SENEB - Seneca Foods: An Extremely Undervalued Market Leader (And Net-Net)

2023-12-18 11:02:42 ET

Summary

- Seneca Foods is a small-cap canned vegetables manufacturer that has seen little change in market cap over the past 10 years.

- In recent years it has undergone operational improvements, resulting in improvements in operating margins, and simultaneously it has seen a significant decrease in competition.

- The stock is extremely undervalued on all traditional metrics, and when adjusting for the LIFO Reserve, Seneca Foods is a Ben Graham style net-net.

- After huge working capital expansion in 2023, Seneca will generate significant cash next year, which will drive significant buybacks at the current depressed price.

Seneca Foods (NASDAQ: SENEA ) is a small-cap canned vegetables manufacturer, and is a great example of a boring business, not covered by any sell-side analyst, with practically zero volume growth. And it is exactly for these reasons why I believe it’s a great investment, hence the buy rating.

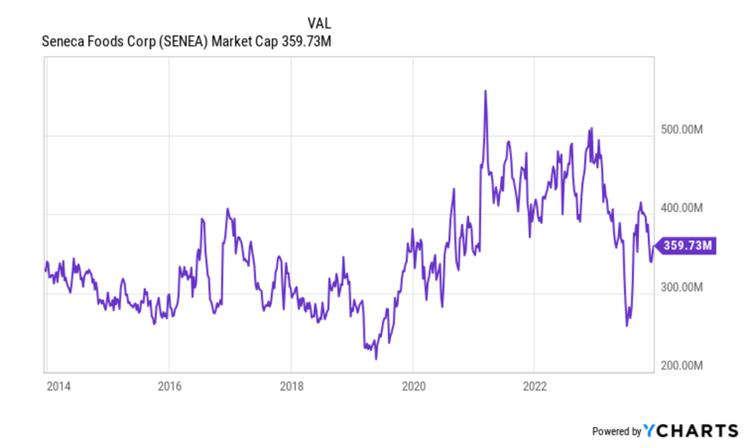

You can see from the chart below that the market cap has not done much in the past 10 years, starting at just over $300m in 2014 to the current capitalization of ~$360m, whereas the underlying business evolved and the tangible book value more than doubled.

{kind=link}

In the first section, Business Overview, I will take a look at the underlying business, then I will analyse the inventory, the competitive landscape, and subsequently the operational improvements made in recent years.

After that, in the Valuation section, I will look at where the stock is trading and look at the buyback situation. Then, before concluding, I make some considerations on catalysts and risks.

Business Overview

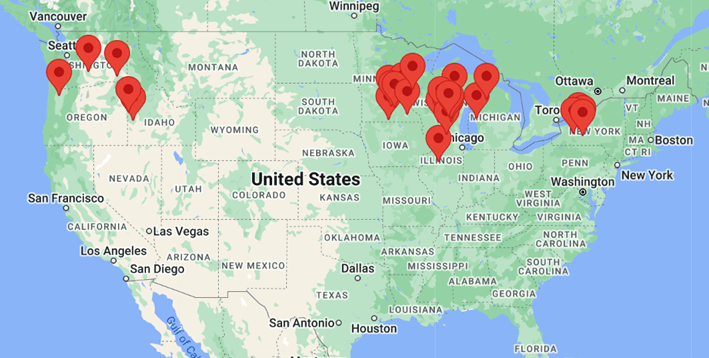

Seneca Foods is one of North America’s leading providers of canned vegetables. The company is vertically integrated, as it sources directly from 1,400 American farms and manufactures its own cans from raw tin-plated steel. It operates 26 facilities throughout 8 states in the US (see map below).

{kind=link}

Core products include canned and frozen vegetables (corn, peas, beans, etc.), and are distributed across the country mainly through grocery retailers, supermarkets and dollar stores.

Excluding co-packing, Seneca sells products both under private label and under the company's brands (which can be either owned or licensed). The most prominent brands include Seneca, Libby’s, Aunt Nellie’s, Cherryman, Green Valley, and since recently Green Giant as well, after a licensing agreement with B&G.

