SEMR - Semrush Holdings: Plenty Of Positives But Currently Overpriced

2024-01-06 00:55:09 ET

Summary

- Semrush is a founder-led online-visibility SaaS platform with multiple market tailwinds.

- The company has reported marked customer and recurring revenue growth but has faced challenges with customer retention.

- Despite a growing economic moat and margin expansion, Semrush has more to prove to justify its current valuation.

- I rate SEMR shares a hold, but will revisit should shares drop below $10.

Investment Thesis

Semrush Holdings (SEMR) is uniquely positioned as an online-visibility software-as-a-service ('SaaS') platform and has grown recurring revenues meaningfully, despite its stock being nearly flat since IPO. The company is founder-led with high inside ownership, has exhibited network effects and pricing power, and holds a cash-heavy balance sheet. Management also revised the company's full year guidance upward for both top and bottom-line performance. Even with all the positives, Semrush looks overpriced in my view given increasing uncertainty around growth and customer retention. I rate SEMR as a hold but will look to buy should prices fall below $10.

Market Opportunity

SeoQuake was founded by current CEO Oleg Shchegolev and former COO Dmitri Melnikov in 2007 as a pioneer within the search engine optimization ('SEO') industry. The company was later renamed Semrush to incorporate its broader SEM (search engine marketing) offering. SEO is the process of improving websites to enhance their organic visibility on search engine results pages. SEM takes it a step further to include pay per click ('PPC') ad spaces on those same search engines. The digital space remains a vital part of advertising efforts, with the global digital advertising market expected to reach $740B in 2024 and search engine advertising comprising nearly half of it. As the number of internet users and hours spent online seem to perpetually increase, both organic ('SEO') and inorganic ('PPC') online visibility become more important for companies. In tandem with the growth in digital advertising is the burgeoning ' Creator Economy ' which reached $130B globally in 2023 and is expected to expand to $530B by 2033. More individuals are opting out of traditional occupations in favor of content creation and entrepreneurship - of which online visibility is paramount to success.

Semrush software uses machine learning algorithms and web-scraping to help these businesses and individuals manage the digital complexity and more effectively reach their target audience. In the company's S-1 filing , management estimated an annual global market opportunity between $13B and $20B based on the number of U.S. businesses (small to enterprise) multiplied by the average recurring revenue per customer (segmented by business size) the company had in 2021. Assuming these estimates have not changed (which is unlikely), Semrush is only about 2% penetrated into its estimated market based on TTM revenue. In my view, Semrush looks well-positioned for continued growth within the vast and expanding online visibility niche.

Business Strategy & Outlook

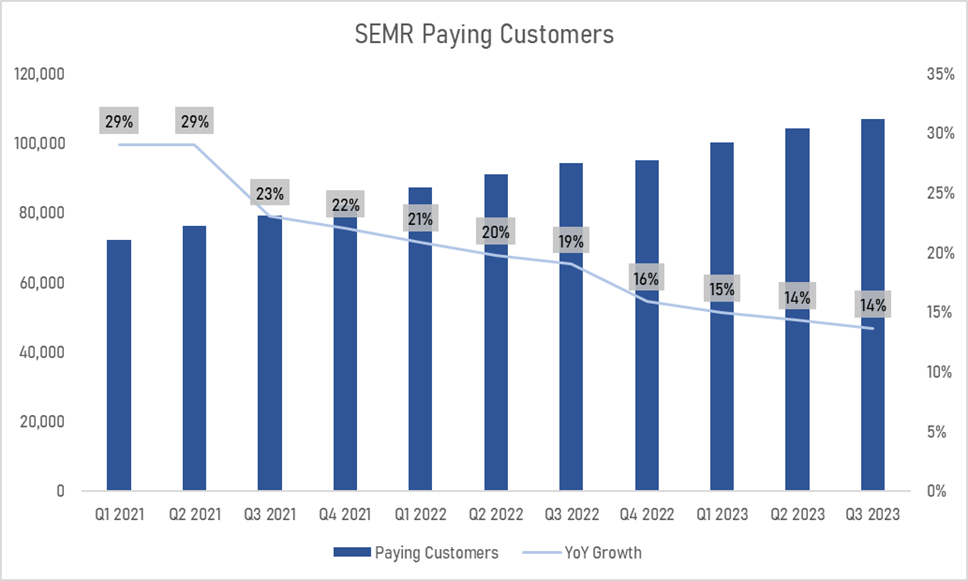

Since going public in March 2021, Semrush has quickly expanded its paying customer base to over 100k.

