MORT - Sell MORT Buy These ETFs Instead

2024-01-10 18:00:30 ET

Summary

- MORT is a poorly performing income ETF with high risk and consistent losses.

- Investors seeking high yields should consider alternatives.

- With an unfavorable view of MORT, I offer my views as to why along with some alternatives.

The VanEck Mortgage REIT Income ETF (MORT) is one of the worst-performing income ETFs in the market, with sky-high risk, consistent losses and distribution cuts. The fund is a terrible long-term hold, and rarely a good short-term investment.

Aggressive investors looking for the highest yields have much stronger options than MORT. These include the VanEck BDC Income ETF ( BIZD ), the Saba Closed-End Funds ETF ( CEFS ), and the Panagram BBB-B CLO ETF ( CLOZ ). These three funds offer investors strong, double-digit distribution yields, and have a much stronger performance and dividend growth track-record than MORT. As such, I would not invest in MORT, and strongly prefer BIZD, CEFS, or CLOZ.

MORT - Basics

- Investment Manager: VanEck

- Underlying Index: MVIS US Mortgage REITs Index

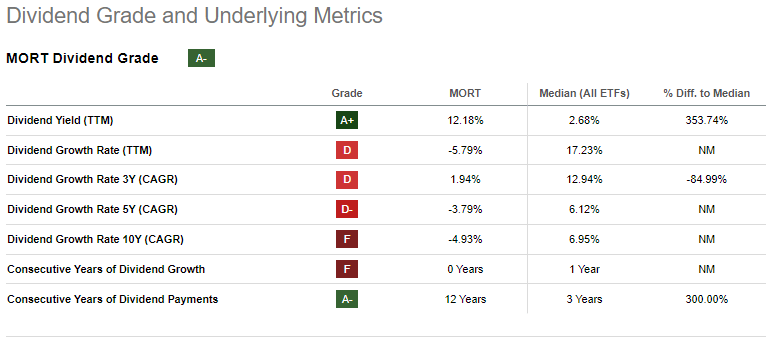

- Dividend Yield: 12.18%

- Expense Ratio: 0.43%

- Total Returns CAGR 10Y: 2.18%

MORT - Overview and Analysis

Index and Holdings

MORT invests in mREITs, financial institutions focusing on leveraged mortgage investments. It tracks a broad-based mREIT index, with investments in most relevant securities of its kind. It currently holds 27 different mREITs, with a significant, double-digit investment in the well-known Annaly Capital Management ( NLY ). The largest holdings are as follows:

MORT

Concentration/Lack of Diversification

MORT is an incredibly concentrated, undiversified fund, as it focuses on an incredibly niche investment asset class: mREITs. Concentration is quite high too, with the fund investing in only 27 different securities, and with the top ten of these accounting for over 60% of its portfolio.

MORT's concentration increases portfolio risk and volatility, and means that the fund's performance might materially differ from that of the broader market. As an example, the fund has significantly underperformed since early 2022, as higher rates hammer real estate industry valuations and earnings. This was the case for more REIT funds, however.

In my opinion, MORT is concentrated enough that large position sizes are unwise.

Leveraged Investments

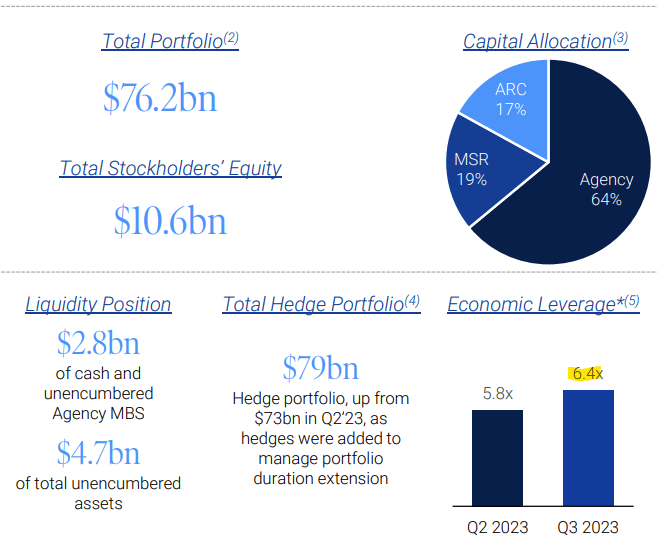

MORT's mREITs investments are highly leveraged investments. Excessively leveraged in many cases. As an example, Annaly Capital Management manages an investment portfolio worth $76.2 billion with only $10.6 billion in shareholder equity. In other words, for every dollar of equity the company has around six dollars of debt (6.4, to be exact).

{kind=link}

Annaly's debt load significantly increases company earnings, turbocharging investor dividends. The logic is, I think, quite simple: more debt means more assets, which means more income, earnings, and dividends. A closer look at how this works might be illuminating.

Unleveraged mortgage investments yield around 4.5% right now:

Annaly Capital Management

Annaly earns 4.5% on these investments, those bought with equity.

Annaly can make even more investments with debt. Debt can be financed at a 3.3% rate (seems unsustainably low). Margins should equal 1.2%, but actually equal 1.5%. Unclear were the 0.3% came from.

Annaly Capital Management

So, Annaly earns 4.5% on their equity-financed investments, and another 1.5% on those funded with debt. With a 6.4x economic leverage ratio, that adds up to 14.1%. Annaly itself yields 13.3%, a bit lower due to the company trading at a slight premium to its assets (PB above 1.0x).

Annaly's debt load significantly increases company earnings and dividends, straightforward benefits for investors. The debt load also has several significant negatives and risks.