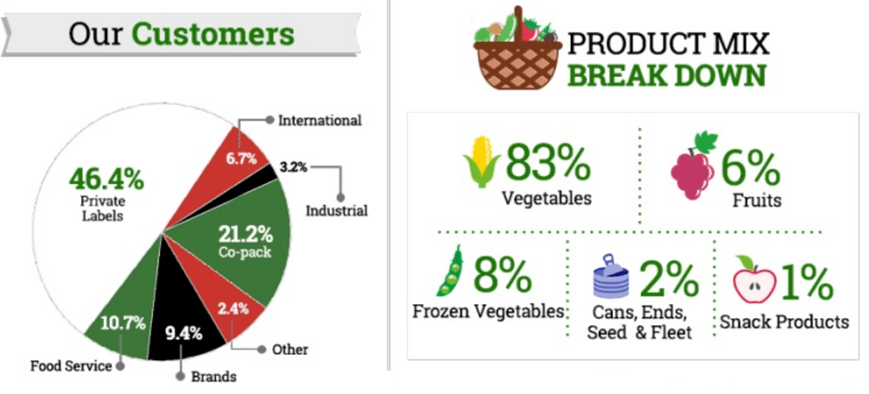

As shown in the snip below, as of 2023, around 46% of revenues came from private label, 21% from co-packing (manufacturing and packaging for other brands which have outsourced production), 11% from food service, and 10% from its own brands. Canned vegetables represent the majority of revenues, followed by frozen vegetables and fruits.

{kind=link}

Make no mistake, Seneca’s end market is not a fast growing one, quite the opposite actually. Management has previously said:

Our core canned fruit and vegetable business … has consistently exhibited stable to declining demand

( 2017 annual report , emphasis added)

Thus, any future revenue increase will most likely come from a change in the product mix, higher selling prices, or inorganic growth, and not from organic volume growth.

Inventory

One key aspect to consider for Seneca Foods is that it is highly seasonal, and I think that understanding how closely it is linked to crop yields is crucial to fundamentally understand the business. This is why I will spend a couple of paragraphs on inventory.

Little to no food packaging takes place in the last fiscal quarter (ending March 31), which corresponds to the quarter where inventory and accounts payable reach their lowest point, before the new seasonal pack (which runs from June to November) begins. During the seasonal pack, the Company builds up significant inventory, which is then sold over the next year.

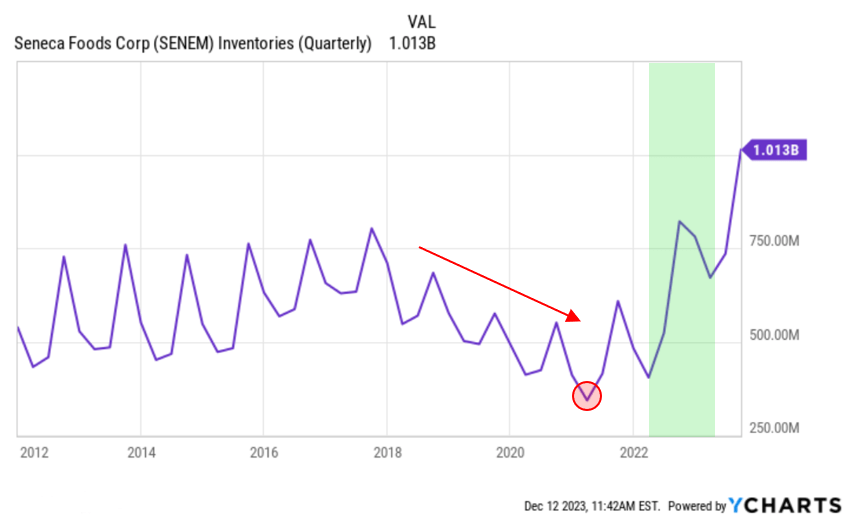

The chart below plots the inventory balance on a quarterly basis, which shows how in each year the peak is reached at end of the second quarter (September 30) and the trough is reached at the end of the fourth quarter (March 31).

{kind=link}

We can see how, starting from mid-2018 (thus in FY2019), the overall inventory level started to decrease, reaching a low point at end of FY2021 (red arrow in the chart). In the FY2020 letter to shareholders (published in mid-2020), the company wrote the following (emphasis added):

the growing season was challenging from the start to finish. … The net effect was that our company was only able to can or freeze about 91% of the crops we had originally planned for. … This was our second consecutive year of challenging growing conditions; therefore we did not have an abundance of inventories in our warehouses coming into the season . As a result, our sales force had to work with our customers to manage limited inventories in order to stay in supply to reach our goal of being a 52-week supplier to our customers.

