SEMR - Semrush Holdings: Long Term Story Intact Initiate At Buy

2023-11-03 04:04:27 ET

Summary

- Semrush is a leading company offering comprehensive solution in the field of online visibility management and marketing analytics.

- Semrush has a strong investment thesis due to its innovative products, growing customer base, and potential for future expansion.

- Despite the macro overhang, we believe the long term story remains intact and the current valuation discount provides a favorable risk reward.

Investment Thesis

We ascribe a Buy rating on SEMrush ( SEMR ) primarily on the back of

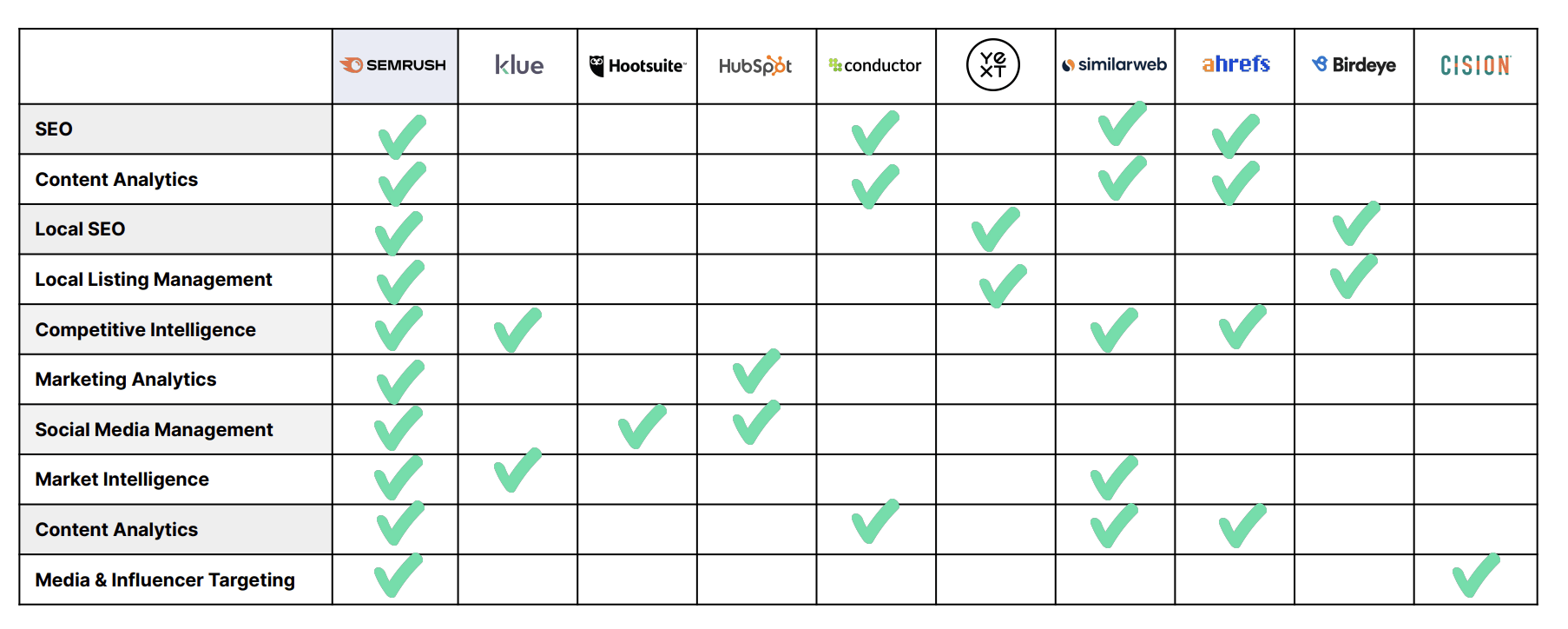

1) Comprehensive product offering: SEMR offers a comprehensive product solution for the online visibility across the marketing technology spectrum compared to its peers which are niche and specific to its key offerings. Its ability to provide a one-stop solutions has enabled them to up sell and cross sell exceedingly well leading to strong retention rates

2) Diversified Business Model: The company has over 100,000 paying subscribers and growing share of free users which ultimately are converted into paid subscribers. In addition, it generates majority of revenues outside of the US which demonstrates the potential for growth within US as well as outside.

3) Growth Oriented with Secular Tailwinds: We believe the company's operations in a rapidly growing online space along with its recent additions of ChatGPT and writing tools to its offering positions them well to leverage its continually growing scale benefitted by secular tailwinds as well as its complete solution

4) Attractive Valuation: SEMR trades at an attractive valuation and steep discount compared to its peers and have recently turned profitable. We believe the current valuation along with solid Q3 serving as a testament to improving financial profile despite macro overhang and provides a favorable risk reward and initiate with a Buy rating

Company Background

SEMrush ( SEMR ) operates a leading online visibility platform helping businesses understand the key drivers of web traffic to ensure their content receives maximum visibility by its targeted audience. Its platform boasts over 987k active free users as well as over 100k paying users across all verticals. It offers 50+ digital online visibility products and tools across SEO, SEM, content marketing, social media management, digital PR and others. The company has strong market positioning providing an entire gamut of integrated services compared to its peers.

