CRGY - Sell U.S. Energy Buy Crescent Energy

Summary

- U.S. Energy recently exchanged stock to outsiders who now control 80% of the voting shares after the sale.

- This transition has been underway since before 2019 when the new board was appointed.

- The major transformative acquisition allows an acquisition strategy to grow.

- Management is unlikely to drill for oil at the current time.

- Crescent Energy provides a far more reputable and experienced team to guide the company than is the case with U.S. Energy.

(Note: This was in the newsletter on January 12, 2023.)

U.S. Energy ( USEG ) has new management that came into run the company back officially in 2019 when the board of directors elected them. The start on this process began before that and is in the SEC filings. In January 2020, the company announced it had regained compliance with NASDAQ listing requirements (as it had gotten behind in statement filings) and did a reverse split of 1 for 10. Since that time the company has announced and pursued an acquisition strategy that has resulted in a lot of acquisitions. But the stock price has not responded favorably.

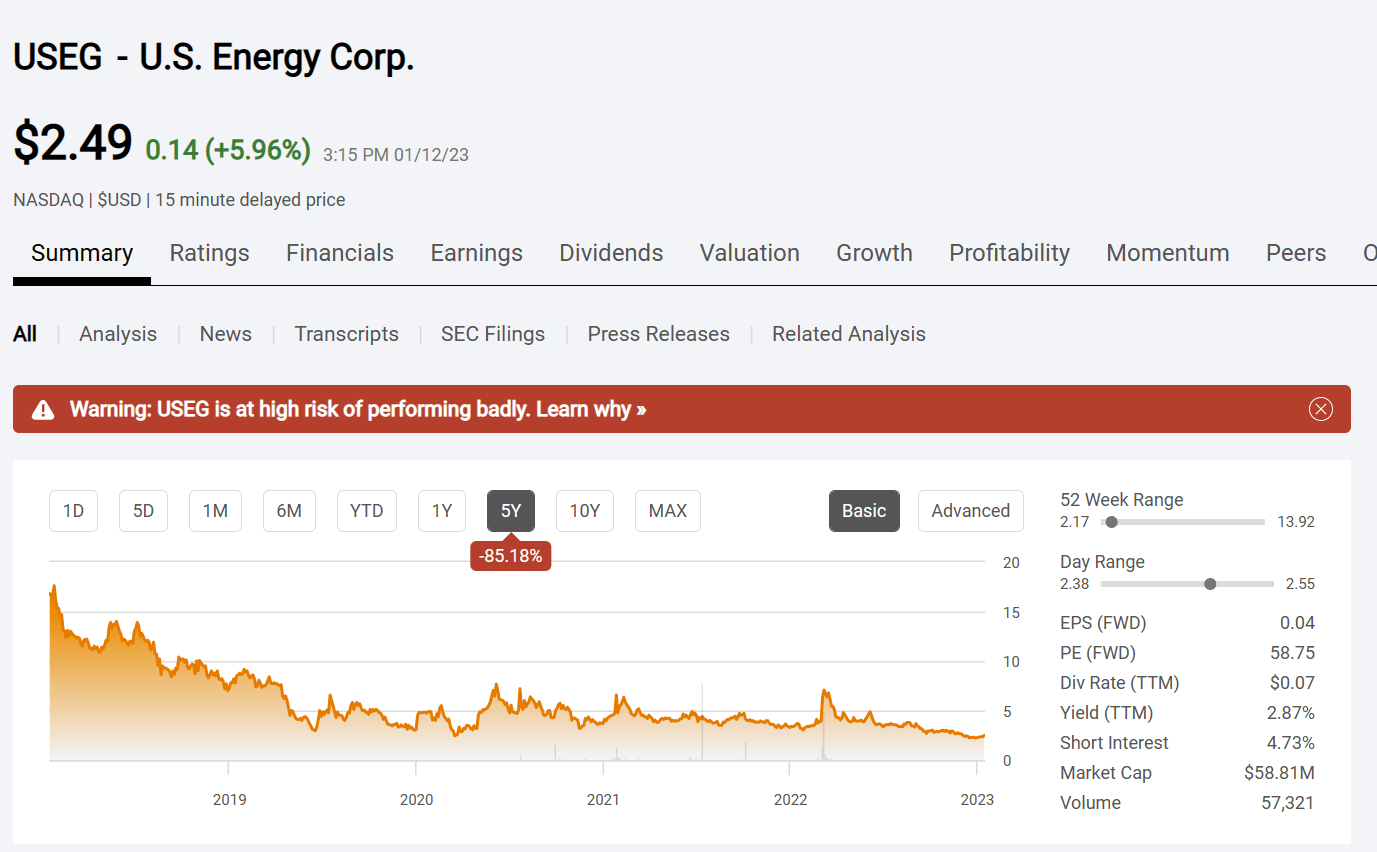

U.S. Energy Common Stock Price History And Key Valuation Measures (Seeking Alpha Website January 12, 2023)

{kind=link}

The group that appointed the new board of directors had to first catch up the reporting while officially taking over after that board meeting in 2019. Since that time the stock price has clearly not done much, and it appears poised to continue to underperform the bull market in oil and gas for the foreseeable future.

