JAAA - Senior Loans Or CLO Debt Which Is Best For Income Investors And Retirees?

2023-09-23 08:16:31 ET

Summary

- Federal Reserve hikes have led to strong dividend growth in most variable rate securities and funds.

- Two of these are senior loans and CLO debt tranches.

- A look at the similarities, and differences, between these two asset classes follows.

Summary

I've written several articles on senior loans and CLO debt ETFs in the recent past . I've been bullish, due to the strong, above-average, growing dividends that these securities and funds offer investors. Looking back at previous articles, I'm not sure that the distinction between these asset classes is all that clear, so thought to write an article looking at these.

Senior secured loans are variable rate loans from banks to medium-sized, riskier companies.

CLOs are bundles of senior loans, with similar variable rates. This is something of a simplification.

Both asset classes have extremely low interest rate risks, due to their variable rates. Both sport strong, above-average, and growing dividends too, due to recent Federal Reserve hikes. CLOs seem to have higher yields, at least the riskier ones.

CLOs have more complicated structures than senior loans. Complexity is a risk in itself, and it makes analyzing these securities and funds more difficult.

Senior loans have higher credit risk than most CLOs, with the exception of the riskiest ones (equity tranches). Lower credit risk does not translate into lower realized volatility for most CLO ETFs, however.

CLOs have several tranches, which gives investors greater flexibility, and allows them to more easily focus on funds with their desired risk-return profile. More conservative investors might focus on AAA-rated CLOs and CLO funds, more aggressive ones might prefer BBB-rated ones.

In my opinion, both senior loans and CLO debt ETFs have similar strong value propositions, and both are buys. On net CLOs seem better, but their complexity makes it difficult to know for certain.

As a general disclaimer, everything here applies to most senior loans, CLO debt tranches, and funds investing in these securities. There most certainly are exceptions, but not that many.

Senior Loans and CLOs - Overview

A quick overview of these two asset classes, before tackling their similarities and differences.

Companies sometimes issue debt, to finance their expansion plans, operations, possible mergers, etc. Some debt is issued as senior secured variable rate loans. Said debt is senior to other debt, secured by company assets, and pays a variable rate of interest, generally indexed to the SOFR, in practice to Federal Reserve funds rate.

Senior loans are the debt above. Senior loan ETFs invest in said debt directly.

Senior loans are sometimes bundled together in CLOs. Each CLO, or bundle of senior loans, is divided into tranches. Income from the senior loans is used to make payments to all tranches. Payments are variable rate, similar conditions to senior loans. Senior tranches get paid first, junior tranches get paid last. CLO ETFs invest in these tranches and receive payments for doing so. A quick look as to how CLOs are structured.

Stanford Chemist - Seeking Alpha

There are ETFs focusing on specific CLO tranches. I'll be focusing on the following three for the remainder of this article.

Fund Filings - Chart by Author

As a simple summary, senior loans are variable rate corporate loans, while CLOs are bundles of senior loans. As should be obvious, there are many similarities between senior loans and CLOs, but some key differences too. Let's have a look at these, starting with the differences.

Senior Loans and CLO Debt ETFs - Differences

Payment Priority

In the event of a default, senior loan investors receive less in income and capital repayment. As an example, the Invesco Senior Loan ETF's ( BKLN ), the benchmark senior loan ETF, invests quite heavily in a loan from Peraton Corporation. If Peraton defaults on its loan, BKLN would receive less in income, leading to dividend cuts. BKLN's share price should decrease as well.

The situation is different for investors in CLO tranches and CLO debt ETFs. As an example, let's assume that the Peraton corporation loan is bundled into a CLO, and that the Janus Henderson AAA CLO ETF ( JAAA ) invests in the AAA tranche of said CLO. If Peraton defaults on its loan, all losses and dividend cuts would fall to the junior-most tranche, the equity tranche in this case. JAAA focuses on AAA-rated tranches, and so would see no losses. In other words, JAAA's dividends would be prioritized over those of other CLO tranches / CLO investors.

Once equity investors are wiped out, all losses and dividend cuts would fall to the BB tranche. Once that tranche is wiped out, losses would fall to the BBB tranche, and so on. In practice, investors in CLO debt tranches rarely experience defaults. As a reminder, I'm only discussing CLO debt ETFs in this paragraph, and senior loans are not prioritized in the same way.