On top of low crop yields in the 2018 and 2019 packing seasons (corresponding to FY2019 and FY2020), which prevented adequate inventory stocking, Seneca experienced a spike in demand thanks to the pandemic, which caused a further depletion in inventory. And finally, the 2020 packing season (which is in FY2021) recorded yet again challenges, as described by management in the FY2021 annual report:

The planting and growing season … still had its challenges with record breaking frost early in the season, excessive heat later in the summer and several severe storms throughout the season. The net effect was that our company was only able to can and freeze about 92% of the crops we had originally planned.

This brings us to the unusually low inventory recorded in FY2021 of ~$340m (red circle). Now, let’s focus on the most recent Fiscal Year, namely FY2023, which closed on March 31, 2023 (shaded in green in the chart). That year saw a tremendous increase in the inventory level, as the company fully restocked. According to its FY2023 annual report (emphasis added):

...overall the crops were good to excellent. Across the board our plants performed better than the previous pandemic years and combined with a favourable fall we packed near budget on all crops with our primary crop, sweet corn, coming in well over budget. The last couple of years of dealing with out of stocks are no longer a concern .

Inventory in the first 6M of FY2024 increased even further, as clear from the chart, to reach the current $1.0bn (on a LIFO basis). One might be concerned that this figure is too high, and that it could indicate that Seneca has trouble selling off its products. I do not subscribe to this view, and I believe that the company has seen such an increase for three main reasons:

1. The price at which raw materials and finished products are accounted for in the books is much higher than the past, obviously due to inflation, thus it is price that has driven the increase, not unsold volume that has piled up. The company gives a few examples of this: First, the cost of tinplated steel, used to manufacture the billions of cans that Seneca sells each year, has doubled since 2021 and reached new highs; and second, Seneca's raw product contract prices were up 50% over a two-year period, in order to stay competitive with producer alternatives to growing Seneca’s vegetable crops.

2. Due to specific issues in the steel industry, Seneca decided to increase the amount of steel held in order to avoid operational issues ( FY2023 AR , author's emphasis):

tinplate supply challenges from existing suppliers led us to expand our sourcing and increase our planned inventory of steel needed to supply our can manufacturing operations.

3. As stated already, Seneca is a highly seasonal business, and its ability to sell products depends largely on the availability and grade of crops in the farmland that Seneca sources from. If you read any shareholder’s letter you will invariably see a mention of the weather and growing conditions of that particular fiscal year’s packing season. Thus, a buildup in inventory most likely reflects a very good harvest for 2023 in terms of quantity and quality, so that if the 2024 harvest turns out to be worse or insufficient, the Company will have some inventories carry over from this year. Keep in mind that canned vegetables have multi-year expiry dates, so there is no risk of the inventory getting spoiled any time soon.

Competitive Landscape

After decades of consolidation, Seneca is among the leading canned vegetables manufacturer for private label in the US, and the rest of the market only sees a few big competitors, namely Lakeside, Del Monte US, and Allens. Harris Perlman from HSP Capital has done an excellent job in researching the competitive landscape of the canned vegetable business in the US. One of his key points is that in 2014 Del Monte started an aggressive price war in the US. In the FY2015 annual report , Seneca explained the following:

As fiscal 2015 unfolded last April, one of our large competitors was sold to offshore interests, and they immediately took a very aggressive posture in the market right through the holiday selling season. In an effort to maintain our business, we took the appropriate steps to support our business through lower prices and higher promotional activity.

However, by 2018, Perlman explains that:

By 2017/2018 the [Del Monte] US business was making an operating loss. [...]. The company brought in new leadership, and started restructuring. They stopped competing against Seneca in private-label manufacturing. In 2019 they closed some of their plants, and even sold a couple to Seneca.

Thus, from FY2019, Seneca experienced a significant reduction in competition.

