WPC - Sell W.P. Carey And Buy These 2 REITs Instead In 2024

2024-01-02 17:33:09 ET

Summary

- The Magnificent 7 took the lead in market returns throughout 2023, leaving REITs far behind in their rearview.

- With falling inflation, impending rate cuts, and a potential GDP slowdown, I'm expecting 2024 will lead to a REIT recovery.

- Even after the year-end rally, numerous REITs are trading at decade-low valuations, offering a compelling opportunity for investors seeking income and dividend growth.

- Let me show you why not all REITs are created equal, and why I sold my W.P. Carey shares to buy other REITs instead.

Market forecasting always comes with its share of hits and misses, but 2023 was a standout for all the wrong reasons.

Predictions of a recession hitting by the third or fourth quarter fell way off the mark. Instead, major indices soared to record highs, and the job market remained robust throughout the year.

Returns were impressive across the board in 2023:

- S&P 500 returned 24.8%

- NASDAQ 100 returned 54.8%, one of its best years ever

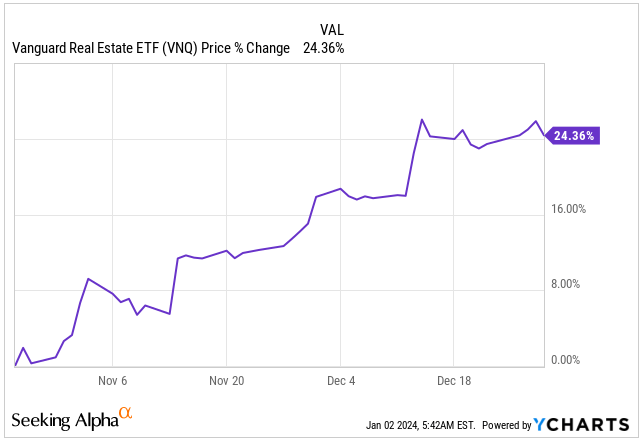

- Vanguard Real Estate ( VNQ ) returned 7.1%

What really stood out, though, was how heavily top-heavy indexes like the S&P 500 became.

A handful of tech giants - the 'Magnificent 7' - started the year making up 19% of the S&P 500 but ended up dominating at 30%. It's unprecedented how much these seven stocks influenced the index, driving a whopping 70% of its total returns for the year.

While I am overweight on many of the Magnificent 7 stocks in my portfolio, I don't anticipate similarly exceptional performance in 2024.

Given that 2024 will most likely be characterized by falling inflation alongside the Fed's pivot and a potential slowdown in GDP growth, I foresee REITs outperforming the market.

Currently, REITs remain attractively priced, trading at levels close to their lowest valuations in decades.

However, the conclusion of 2023 has been characterized by the year-end rally, implying the reversal has already commenced, signaling that the opportunity window is likely closing.

{kind=link}

Price Change (Seeking Alpha)

Investors who took advantage of the market's mispricing of REITs are already sitting on substantial gains. However, I believe that the ongoing low valuation continues to offer a compelling investment opportunity even after the run-up.

Yet, not all REITs are created equal. Let me explain why I disposed of my W.P. Carey stake and which REITs I am buying instead.

Realty Income ( O ) - Strong Buy - Potential Annual Return of 22%

I previously analyzed Realty Income in depth back in November, examining its suitability as an investment for younger individuals with a 30+ year investment horizon.

You can find the article here .

Since the article was published, Realty Income has delivered a return of 9.75%, surpassing the market by over 4%.

This REIT specializes in well-diversified single-tenant properties using triple-net leases , shifting responsibilities for taxes, insurance, and maintenance to the tenant.

The effectiveness of this leasing structure heavily relies on thoroughly evaluating potential tenants, given its substantial long-term financial commitment.

Retailers in discretionary markets, like fashion retail, usually don't meet the criteria. Instead, ideal tenants operate in defensive industries that demonstrate resilience to economic cycles—such as drugstores, dollar stores, or convenience stores.

