SRE - Sempra: A Well-Financed And Diverse SWAN Stock

2023-06-26 18:02:59 ET

Summary

- Sempra is one of the largest regulated utilities in the nation, serving both California and Texas.

- The company typically enjoys remarkably stable cash flows that are unaffected by problems in the economy.

- The company is positioned to deliver a 9% to 11% total average annual return going forward.

- The balance sheet is very strong, but TTM dividend coverage is very weak. This should be a one-off problem, though.

- The valuation is questionable, but Sempra is probably still worth taking a shot at.

Sempra ( SRE ) is an American regulated electric and natural gas utility that primarily operates in the states of California and Texas. This is almost certainly somewhat surprising as those two states could not be any less in common. However, the company still boasts many of the same characteristics as other utilities that have generally caused the sector to be a favorite of conservative investors, such as retirees. Most notably, Sempra enjoys remarkably stable cash flows over time, which could be a very appealing trait given the economic certainty that plagues the economy as we prepare to enter the second half of the year. The company also boasts a very attractive 3.31% dividend yield that is obviously well above many other things in the market.

Unfortunately, Sempra is a bit more expensive than many of its peers, which is unusual for a natural gas utility considering that many in the market believe that natural gas will be obsolete in the near future. While it is highly unlikely that natural gas will be supplanted as a fuel for heating homes and businesses anytime prior to 2050, even in California, the company's high valuation still means that investors will want to be cautious before entering or adding to a position.

About Sempra

As stated in the introduction, Sempra is a regulated electric and natural gas utility that primarily operates in California and Texas. The company is headquartered in San Diego, California, and primarily serves the San Diego area, although it also acts as the primary natural gas utility in Southern California through its Southern California Gas Company utility (SoCalGas). The company also owns Oncor Electric Delivery Company, which is the largest electric utility in the state of Texas. As Southern California and Texas are among the most populated regions of the United States, we can likely guess that Sempra is one of the largest utilities nationwide in terms of customer count. This is certainly the case, as the company provides its services to more than forty million customers. However, as I have pointed out in various previous articles, the overall size of a utility does not affect its defining characteristics.

The most important characteristic possessed by Sempra is that it has remarkably stable cash flows over time. We can see this quite clearly by looking at the company's operating cash flows. Here they are for each of the past eleven twelve-month periods:

{kind=link}

This is a period of time that includes multiple economic environments. For example, the early periods shown in the chart above include the pandemic lockdowns, which were quite severe in California. We also see the recovery period, the inflationary period of 2021 and 2022, as well as the monetary tightening that started weakening the economy starting last year. As we can clearly see, none of these had much of an impact on the company's operating cash flows.

In fact, the only event that did have an impact on the company's cash flow performance was the warm winter of 2023. The fact that this will affect the company should not be surprising considering that Sempra is primarily a natural gas utility. The primary use of utility-supplied natural gas is as a heating fuel for homes and businesses, so naturally, consumption is going to be a lot less during a warm winter than a more normal one. That means lower utility bills and less revenue that the company can use to cover its expenses. We saw just about every utility with a presence in the natural gas space experience lower-than-normal operating cash flows over the most recent winter so Sempra is hardly alone in this.

Fortunately, the unnaturally warm weather that we saw this winter is unlikely to be a permanent fixture so we should see the company's operating cash flows return to their normal levels of just under $4 billion annually in the near future.

The reason for this overall stability is that Sempra provides a product that most people consider to be a necessity for our modern way of life. After all, there are not very many people in the United States that do not have electricity in their homes or businesses. In the case of those people that have natural gas heat, they likewise will consider natural gas to be a necessity due to the simple fact that nobody wants to be without heat in the winter. As such, most people will prioritize paying their utility bills ahead of making discretionary expenses during periods in which money gets tight. This is something that could be very important today, since high inflation and declining real wages have ravaged the average household's finances (see here and here ).

The Federal Reserve's economists are currently unanimously predicting that a recession will occur during the second half of this year, which will deliver another negative blow to consumer finances. As such, it could be a good idea to have at least part of your portfolio invested in a company that will not be adversely impacted by weakness in the economy or in the American consumer. Sempra could be a good choice to serve as this sleep-well-at-night position.

Growth Prospects

Naturally, as investors, we are unlikely to be satisfied with mere stability. We like to see any company in which we are invested grow and prosper with the passage of time. Fortunately, Sempra is well-positioned to deliver forward growth. There are two ways through which the company can accomplish this:

- Population Growth Of The Service Territory

- Rate Base Growth.

