SOFI - Sell SoFi Technologies Because Of Macro Demand And Supply Challenges

2024-01-16 18:40:01 ET

Summary

- SoFi's products are mature and growing modestly, with competition in the market being strong.

- SoFi's rapid growth plans are risky and likely to be disappointing relative to its current valuation, as history shows.

- SoFi's strategy to build trust and a lifetime relationship with members is unlikely to overcome its strong competition.

- The company's valuation is based more on hope than on the reality of supply and demand.

Most commentary about fintech company SoFi (SOFI) focuses on “micro” issues, most typically some measure of its revenue and customer growth. I’m adding to the conversation by focusing on SoFi’s “macro” issues, namely:

- Demand – What are the growth rates of the products that SoFi is competing for?

- Supply – What does the competition for these products look like?

I conclude that SoFi’s products are mature and growing modestly, and that its competition is generally pretty strong. SoFi’s rapid growth plans are therefore risky, and history says that the results will be disappointing relative to its current valuation. SoFi is currently selling at 240% of tangible book value (rich for a bank) and a silly 137 P/E of ’24 expected EPS of $0.06 ( Seeking Alpha ).

But first…

What is SoFi?

SoFi today is a version of a commercial bank plus a software company. As the company says in its latest 10-K :

“We are a member-centric, one-stop shop for financial services that, through our Lending and Financial Services products, allows members to borrow, save, spend, invest and protect their money.”

That is exactly what the average bank does. In fact, SoFi is a bank holding company. Like any bank, it has some differentiating features. SoFi is:

- Fully online, with no branches. This does not make SoFi unique – there are other online banks, and the great bulk of banks have online access. But it is somewhat different.

- A consumer bank, with few business customers.

- Focused on two unusual loan products – student loans and unsecured personal loans. It also has fledgling home mortgage and credit card businesses.

SoFi’s software company is pretty mysterious, at least for this non-tech-savvy writer. I’ll leave the description to the company:

“Our products and capabilities are designed to appeal to enterprises, such as financial services institutions that subscribe to our enterprise services and have become interconnected with the SoFi platform. We have continued to expand our platform capabilities for enterprises through our acquisition of Galileo in 2020, which provides technology platform services to financial and non-financial institutions…and the Technisys Merger in the first quarter of 2022, through which we added a cloud native digital and core banking platform into our technology platform offerings and expanded our technology platform services to a broader international market.” ( SoFi 10-K )

That’s all I have to say about it.

SoFi’s demand challenge

Any business’s growth comes from two sources – (1) organic growth of its product categories, and (2) market share. In this section I’ll present the organic stories.

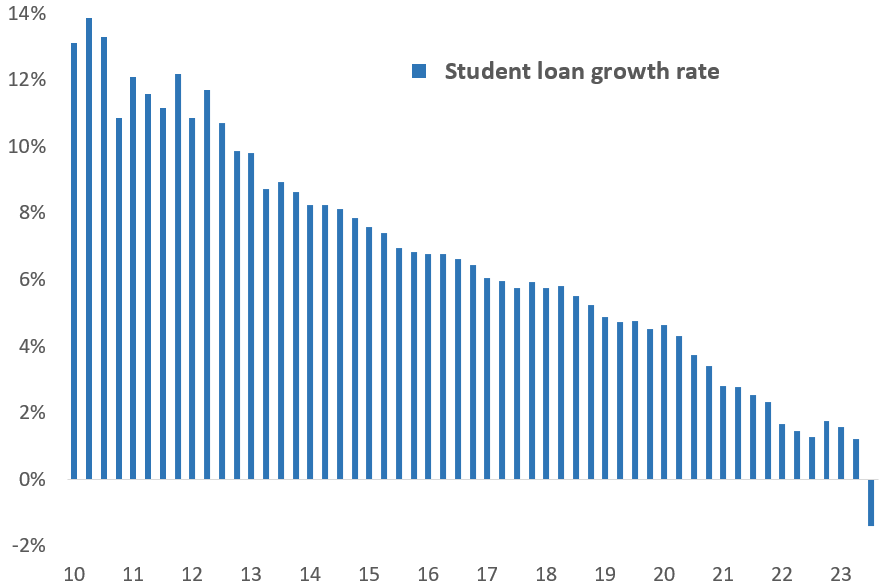

Let’s start with SoFi’s original product, student loans . This chart shows a history of U.S. student loan debt growth:

{kind=link}

Source: Federal Reserve

Rapid deceleration to now shrinkage, with a lot more shrinkage ahead because of government-mandated student loan forbearances. So student loan debt is the opposite of a growth product.