Ensuring tenant diversification is crucial for stability in any REIT.

Realty Income prides itself on a diversified portfolio , with no single tenant exceeding 5%. Its top 10 clients make up 27.1% of the portfolio, with key tenants like Walgreens ( WBA ) at 3.8%, Dollar General ( DG ) at 3.8%, and Dollar Tree ( DLTR ) at 3.3%.

Client Diversification (O IR)

Additionally, about 41% of its tenants represent investment-grade credit companies, signaling a lower risk of default.

Realty Income's consistent occupancy rate is particularly noteworthy, averaging 98.2% over the past two decades, significantly surpassing the average REIT median of approximately 94.2%.

Many are familiar with Realty Income as the "monthly dividend company," and with its current 5.36% dividend yield, it lives up to that reputation. Since 1994, it has steadily increased its dividend at a rate of 4.3% CAGR, now standing at $0.256 monthly.

Over the past 20 years, Realty Income has seen a 5.4% growth in its FFO. While not the most rapid growth, it's worth noting that over the last five years, this growth has actually accelerated to 6.6%.

Looking ahead, a growth rate of around 3% to 4% seems reasonable to expect.

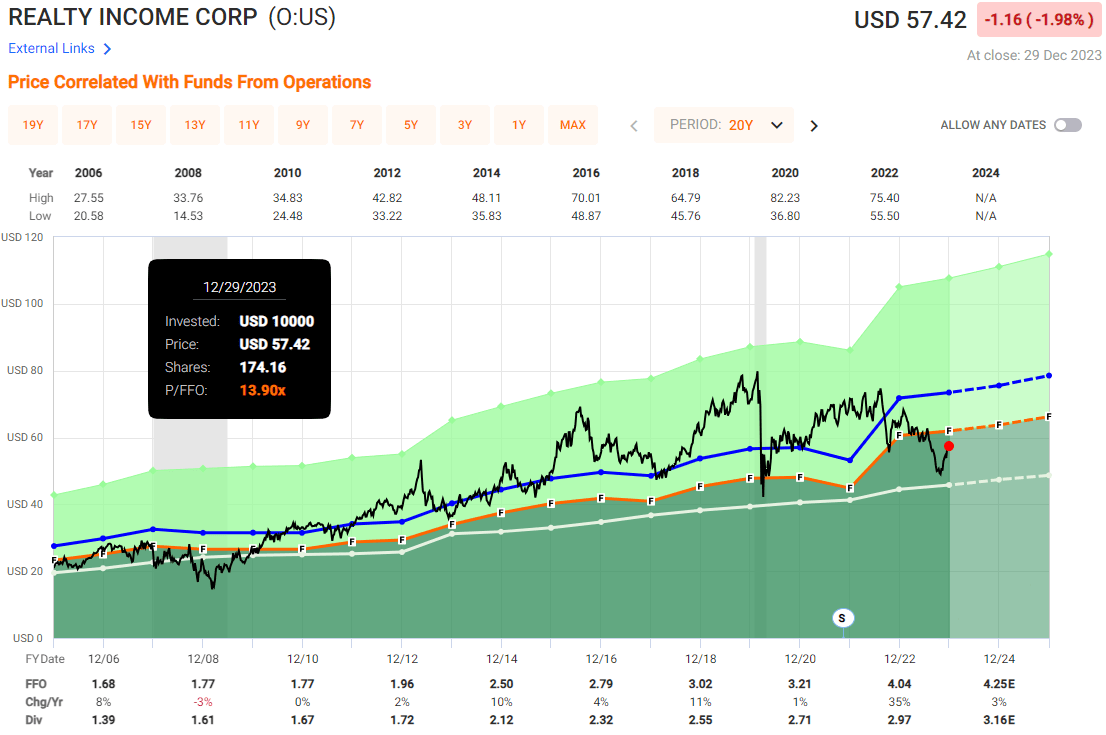

This leads me to emphasize that while Realty Income might not experience the fastest growth ahead, its strength lies in its valuation .

