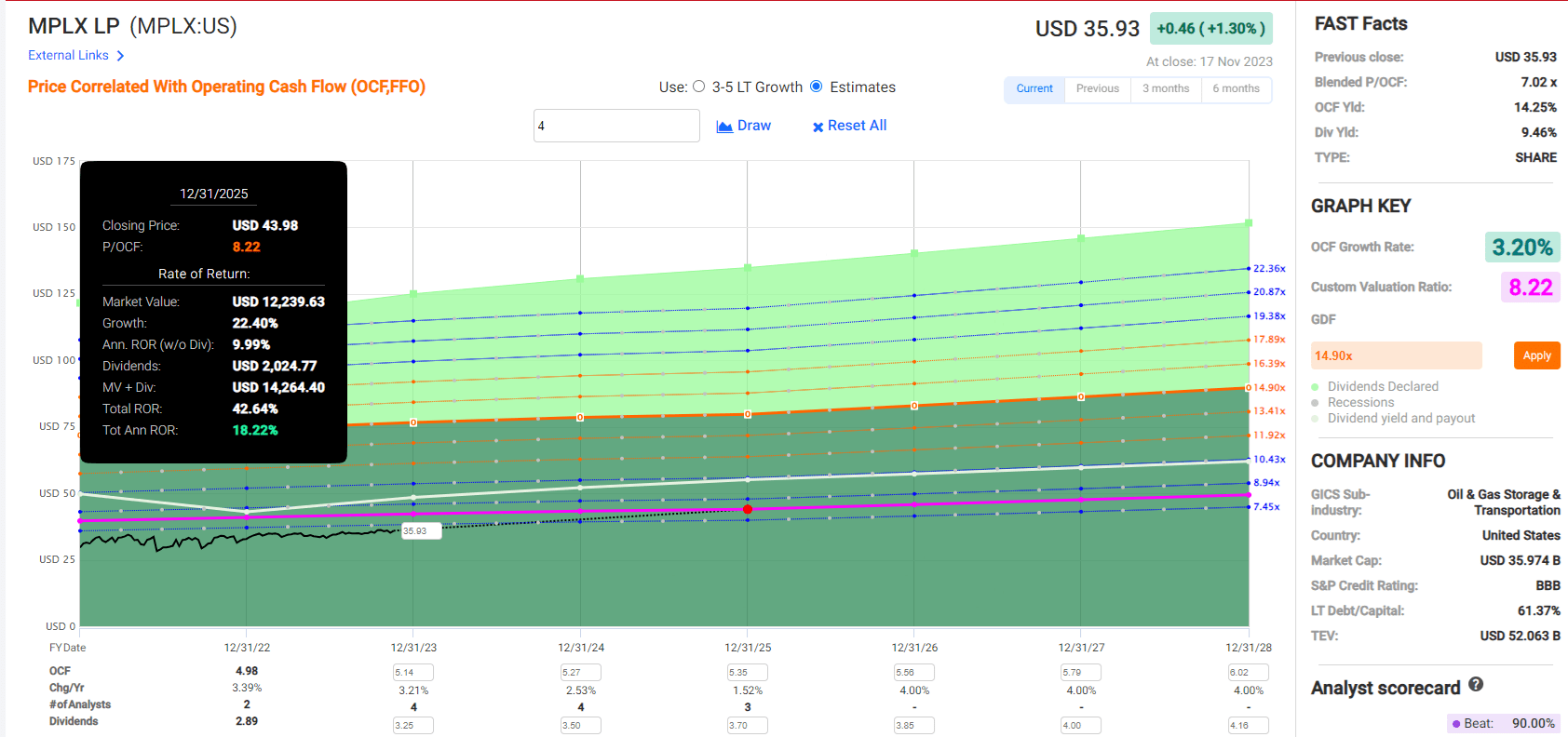

MPLX

{kind=link}

British American

{kind=link}

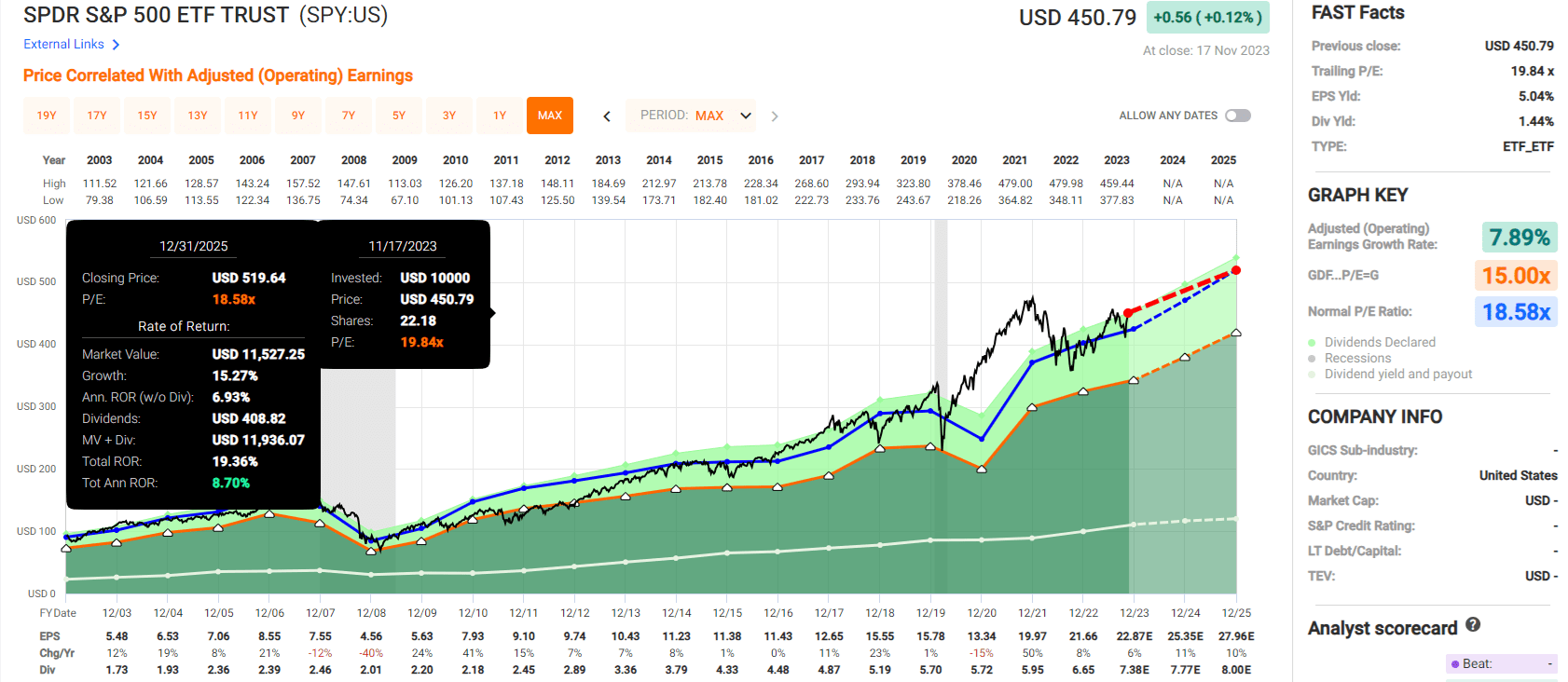

S&P 500

{kind=link}

S&P 500 (SP500) has a 20% total return potential in the next two years.

These three 10% yielding SWANs could almost double.

5X the return potential over the next two years and 6X the very safe yield.

Bottom Line: Why Take Unnecessary Risk With MPW When There Are Far Superior Ultra-Yield Options?

Some people like buying dirt cheap cigar butt-style stocks, like what Buffett and Graham started their careers doing.

MPW certainly qualifies for that. It's dirt cheap at 4X AFFO and 3X FFO.

I'm not predicting that MPW is going bankrupt. That's just a 17% risk.

Nor am I saying the dividend will likely be cut (17% risk of that).

But the fundamentals are deteriorating, and the statistical data is clear. The odds are not in favor of MPW investors at this point.

Compared to 10% yielding alternatives like MO, MPLX, and BTI, I am saying that the risk of a dividend cut for MPW is about 15 times higher.

These 10% yielding SWANs will likely beat MPW long-term on the current yield alone.

Add their modest growth rate and attractive valuation, and you can potentially get a 5X return in a decade.

For further details see:

Sell Medical Properties Trust And Buy These 10%-Yielding Blue Chips Instead