BKLN - Senior Loans (BKLN) Vs. High-Yield Corporate Bonds (HYG) Which Is Best For Income Investors And Retirees?

2023-07-10 10:58:15 ET

Summary

- Higher interest rates have led to higher yields on most bonds and bond funds.

- Senior loans and high-yield corporate bonds both offer investors particularly strong, growing dividends.

- A comparison of these two securities follows.

Author's note: This article was released to CEF/ETF Income Laboratory members on June 26th.

Senior loans and high-yield corporate bonds are two of the most common, highest-yielding, sub-asset classes in the market today. These securities have many similarities, with some key differences.

Both offer investors strong, growing dividends. Senior loans have higher yields, and faster dividend growth, however.

Both have high levels of credit risk.

Senior loans have almost no interest rate risk, while high-yield bonds have below-average interest rate risk.

Senior loan ETFs tend to be more expensive than high-yield corporate bond ETFs.

In my opinion, senior loans are the superior investment opportunity right now, due to their higher yields and faster dividend growth.

I'll be focusing on the Invesco Senior Loan ETF ( BKLN ) and the iShares iBoxx $ High Yield Corporate Bond ETF ( HYG ), the two largest index funds for their respective securities, for the remainder of this article. Everything here should apply to the senior loan and high-yield corporate bond funds in roughly equal measure.

Senior Loans versus High-Yield Corporate Bonds

Security Comparison

Senior loans are senior secured variable rate loans from non-investment grade corporations.

These loans are senior to other debt, and secured by company assets.

These loans are almost always variable rate loans, indexed to specific benchmark rates, and so see higher coupon rates when interest rates rise. Most are indexed to LIBOR or SOFR, which closely track the federal funds rate.

Rates are reset at specific intervals, generally quarterly.

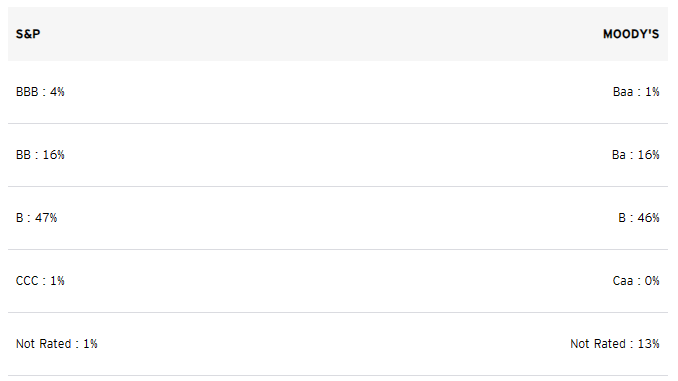

These loans are generally issued by mid-sized corporations with non-investment grade credit ratings. These are risky issuers, but not excessively so. For reference, BKLN's credit profile.

{kind=link}

High-yield corporate bonds are fixed-rate bonds issued by non-investment grade corporations.

As rates are fixed, these securities do not see higher coupon rates when interest rates rise. Funds focusing on these securities do, with some delay, as their investments mature, and are replaced by newer, higher-yielding alternatives.

These securities are issued by relatively risky issuers, but not excessively so. For reference, HYG's credit profile.

HYG

The biggest difference between senior loans and high-yield bonds is that the loans are variable rate, while the bonds are fixed-rate. Which brings me to my next point.

Interest Rate Risk Comparison

High-yield corporate bonds see lower prices when interest rates rise, as investors focus on newer, higher-yielding issues. As an example, let's have a quick look at one of HYG's largest positions. (Data as of late June)

HYG

Simplifying things a bit, we can say that HYG loaned $76.6M, as per its par value, to Mozart Debt Merger Sub at a 3.88% coupon rate, from 2021 to 2029. Said rate made sense at the time, with Fed rates at 0.0%, and 10Y treasuries yielding 1.50%. As the Fed hiked rates, however, that 3.88% became less and less compelling. Demand for these bonds started to drop, causing prices to drop by around 12%, with HYG's investment dropping in value from $76.6M, par value, to $67.2M, notional value.

As rates rose, demand for HYG's portfolio of bonds decreased, leading to lower prices. HYG's share price is down 15.1% since early 2022, broadly consistent with the performance of the specific bond above.