Currently, the REIT is trading at 13.9x its FFO. However, considering the company has historically traded at a premium, the normalized valuation over the past two decades has been around 19.17x its FFO.

Despite the 17% rally in the price since its low in October when the REIT hit a low of 11.91x its FFO, it is still trading at a 38% discount compared to its historical valuation.

{kind=link}

Realty Income Valuation (Fast Graphs)

It might be wise not to anticipate a return to its original premium valuation, even with the Fed's pivot in 2024, as I don't foresee rates dropping to their 2020-2021 levels.

However, even if we consider even a bit more pessimistic valuation of 18x its FFO, we could expect an annualized return of 22.3% over the next two years, hence my strong buy conviction.

{kind=link}

Potential Return (Fast Graphs)

Vonovia ( OTCPK:VONOY ) - Strong Buy - Potential Annual Return of 30%

For those not familiar, Vonovia is a leading German real estate company specializing in residential properties with over 540.000 residential units.

It's also one of Europe's largest landlords, managing, developing, and renting out apartments.

With a vast portfolio across Germany, Austria and Sweden, Vonovia focuses on providing housing solutions, but also offering a range of services from property management to modernization and sustainability initiatives.

Revenue by Geography (VONOY IR)

To put its size in perspective in comparison to US REITs, Vonovia boasts a market cap of $25.7 billion. While it ranks among Europe's largest REITs, it would hold the 10th position in the US, just behind VICI Properties ( VICI ).

Vonovia's portfolio is valued at approximately €85 billion, offering an appealing blend of development, management, services, and more. Presently trading at $15.70, Vonovia's stock plummeted to as low as $8.20 during the 2023 pullback, facing a lack of enthusiasm.

While Vonovia has seen heightened volatility over the past three years, especially during times when REITs weren't favored, it's crucial to grasp the landscape of European real estate first.

{kind=link}

Price Change (Seeking Alpha)

Vonovia went public in 2013, stemming from the merger between Deutsche Annington and GAGFAH. It transformed into Vonovia SE and has been listed on the Frankfurt Stock Exchange since then.

This period was opportune for real estate companies that heavily relied on debt for operations and frequently issued new shares for financing, thereby diluting existing shareholders.

While interest rates remained generally low across the developed world throughout the 2010s, the European Central Bank (ECB) chose to drive rates into negative territory in 2015 to combat inflation, which had fallen well below the 2% target, and stimulate growth.

These negative rates persisted until 2022, allowing real estate companies to borrow at minimal costs, with interest expenses posing no significant challenges.