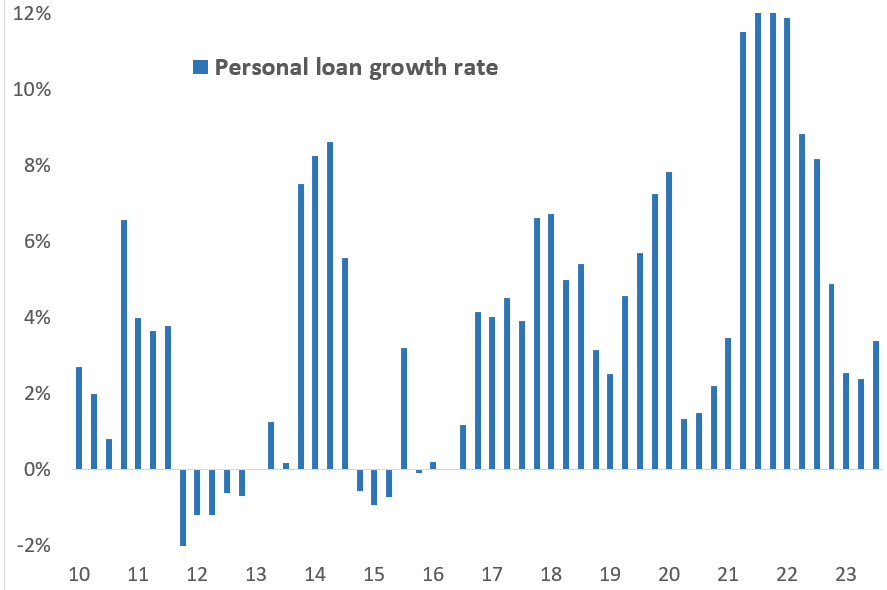

On to SoFi’s current primary loan product, unsecured consumer loans . This chart shows the growth rate history of credit card and other consumer credit, excluding mortgage, auto and student loan debt:

{kind=link}

Unsecured consumer credit grew by only 3% a year from 2010 up until the Pandemic. It then had a growth spurt after the COVID checks stopped coming in mid-’21, but is now in the 3% range again. Not a growth product.

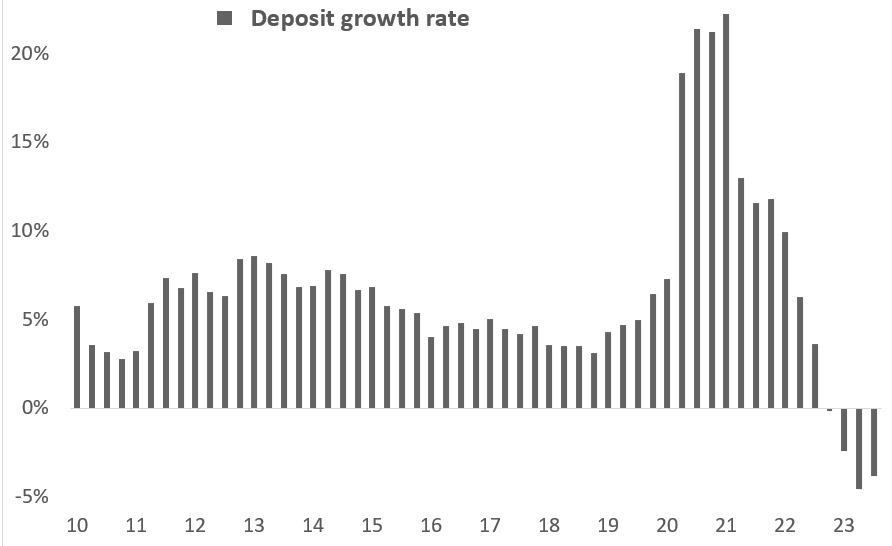

Finally, the growth rate of SoFi’s new hot product, namely consumer deposits :

{kind=link}

Up until the Pandemic consumer deposits grew by 6% a year. Not growthy, but not too bad. Then deposits surged as consumers put much of their COVID checks in the bank. But now consumers are spending down those excess deposits, so growth for the next few years will certainly be well below 6%.

Net/net, it cannot be said that SoFi is operating in growth businesses. That’s why the average bank P/E ratio is about 9, or less than half the market average.

SoFi’s supply challenge

Does SoFi offer products to underserved customer bases? Not really.

Student lending is likely the one product where SoFi faces relatively weak competition. NerdWallet lists these companies as its main competition: LendKey, College Ave, RISLA and ISL. I haven’t heard of them either.

Unsecured consumer loans are a very different story. Heard of JPMorgan Chase? Capital One? American Express? Discover? Citibank? Plus Upstart, Lending Club and other fintechs. Plus loads of banks.

Consumer deposits are obviously even worse. Clearly every bank in the country is a competitor. Plus nonbanks like American Express, Schwab, Goldman Sachs, brokerage firms and fintechs like Chime and Venmo.