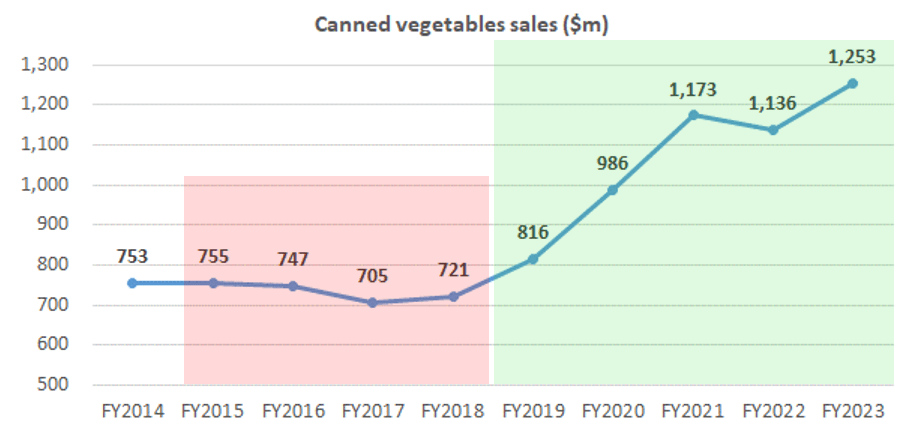

All of this can be seen in the chart below, representing Seneca’s canned vegetables sales (excluding Green Giant co-packing) (I did not plot total revenues because in 2019 Seneca exited the canned fruit business representing ~15% of sales, thus total revenues were not comparable year on year).

{kind=link}

It is clear how, from FY2015 to FY2018 (red shaded), canned vegetables sales were under pressure, with revenues slightly decreasing, due to increased competition and pricing pressure, as explained above. However, after Del Monte US stopped competing in private label, Seneca started to increase sales, thanks to additional market share and more pricing freedom (green shaded).

One objection that can be made is that competition can return any time and deteriorate Seneca’s position. However, I believe it to be unlikely. First, as competitors have seen what happened to Del Monte US after it started promoting aggressively, they are likely not foolish enough to repeat it. Secondly, Del Monte US (currently owned by holding firm Del Monte Pacific, listed in Singapore), is planning to list on the US stock market in 2024. Resuming a price war ahead of an IPO, and hurting its own profitability in the process, is generally not advisable, as the stock market wants to see strong margins and cash conversion from mature businesses like these.

Operational improvements

During FY2019, Seneca also undertook a few significant changes in its operations:

- Divestment of the canned fruit business with the sale of the Modesto plant and Washington state plants, due to worsening trends in the canned fruit segment

- Plant rationalization in canned and frozen vegetable and can-making operations, which resulted in the closure of two facilities and the sale of another

Thanks to these initiatives, the company stated in its FY2019 annual report (author’s emphasis):

When combined with the exit of the money losing canned fruit, the plant rationalization moves, and the divestitures, we expect significant improvements in our operating margins after the annual bids cycle through this fall in our core seasonal processing operations.

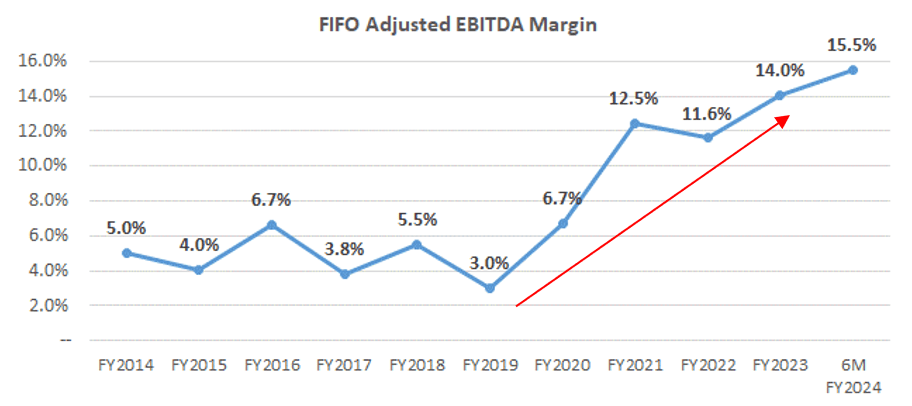

I wanted to check this statement against what actually happened afterwards, and if we look at FIFO Adjusted EBITDA margin (chart below), we can see that Seneca indeed saw a huge boost from 3.0% in FY2019, to 14.0% in FY2023.

