ASAI - Sendas Distribuidora: Maintaining A Neutral Stance Amidst Brazilian Disinflation

2023-08-03 16:19:30 ET

Summary

- Sendas Distribuidora (Assaí Atacadista) is a leading company in the Brazilian cash and carry wholesale market with operational autonomy after its spin-off in 2021.

- Despite challenges from falling commodity prices, Assaí Atacadista has shown resilience compared to its domestic competitors as recently reported its second-quarter results.

- Given the current macroeconomic pressures, such as disinflation and high-interest rates in Brazil, I find the company's above-industry-average valuation less attractive.

Sendas Distribuidora ( ASAI ), operating under Assaí Atacadista, currently holds the position of the second-largest retailer in Brazil and is the leading brand of the French group Casino in gross revenue. Formerly controlled by Grupo Pão de Açucar (CBD), the company gained operational autonomy after its spin-off in 2021.

Over the past five years, Assaí Atacadista has been the driving force behind the expansion of the Brazilian cash and carry market, successfully opening over 600 new stores. This business model has proven resilient during periods of economic instability, offering consumers attractive benefits that continue to attract customers even as normality returns.

Despite facing challenges this year, including a 22% decline in its market value due to falling food and commodity prices, Assaí Atacadista remains competitive, as reported in its second-quarter earnings results. The negative impacts of the sector's volume recomposition and category disinflation were better managed by Assaí Atacadista than its primary Brazilian cash and carry competitor, Atacadão, which is part of the Carrefour ( OTCPK:CRRFY ) group.

While Assaí Atacadista appears to be a strong contender in the Brazilian wholesale market compared to its peers, I am cautious about investing now. The food sector will likely face continued pressure from deflation and the prevailing scenario of high-interest rates in the coming years.

Coping with Disinflation: Challenges for Assaí Atacadista

Assaí Atacadista shares have been performing poorly this year, diverging from other major Brazilian companies as inflation has been falling and interest rates have finally been cut for the first time since September last year.

Over the last twelve months, Brazil's main inflation index (IPCA) has accumulated at 3.16%, a significant decrease compared to the more than 11% recorded in June 2022. While this decline in inflation is generally positive for the overall economy, it has posed challenges for wholesale stores like Assaí Atacadista.

Historically, wholesale stores have thrived during periods of high inflation, boosting revenue and allowing for higher margins by appreciating stock products. Moreover, with people's incomes under pressure, they tend to gravitate towards these options that offer products at lower prices.

However, the current slowdown in food inflation is impacting the revenues of companies like Assaí Atacadista. This trend is expected to continue until the end of 2023, leading to a revenue drop and a decline in same-store sales (SSS).

While lower inflation benefits the broader economy, it poses specific challenges for businesses reliant on inflation-driven gains. Companies in the wholesale sector may need to adjust their strategies to navigate this period of reduced inflationary pressures and adapt to changing consumer preferences and spending patterns.

On the earnings front, Assaí Atacadista has faced challenges from a combination of debts incurred during acquisitions and high-interest rates in Brazil. The company's wholesale chain, Assai, has been aggressively expanding its store presence, with around 60 new stores opened in the last twelve months, achieved through organic growth and the conversion program of Hipermercados Extra, a major supermarket chain in Brazil.

These pressures will persist throughout the year's second half as interest rates remain above 13%. However, there is a potential for some relief from mid-year onwards, with a projected Selic rate of 12.25% by the end of this year. This anticipated decrease in interest rates could ease some of the financial burden faced by Assaí Atacadista, providing some respite to its earnings outlook.

Improved Governance: Lesser Concerns for Assaí Atacadista

In 2021, the French group Casino, burdened with significant debts, decided to spin off some of its assets in Latin America, including Assai Atacadista (Sendas Distribuidora) and Grupo Pão de Açúcar (Companhia Brasileira de Distribuição), while retaining control over both companies.

Assai Atacadista acquired 71 stores from the Extra chain for R$5.12 billion as part of the spin-off. However, the market viewed this move skeptically due to the corporate governance model allowing the purchase without consulting minority partners.

This year, Assaí Atacadista made a positive shift by electing a new board of directors, resulting in the company becoming a Corporation with a majority of independent members. This move is seen as improving governance issues, addressing concerns associated with its main controlling shareholder, Casino. Investors had eagerly awaited Assaí Atacadista's complete exit from Casino's ownership since the group began reducing its stake in the company last year.

If Assai Atacadista takes advantage of this new corporate model, it could potentially conduct a primary equity offering to raise funds, positively impacting the company. By using these resources, the company could reduce its high leverage. Additionally, a joint primary offering might be considered to further enhance the company's capital structure in the event of a follow-on offering.

Latest earnings results

Assaí Atacadista's latest second-quarter earnings results suffered but had some positive highlights after the negative impacts of lower revenue deceleration than its main peers like Atacadão and Central Brasileira de Distribuição.

Assaí Atacadista suffered in the second quarter due to the drop in food and commodity prices negatively impacting the gross revenue growth curve of wholesale stores in the second quarter of this year, as the disinflation of the food industry is not yet accompanied by a volume recovery.