We will discuss each of these in turn.

Population Growth

As just mentioned, one of the ways in which Sempra can generate growth is by increasing its customer base. After all, the more people that it services and the more people that are paying their monthly utility bills, the more revenue that the company will bring in. That means that the company will have more money available to cover its fixed expenses and make its way down to the bottom line.

Unfortunately, Sempra is a regulated utility and one of the characteristics of these companies is that they are monopolies that have pre-defined service territories. As a result, Sempra cannot simply expand into other areas to get more customers. It is instead dependent on the population growth of its service territory and this is entirely out of the company's control. This poses an interesting conundrum for the company because Texas and California have very different demographics.

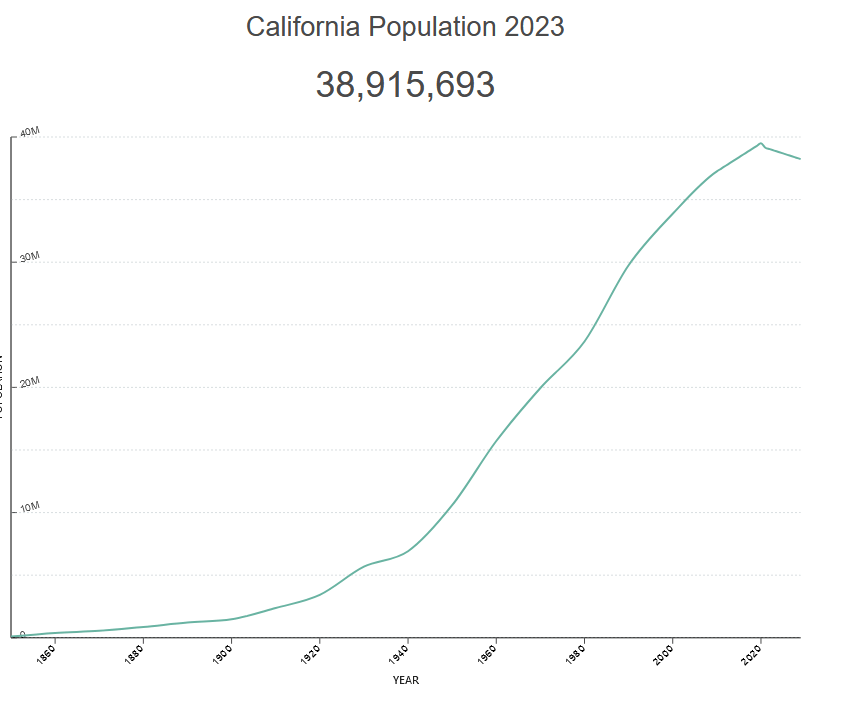

In the case of California, people have been leaving the state in huge numbers. Anecdotally, U-Haul Holding Company ( UHAL ) has had shortages of trucks in Southern California because people are renting trucks to leave the state in much greater numbers than people renting trucks to move into California. The state's population peaked in 2020 and has been declining ever since:

