SRE - Sempra: Decent For A Weak Economy But Stock Looks Pricey

2023-09-05 11:22:18 ET

Summary

- Sempra is a large regulated electric and natural gas utility serving millions of customers in Southern California and Texas.

- The company's stability and cash flow make it a safe haven investment during an economic downturn.

- Sempra has respectable growth prospects, with plans to increase its customer base and invest in renewable energy infrastructure.

- The company's 3.40% dividend yield appears sustainable and it boasts a very strong balance sheet that should bring benefits if rates stay high.

- The stock appears overvalued relative to its peers right now.

Sempra ( SRE ) is one of the largest regulated electric and natural gas utilities in the United States, serving approximately forty million customers in Southern California and Texas. These are the two most heavily populated states in the nation, especially in the areas around the major cities where Sempra's operations are based. However, as I have pointed out in numerous previous articles, a utility's customer count has little impact on its characteristics. The most important of these characteristics right now is that Sempra should enjoy very stable revenue and cash flow over time, which is very important as the economy is showing signs of weakening. Sempra's stability could thus allow the company to be a safe haven investment for a portfolio until conditions improve. The company's 3.40% dividend yield ensures that any investor will be well-compensated while waiting for better times, although admittedly this yield is not as appealing today as it would have been a year or two ago. The company also has respectable growth prospects, so it is not entirely a yield play.

We last discussed this company back in June, and the thesis was very similar to the one that was just presented. The company's most recent results certainly fit in with our thesis and some macroeconomic events show that the company's safe haven status may be even more needed than it was just a few months ago. Thus, it seems like it is a good time to revisit the company and see how our thesis is playing out.

About Sempra

As stated in the introduction, Sempra is a very large regulated electric and natural gas utility that serves Southern California and Texas. Sempra's service area includes San Diego, California, and much of the surrounding area, which is one of the most populated regions of the United States. San Diego is the eighth-largest city in the United States with a population of approximately 1.39 million, but the company actually serves most of Southern California through SoCal Gas, which is the largest natural gas utility in the area around San Diego and Los Angeles. Sempra also owns the largest utility in Texas, which is the second-most populated state in the nation (after California). This gives the company a very impressive customer number of almost forty million. That is a level that very few American utilities can hope to match.

As mentioned in the introduction though, Sempra's size is not its most important characteristic. The company's most attractive characteristic is its very stable cash flows. This chart shows the company's operating cash flow during the past eleven twelve-month periods:

{kind=link}

As we can clearly see, Sempra's operating cash flow does not usually vary by much from period to period, although it was much lower than normal during the most recent winter. This is something that we have seen all across the utility sector. As I mentioned in a previous blog post , the most recent winter was much warmer than normal across most of the United States. As a result, the consumption of natural gas was not as high as normal. This had a negative impact on the cash flow of most natural gas utilities, and Sempra's SoCal Gas subsidiary is the most important for the company's financial performance. In the first six months of 2023, SoCal Gas had a net income of $515 million, which is higher than any of the company's other major segments:

| Business Segment |

| H1 2023 Net Income |

| % of Total |

| San Diego Gas & Electric |

| $442 |

| 26.50% |

| SoCal Gas |

| $515 |

| 30.88% |

| Sempra Texas |

| $287 |

| 17.21% |

| Sempra Infrastructure |

| $424 |

| 25.42% |

(all figures in millions of U.S. dollars)

In addition to the adverse impacts of lower natural gas consumption compared to usual, Sempra also cites higher interest expenses as a drag on its financial performance compared to earlier quarters, which would reduce the company's operating cash flow. We will discuss this later in this article. The point though is that Sempra derives a significant portion of its cash flow from natural gas and the fact that consumption was lower than normal over the past winter had a negative impact on the company's normal stability. Fortunately, forecasters are projecting that this winter will be somewhat colder than last winter so that should help the company's cash flow get back to its usual twelve-month levels.

In my last article on Sempra, I explained the reason for this general stability:

The reason for this overall stability is that Sempra provides a product that most people consider to be a necessity for our modern way of life. After all, there are not very many people in the United States who do not have electric service to their homes or businesses. In the case of those people who have natural gas heat, they likewise will consider natural gas to be a necessity due to the simple fact that nobody wants to be without heat in the winter. As such, most people will prioritize paying their utility bills ahead of making discretionary expenditures during periods in which money gets tight.