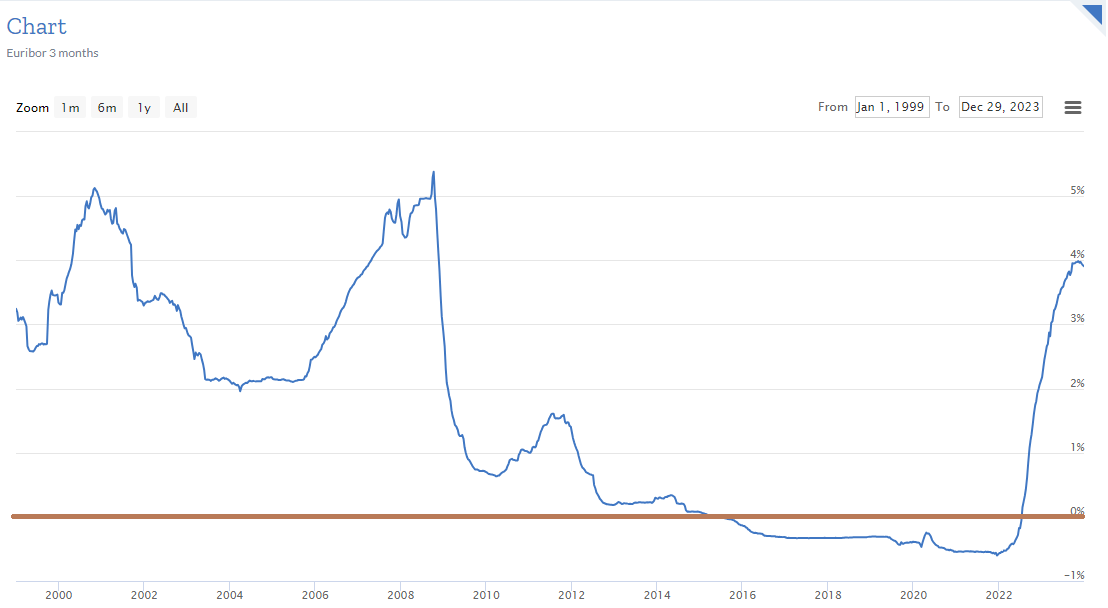

However, reality isn't a fairy tale, and rates have surged close to 4%, specifically the 3-month Euribor. This sudden shift led to a decline in the value of existing properties and made refinancing existing debt considerably more expensive, consequently causing a drop in the stock price.

{kind=link}

3-month Euribor (Euribor Rates)