Home mortgages? This is a new SoFi product. No banking product is likely more competitive than mortgage lending, where the #1 lender has only a 7% market share. And #2 lender Rocket Mortgage could only break even during last Q3.

Financial services growth stories therefore require taking market share. Which is seriously problematic.

Most consumer products are sold with emotional pitches. Think how many car ads have dogs in them. But how often do you get a positive emotion from a financial product? So financial services companies are forced, far more than other consumer products companies, to offer better features than competitors if they seek market share gains. And those features are pretty much limited to:

- Price. Namely lower loan yields and higher deposit rates.

- Underwriting. Taking more risk of default by increasing approval rates or making bigger loans.

How can a financial services company consistently give up price and still earn a respectable profit? At least in theory, it can employ technology to its lower administrative, marketing, and other costs below competitors’. And how can a financial company loosen its lending standards and still earn that respectable profit? By being a better credit analyst than peers. Both strategies are good in theory, but rare in practice.

The history of price- or credit-based market share strategies is not good.

Some examples:

Price strategy: Robinhood. Eliminating trading commissions was a bold move. The payoff? $5.5 billion of cumulative losses to date. A $38 IPO has turned into a $12 stock price at present. 2024 earnings are expected to be $0.02 per share ( Seeking Alpha ).

Price strategy: Redfin. Another low-commission competitor, this time of realtor commissions. The payoff? $800 million of cumulative losses, which is all but $6 million of what investors put into the company. I do not believe it has had a profitable year in its 21-year history. Are brighter days ahead? Seeking Alpha finds that Wall Street analysts expect a $1.05 per share loss this year. The $15 IPO in 2017 is $10 today.

Credit strategy: Subprime mortgage lenders. Many lenders decided in the early ‘00s that they had cracked the code on subprime (average 600 credit scores) mortgages. A working paper from the Federal Reserve Bank of St. Louis says that the number of subprime loan originations surged from 552,000 in 2001 to 2.3 million in 2005. This presumed credit breakthrough resulted in nearly universal bankruptcies for subprime mortgage originators by 2008.

Credit strategy: Subprime auto lenders. From the American Bankruptcy Institute :

“ In the early 1990s, the subprime automobile finance industry was regarded as a Wall Street darling. Earning growth rates of 100% were not uncommon as capital poured into the industry…In January 1997, Mercury Finance, the largest independent subprime auto finance company, disclosed accounting irregularities. This event started a chain reaction that led to the collapse of many large players in the industry. ”

One more. Credit strategy: Credit card issuer NextCard. From the Los Angeles Times :

“ Bankrupt credit card lender NextCard is planning to liquidate, according to court documents…A onetime darling of the dot-com boom, NextCard fell into trouble with regulators a year ago after issuing too many credit cards to deadbeat borrowers. Shareholders aren’t expected to receive any payments from the liquidation. NextCard’s stock peaked at $53.12 in 1999. ”

So how does SoFi expect to profitably take market share?

First, so far the profitability thing hasn’t been happening. To date, SoFi generated a $1.9 billion loss, including $340 million of losses during the first 9 months of last year. But here is SoFi’s plan, with the key points underlined by me:

“ Our strategy, which is rooted in what we refer to as our “Financial Services Productivity Loop”, is centered around building trust and a lifetime relationship with our members, which we believe will help build a sustainable competitive advantage…In order to deliver on our strategy, we must develop best-in-class unit economics and best-in-class products that build trust and reliability between our members and our platform. Our acquisition of SoFi Bank was also an important step...” (SoFi 2022 10-K)

“I [the CEO] remain confident that no company is better positioned than SoFi to be the winner that takes most in the digital transformation of financial services…Add to that, the regulatory requirements and sizable financial capital and resources required and it's fair to conclude, SoFi is in a class of one.” ( SoFi Q3 ’23 earnings call transcript )

Do you see any potential holes in this plan? I do.

Strategy hole #1: “Our acquisition of SoFi Bank was an important step.”

Really? That puts SoFi in the exclusive club of 4,236 other banks. A bank charter is clearly not a competitive advantage for SoFi. And the other 4,235 other banks also meet the “regulatory requirements” required to maintain the bank charter. This supposed advantage only makes sense if you assume that SoFi’s only competition is other fintechs.

Strategy hole #2: “Sizable financial capital and resources required.”

Yes, SoFi is big for a fintech. It has $5 billion of capital and last year spent about $500 million on technology and product development and $725 million on marketing. But Capital One is also a competitor. It has $53 billion of equity capital. My calculator says that $53 billion > $5 billion. Capital One spent nearly $4 billion on marketing last year. Capital One doesn’t disclose its tech spending, but it did say this in its ’22 annual report :

“A key part of our strategic focus is the development and use of efficient, flexible computer and operational systems, such as cloud technology, to support complex marketing and account management strategies, the servicing of our customers, and the development of new and diversified products.”