{kind=link}

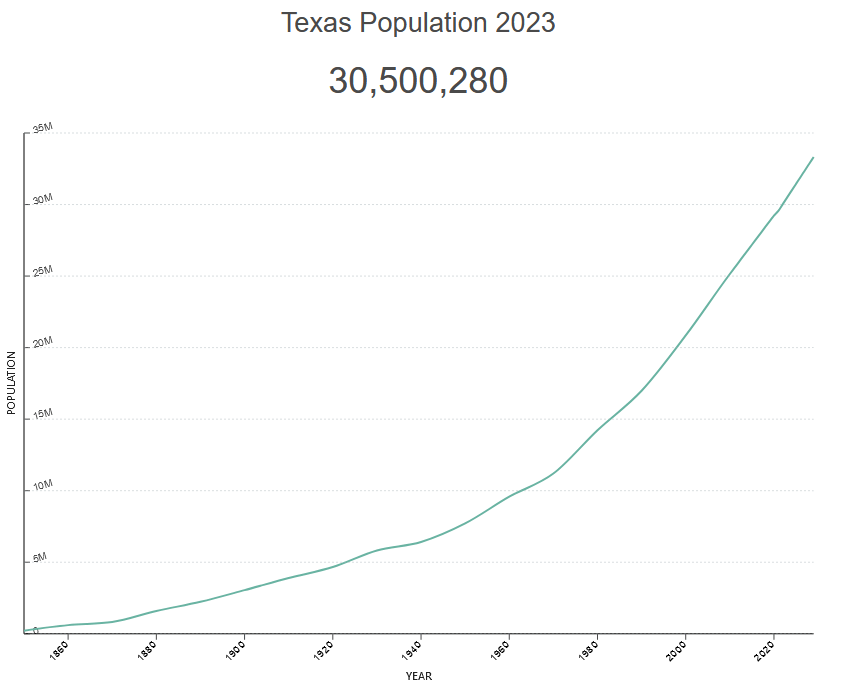

We see the exact opposite in Texas. The Lone Star State has been steadily gaining people since 2020:

{kind=link}

We can debate all day about the reason for this apparent migration, but frankly, that is irrelevant to our purposes today. The important thing is that one of the states that Sempra serves is losing population but the other is gaining population. This actually puts Sempra in a much better position than most California utilities because it is at least able to partially offset some of the adverse impacts of the declining population in California because it can still add customers in Texas.

Rate Base Growth

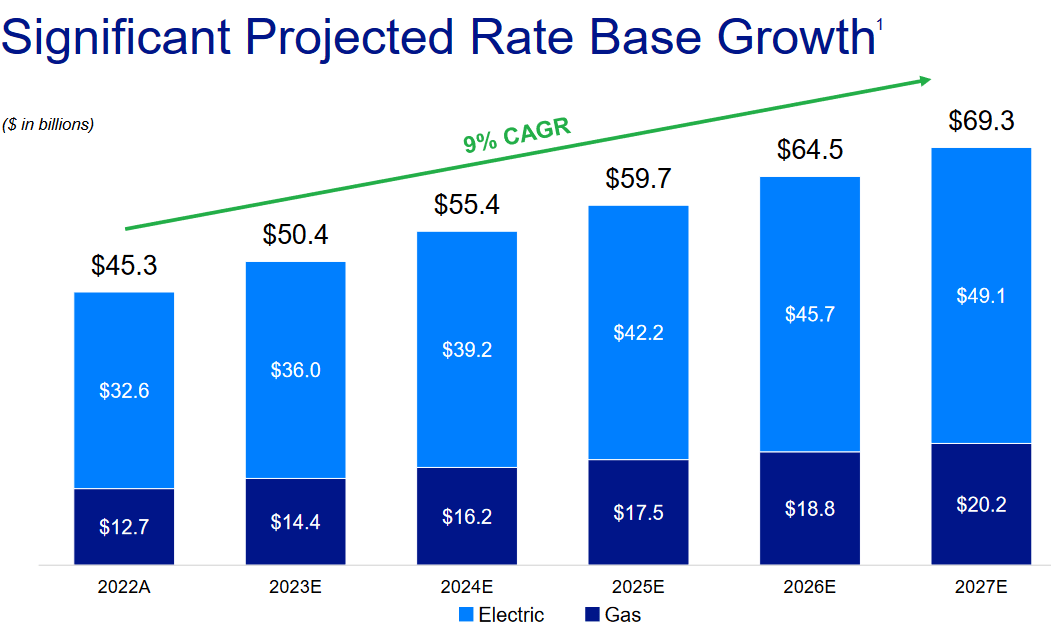

The second way through which Sempra can achieve earnings growth is by increasing its rate base. The rate base is the value of the company's assets upon which regulators allow it to earn a specified rate of return. As this rate of return is a percentage, any increase to the rate base allows the company to increase the price that it charges its customers in order to earn this specified rate of return. The usual way that a utility will grow its rate base is by investing money into upgrading, modernizing, and possibly even expanding its utility-grade infrastructure. Sempra is planning to do exactly this as the company plans to spend approximately $40 billion over the 2023 to 2027 period on this task:

Sempra

The fact that the company has provided its plans through 2027 is rather nice. As I have noted in recent articles, not all of its peers have provided information for the full five-year period. The fact that Sempra is providing information aids us in projecting the company's financial performance going forward, which is important for long-term investors as it allows us to make an educated guess about where the company will be on a given date.