{kind=link}

Latest developments: 6M FY2024

In the first 6 months of FY2024 (ended on September 30 , 2023), the company reported flat sales compared to 6M FY2023, but reported a 10% increase in FIFO Adjusted EBITDA to $109m, with the margin expanding to 15.5%.

Sales for the second quarter in particular were 7% lower YoY, however I believe management was expecting this, as they wrote the following in the FY2023 annual report (authors’ emphasis):

Our planned production volume for the 2022 pack season was the highest in company history …. For 2023, our volumes are down slightly reflecting a number of our customers managing inventory coming out of a very large pack season in 2022.

Thus, on a short-term basis, I think there is no evidence of a significant sales decline.

Valuation

A deep value play

The stock currently trades at roughly $50 with a total market cap of around $360m. As everyone knows by now, Seneca trades at a significant discount to book value of ~$80/share, and by even a wider margin if compared to FIFO Adjusted BV of ~$110/share (tax adjusted assuming Seneca’s recent effective tax rate of 24%). This does not include the true value of all the land and real estate that Seneca holds in its books, which are likely stated at a significant discount to current market value.

As an example of hidden value in the balance sheet, when in 2019 Seneca divested its canned fruit business with the sale of the Modesto plant and equipment, it recorded a $51.4 million gain (p.22 FY2019 annual report ). At closure of FY2019 (31 st March 2019), the company had a market capitalization of ~$240m, thus, only the gain on the sale of those operations (which represented roughly 15% of revenue) were more than 20% of the market cap at the time, whereas total proceeds from asset sales in FY2019 were $104m, or 43% of market cap. I think this clearly exemplifies how much hidden value Seneca has on its books.

However, even if we did not consider a single dollar of hidden value, at current prices the company is a Ben Graham style net-net, meaning that the Net Current Asset Value per share of ~$65 (NCAV defined in this case as Current Assets + LIFO Reserve – Total Liabilities), is higher than the share price of ~$50. This indicates that the market is attributing a value to Seneca which is less than what can be conservatively obtained from a potential liquidation of the company.

This brings me to my next point. Ben Graham, in developing his thesis for net-net stocks in his book Security Analysis, co-authored with David Dodd, allowed for objections to stocks trading at a discount to liquidation value by writing:

The objection to buying these issues lies in the probability, or at least the possibility, that earnings will decline and losses continue, and that the resources will be dissipated and the intrinsic value ultimately become less than the price paid .

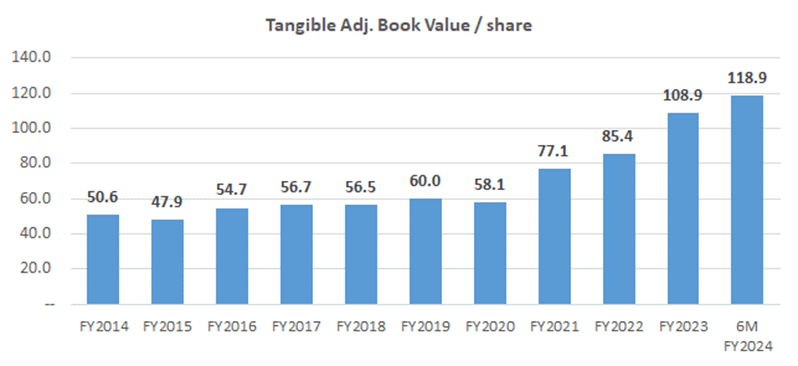

It is my belief, however, that Seneca Foods is everything but a company with mounting losses that erode its intrinsic value. Looking at the chart below, the company has doubled Tangible Adj. Book Value per share (which includes LIFO reserve not adjusted for tax) in less than 4 years.

{kind=link}

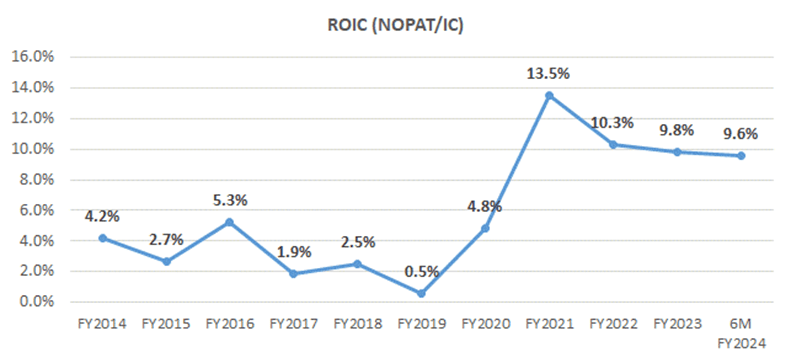

One might argue, also, that the company has almost become a quality business, if judged based on its ROIC (NOPAT defined as FIFO Adjusted EBIT * (1 - Effective tax rate of 24%), and IC adjusted with LIFO Reserve).

