ASAI - Sendas Distribuidora: A Pre-Q3 Buy Opportunity

2023-10-16 07:53:20 ET

Summary

- Assaí Atacadista is about to release its Q3 results amid challenges from food disinflation and high-interest rates, but it has managed them well compared to peers.

- The company is expected to benefit from improving economic conditions, with lower interest rates on the horizon, potentially leading to a 41% upside.

- With its resilience and firm performance in the Brazilian cash and carry sector, Assaí stock presents an attractive investment opportunity.

Sendas Distribuidora ( ASAI ), which operates in Brazil under the name Assaí Atacadista, is on the verge of reporting its third-quarter results at the end of October.

This year, in contrast to the performance of the Brazilian stock market as represented by the iShares MSCI Brazil ETF ( EWZ ), Assaí has encountered challenges, primarily due to its direct exposure to the decline in food and commodity prices.

The negative impacts on the volume recovery in the sector and the deflation in the category have, however, been better managed by Assaí in Brazil compared to its peers, such as Atacadão, which is part of the Carrefour ( CRRFY ) group's operations in Brazil.

In my previous article about the Brazilian cash and carry sector, I adopted a neutral stance regarding Assaí shortly after its second-quarter results. The food sector appeared to remain under pressure due to deflation and an expectation of prolonged high-interest rates in the coming years.

However, with the recent interest rate cuts in Brazil of 50 basis points and indications of further reductions, with a projection to end the year at 11.75%, consumer spending is expected to show more favorable same-store sales numbers for the second half of this year.

The significant drop in Assaí's share price also supports a more favorable risk-return perspective, even in a deflationary and uncertain scenario. Trading at valuation multiples below its historical three-year average and, based on my discounted cash flow ((DCF)) analysis, considering conservative assumptions about interest rates for the coming years, Assaí's shares could have a 41% upside potential based on the current share price of $11.50.

The Current Cash and Carry Scenario in Brazil

Brazil's current cash and carry scenario closely resembles the second quarter of this year. It's characterized by consumers experiencing reduced purchasing power, deflation in the food sector, and a shift in B2B customer behavior. There's an expectation that a more accommodating interest rate environment will prevail.

In general, the second-quarter earnings season in Brazil proved to be weak, with a 30% decline in earnings per share ((EPS)) for Ibovespa compared to the same period last year. This reflects the ongoing challenges of a macroeconomic environment with more expensive credit, a challenging external landscape (including the U.S. and China), and high levels of household debt.

Therefore, the second quarter of 2023 potentially represented the worst quarter regarding results for Assaí Atacadista. We continue to face short-term challenges in results dynamics due to food deflation, constrained consumer purchasing power, and financial performance pressure.

Assaí Atacadista faced difficulties in the second quarter due to the drop in food and commodity prices, which negatively impacted the gross revenue growth of wholesale stores during that period. This is because a recovery in sales volume has not yet accompanied the disinflation in the food industry.

I anticipate that the trends in the cash and carry sector will show sequential improvement in the third quarter, with conversions reflected in same-store sales (SSS), especially starting in the fourth quarter of 2023. This positive outlook is supported by more normalized comparison bases, increased purchasing power, and declining Brazilian interest rates (Selic).

The Selic rate saw its first rate cut in early August, with a reduction of 50 basis points. Despite the overshadowing impact of rising global interest rates, I still consider this rate cut a positive beginning to a cycle for Brazilian stocks, as it signifies a departure from excessively restrictive interest rate levels. This optimism is rooted in the expectation of lower inflation.

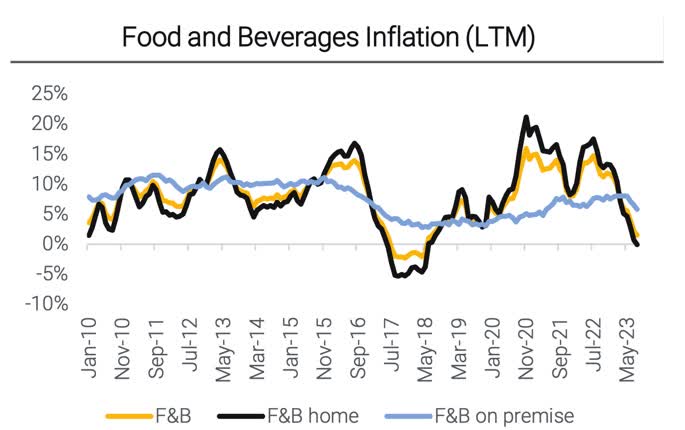

Data from the supermarket sector in Brazil indicates that food and beverage inflation has been consistently decreasing since the end of 2022, and this downward trend is expected to continue throughout the second half of this year. Although this trend will likely put continued pressure on the margins of the Brazilian cash and carry sector, it should enhance consumers' purchasing power.