Author, data from SEMR Quarterly Results

{kind=link}

Additionally, a large part of the company's customer acquisition comes through a free version of the platform with limited features, which helps attract individual creators and small businesses. Semrush's free active user base has expanded from 307k in 2020 to 803k in 2022 according to the company's 10k filing . Semrush uses this multi-tier subscription strategy to both grow and upsell its existing base. In addition to almost all revenues being recurring, Semrush can grow per customer revenue through higher usage and new products. The company started with SEO but now has a product suite of 50+ products across advertising, content marketing, social media and more. A few helpful metrics to highlight the point are annual recurring revenue ('ARR'), dollar-based net revenue retention ('NRR'), and average recurring revenue per customer ('ARPU').

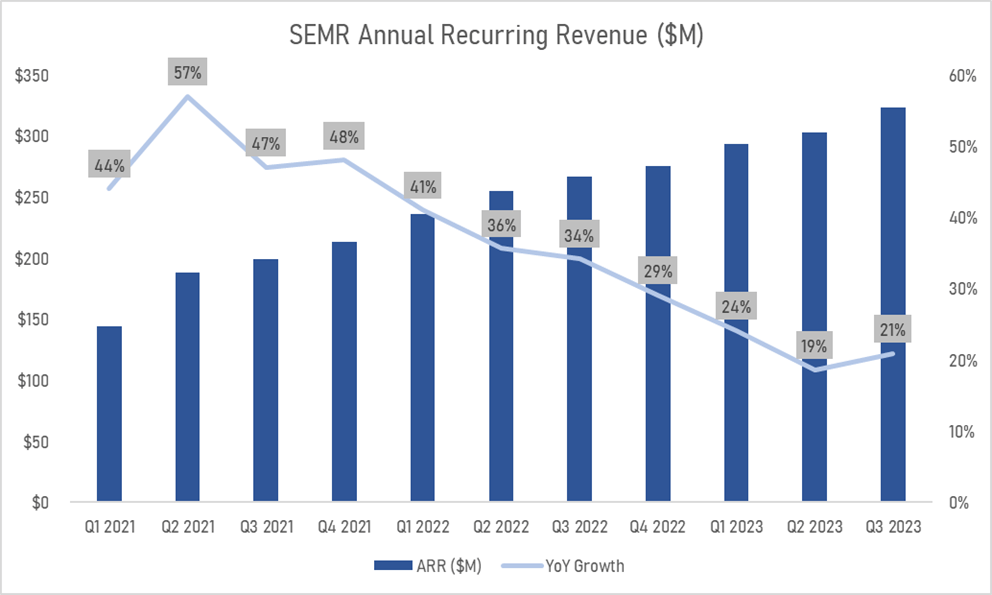

Semrush's ARR growth has been robust, inline with overall revenue growth which has grown at a 37% annual clip the last 5 years.

Author, data from SEMR Quarterly Results

{kind=link}

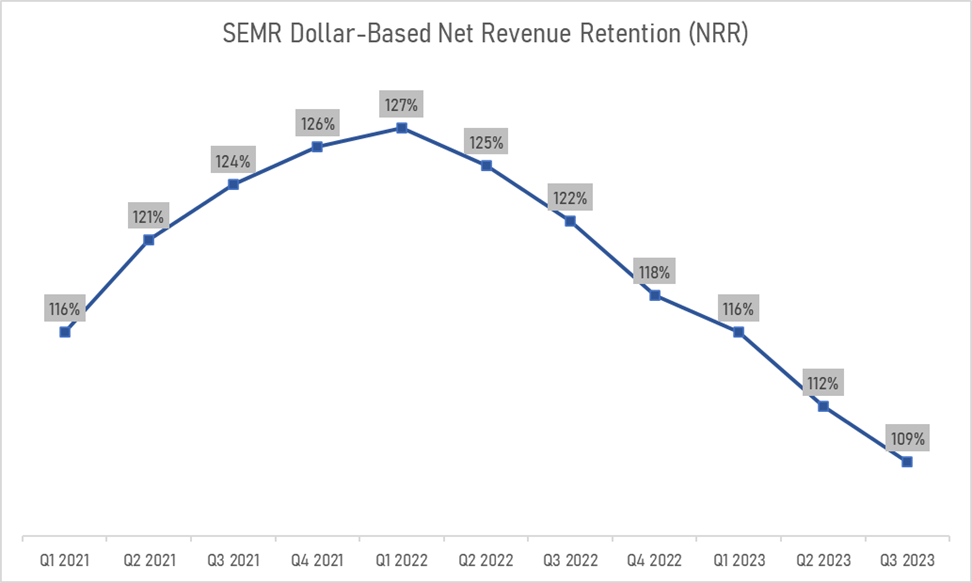

As shown above, growth cooled throughout 2022 but has recently bottomed around 20%, due to a few reasons. First, 2022 was a difficult year for businesses and individuals given a tighter macroeconomic picture with higher interest rates and inflation driving more stringent customer budgets. Similarly, NRR expanded through 2021 to nearly 130%, speaking to Semrush's ability to upsell and monetize its user base. But the contractionary environment spurred customer churn, driving a steep decline in NRR.