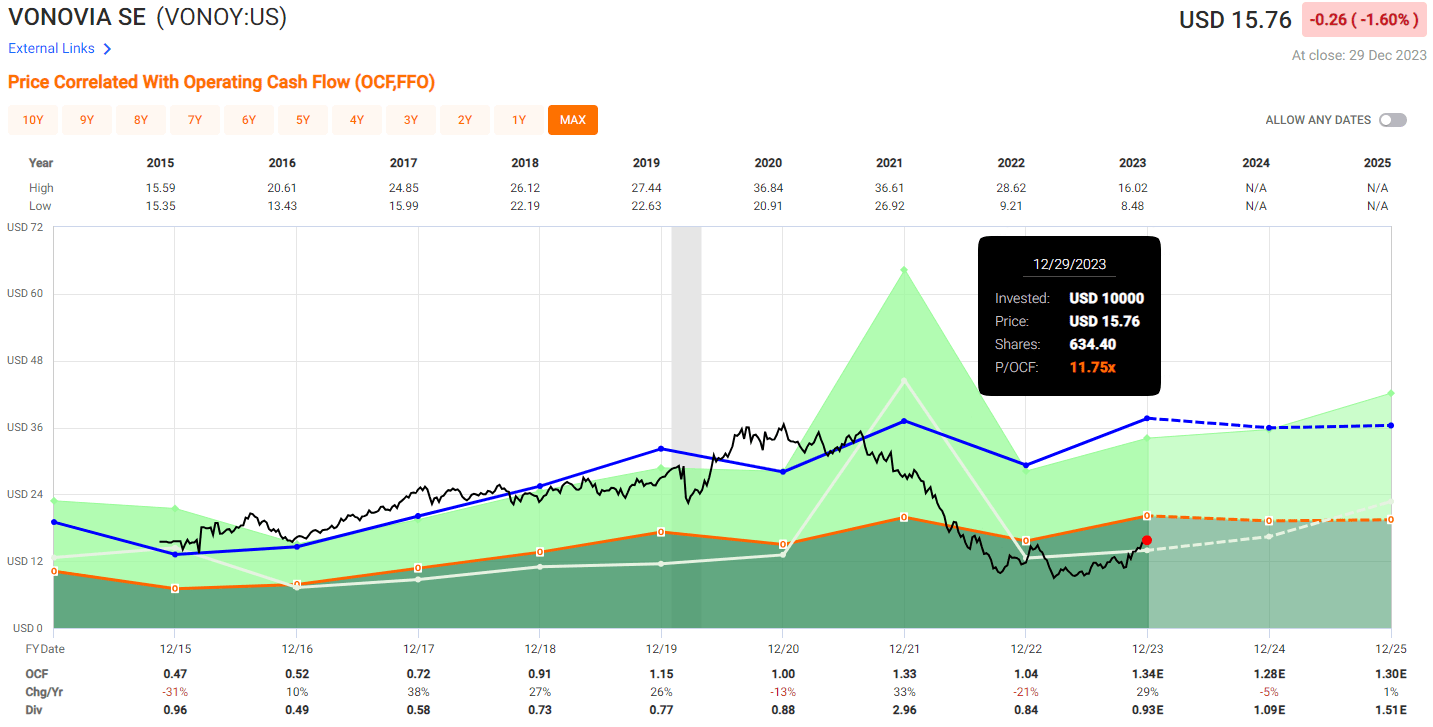

While German property prices have seen an average decline of 10% since the hiking cycle began, the bears have driven the valuation to as low as 0.3x its NAV at its lowest point.

Despite the stock rising by 49% since October 2023, the NAV currently sits at roughly 0.6x, indicating a considerable discount to its book value.

Traditionally, Vonovia traded around its NAV, albeit during a period of significantly lower interest rates in the eurozone. However, Vonovia is anticipated to benefit from accelerated rental growth in the coming years due to Germany's unique system, which regulates rent.

Considering the acute shortage of residential apartments in Germany, especially in major cities, rising demand from immigrants like the Ukraine war refugees, and high construction costs, I anticipate property prices in Germany to rebound over the next 2-3 years, leading Vonovia to trade at its fair value once again.

Keep in mind, Vonovia has a BBB+ rated balance sheet, benefitting from strong tailwinds such as increasing rents and land scarcity in Germany and across various European nations.

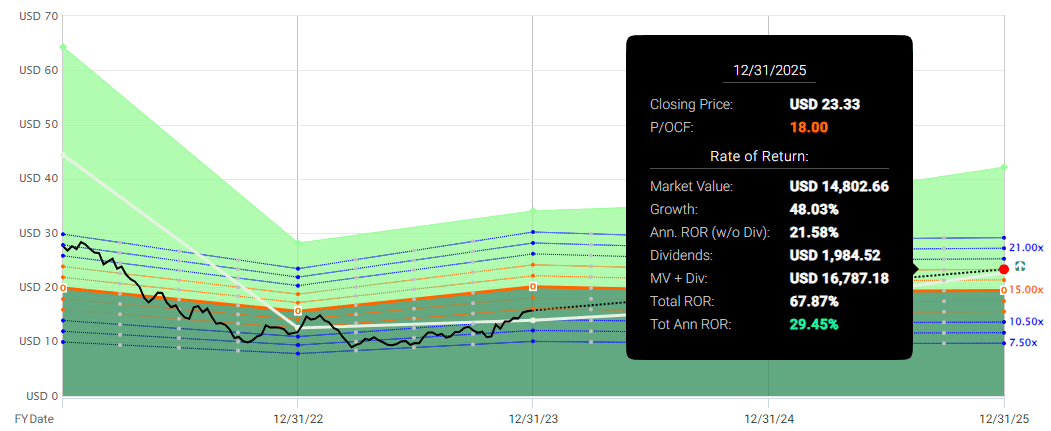

Since 2015, Vonovia has managed to grow its OCF at a rate of 6.1%, and the normalized P/OCF ratio has been 28.1x. However, it's currently trading at only 11.75x.

{kind=link}

Vonovia Valuation (Fast Graphs)

While it's unrealistic to anticipate the eurozone returning to negative rates in the near future, it's reasonable to expect that when the ECB begins cutting rates in 2024 and the real estate market in Germany rebounds, the stock could trade around 18x P/OCF again.

Given that scenario, we could anticipate nearly 30% annualized returns up until 2025, hence the strong buy .

{kind=link}

Potential Return (Fast Graphs)

W.P. Carey ( WPC ) - Sell - Potential Annual Return of 6.5%

I believe I won't be alone in expressing disappointment in W.P. Carey's 2023 performance, particularly the ill-timed office spin-off. This, in my view, signifies poor management decisions alongside the dividend reduction.

This investment has resulted in a loss of over 20% for me. Given the lack of growth and perceived poor management, I've opted to sever ties rather than continue holding onto this company.