{kind=link}

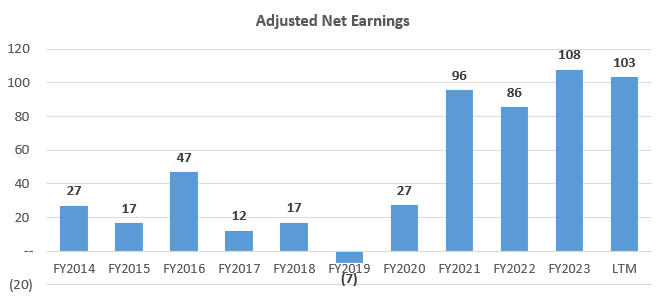

Finally, LTM adjusted earnings of Seneca sit at $103, for a trailing P/E ratio of ~3.5x, which leaves substantial margin of safety should earnings come under pressure in the future (prior to 2021 exact adjustment figures were not disclosed, thus the effective tax rate has been used).

{kind=link}

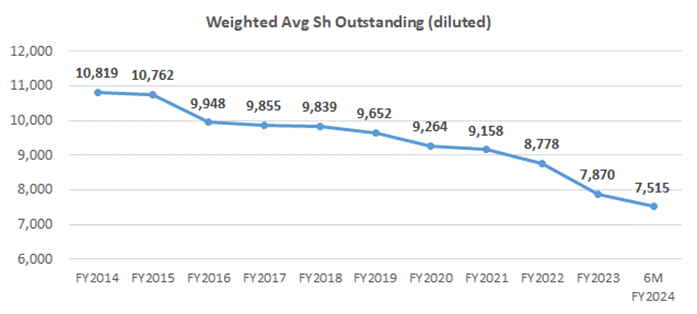

Buybacks

Management is well aware of its depressed stock price, as they have repeatedly stated in their past annual reports, and as a result they have been buying back stock, slowly but steadily (see chart below, representing weighted average shares for each period in thousands).

{kind=link}

In the latest annual report management has stated that:

In an effort to leverage our cash position driven by strong performance, and in order to maximize shareholder value, we continue to view our own stock as a value, and we continued to buy back significant shares of our own stock. During fiscal 2023 we repurchased 766,071 shares at an average price of $54.25 per share. This represents 9.2% of our outstanding shares.

Thus, they clearly believe that at $54 per share the stock is a good buy, and I tend to believe them. In addition, in 2021 the Company had announced a tender offer for the shares at a price of $46. However, only 531 shares were tendered, suggesting that investors too knew that Seneca was deeply undervalued.

Personally, I would love for the stock price to keep dropping, so that the company can repurchase shares faster. Despite the fact that management announced in the FY2023 annual report that due to the increased working capital needs they have reduced focus on the buyback program, the Company still repurchased almost $18m worth of shares in Q2 (July through September) reducing share count by 4.5%.

As an additional note, on the 6 th of December, the CFO, Michael Wolcott, purchased ~1.5k shares in the open market at an average price of $50.54, for a total sum of almost $80,000. Even if the absolute amount is not extremely high, and even if it only represented a 3% increase in his holdings, I still believe this to be a bullish signal.

To conclude, it is clear how the market is not appreciating the evolution of Seneca Foods, that has become a leading canned vegetables producer, with significant scale and increased pricing power compared to the past. In fact, its current market cap is roughly in the past 10-years’ trading range, as shown in the chart below. I believe this presents a compelling asymmetric opportunity with a substantial margin of safety, supported on the downside by decisive buybacks and solid asset values.