U. S. Energy emerged from a lot of financial issues of the previous administration. The weak oil and natural gas market wreaked havoc on the company's balance sheet. It ended up leaving a company that was a financial mess. The new crowd gets full credit for creating a viable company compared to what they walked into. But that does not mean that this is a good thing for investors.

Part of the problem is the small size of the company. the acquisition announced as part of the board meeting was a whole 1 acre. But that was all the company resources allowed. In March 2020, management announced another small acquisition using a combination of stock and cash.

The acquisitions continued throughout fiscal year 2020. Management sold stock in a $3 million offering. That was followed by a nearly $5.8 million share offering.

Then came the transformative acquisition announced in 2021 and completed in 2022. The company issues nearly 20 million shares to the sellers who will own 80% (roughly) of the company. The transaction was valued at nearly $100 million. Yet the market value of the stock is currently closer to half of that. That does not include all the transactions leading up to this.

One of the reasons for doing the transaction was that this company needed to acquire size to be a consolidator. Supposedly the acquisition was accretive in a number of ways. However, oil prices had declined lately, and this remains a small company. So right now, the results of the transaction are not apparent to shareholders.

My own opinion is that this remains a very small company and a lot of what is acquired is not that liquid. Therefore, market value of the various holdings would be discounted. It may take a long time for the company strategy to show results.