Typically, a dividend cut spells bad news for shareholders, often causing a drop in a company's share price upon announcement. However, it's not always a straightforward scenario.

Take Vonovia, which I have just covered above for instance, which also cut its dividend in 2023.

I also own a significant portion of another REIT, Prologis ( PLD ), which slashed its dividend in 2009. Despite this, it has consistently outperformed the market and emerged as the largest REIT globally.

Sometimes, cutting dividends helps a company regain financial stability or invest in its business rather than sustaining an unsustainable dividend at all costs.

I initially considered W.P. Carey ( WPC ) as one of the safest dividend stocks, an investment for the long haul. However, my perspective has drastically changed as its flagship asset "dividend" took a hit, leaving the company with little else to offer.

WPC's decision to spin off its office assets, similar to Realty Income's past move with Orion Office ( ONL ), resulted in WPC's spin-off called Net Lease Office Properties ( NLOP ).

WPC now operates with a notably smaller portfolio of office properties, a strategy management believes will boost shares to trade at a higher FFO multiple.

However, I completely disagree with this approach. If WPC's crown jewel is its dividend, a major draw for investors, removing that core aspect could upset shareholders.

Furthermore, WPC's FFO growth has been sluggish, averaging a mere 3.4% annually over 20 years and dwindling to 1.4% in the last decade.

Additionally, WPC is using it as an opportunity to "reset", with the intention of paying out 70-75% of AFFO, which led to reducing the dividend by 19.7% to $0.86 per share from the prior $1.07.

Bear in mind that WPC had raised its dividend before deciding to cut it. This action directly contradicts the adage that the safest dividend is the one that was recently increased.

While some argue that shareholders will receive dividends from the spun-off office REIT, there's a significant caveat. The transaction incurred $46.8 million in fees, leaving investors with inadequate shares to compensate for the lost dividends.

In my view, the spin-off won't drive higher FFO growth, and management appears to be betting on the market forgetting the dividend cut and revaluing the company at higher multiples based solely on hope.

I firmly believe that valuation should be earned through robust and well-managed growth, rather than gambling on market inefficiencies.