{kind=link}

What to Expect for the Third Quarter

Assaí is set to release its third-quarter results on October 30th.

The reduction in food inflation and B2B consumers adjusting their consumption habits over the months will likely keep Same Store Sales in the negative territory for the third quarter. It's important to note that, even though it's expected to be negative, this indicator should be less affected than its main competitors, such as Atacadão, part of Carrefour Brasil. This is because Atacadão has a greater exposure to B2B customers.

In this context, the growth in the top line is expected to be driven by the 52 new store openings in the last 12 months, which should result in a more substantial gross revenue.

As for the gross margin, I do not anticipate significant changes. I believe that the surplus margin from converted stores will likely continue to be invested in more competitive regions. Hence, expecting a relatively stable annual margin of around 16.4% is reasonable.

With fewer conversions in the quarter and fewer stores left to be converted, a reduction in pre-operational expenses is also likely. Simultaneously, the positive performance of the converted stores, with sales uplift exceeding that of the second quarter of 2023 by 2.5 times, should help mitigate the impact of quarterly expenses.

Regarding the R$1.0 billion in EBITDA in July, there is a trend where the amount of financial expenses is expected to affect the bottom line, significantly reducing net profit.

Another point to consider is that Assaí is not expected to reduce its leverage in the third quarter. The second half has been remarkable regarding working capital, with the company showing significant improvements in inventory. This has substantially boosted operating cash generation in the quarter, resulting in R$5.4 billion, representing a R$2.6 billion improvement compared to last year. This boost in cash generation has led to a 0.2 reduction in the company's net debt/EBITDA ratio, bringing it down to 2.6x.

However, considering the seasonality in Q3, we should anticipate inventory restocking in preparation for the anniversary event, Black Friday, and year-end holidays. Given this dynamic, leverage should moderate to around 2.5x Net Debt/EBITDA.

Furthermore, looking ahead, we can still identify some positive signals. With improved seasonality in 4Q23 and inventory normalization, we should expect a return to the deleveraging path. Starting in 2024, with reduced investments, the conclusion of transaction payments, and a declining interest rate trend, a substantial financial deleveraging process is highly likely.

Valuation

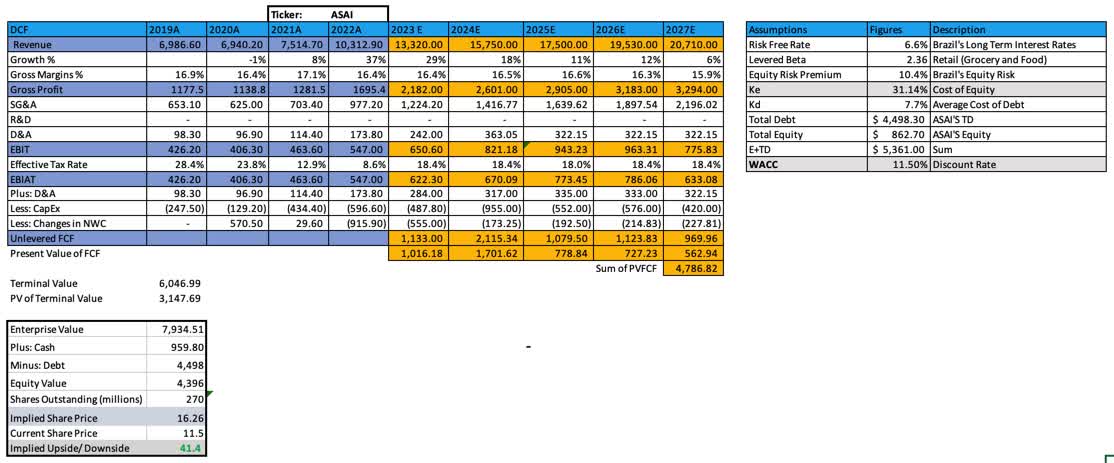

Concerning Assaí's valuation, I employed the Discounted Cash Flow ((DCF)) model to provide a more precise overview of the company's standing. Given relatively conservative assumptions, I have concluded that there is a potential appreciation of approximately 41% for the company's shares, considering the current share price of $11.80 as of October 13th—roughly 42% below the historic peak in January of this year.

My estimations for top-line growth adhere to the Seeking Alpha consensus , projecting an increase of 29% in 2023E, 18% in 2024E, 12% in 2024E, and 6% in 2025E. For EBIT, D&A, and Capex, I've utilized the consensus data provided by S&P Capital IQ .

The effective tax rate considered was an average of the last five years, which averaged 18.4%. This is a somewhat conservative assumption, considering the downward trend of interest rates in Brazil.

Concerning NWC (Net Working Capital), I've considered an average of -1% of revenues over the last five years, except for 2023E, where I've factored in the TTM (Trailing Twelve Months) period. Considering the company's robust business revenues, my terminal growth rate has been set at 2%.