Thus, the company presented a gross revenue of R$ 17.6 billion, around 21% above the same quarter of the previous year. The increase was mainly due to the performance of the new stores opened last year, Like-for-Like (comparable store sales), commercial strategy, and store customer flow. As a result of these efforts, the company posted market share gains of 2.4%.

Sendas Distribuidora's Investor Relations

Another highlight is the cost of goods sold, which appreciated in the quarter, reaching R$ 12.6 billion - an increase of 31% YoY. Given the figure, gross profit reached R$ 2.4 billion, increasing 33% YoY, with a small gross margin gain of 0.1%, reaching 16%.

Expense dilution showed higher-than-expected monthly turnover, as the company achieved a 2.5x sales uplift considering the Hipermercado Extra. With higher operating leverage, Assaí Atacadista's adjusted EBITDA margin was consolidated at 7% with a 10 bps increase, moving the company towards achieving its year-end guidance of 7.2% operating profitability.

Assaí Atacadista also showed improved cash generation as it showed a significant improvement in its inventories of 6 days to 45 days in Q2 2023 and also improved by one day in suppliers to 65 days in the most recent quarter. This inventory improvement gave a significant injection to operating cash generation in the quarter, which brought the company to R$ 5.4 billion, representing an improvement of R$ 2.6 billion over the same period last year.

Finally, this improvement in cash generation caused the company's net debt/EBITDA to decrease by 0.2 reaching 2.6x and thus managing to distance itself from the limits imposed by loan agreements that impose restrictions or specific obligations on the parties involved where they stand at 3x. Assaí Atacadista's goal is for the company to reach 2.2x by the end of this year, and the second quarter results hinted that this possibility remains in place.

Valuations are not particularly favorable

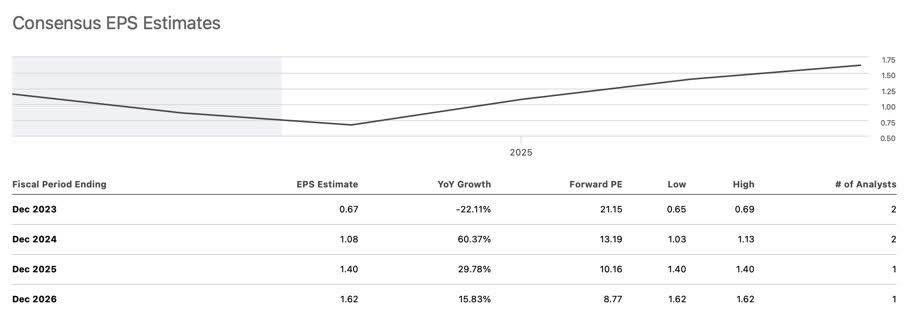

As of now, Assaí Atacadista's valuation multiples do not appear very attractive. The forward P/E ratio of 21x is above the industry average of 20x, and the consensus forecast indicates a projected 22% decline in EPS for this year. The company's margins are under pressure due to the prevailing scenario of disinflation and high-interest rates.

Looking at the earnings consensus a little further ahead, multiples look more attractive. The 2024 P/E stands at 13.1x, in 2025 at 10.1 and 2026 at 8.7x. Of course, for this scenario to materialize, Assaí Atacadista needs to conduct the growth of its operations considering the drastic reduction of the Brazilian basic interest rate in line with inflation.

{kind=link}

Seeking Alpha

According to the most recent report from the Brazilian Central Bank, the inflation forecast 2024 is expected to be below 4%, while it is projected to be 3.80% for 2025 and 3.72% for 2026. The basic interest rate (Selic) is projected to be 9.5% in 2024, 9% in 2025, and 8.75% in 2026.

On a positive note, Assaí Atacadista trades at a discounted multiple of 4x compared to its prominent domestic peer, Atacadao, which is part of the Carrefour Brasil group. This comparison considers that Atacadao has a net debt/EBITDA ratio of 2.6x, whereas Assaí Atacadista's ratio is 2.2x.

The bottom line

I think Sendas Distribuidora (Assaí Atacadista) is a great company with a competitive advantage over its national peers, focusing entirely on the cash and carry segment in the Brazilian market.

Furthermore, the recent improvements in corporate governance bode well for the company's future, especially now that Assaí Atacadista has become a diversified company.

However, the disinflation of the Brazilian economy this year has harmed Assaí Atacadista, which already faces challenges due to its high leverage from recent acquisitions and store expansions.

The prospect of lower inflation in the coming years, coupled with the expectation of the Selic rate remaining at high levels, could continue to exert pressure on the domestic food industry, potentially affecting Assaí Atacadista as well.

Although Assaí Atacadista's price-to-earnings projection for the next few years indicates a discounted valuation from 2024 onwards, the current above-industry-average valuation offers limited attractiveness, considering the macroeconomic pressures likely to affect the company.

Assaí Atacadista appears to be the top choice in the Brazilian cash and carry wholesale market compared to its peers. However, I prefer to exercise caution and remain on the sidelines. The Brazilian food industry will likely face continued pressure from disinflation and the persistent high-interest rate scenario for a while.

For further details see:

Sendas Distribuidora: Maintaining A Neutral Stance Amidst Brazilian Disinflation