CRDO - Semtech: Recommend Neutral Rating As There Are 3 Big Uncertainties

2023-09-26 04:57:50 ET

Summary

- Sales of IC components, particularly for Cloud Data Center products, have contributed to SMTC's strong revenue and gross margin performance.

- Despite SMTC's strong 1H24 performance, caution is advised as industry peers express concerns about inventory issues and soft demand in end markets.

- The key question is whether the new CEO can successfully execute cost reduction initiatives, potentially driving a positive multiple re-rating.

Summary

This post is to provide an update on my thoughts on Semtech Corp. ( SMTC ) business and stock. While my model suggests an upside, if the business sees recovery in FY25, I am recommending a hold rating. There are three uncertainties here that could swing the near-term performance: end-market demand, market inventory level normalizing, and management cost-cutting initiatives. Two out of three (the former two) are out of management hands and could turn for the worse if the economy turns bad (demand remains poor and customers reduce the pace of inventory depletion to stay afloat longer). Lastly, while the traction with cost cuts has been positive so far, it is still uncertain whether it is due to cutting the low-hanging fruits.

Business overview

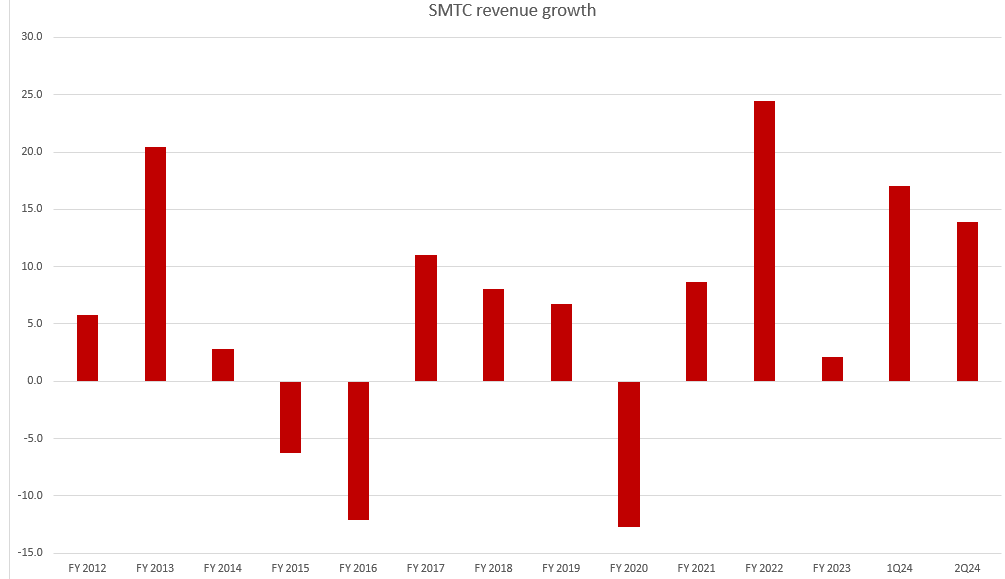

SMTC designs, manufactures, and markets a diverse range of analog and mixed-signal semiconductor products, encompassing integrated circuits, discrete circuits, and assembly components. These devices find applications in various sectors, including computing, communications, industrial, military-aerospace, and automotive industries, among others. SMTC is a cyclical business that has seen its growth swing between negative and positive regions over the past years. In each boom and bust, it follows a typical pattern where end-markets saw elevated inventory levels due to oversupply in the preceding years. This would be followed by a downcycle where inventory gets digested. I believe SMTC is gradually exiting the trough of this cycle, as can be seen from its revenue performance.

{kind=link}

Investment thesis

Sales of IC components, especially those for use in Cloud Data Center products, were a major contributor to SMTC's $238.4 million in revenue. The improved product mix helped push the non-GAAP gross margin up to 49.6%. Lower operating costs were a major factor in the company's $0.11 non-GAAP EPS, which was significantly higher than the consensus estimate of $0.02.