In numerous previous articles, I pointed out that the finances of the average American household appear to be getting very tight. According to a recent report by Lending Club, approximately 61% of American households are now living paycheck-to-paycheck, which represents a 2% year-over-year increase. Granted, 10% of these people state that they would be fine were it not for non-essential spending. Thus, they could conceivably cut back on discretionary expenditures and be fine financially. However, such a cutback would still have a negative impact on any company that is heavily dependent on consumer discretionary spending. Sempra, on the other hand, would not be affected by such an event. At some point, consumers will almost certainly be forced to cut back on such non-essential spending if a recession causes job losses and inflation continues. A company like Sempra could be a good hedge for such an event due to the general stability and non-cyclical nature of its cash flows.

Growth Prospects

While Sempra's stability is likely to be appealing for anyone looking to ride through any coming economic weakness with ease, the company's stability is unlikely to be sufficient for any investor. After all, right now a money market fund is yielding 5% and is about as close to risk-free as someone can get. When we consider this, there would be no reason to purchase any stock that only has a 3.40% dividend yield unless that stock was issued by a company that could deliver reasonable earnings per share growth. Fortunately, Sempra is well-positioned to deliver that growth over the next few years.

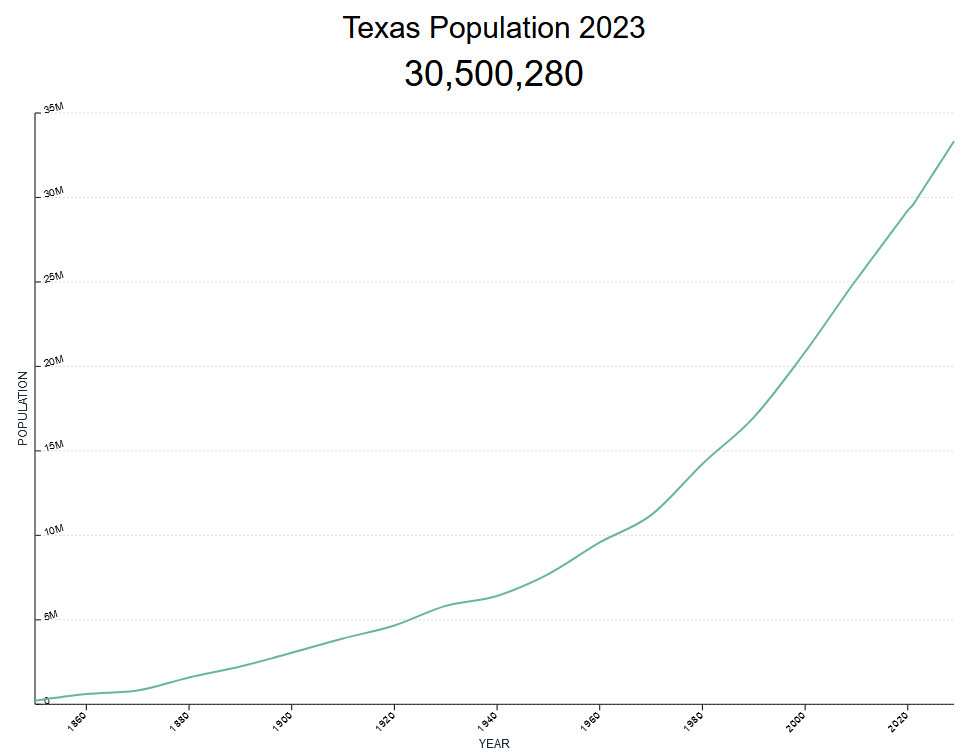

One way that it might be able to accomplish this growth is by increasing the size of its customer base. This will be easiest in Texas, which is one of the most rapidly growing states right now in terms of population. We can see that here:

{kind=link}

According to the U.S. Census Bureau, the population of Texas is currently growing at a 1.57% annual rate and the state is expected to continue to grow for at least the remainder of this decade. This could be beneficial for Sempra since a growing population could mean that more customers want the company's utility services. Sempra is the largest utility in Texas after all, so it seems likely that at least some of the population growth will be within the company's service territory.