High-yield corporate bonds tend to have lower interest rate risk than other bonds, due to having comparatively low maturities. Less selling pressure on short-term bonds when rates rise, as these are quickly replaced, so investors are stuck with low coupons for a shorter period of time. HYG has outperformed other bond sub-asset classes since rates started to rise, as expected.

Senior loans tend to see sustained demand and prices when interest rates rise, as their coupon rates increase too: no reason to sell a lower-yielding security if it will turn into a higher-yielding one in a couple of months.

Senior loans might see some losses when interest rates rise, due to changes in investor sentiment, market fluctuations, widening spreads, and any changes in interest rates are somewhat delayed (usually by a quarter). Still, losses should be small, as has been the case for BKLN since early 2022.

As should be clear from the above, senior loans have significantly less interest rate risk than high-yield bonds. Expect senior loans to outperform when rates rise, due to lower capital losses, as has been the case since early 2022.

Senior loan funds should also see swifter dividend growth when interest rates rise, as it generally takes a few months for a loan's rate to be reset, but several years for a bond to mature. This has been the case for BKLN since early 2022, as expected.

Senior loans have significantly lower interest rate risk than high-yield bonds, an important benefit for investors. As the Federal Reserve is slowing down the pace of hikes, pausing these at their last meeting, lower rate risk is unlikely to have any tangible short-term benefits, but the long-term impact will likely be positive.

On the other hand, the higher interest rate risk of high-yield bonds should cause these to outperform if interest rates decrease by more than expected . Several rate cuts are priced-in, as evidenced by an inverted yield curve , and these would have a limited impact on bond prices. A closer look at market expectations of future rate cuts, and implications thereof, seems warranted, but these issues are very dependent on sentiment, which is sometimes irrational, and extremely difficult to forecast.

Credit Risk Comparison

Senior loans and high-yield bonds are both non-investment grade securities, with high credit risk.

BKLN focuses on securities rated B.

HYG focuses on securities rated BB.

HYG

BKLN's senior loans are, well, senior to other debt, and secured by company assets. The same is not necessarily true for HYG.

Senior loans and high-yield bonds both have comparable, high levels of credit risk. Expect high losses during downturns and recessions, as was the case in 1Q2020, the onset of the coronavirus pandemic, and the most recent recession. BKLN technically saw higher losses, but recovered a bit faster too.

Data by YCharts

Considering their credit risk, more conservative income investors and retirees might wish to avoid both securities and funds.

Dividend Comparison

Both senior loans and high-yield bonds have comparatively strong yields, as compensation for their high credit risk.

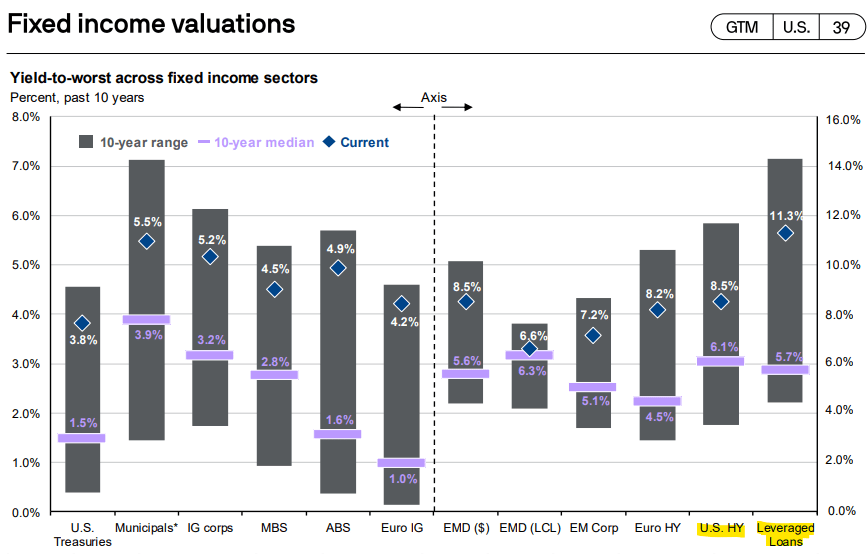

Senior loans currently yield 11.3%, the highest in the fixed-income space, versus 8.5% for high-yield corporate bonds. Data as per JPMorgan ( JPM ), senior loans are referred to as leveraged loans in the graph below.