Author, data from SEMR Quarterly Results

{kind=link}

Management sees both KPI drop-offs as temporary, expecting ARR growth to reaccelerate into the 20s and NRR to rebound. In Q2 of 2023 they touched on the topic:

…there is a couple of things I'd give some color on. First, there's some macro factors influencing that metric. So while it's been strong in some periods, we've had record new customer adds and demand for our products. We've also had a slight uptick in churn. And the churn is a function of the current macro environment as our customers tighten budgets and look to optimize their spend. But the good thing for us is we see a significant portion of our customers' return. And as the macro improves, we'll expect that trend to continue. So, historically, we've seen 30% of our customers return to us in a short period of time. And I think as the macro environment improves, we'll actually see that uptick.

I tend to be optimistic with management as we've seen this apparent reacceleration of ARR in Q3 and expected Q4 estimates, but the retention figure is more concerning. In Q4 of 2022, management expected NRR to pick back up to the mid-110s long-term, thanks largely to customers returning quickly as conditions improve. But the metric trended further downwards in Q3. Management then adjusted their rhetoric to just keeping NRR above 100%. Though an NRR above 100% is healthy, the deterioration we've seen doesn't appear to be slowing even as the economy improves. Part of this drop could also be attributable to price increases in 2023, which drove 20% of ARR growth according to management. Perhaps smaller customers were squeezed a bit but will return when the economy improves. I don't put all my weight into a single metric, but NRR is extremely important for high-growth SaaS firms as it underscores customer lock-in and the efficacy of the platform. I will be watching this metric closely in Q4 and beyond.

Thankfully, ARPU has held strong, helping to highlight the firm's ability to absorb higher costs and expand per customer spend. Some of the success here is attributable to an increasing share of enterprise users which have an overall greater ARPU.

Author calculations, data from SEMR Quarterly Results

{kind=link}

Economic Moat

Semrush is a relatively small fish when looking at digital advertising alone, competing indirectly with firms like Google and Facebook. But Semrush differentiates itself as a pure, independent player in the space. A criticism of these behemoth firms is their lack of independence as they can promote their own paid advertising channels even if not optimal for customers. Google and Facebook present the largest competitive risk to Semrush in my view, should they double-down within online visibility. However, Semrush has a few growing economic advantages by nature of the company's business model.

Semrush has been operating for 15 years, collecting tons of data along the way. In 2022 the company captured trillions of data points across 770 million unique domains. Semrush's platform was built using machine learning and web scraping techniques which only grow stronger with more data inputs. Data is becoming a currency of competitive advantage as the AI race chugs along. This is also underscored by the platform's leading rating vs peers according to G2 . Like many other SaaS platforms, scalability is another benefit. Semrush has quickly expanded its customer base and ARR all while expanding its gross margin from 75% in 2019 to nearly 83% the last twelve months. Semrush is a small player in digital advertising and by no means has a massive moat, but it appears to be expanding nicely within its niche.