Sempra's plan as outlined should allow the company to grow its rate base at a 9% compound annual growth rate through 2027:

{kind=link}

This is a much greater rate base growth than many of the company's peers have projected over the same period. That should be appealing at first glance, but remember that Sempra has to finance the capital expenditures that are required to make this happen. This will require the company to issue both debt and equity. The equity issuance will unfortunately dilute some of the growth that the shareholders would otherwise receive. We can see this impact in the fact that the company is only projecting 6% to 8% earnings per share growth rate over the same period.

When we combine this with the company's current 3.31% dividend yield, we get a projected total return of 9% to 11% annually over the next five years. That is very reasonable for a utility stock as these companies tend to be more stable than high-growth stocks, but have lower returns.

Financial Considerations

It is always important to analyze the way that a company finances its operations before making an investment in it. This is because debt is a riskier way to finance a company than equity because debt must be repaid at maturity. That is usually accomplished by issuing new debt and using the proceeds to repay the existing debt. After all, very few companies have the ability to completely pay off their debt with cash as it matures. As new debt is issued with an interest rate that corresponds to the market interest rate at the time of issuance, this process can cause a company's interest expenses to increase following the rollover in certain market conditions. As of the time of writing, interest rates in the United States are at the highest levels that we have seen since 2007 so this is a very real concern today.

In addition to interest-rate risk, a company must make regular payments on its debt if it is to remain solvent. Thus, an event that causes a company's cash flow to decline could push it into financial distress if it has too much debt. While utilities like Sempra tend to have remarkably stable cash flows, this is still a risk that we should not ignore as there have been bankruptcies in the sector before.

One metric that we can use to analyze a company's financial structure is the net debt-to-equity ratio. This ratio tells us the degree to which a company is financing its operations with debt as opposed to wholly-owned funds. It also tells us how well the company's equity will cover its debt obligations in the event of bankruptcy or liquidation, which is arguably more important.

As of March 31, 2023, Sempra had a net debt of $29.270 billion compared to $30.245 billion in shareholders' equity. This gives the company a net debt-to-equity ratio of 0.97 today. This is fairly low for a utility, as these companies usually rely heavily on debt to finance their operations. Here is how Sempra compares to some of its peers:

| Company |

| Net Debt-to-Equity Ratio |

| Sempra |

| 0.97 |

| Entergy Corporation ( ETR ) |

| 1.91 |

| NiSource, Inc. ( NI ) |

| 1.43 |

| Edison International ( EIX ) |

| 1.93 |

| Atmos Energy ( ATO ) |

| 0.62 |

As we can see, many of the company's peers employ more debt than equity in their financial structure. The fact that Sempra's equity exceeds its total debt is thus somewhat unique in the sector. It does mean though that the company has a substantially stronger balance sheet than any of its peers. This is a good position for the company to be in from an investment standpoint since it should reduce our risks somewhat. Overall, there is nothing to complain about here.

Dividend Analysis

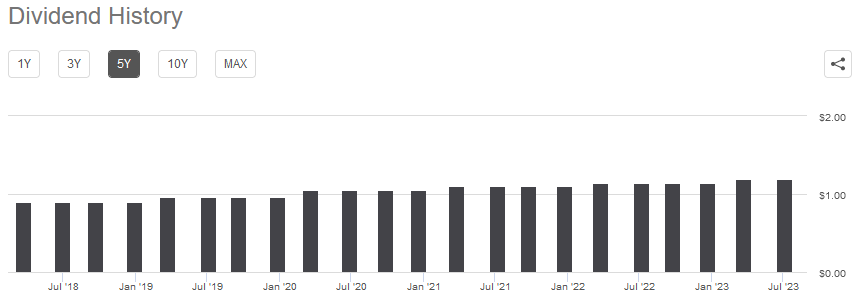

One of the biggest reasons why investors purchase shares of utility stocks is that they tend to have a higher dividend yield than just about anything else in the market. This comes from the fact that these companies have fairly low growth rates so they do not have the capital gains potential of companies in other sectors. They compensate by paying out a large percentage of their cash flows to the investors in order to provide an investment return and since their stocks are not assigned huge multiples, the dividend ends up being a significant percentage of the stock price. Sempra is certainly no exception to this as the stock yields 3.31% at the current share price. The company also has a long history of raising its dividend on an annual basis:

{kind=link}

The fact that the company increases its dividend regularly is something that is quite attractive during inflationary environments, such as the one that we are experiencing today. This is because inflation is constantly reducing the number of goods and services that we can purchase with the dividend that the company pays out. This can make it seem as though an investor is getting poorer and poorer with the passage of time, particularly if that person is depending on their portfolio for the income that they need to live. The fact that the company increases its dividend on an annual basis helps to offset this effect and ensures that the dividend maintains its purchasing power over time.