{kind=link}

As per SA, BKLN currently sports a 7.1% yield, while HYG yields 5.8%. Both figures are somewhat volatile, however.

Both funds yield less than their respective asset class , as it takes a while for higher interest rates to cause higher fund income, and for funds to distribute excess income to investors as dividends. Still, bond fund yields should be quite close to those of their underlying assets, so both funds should see dividend growth until this is the case.

Although both senior loans and high-yield corporate bonds have strong dividends, senior loan dividends are a bit stronger, for four reasons.

First, is the simple fact that senior loans have higher yields. This is true at the asset level, as per JPMorgan, and at the fund level, as per the graph above. Higher yields are almost always beneficial for investors, and senior loans are no exception.

Second is the fact that senior loan funds see swifter dividend growth when interest rates rise, as it generally takes a few months for a loan's rate to be reset, but several years for a bond to mature. This has been the case for BKLN since early 2022, as expected.

Senior loans should continue to see fast dividend growth for at least a couple more months, due to previous Fed hikes. Medium-term and long-term dividend growth is dependent on future Fed hikes, which are obviously not certain.

Third, is the fact that senior loans have the most value out of all fixed-income asset classes right now, with much, much higher yields than their historical averages. All fixed-income asset classes yield more right now than in the past, but the gap is widest for senior loans, and by a healthy margin.

Fourth, is the fact that senior loan yields relative to high-yield bond yields are also much wider than their historical averages. BKLN itself yields around 1.0-1.5% more than HYG, a much wider spread than average (never mind the volatility in the graph below, it is a data calculation issue).

Senior loans have higher dividends and stronger dividend growth than high-yield corporate bonds, a significant benefit for investors. In my opinion, as yields currently stand, senior loans are currently the stronger investment.

Expenses Comparison

Senior loan ETFs tend to be more expensive than high-yield bond ETFs. Most of the difference is due to the existence of several cheap ETFs in the latter group, including the SPDR Portfolio High Yield Bond ETF ( SPHY ), with a 0.10% expense ratio, and the iShares Broad USD High Yield Corporate Bond ETF ( USHY ), with 0.15% in expenses. A quick table of some of the larger ETFs in each category.

Seeking Alpha - Chart by author

The lower expenses of high-yield bond ETFs are a significant benefit to investors, and a key advantage relative to senior loan ETFs. Quantitatively, said benefit is quite low, averaging 0.35%, and is quite a bit lower than the difference in yield between these funds and their respective asset class, averaging 2.0-3.0%.

In my opinion, the greater yield on senior loans outweighs their excess expenses, but the situation is not all that clear cut, and I had some difficulties in arriving at said conclusion. Lower expenses are a more reliable, consistent, long-lasting benefit than dividends, which are sometimes fickle, and more volatile. Senior loans have seen swift dividend growth from recent Federal Reserve hikes and would almost certainly see swift dividend cuts from lower rates too. The higher dividends on these securities are not certain.

As an aside, I've grown more bullish on senior loans in the recent past, as Federal Reserve hikes have been a bit more aggressive than I expected, and some of these were not reflected in senior loan ETF dividends in prior months. I was bullish before , and during, most of the hiking phase, however.

Performance Comparison

Senior loans tend to yield a bit less than high-yield bonds, and their funds tend to be more expensive, so their long-term performance should be a little bit weaker. This has been the case for BKLN since inception, as expected.

Senior loans have lower interest rate risk and have seen stronger dividends in the recent past, allowing them to outperform since early 2022, when the Fed started to hike.

Recent gains have allowed senior loans to outperform for several other time periods, including the 5Y mark. Do bear in mind, outperformance was entirely concentrated from 2022 onwards, it's just that these recent gains outweighed underperformance in prior years.

Data by YCharts

Long-term, high-yield corporate bonds seem like the stronger, better-performing asset class. Right now, under current conditions, senior loans seem stronger.

Conclusion

Senior loans and high-yield corporate bonds have broadly similar characteristics, with some key differences. Right now, senior loans offer investors higher yields and stronger dividend growth, making them broadly superior investments, in my opinion at least.

For further details see:

Senior Loans (BKLN) Vs. High-Yield Corporate Bonds (HYG), Which Is Best For Income Investors And Retirees?