And JPMorgan Chase, from its ’22 annual report :

“AI and the raw material that feeds it, data, will be critical to our company’s future success — the importance of implementing new technologies simply cannot be overstated. We already have more than 300 AI use cases in production today for risk, prospecting, marketing, customer experience and fraud prevention...”

SoFi is far, far from alone in recognizing the importance of technology innovation and marketing, and having the financial and technical resources to do something about it.

Strategy hole #3: “We must develop best-in-class unit economics and best-in-class products”.

Stating that goal is easy; doing it is hard. Is there evidence to date that SoFi is doing it? Not that I can see. Those $1.9 billion of losses to date, and minimal earnings expected for this year, says that SoFi is far from achieving best-in-class economics. While SoFi is expected to generate a 1% return on equity next year, Discover is expected to earn 23% ( Seeking Alpha ).

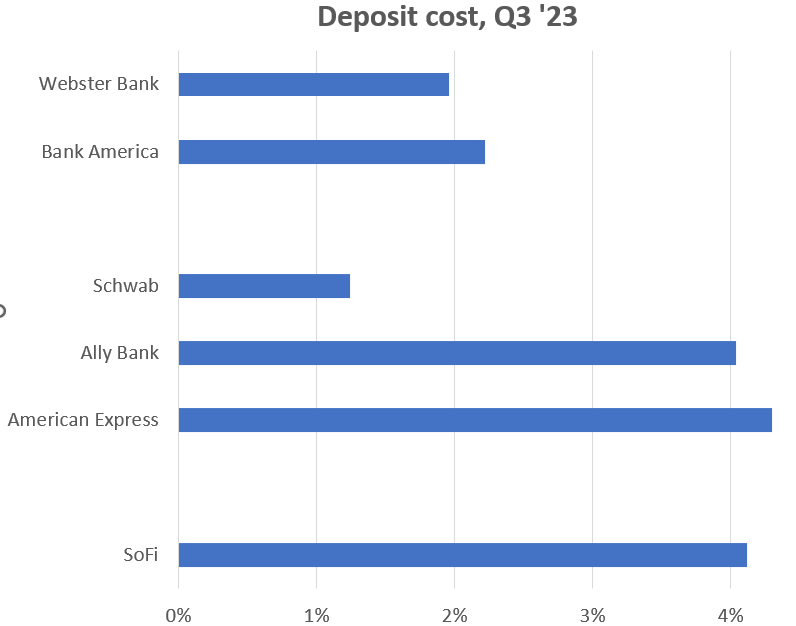

One seeming success story for SoFi has been a dramatic growth in consumer deposits; they more than doubled through the first 9 months of last year. Is it because of SoFi’s best-in-class deposit products? Or price? You tell me after you look at this chart:

{kind=link}

Sources: Company financial reports

SoFi pays way more than the branch banks, and in line with the online banks. Nothing special that I can see.

Strategy hole #4: “No company is better positioned than SoFi to be the winner.”

First, it is ludicrous to believe that any company is going to be the winner in financial services. Rather, this is the standard fantasy of the “industry disruptor” fintech pitch. As proof, here are the fantasies of other fintech disruptors:

Rocket Companies. “ As I look around Rocket, I see a company with the talent, the culture and the assets to drive meaningful disruption and transformation. I am beyond excited for the tremendous opportunities that lie ahead of us .” ( Q3 ’23 earnings call transcript )

Upstart. “ We're making rapid progress in building the world's first and best AI lending platform. We do this with a focus on our mission, and with an optimistic eye toward the transformation of an industry that is inevitable over the next decade and beyond. ” ( Q3 ’23 earnings call transcript )

Robinhood. “ Robinhood is no longer just a trading app, we've been rapidly evolving into a broad financial services platform serving multiple financial needs, including spending, savings, and retirement. Our ambition and the opportunity ahead of us has expanded greatly. ” ( Q3 ’23 earnings call transcript )

Which disruptor are you going to believe? My answer – none of them.

Summing up. Sell this stock. And the risk to shorting.

On the one hand, there is the disruptor theme pitched by management and desperately believed by many looking for the next monster tech story. On the other hand is the reality of slow demand and abundant supply. I recommend reality.

There are two main risks to my short thesis. One is continued investor speculation that self-proclaimed disruptors will deliver as promised. Dreams die hard, so it is reasonable to expect that speculative rallies will continue to occasionally recur.

The other risk is that my supply/demand thesis is wrong; that SoFi somehow creates a differentiated and profitable market niche. With product categories this commoditized, and with the substantial amount of competition for these products, that seems highly unlikely, but nothing in this world is absolute.

For further details see:

Sell SoFi Technologies Because Of Macro Demand And Supply Challenges