Despite SMTC's strong performance in 1H24, my cautious approach to investing makes me wary of the stage of recovery that the company (and the industry) is at. My worries are not baseless. In their latest transcript, Analog Devices ( ADI ) and Ambarella ( AMBA ) expressed concern that inventory issues would remain in the end markets. Importantly, both parties stressed the continued shortening of product lead times and the continued softness of demand in end markets. I believe these factors could pose a threat to SMTC near-term results, which currently seem to be on hot wheels as consensus estimates imply that SMTC is already ahead of the recovery curve (consensus expects 17%/6%/13% revenue growth in FY24/25/26).

“I want to turn to the current business environment now just for a moment. As we shared last quarter, we believe we're in a period of customer inventory reconciliation following three consecutive years of steady growth.” ADI 3Q23

“So I think, one way to look at this is, how long will the inventory correction take? My sense is it will be two to three quarters before we get through the inventory digestion cycle.” ADI 3Q23

“Customers are now more aggressively reducing their inventory and we are now seeing some pockets of weak end-market demand, which complicates our customers' ongoing inventory reduction efforts. Given this, we have reduced our second half outlook.” AMBA 2Q24

“We are not expecting a recovery in calendar 2023, but we do anticipate our customers' inventory will normalize by the end of the year and set us up for a return to growth in calendar 2024.” AMBA 2Q24

One bright spot, however, is the possibility that SMTC data center signal integrity solutions will continue to perform well, mitigating the effects of a potential downturn in the other segments (caused by the inventory and demand dynamics discussed above). Peer companies' comments, such as those from Marvell ( MRVL ), MACOM Technology ( MTSI ), and Credo Technology ( CRDO ), all point to the same thing: sustained high demand.

“And it's obviously within overall data center, all of that sort of inventory adjustment and weakness at the end-market levels being just blown away obviously by the AI and cloud infrastructure piece, which is still driving very healthy growth into Q3, and then another step up obviously in Q4, and that's assuming really no material recovery in the on-prem side.” MRVL 2Q24

“Sure. So, from a data center point of view going into Q4, it would be up certainly quarter-over-quarter significantly as well as year-over-year. I would say very strong double-digit quarter-over-quarter and high single-digit year-over-year.” MTSI 3Q23

“We -- So as I mentioned in my prepared remarks actually, we do remain cautious as you say in the back half because a lot of the shift that's happened in hyper -- hyperscale data center spend to AI, it's given us a lot of opportunity to engage with customers that are existing customers and new customers on new programs that we're having a lot of success in.” CRDO 1Q24