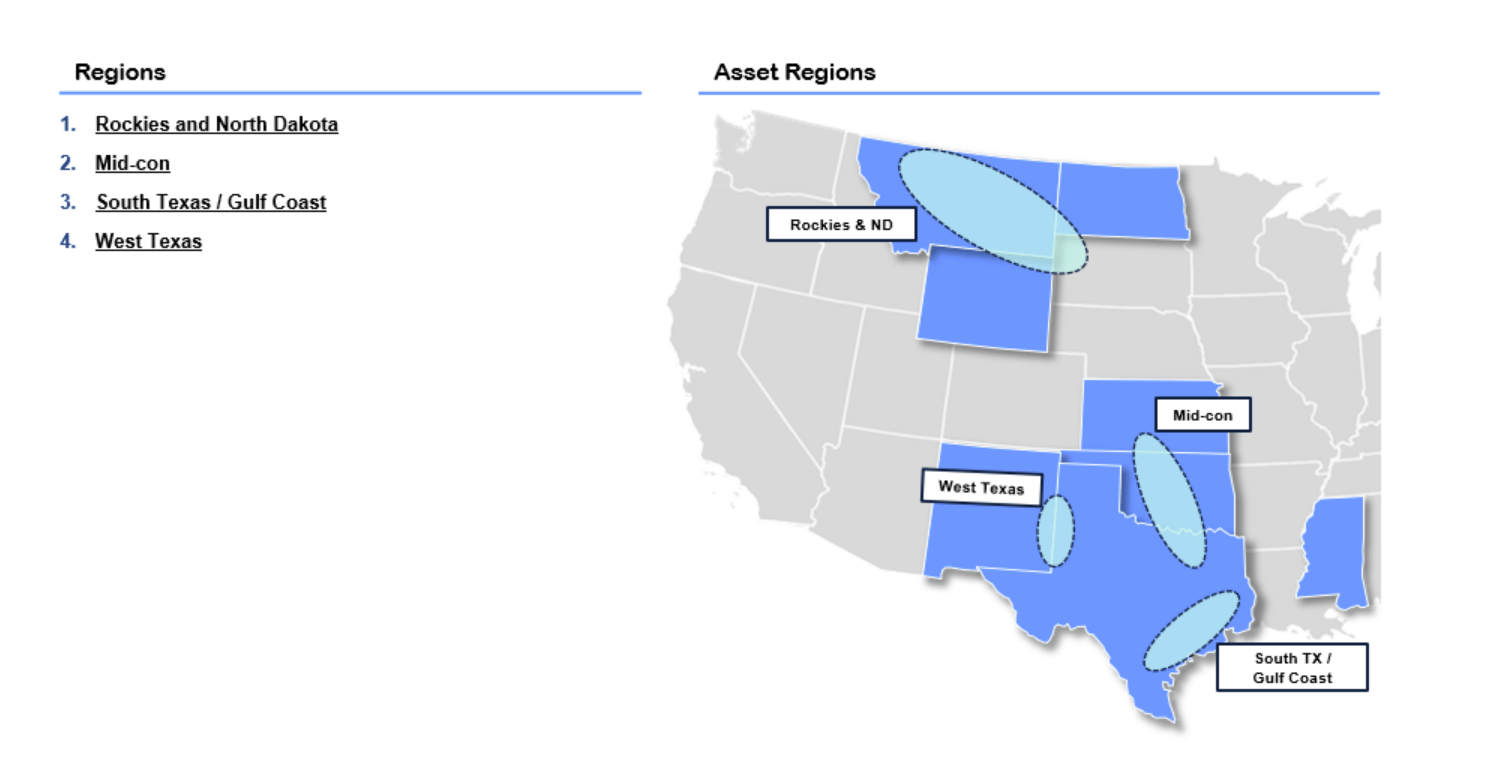

U.S. Energy Area Of Operations (U.S. Energy Company Website)

{kind=link}

The result of the acquisitions has been a lot of basin diversification as shown above. But the individual positions have been very small and likely illiquid positions. Most likely whenever any company makes a major acquisition, it needs about 5 years for investors to determine whether or not the acquisition is going to be a positive event. In this case the major acquisition, in which controlling shareholders acquired a majority of the company completed in 2022. Therefore, it is likely too soon for this acquisition to be evaluated.

Since this one another acquisition was completed in July 2022 for cash. The first announced "bolt-on " acquisition was announced in May. That is the kind of acquisition that can build value. Piecing together small holdings into a larger more marketable holding has been a sure-fire way to build value for some time. However, with this company it could take some years for this strategy to bear fruit. The question is whether shareholders want to wait that long.

U.S. Energy, the company, has had some considerable successful periods in the past. But those periods have long been separated by forgettable periods in between. This is one of the higher risks of a smaller company.

The company as structured has only been this way for really less than a year. Unless investors are very familiar with the controlling shareholders, a company the size of U.S. Energy has to be considered very risky.