The Weighted Average Cost of Capital ((WACC)) was 11.5%. This calculation considered several factors, including Brazil's long-term interest rates, currently at 6.6%, a leveraged beta of 2.36 for the retail (grocery and food) sector, and the Brazilian Equity Risk Premium of 9.6%, leading to a cost of equity of 31.14%. Additionally, considering interest expenses of $426 million throughout this year and a tax rate of 18.4%, Assaí's cost of debt is determined to be 7.7%.

In the Discounted Cash Flow ((DCF)) model for Assaí, the cash flows were aggregated until 2027, resulting in a total value of $4,786.8 million. When factoring in a terminal value for 2027 and bringing it to the present value, the model reaches a figure of $3.14 billion, calculating an enterprise value of $7.9 billion. Assaí's equity value amounts to $4.39 billion after adding cash and subtracting debt. Dividing this value by the 270.29 million shares outstanding, the implied value arrives at $16.26 per share for Assaí.

Assaí's DCF model. (Assaí's IR, compiled by author)

{kind=link}

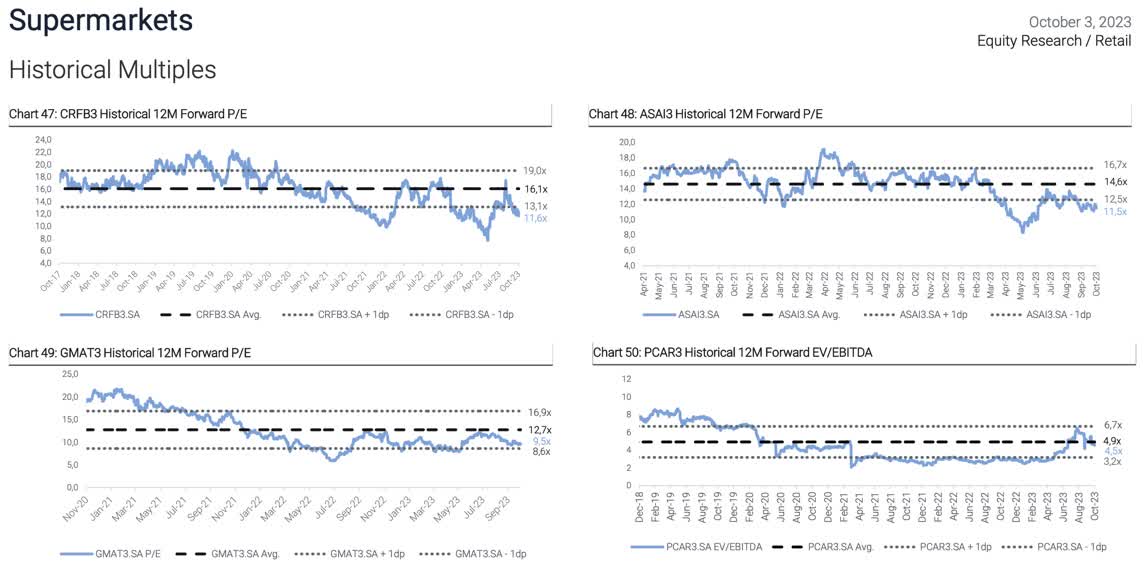

When we compare Assaí to its major domestic peers, we can see that the company has been trading at historical multiples of a forward P/E (Price-to-Earnings) of 11.5x in October. This is still below its historical average over the past three years and is practically in line with its main local competitor, Carrefour Brasil (Atacadão).

Looking at other domestic peers, such as Grupo Mateus, the forward P/E of 9.5x may seem more appealing, but it's closer to the historical average than Assaí's valuation.

Carrefour Brasil (Chart 47), Asai (Chart 48), Grupo Mateus (Chart 49), and Grupo Pão de Açucar (Chart 50). (XP Inc.)

{kind=link}

The Bottom Line

Given that the Q3 scenario is expected to be quite similar to Q2, it is improbable that Assaí's results will deteriorate further. It seems that the worst of the revenue growth slowdown, driven by a combination of food disinflation and high-interest rates, may have already passed. In this context, the Brazilian economy's leaning toward lower interest rates for the second half of 2023 and beyond 2024 is expected to drive Assaí's deleveraging trend.

It's important to acknowledge that a signal of interest rate reduction in Brazil happening at a slower rate than anticipated, especially in the context of a more uncertain macroeconomic environment, could present a significant risk to Assaí's deleveraging efforts, given its substantial debt burden.

Despite trading at a more discounted valuation compared to its primary peer, Carrefour Brasil (owner of Atacadão), my valuation model, which incorporates rather conservative assumptions, especially regarding effective tax rates, suggests a 41% potential upside based on the current share price of $11.50 per share. Therefore, I recommend considering Assaí as a "buy" ahead of the Q3 results.

For further details see:

Sendas Distribuidora: A Pre-Q3 Buy Opportunity