As is always the case though, we want to ensure that the company can actually afford the dividends that it pays out. After all, we do not want to be the victims of a dividend cut since that would reduce our incomes and almost certainly cause the stock price to decline.

The usual method that we use to judge a company's ability to cover its debt is looking at its free cash flow. The free cash flow is the amount of cash that was generated by the company's ordinary operations and is left over after the company pays all of its bills and makes all necessary capital expenditures. This is the money that can be used for things that benefit the shareholders, such as reducing debt, buying back stock, or paying a dividend. In the twelve-month period that ended on March 31, 2023, Sempra had a negative levered free cash flow of $4.3341 billion. That was obviously not enough to pay any dividends, yet the company still paid out $1.485 billion to its shareholders during the period. At first glance, this is likely to be concerning as Sempra can clearly not afford to pay its dividend out of free cash flow.

However, it is not uncommon for a utility to finance its capital expenditures through the issuance of debt and equity. The company will then pay its dividends out of operating cash flow. This is done because it is extremely expensive to construct and maintain utility-grade infrastructure over a wide geographic area and these costs would prevent a utility from ever giving investors a return if they had to be paid entirely out of cash flow. During the most recent trailing twelve-month period, Sempra had an operating cash flow of $1.515 billion. That was barely enough to cover the $1.485 billion that the company paid out in dividends during the period. That is quite concerning, but keep in mind that the most recent period saw the company's cash flow come in a lot weaker than normal for reasons that were already discussed.

For the past few years, Sempra has been averaging an operating cash flow of $3 billion to $4 billion annually. Thus, it can normally cover its dividends with a significant amount of money left over for other purposes. For the most part, the company's dividend is probably sustainable but we will want to keep watching its cash flow to make sure that it does indeed recover going forward.

Valuation

It is always critical that we do not overpay for any asset in our portfolios. This is because overpaying for any asset is a surefire way to earn a suboptimal return on that asset. In the case of a utility like Sempra, we can value it by looking at the price-to-earnings growth ratio. This ratio is a modified version of the familiar price-to-earnings ratio that takes a company's forward earnings per share into account. A price-to-earnings growth ratio of less than 1.0 is a sign that the stock may be undervalued relative to its forward earnings per share growth and vice versa. Unfortunately, there are very few stocks that are undervalued relative to their earnings growth, particularly in today's overheated market . As such, the best way to use this ratio is to compare Sempra to its peers in order to determine which company has the most attractive relative valuation.

According to Zacks Investment Research , Sempra will grow its earnings per share at a 4.80% rate over the next three to five years. That seems very low considering the company's rate base growth over the same period. The Zacks earnings growth estimate gives us a price-to-earnings growth ratio of 3.33 at the current stock price. That is a bit expensive compared to its peers:

| Company |

| PEG Ratio |

| Sempra |

| 3.33 |

| Entergy Corporation |

| 2.56 |

| NiSource, Inc. |

| 2.39 |

| Edison International |

| 3.75 |

| Atmos Energy |

| 2.54 |

We can clearly see here that several of the company's peers appear to be much more attractively valued than Sempra. However, this is using the Zacks earnings per share estimate, which as we have already mentioned seems a bit low as its 9% rate base growth should deliver earnings per share growth of at least 6% over the three- to five-year period in question. A 6% growth rate reduces the price-to-earnings growth ratio to 2.67 at the current stock price, which is pretty reasonable compared to its peers. If the company manages to achieve higher than 6% growth then it starts looking comparatively cheap relative to its peers. Thus, it might still make sense to purchase the shares at the current price.

Conclusion

In conclusion, Sempra is a rather interesting utility, as its exposure to both California and Texas gives it exposure to states with two very different fundamentals. The company has reasonable growth prospects as its rate base is likely to grow at a very good rate, driving the company's forward earnings per share growth. When we combine this with a very strong balance sheet , we see a lot to like. The only two problems here are that the dividend coverage is weak and the company might be overvalued. However, both of these may also be non-issues as the dividend coverage should revert to normal over the near term and the Zacks earnings estimate seems low. It might be worth taking a position in Sempra stock as a stable dividend play for an uncertain economy.

For further details see:

Sempra: A Well-Financed And Diverse SWAN Stock