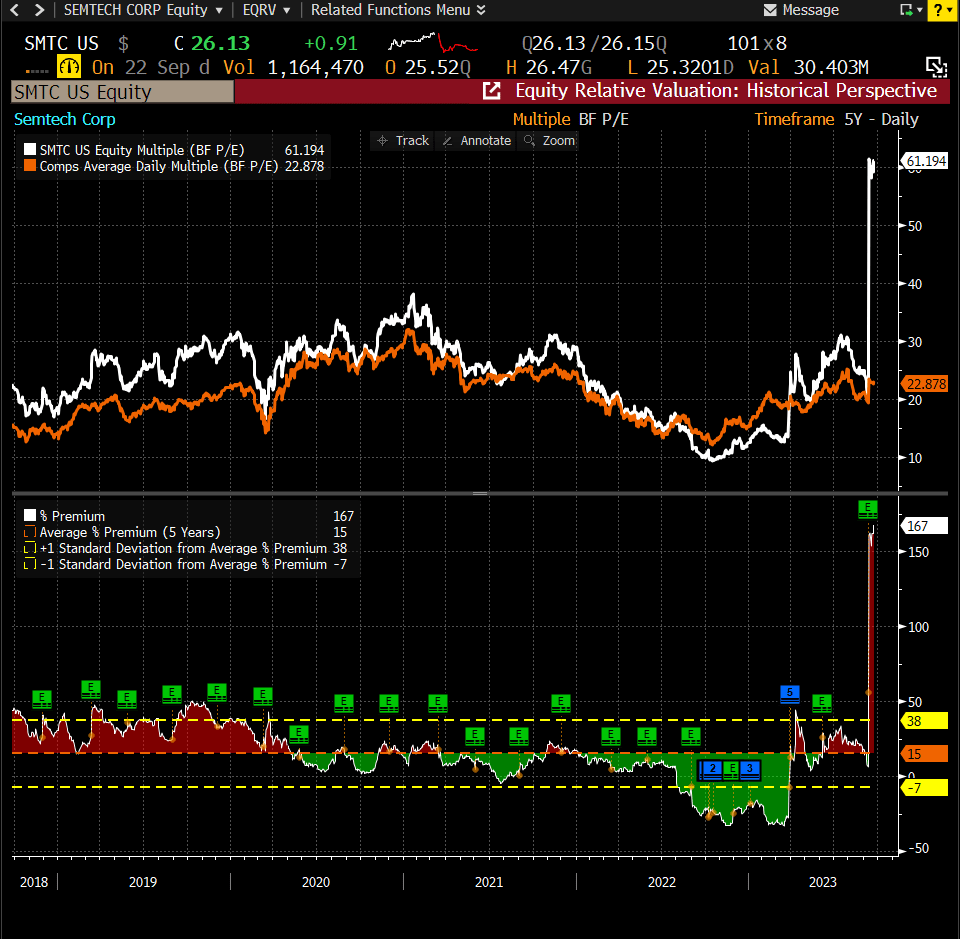

With a mix business outlook, the key question lies in whether the new CEO – Paul Pickle – can deliver against the targets it has listed out, in particular, the cost reduction initiatives. Since SMTC's EBIT margin has lagged behind that of its competitors, this development has the potential to serve as a powerful catalyst for driving a positive multiple re-rating. Importantly, unlike end-market demand and customers' efforts to reduce inventory, this initiative falls within the walls of SMTC business and is therefore dependent on management's ability to execute. So far, I'm impressed with management's performance, as I can see evidence of serious efforts being made to rein in expenses. Recent operating expenses totaled $85.8 million, a decrease from the previous quarter. The next quarter is expected to follow suit with the previous two, with management projecting a midpoint of $83 million for 3Q24. If this trend continues, I anticipate operating costs to continue falling through FY24. If this trend holds, and a full recovery occurs across all segments in FY24 or FY25, SMTC's EBIT could see a sizable increase (higher revenue on a lower operating cost base) in the following years.

Own calculation

Valuation

Own calculation

I believe the fair value for SMTC based on my model is $35.50. My model assumptions are that SMTC will not be able to meet consensus optimistic estimates given the underlying industry trend (inventory issues and weak end-demand). I believe the growth will be seen more in FY25, which is reflected in my 10% FY25 growth. I used 10% as I expected the growth to face a partial strong 1H24 comp (note that 1H24 saw ~15% growth). While the cost-cutting initiatives have been going well so far, I continue to model a flat margin in FY25 vs. FY23. Any meaningful improvement in margins will have additional upsides. I valued SMTC using 22x forward PE as I see no reason for SMTC to trade above comps level, which it has historically traded in line with.

{kind=link}

Risk

SMTC is still under the mercy of end-market demand turning around, which could take a lot longer than expected. While the cost-cutting initiatives are very positive so far, this is a new CEO for the business, after all. Initial results could be due to low-hanging fruits, which might not be available in the coming quarters. If the cost-cutting initiative fails to gain further traction, I’m afraid investors will further shun the stock as management has lost its creditability.

Conclusion

In conclusion, I maintain a hold rating for SMTC due to three significant uncertainties that could impact its near-term performance. Firstly, uncertainties in end-market demand and inventory normalization are beyond management's control and could worsen if the economy takes a downturn, affecting demand and inventory dynamics. Secondly, while SMTC has made positive strides in cost-cutting initiatives, it remains uncertain whether these efforts are sustainable or if they are primarily due to low-hanging fruit. Despite SMTC's strong performance in 1H24, caution is warranted, as industry peers like Analog Devices and Ambarella express concerns about lingering inventory issues and soft demand in end markets.

For further details see:

Semtech: Recommend Neutral Rating As There Are 3 Big Uncertainties