Catalysts

In this type of deep value stocks it is useful to check whether there are any catalysts in sight. The first and most obvious one is that, in the next 2 quarters, as Seneca progressively disposes of its inventory at a healthy margin, it will generate substantial cash to pay down the revolving credit facility and resume a more aggressive buyback of the stock. Currently, FIFO Net Working Capital (NWC, defined as A/R + FIFO Inventory – A/P) sits at ~$1.1bn, and the revolving credit facility is drawn for $135m. If by end of Q4 FY2024 Seneca manages to shrink its NWC by just 25%, after paying down the revolver in full it will have ~$150m in additional cash flow from operations, or roughly 40% of market cap, on top of any operating cash flow generated before NWC changes. I believe this will give Seneca enough firepower to pursue buybacks.

Another catalyst is the planned IPO of Del Monte US in 2024 that I mentioned earlier. If a new peer comes to public markets, it will help boost the current coverage of the fruit and vegetables canning industry, at least during the marketing phase of the offering. This in turn will hopefully attract investors’ attention to Seneca Foods and boost its multiple upwards.

Risks

Let’s look at a few risks now. Seneca is on the low side for small cap stocks, and its liquidity is not the greatest, with daily average volume of just 44k shares. These types of stocks usually carry higher risk, however I believe it not to be that significant.

Regarding the debt position of Seneca, while it may appear high (net debt including leases increased from $480m at end FY2023 to $540m at end Q2 FY2024), I believe that it simply followed the working capital expansion. If you think about it, with what else should the company have funded that increase in inventory? Most certainly not with equity. Here are a few lines of commentary from management regarding the financial position and liquidity:

In an effort to provide capacity on the balance sheet for previously mentioned steel inventory, the large pack and any potential acquisition opportunities, we have taken on new term debt …. In January we closed on a $175 million term loan through Farm Credit East and subsequently upsized by another $125 million in May, putting us in a very solid balance sheet and liquidity position.

Net Debt / LTM FIFO Adj. EBITDA currently stands at 2.4x, still very manageable in my opinion.

One thing that I believe investors should be cautious with, is the fact that in July the company had to restate its accounts ( form 8-k ), due to a material misstatement relating to the accounting for valuing inventory using the LIFO method, and the related internal controls. Furthermore, just one month prior, the company’s auditor Plante Moran PC notified Seneca that it would decline to stand for reappointment, leaving the place for current auditor Deloitte . A similar event happened in 2019, when in June 2019 audit firm BDO expressed an adverse opinion on the company’s effectiveness of internal control over financial reporting. Two months later, in August 2019, Seneca’s audit committee approved the dismissal of BDO as auditor.

Overall, I must say that this matter is a bit tricky. However, it is true that the FY2023 10-K restatement only related to the valuation of inventory under LIFO, and had no impact on FIFO results. Given that the company moves billions of items per year and has a LIFO reserve going back decades, an error in the LIFO accounting does not bother me too much. In addition, all the relevant metrics that I presented in this article are adjusted for FIFO, which paints a more realistic picture of the underlying business and which was not affected by the restatement. For these reasons, I think that the audit matter does not present a significant risk to the thesis.

As a final note, I want to mention the conservatism of management with one sentence from the FY2023 annual report that I think highlights how they are responsibly managing a business for the long term:

With the completion of another year of encouraging performance, we must continue to keep in mind that we are in a commodity business that is subject to inherent ups and downs. ... we believe a key is that the Company has a strong balance sheet and the financial wherewithal to ride out whatever challenges lie ahead.

Conclusion

To sum up, Seneca Foods is an under-followed stock that has experienced quite an evolution in the past 5 years into an operationally strong leader in the canned vegetables space. The market, however, has not noticed such evolution. I believe that future positive earnings will allow Seneca to boost its share buyback program, and this will ultimately boost the share price as well. I have no specific target price, but I would expect the stock to at least converge to reported book value per share of ~$80, representing 60% of upside from current levels.

The most important aspect of this opportunity, however, is the margin of safety, reflected in an incredible amount of net asset value not priced by the stock. Thus, as a famous investing quote goes, if the downside is protected, the upside will take care of itself.

Editor's Note: This article was submitted as part of Seeking Alpha's Top 2024 Long/Short competition, which runs through December 31 . With cash prizes, this competition -- open to all contributors -- is one you don't want to miss. If you are interested in becoming a contributor and taking part in the competition, click here to find out more and submit your article today!

For further details see:

Seneca Foods: An Extremely Undervalued Market Leader (And Net-Net)