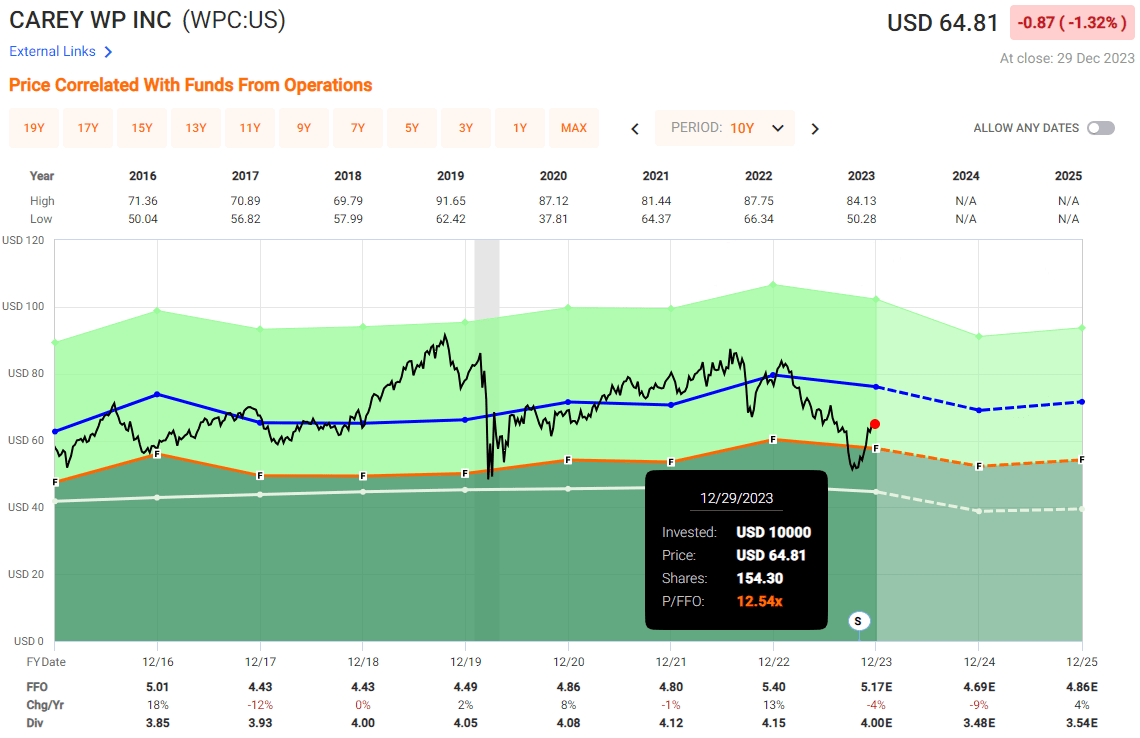

{kind=link}

WPC Valuation (Fast Graphs)

Considering this, WPC currently holds a BBB+ rated balance sheet and is trading at 12.5x its FFO, not far from its 20-year average of 14.7x its FFO.

However, I anticipate that the company won't revert to trading at its historical FFO.

Instead, it might trade around 13.5x FFO, suggesting an annualized rate of return of approximately 6.5%, hence the sell rating .

In my view, this return seems too low when gauged against other opportunities in the REIT market today as shown in this article.

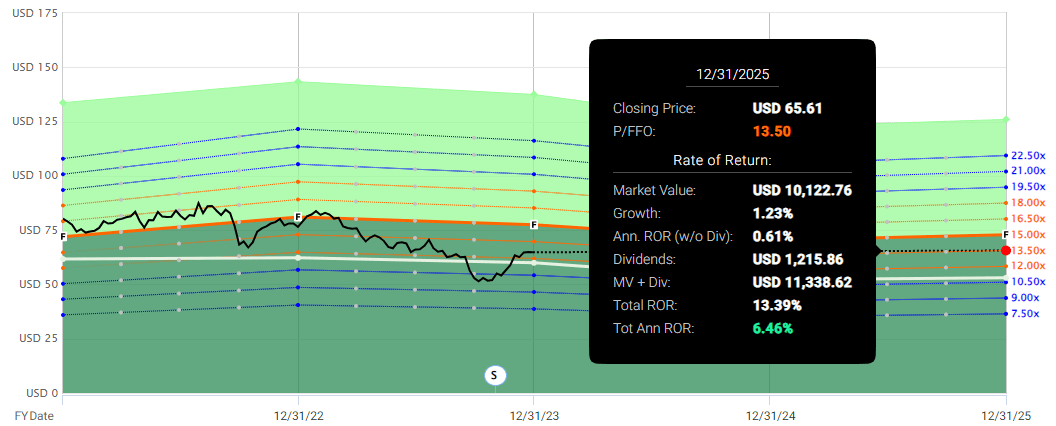

{kind=link}

Potential Return (Fast Graphs)

Takeaway

As the Fed and ECB rates reached their peaks, 2023 proved challenging for REITs, witnessing most companies trading in negative territory for the year.

However, a year-end rally triggered by the Fed's optimistic outlook and indications of first rate cuts due to declining inflation and slower growth led to revaluation, causing many REITs to soar.

Despite this rally, most REITs continue to trade at historically low valuations, presenting compelling opportunities for investors seeking reliable income or dividend growth.

Heading into 2024, I anticipate REITs will outperform the market and even the Magnificent 7.

However, not all REITs are created equal. After W.P. Carey's office spin-off and management deciding to cut its dividend, its main 'crown jewel' and reputation suffered, eroding my trust in this slow-growing REIT.

As a result, I divested my stake in W.P. Carey to purchase Realty Income and Vonovia instead. These alternatives offer more enticing opportunities with significantly higher return potentials while maintaining similar risk profiles.

For further details see:

Sell W.P. Carey And Buy These 2 REITs Instead In 2024