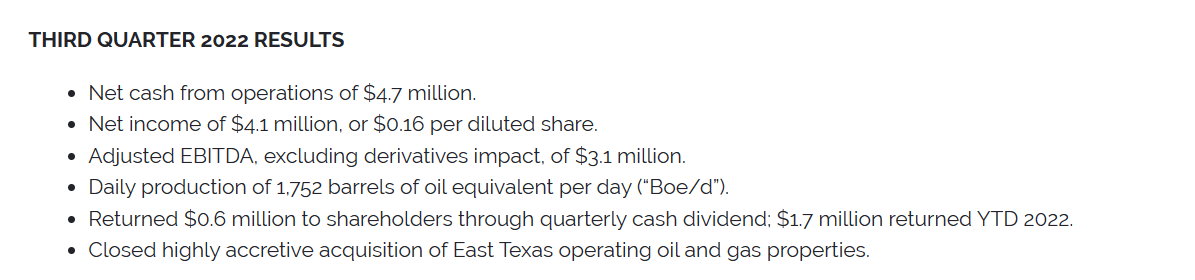

All of this led to the latest operating results:

U. S. Energy Third Quarter Results Summary 2022 (U. S. Energy Third Quarter 2022, Earnings Press Release)

{kind=link}

The result of all the financial moves made is shown above. The balance sheet remains strong with debt outstanding of $12.5 million. That can be easily handled by the cash flow shown above in the quarterly results.

However, with most of the industry out of favor, this issue is fully valued. There are other equities that are very likely to be in favor or catch the favor of the market sooner. This issue needs more time to carry out its growth goals to attain a size that would attract market attention.

This management is unlikely to drill for oil at the current time because it believes it is cheaper to buy production. There is a lot of people that would agree with this strategy.

Crescent Energy

My own idea would be to sell U.S. Energy and buy Crescent Energy ( CRGY ). Both companies are currently out of favor. But Crescent Energy is much larger and able to therefore extract a better price as a larger bargainer.

This company combines the skills of well-known investor John Goff and KKR. These two entities have a very long history that can be easily verified.