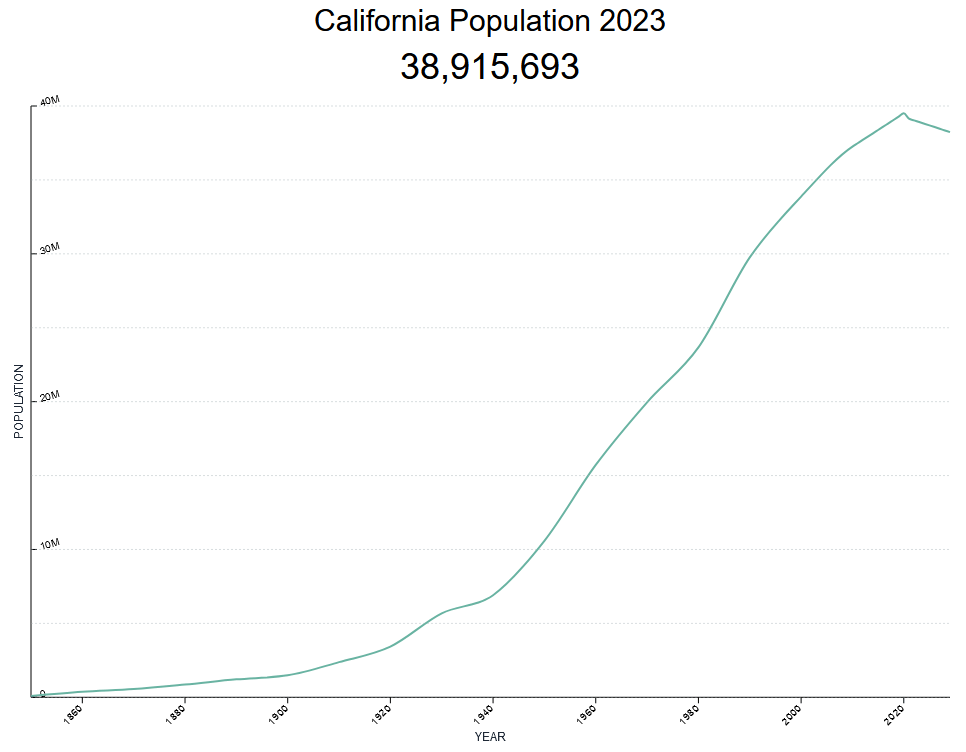

Unfortunately, the growth in Texas will almost certainly be at least partially offset by the declining population in California:

{kind=link}

The U.S. Census Bureau states that California's population is declining at a 0.29% annual rate. Texas is adding more people than California is losing, so in the end, it is only a partial offset, and the company will probably benefit from an increase in its customer base on the net. However, it is somewhat telling that Sempra has not listed a growing customer base among its growth drivers. As such, the company itself may not believe that demographic trends will not make any real difference in the long term.

The primary growth driver for Sempra will be the company increasing the size of its rate base. I explained the rate base in my last article on the company:

The rate base is the value of the company's assets upon which regulators allow it to earn a specified rate of return. As this rate of return is a percentage, any increase in the rate base allows the company to increase the price that it charges its customers in order to earn this specified rate of return. The usual way that a utility will grow its rate base is by investing money into upgrading, modernizing, and possibly even expanding its utility-grade infrastructure.

Sempra is currently planning to invest $40 billion over the 2023 to 2027 period toward the task of growing its rate base:

Sempra

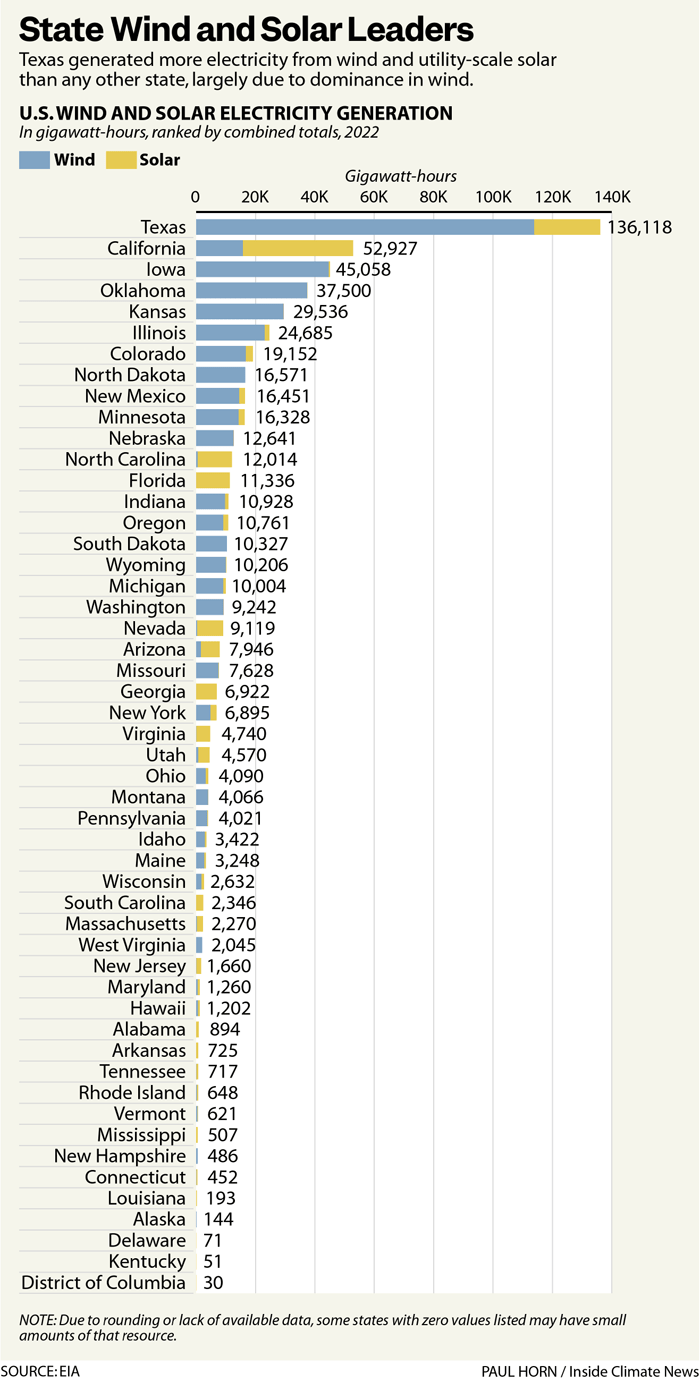

We can see that the majority of the company's spending is devoted to its operations in California, which makes sense. As we saw earlier, California does account for a greater proportion of the company's revenue and profits than Texas. Interestingly, California is also a bit behind Texas in the deployment of renewable energy. As of 2022, Texas generated significantly more renewable energy than any other state:

{kind=link}

Some of Sempra's capital expenditures will be spent on developing renewable energy in its region to meet the aggressive net-zero targets that have been imposed by the state's regulators. It clearly has a way to go as the state is the largest in the nation, but it does not have the most developed renewable generation infrastructure. One area of development that Sempra is working on is the infrastructure to handle electric vehicles, as the number of electric cars in San Diego alone increased by 112,000 during the twelve-month period that ended on June 30, 2023. As I have mentioned in a few previous articles, electric vehicles are a massive draw on the power grid, and it requires substantial investment to upgrade the electric grid to be able to handle the power demands of these vehicles. In addition to the electric vehicles, the Port of San Diego desires to fully electrify its operations, which will result in further draw on the grid. Fortunately for Sempra, the increased power consumption should have a positive impact on the company's revenues and ultimately profits.

The company has projected that the rate base growth from its capital investment program, as well as the increased draw on the grid from the electrification of certain things in its service area should allow it to grow its earnings per share at a 6% to 8% annually going forward. When we combine that with the company's current 3.40% dividend yield, we get a 9.50% to 11.50% total average annual return. That is not a bad total return for a conservative utility stock, and it is certainly much better than a money market fund as it will probably result in dividend growth over time.

Financial Considerations

As of June 30, 2023, Sempra had a net debt of $30.153 billion compared to a shareholders' equity of $31.014 billion. This gives the company a net debt-to-equity ratio of 0.97 today. This is in line with what the company had the last time that we discussed. Sempra's net debt and shareholders' equity both increased during the second quarter, which kept its ratio stable at 0.97. Here is how that compares to some of the company's peers:

| Company |

| Net Debt-to-Equity Ratio |

| Sempra |

| 0.97 |

| Entergy Corporation ( ETR ) |

| 1.92 |

| NiSource, Inc. ( NI ) |

| 1.65 |

| Edison International ( EIX ) |

| 1.95 |

| Atmos Energy ( ATO ) |

| 0.61 |

As regular readers are likely aware, it is rather rare for any utility to have a lower net debt than it has shareholders' equity. Thus, Sempra is part of a very elite group of companies that have a net debt-to-equity ratio below 1.0. Sempra does not have the lowest ratio out of its peers, but it is still low enough to conclude that the company is not overly reliant on debt to finance its operations. This is a very good sign.