First, debt is expensive, excessive debt loads doubly so. In most cases, the interest earned on productive assets is higher than the costs incurred by the debt, but this is not always true, and margins or spreads vary. Some financial institutions have seen much lower margins these past few years, as Federal Reserve hikes increase interest rates on debt. As an example, net interest margins for Annaly have decreased by around 0.15% this past quarter:

Annaly Capital Management

Margins are down 0.50% since late 2020, before rates started increasing:

Annaly Capital Management

mREITs earnings and dividends are dependent on fat margins and low cost of debt, neither of which is certain, both of which have worsened these past few years.

The second issue with high debt loads is that these generally have to be rolled over, which might not necessarily occur at reasonable terms, if at all. Liquidity sometimes dries up, especially during severe recessions and financial crisis, which could spell trouble for mREITs like Annaly, with tens of billions of debt.

The third issue with high debt loads is that these serve to magnify any capital losses experienced. Remember, more debt means more assets, which means more losses when asset prices decline. Significant reductions in price could lead to mREIT bankruptcies. Sizable reductions could lead to forced asset sales, as debt covenants generally compel companies to meet reasonable capital and leverage ratios. I'm familiar with the case of the Invesco Mortgage Capital ( IVR ), which saw significant losses in early 2020, was forced to sell off assets at rock-bottom prices, and then never recovered (you can't recover if you sell).

Data by YCharts

In my opinion, many mREITs are excessively leveraged investments, so significant investments in these, especially as an asset class, are unwise. Smaller, targeted investments in the best of these might make more sense. Annaly seems to do reasonably well, recent weakness notwithstanding.

Dividend Analysis

The high debt loads on mREITs do have one important benefit: higher dividends. MORT itself yields a whopping 12.2%, almost five times as much as mortgage-backed securities, or MBS, themselves.

Rates on both MBS and MORT look somewhat low, as benchmark 30Y mortgage rates are at around 7.0%. MBS should yield around that, MORT much higher. Yields are lower than expected as it takes time for higher interest rates to impact investment markets, and for older, lower-yielding mortgages to mature and funds transferred into newer, higher-yielding mortgages.

MORT's dividends are incredibly high on an absolute basis, and much higher than that of most asset classes.

On the other hand, the fund's dividend growth track-record is decisively negative, with dividends seeing consistent cuts since inception. Cuts were due to sporadic mREIT implosions (IVR in early 2020), lower interest rates in past years, and narrowing margins in recent years.

{kind=link}

In my opinion, the consistency of these dividend cuts indicates significant issues with the strategies and business models of most mREITs. Companies should see higher earnings and dividends long-term, and the fact that mREITs were unable to successfully leverage higher rates these past few years is a very negative signal.

Consistent dividend cuts means long-term investors tend to see weak, declining income long-term. Yield on costs average 6.5% before the pandemic, 7.5%-8.5% in the years immediately after. MORT's 15.8% in dividends are quite strong, but they don't seem to last long.

{kind=link}

Performance Analysis

MORT's overall performance track-record seems about average, at best. Returns are generally lower than those of high-yield bonds, at much higher risk. Returns are generally higher than those of bonds in general, but at much higher risk. The fund's overall risk-return profile looks extremely weak.

MORT - Some Alternatives

Investors looking for strong, double-digit dividend yields have several strong alternatives to MORT.

BIZD is the obvious choice. The fund focuses on BDCs, leveraged financial institutions focusing on riskier small and medium-sized enterprises. In practice, BDCs have a much stronger track-record than mREITs, with BIZD significantly outperforming since inception, and with lower risk and drawdowns.

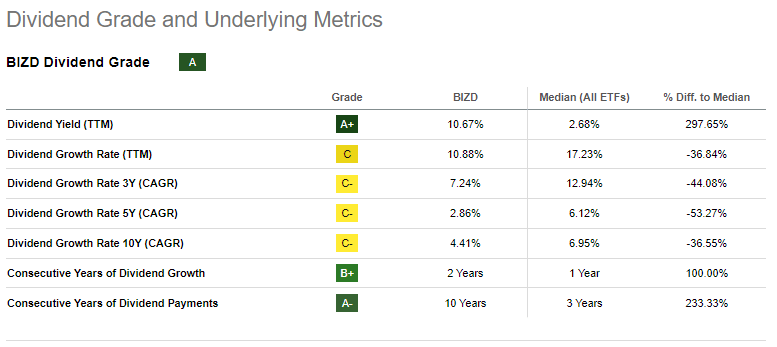

BIZD sports a 10.7% dividend yield, quite a bit lower than MORT's 12.2% figure. BIZD's dividend growth track-record is much stronger, however, so long-term investors should see higher income from BIZD than MORT.

{kind=link}

I last covered BIZD here .

The Saba Closed-End Funds ETF ( CEFS ) is an actively-managed ETF investing in a diversified portfolio of CEFs. CEFs tend to sport strong distribution yields, as does CEFS, with an 8.8% yield (excluding a special distribution late last year). Although dividends are lower, dividends have been stable since inception, and the fund sometimes pays a special distribution at the end of the year. CEFS sometimes engages in activist campaigns, and is sometimes aggressively positioned. Both tend to be successful, with the fund performing quite well since inception.

I last covered CEFS here .

Finally, CLOZ invests in BBB-BB CLO debt tranches. Right now, and in my opinion, CLO debt tranches offer very compelling risk-return profiles, with CLOZ sporting a 10.3% SEC yield at low credit and interest rate risk. CLOZ's performance track-record is outstanding, but also quite short.

I last covered CLOZ here .

Conclusion

MORT is one of the worst-performing income ETFs in the market, with sky-high risk, consistent losses and distribution cuts. As there are several stronger income ETFs in the market, I would not be investing in MORT.

For further details see:

Sell MORT, Buy These ETFs Instead