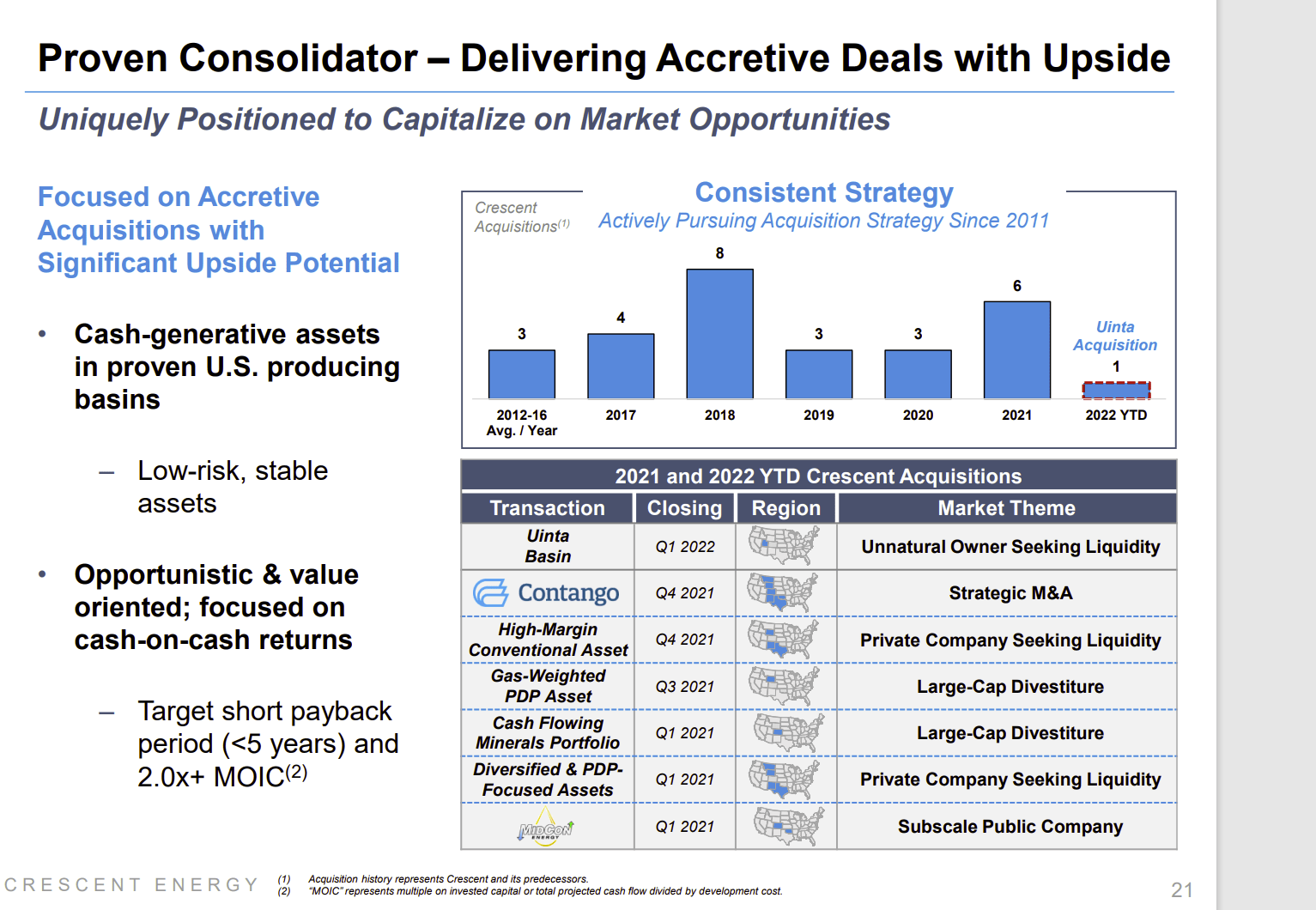

Crescent Energy Consolidator Strategy (Crescent Energy Third Quarter 2022, Earnings Conference Call Slides)

{kind=link}

The result of the combination of the two is a far larger company able to do bigger deals often with a very large discount. The individual holdings throughout the United States are large enough to be marketable.

But the reputation of the two main backing parties combined with more liquidity through more marketable holdings helps to prevent downside issues. Small companies on the OTC market can become extremely cheap due to marketability issues and liquidity of the stock. Then they can stay cheap for a very long time as well. That is unlikely to happen with Crescent Energy.

The NYSE listing assures a reasonable amount of liquidity for the stock and the reputation of both backers is very hard to match. The experience of both is world class level. The main reason they combined forces was to go after big deals in a market that favors buyers.