{kind=link}

Historical Financials

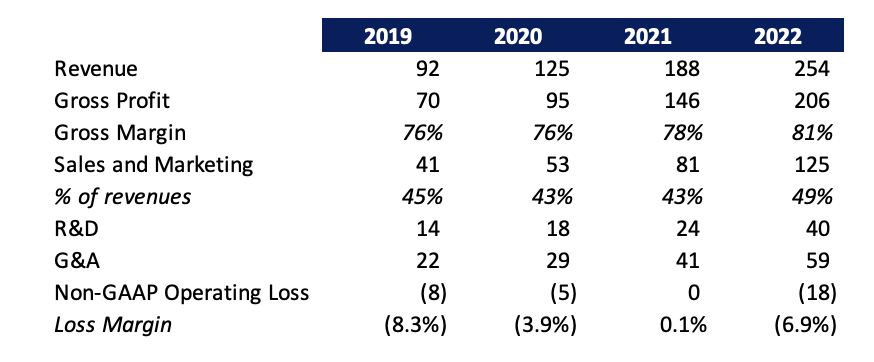

The company reported a solid growth over the historical period of 2019-2022 with revenues growing at a CAGR of 40%, albeit on a low base. The company has diversified revenue with US contributing less than 50% and rest of the world contributing over 40% of the total revenues. Gross margins continue to be healthy and has been steadily growing primarily driven by improvement in hosting service costs as well as revenue growth outpacing the personnel growth and fee costs. The company continues to invest significantly to acquire customers with sales and marketing expenses as % of revenue increasing to 49% in 2022 which is typical of a growth SaaS based growth companies and still significantly better than other vertical software companies as the company was already near operational breakeven at the end of 2022 and had the potential to accentuate robust margin expansion as the customer profile matures.

{kind=link}

Resilient Q3 Results

The company reported resilient Q3 in an otherwise challenging market conditions with revenue growing by 20% YoY to $79 mn, in line with the consensus expectations. Revenue growth has consistently slowed since past few quarters driven by declining dollar net retention rate and customer churn amidst macro slowdown in tech spends.

Paying customers continue to increase sequentially with net additions slowing slightly amidst cautious outlook, still below the ~4% average QoQ growth.

{kind=link}

Dollar based net retention ratio remains a concern amidst rapid churn in the subscribers while cross selling and up selling metrics fared relatively stable. NRR has fallen consistently over the past quarters and is now down to 109% compared to 115% in Q1 and significantly down below the company's ~120% average.

{kind=link}

Gross margins improved by about 220 bps YoY to 83.4% largely driven by lower headcount growth in customer and service support categories. Sales and marketing expenses decreased by 2% YoY primarily on account of $8 mn reduction in advertising expenses as the company focuses on improving CAC levels. Sales and marketing expenses as % of revenues leveraged by 8 percentage points as revenue growth outpaced the ad spends. This also focuses on the management's commitment to focus on improving CAC levels and profitability rather than growth.

Adjusted income from operations came in at ~$7.0 mn compared to loss of $8.3 mn in the previous year driven by strong gross margin expansion and optimization of its marketing expenses partially offset by continued investments in R&D. Adjusted net income came in at $8.4 mn compared to net loss of $7.1 mn in the previous year driven by strong operating income and higher other income.

SEMR tightened its guidance and expects full year revenue of ~$307.5 mn at midpoint, up 21% YoY and Q4 revenues of $83.2 mn, implying a 21% growth YoY. It raised its guidance for Adj. net income for the full year and expects Adj. net income of $10 mn at midpoint (vs $3 mn previously) driven by continued earnings momentum with Q4 Adj. Net income expected to be ~$5 mn. We expect the guidance is likely achievable driven by continued momentum and traction on its optimization of marketing spends.

Balance sheet remained healthy with cash balance of ~$220 mn compared to $230 mn at the beginning of the year with no debt.

Innovative AI Products

SEMR in its quarterly earnings stated that it is seeing encouraging trends within its AI capabilities with over 700k users having used its AI products. It highlighted that its writing assistant tool as well as a generative AI tool that helps customers reply to reviews, reported 42% growth in the number of posted replies within weeks after launch. We remain bullish on the AI space and believe SEMR is positioned well to leverage its presence with multiple easy to user tools already launched in the market and with further products in the pipeline.

Valuation

Given the company's growth profile and lack of mature bottomline, we value SEMR on an EV/ Sales approach, as is typical of a SaaS based growth company. SEMR trades at a significant discount to its peer average trading at 5.5x. We believe a discount is warranted given SEMR's smaller scale, lower operating margin profile and lower cash generation along with limited track record of execution as a listed entity. However, despite that a 50% discount is too steep and if we exclude Yext which declined over 50% from its peak due to operational challenges, the discount factor grows up to 60%. We ascribe a 30% discount to its peer average which implies an EV/ Fwd Sales of 3.8x and ascribe a target price of $10.5.

Risks to Rating

Risks to rating include

1) SEMrush's products are highly dependent on public data and third party service providers primarily through web-scrapping which remains a contentious issue and most sites attempting to block it. Its business operations would be adversely impacted in case of stringent policy or its inability or increasing difficulty to scrape data

2) SEMR has to rely on aggressive marketing spends to drive revenue growth. Its inability to improve customer lifetime value and bring down CAC would significantly impact its operating margin profile

3) Technology spends can come under further pressure as a result of prolonged macro headwinds which can hamper growth

4) SEMR operates in a highly competitive and fragmented market and an increase in competitive intensity can impact its business

Conclusion

We believe the near term environment remains challenging for the overall technology industry as well as for SEMR which has resulted in slowing customer net additions and declining dollar retention rates. While the macro outlook continues to remain an overhang and weigh on growth, we are constructive on the long-term outlook and believe SEMR will benefit from secular tailwinds as companies increasingly seek to utilize its suite of online visibility and competitive intelligence tools. In addition, the current valuation provides a favorable risk reward and we initiate with a Buy rating with a target price of $10.5 (at 3.8x Fwd EV/ Sales, 30% discount to peer average).

For further details see:

Semrush Holdings: Long Term Story Intact, Initiate At Buy