Valuation & Fundamental Drivers

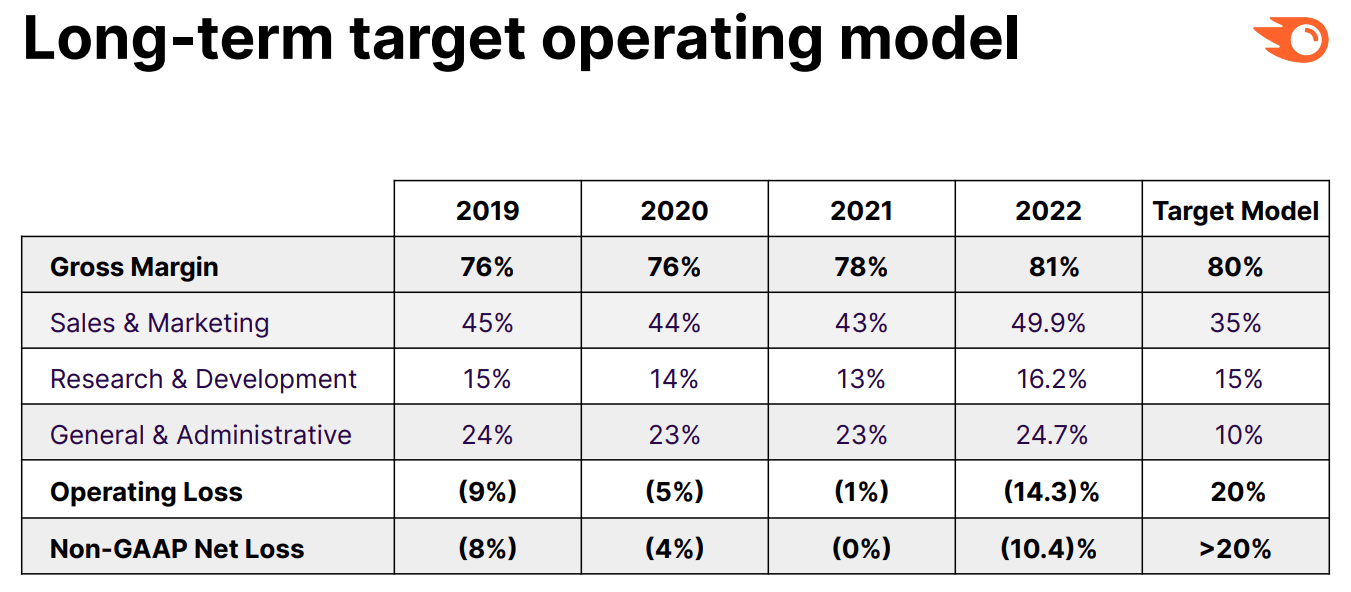

Semrush has done well in expanding gross margins as we saw but operating margins have been weighed down by increased sales & marketing expenses - though the company expects to see operating profit this next fiscal year. In 2022, management released their long-term operating model targets :

SEMR 2022 Investor Presentation

{kind=link}

I believe the gross margin improvements in 2023 warrant a higher long-term estimate but view the company's operating targets as reasonable. My base case holds revenue growth of 15% annually the next 10 years given the industry tailwinds and business runway we saw, the rebound in ARR growth, and Semrush's ability to expand revenue retention in excess of 100% through upselling and platform scalability. I also expect the company to maintain gross margins of 84% long-term and operating margins to slowly expand to 18% by 2032 as the company seeks to balance growth and profitability. Additionally, my base case holds that fixed and working capital investment will remain close to historical averages:

- Capex at 1% of revenues

- Depreciation & Amortization at 60% of Capex

- Change in Net Working Capital averaging about 1.5% of revenues.

Lastly, I introduced an upside and downside case and assigned probabilities to each. This allows us to test a range of assumptions and estimate the likelihood of potential outcomes. As you can see from the below results, each case has wide variability in implied share price, with currently more downside than upside based on the case assumptions. Additionally, I assigned a probability to each case, with the heaviest weight given to my base case. Even with a higher probability of the upside case, the result is an expected value of $9.60 or 29% downside.

Author Estimates

Risks & Uncertainty

In addition to the risks already discussed, contracting NRR and competitive threats, Semrush has a few other risks investors should note. As we saw, Semrush's performance suffered from macroeconomic headwinds in 2022 and 2023. The macro landscape is still a bit uncertain moving into 2024, and I expect Semrush to closely follow consumer sentiment. If rates are cut and inflation continues to cool, Semrush will likely see tailwinds in performance and vice versa. Thankfully, the company holds $230 million in cash equivalents versus only $13 million in debt, a nice cushion against this external risk.

Internally, Semrush is founder-led with insiders holding 53% of shares and 75% of voting power. This tends to be good for shareholders as it aligns leadership's incentives with that of shareholders but also introduces key-person and principal-agent risks. If insiders leave or take the wrong direction with the company, shareholders have less influence to right the ship. Semrush is also listed as an Emerging Growth Company under the JOBS act , which allows them to report less data than comparable publicly traded companies. This increases the principal-agent risk as management could be withholding information relevant to shareholders.

Conclusion

Semrush has much potential within the online visibility niche. It has shown an ability to expand its customer base and recurring revenues at a marked pace. But the company's overall growth and customer retention suffered through the difficult environment of 2022 and 2023. The Semrush platform has a few economic positives including scalability and data advantages, but the company has more to prove to justify its current valuation. I will be looking for improvements in customer retention and renewed growth going into 2024 while looking to buy should shares fall below $10.

For further details see:

Semrush Holdings: Plenty Of Positives But Currently Overpriced