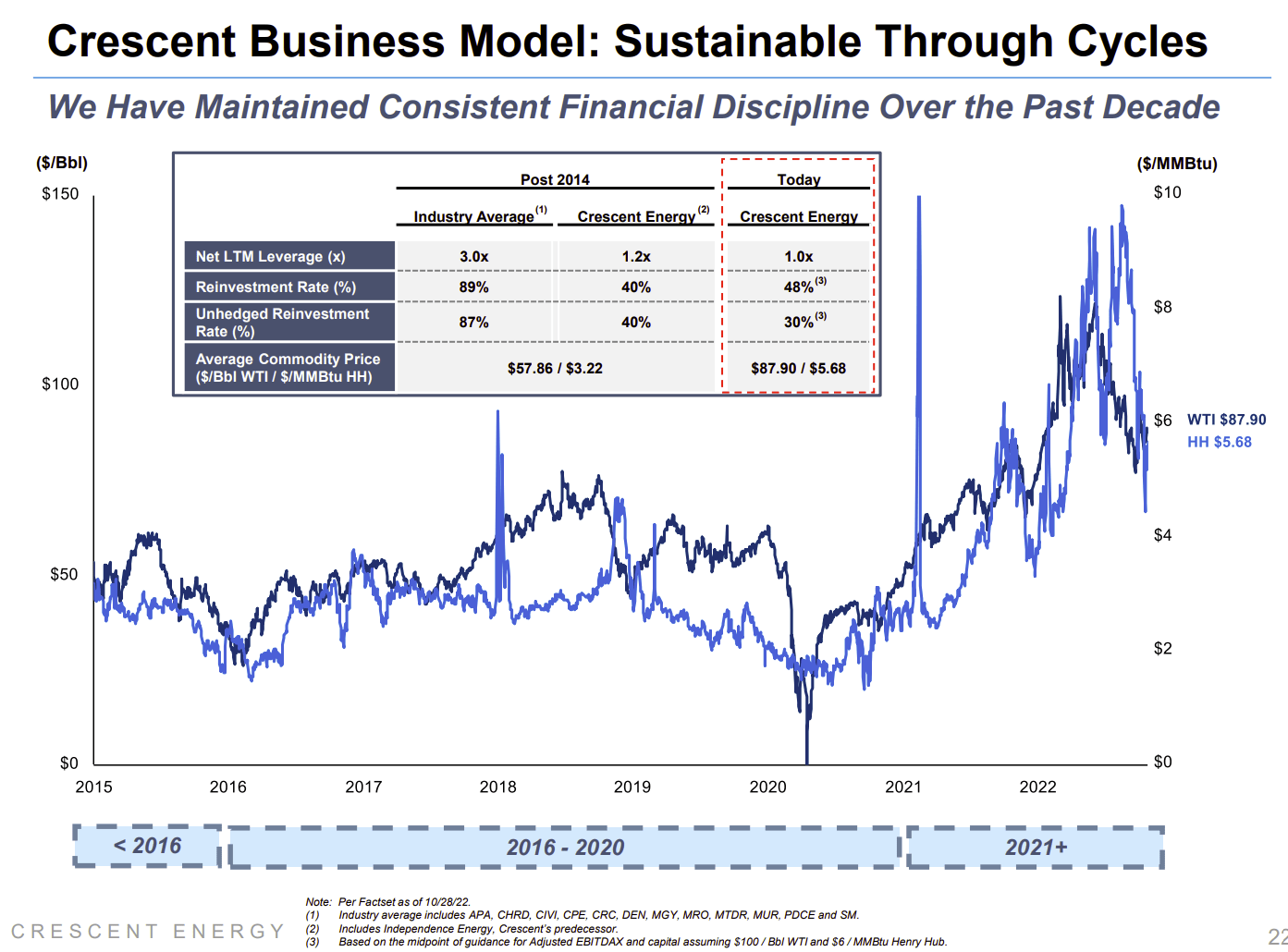

Crescent Energy Business Model Highlights (Crescent Energy Third Quarter 2022, Earnings Conference Call Slides)

{kind=link}

The faith in the "cheap assets available strategy" is shown by the atypically lower financial leverage. KKR (Kolberg, Kravis, and Roberts) is known for making leveraged buyouts. But that strategy crashed and burned in fiscal years 2015-2020 when it came to oil and gas. So, this time around, debt will be conservative, and the money will be made by purchasing bargains.

Investors very seldom get the chance to invest alongside KKR and John Goff. This is one of those rare times. It can be done to get really decent cash flow at the current price. Currently management shows about $7 billion of proved reserves to go with a market cap in the $2 billion range.

Cash flow from operating activities in the latest quarter was roughly $140 million. It doubled from the previous fiscal year. That figure is likely to climb as the hedging program approaches the market prices.

This company has an extremely experienced acquisition team that has made money before. It is very likely to make a lot of money for shareholders in the future. To me there is far less risk with Crescent Energy than with U.S. Energy.

For further details see:

Sell U.S. Energy Buy Crescent Energy