The company's lack of reliance on debt is perhaps more important today than it has been in years. As I pointed out in a recent article , we are starting to see utility companies suffer the adverse impacts of rising interest rates on their cash flows and profits. Sempra also cited this as being one of the most significant adverse factors that it experienced during the first half of this year. The fact that this company is not as dependent on debt to finance itself as some of its peers is thus generally a good thing as it should mean that the company's financial performance will be more resistant to high interest rates than some other utilities. This reinforces our safe haven thesis that was outlined above.

Dividend Analysis

One of the biggest reasons why investors purchase shares of utility companies like Sempra is that they tend to boast a very high dividend yield. Sempra is no exception to this, as the company's 3.40% current yield is quite a bit higher than the 1.45% yield of the S&P 500 Index ( SPY ). Sempra's yield is also above the 2.70% yield of the U.S. Utility Index ( IDU ). However, for the first time in quite a long time, the stock's yield is below that of a money market fund. As many investors purchase utilities for safety, this fact could cause some people to eschew the sector in favor of risk-free investments, which could push Sempra's stock price down and dividend yield up. As has already been shown though, the company should be able to deliver a higher total return than most risk-free assets.

Sempra has a long history of raising its dividend on an annual basis:

{kind=link}

This is something that is very nice to see during an inflationary period. It is also something that gives Sempra an advantage over safe money market funds since it should result in the stock having a higher yield-on-cost than any risk-free asset after only a few years.

As is always the case though, we want to ensure that the company can actually afford the dividends that it pays out. After all, we do not want to be the victims of a dividend cut since that would reduce our incomes and probably cause the stock price to decline.

The usual way that we judge a company's ability to pay its dividends is by looking at its free cash flow. During the twelve-month period that ended on June 30, 2023, Sempra had a negative levered free cash flow of $4.7868 billion. That is obviously not enough to pay any dividends, but the company still paid out $1.497 billion during the period. At first glance, this will likely be concerning as the company cannot cover its dividends out of its free cash flow.

However, it is not uncommon for a utility to pay for its capital expenditures by raising money through the issuance of debt and equity. It will then pay its dividends out of operating cash flow. During the twelve-month period that ended on June 30, 2023, Sempra had an operating cash flow of $2.515 billion, which was easily enough to cover the $1.497 billion in dividends that it paid out and still left it with a lot of money left over for other purposes. Overall, the company's dividend is probably reasonably safe.

Valuation

According to Zacks Investment Research , Sempra will grow its earnings per share at a 4.95% rate over the next three to five years. This is quite a bit less than the company should be able to achieve based on its rate base growth, so it might be a bit lower than the company will actually achieve. With that said, this growth rate gives the stock a price-to-earnings growth ratio of 3.52 at the current stock price. Here is how that compares to the company's peer group:

| Company |

| PEG Ratio |

| Sempra |

| 3.52 |

| Entergy Corporation |

| 2.50 |

| NiSource Inc. |

| 2.41 |

| Edison International |

| 3.92 |

| Atmos Energy |

| 2.63 |

According to this, Sempra is a bit more expensive than the last time that we discussed the company. This is despite the fact that the market has been declining over the past month and Zacks actually increased its earnings growth projections for this company. The stock also looks incredibly expensive relative to comparable utilities, with the exception of fellow California utility Edison International. However, this is using the Zacks growth estimates. If we use the 7% midpoint of the company's own guidance, then the stock has a price-to-earnings growth ratio of 2.49 at the current price. That looks pretty reasonable relative to its peers.

At best then, it appears that Sempra is fairly valued at the current price. A good argument could be made for it being expensive right now. As such, it might make sense for a conservative investor to wait for a stock decline before buying in.

Conclusion

In conclusion, we continue to see signs that the economy could be weakening compared to where it was earlier this year. In particular, we are seeing consumers showing signs of financial stress, even if they are not slowing down on discretionary spending yet. It is questionable how much longer the current condition can continue before the average person cuts back to focus on paying off the copious amounts of credit card debt that they have taken over the past few years. Sempra is very well positioned to weather a weak consumer environment and still produce growth. The real downside with this company is that Sempra looks somewhat expensive compared to its peers. As such, it may be best to wait for a correction before buying shares in the company.

For further details see:

Sempra: Decent For A Weak Economy, But Stock Looks Pricey