Credit Risk

Senior loans tend to have default rates in the 2.0% - 3.0% range , higher than average, but still quite low on an absolute basis. Default rates were at 0.85% earlier in the year, much lower than average due to strong economic fundamentals and (past) low interest rates. Defaults have increased all year, and are expected to reach +2.5% later in the year.

CLO debt tranches and ETFs have very low default rates, because equity tranches are the first to bear any losses and, in practice, generally bear all losses. As per S&P, A-rated tranches have annual default rates of 0%. BB-rated tranches default rates of only 0.02%. These are very low figures, and much lower than those of senior loans themselves. The more junior CLO tranches do have higher default rates, but I'm not discussing these in this article.

S&P

CLO Tranches - Greater Investor Flexibility

The existence of CLO tranches, and of ETFs focusing on different tranches, allows investors greater flexibility in their investment / preferred risk-return profile. Risk-averse investors can focus on more senior tranches / ETFs, including JAAA. More aggressive, yield-seeking investors can focus on more junior tranches / ETFs, including CLOZ.

As there are several senior loan funds out there, investors do have some flexibility in these securities, but not a whole lot. Funds focusing on other variable rate securities might work too, however.

Complexity

Senior loans are generally simple investments. CLOs are not. Complexity is a risk in itself, and it makes analyzing these securities and funds more difficult.

Senior Loans and CLO Debt ETFs - Similarities

Strong Growing Dividends

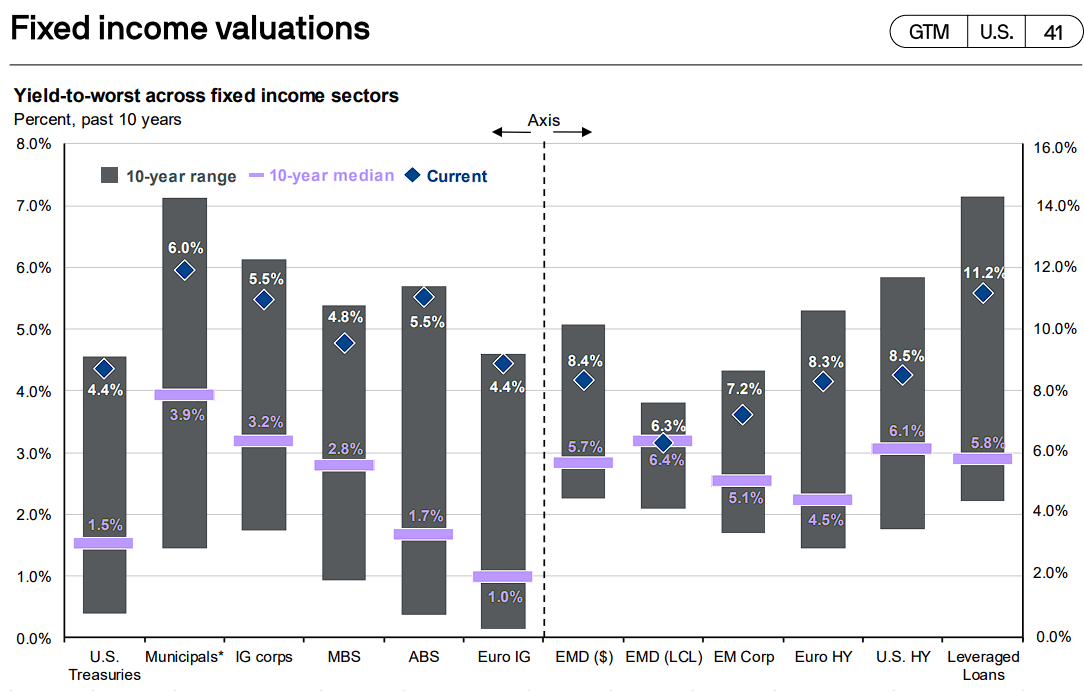

Senior loans are the highest-yielding fixed-income securities in the market right now, with a 11.2% yield. These are the highest dividends in the market, and much higher than their historical average too.

{kind=link}

The above is almost entirely due to recent Federal Reserve hikes. Remember, senior loans are variable rate loans, and see higher coupon rates when the Fed hikes, and the Fed has hiked really aggressively these two years. Benchmark rates are up by 5.25% since early 2022, and further hikes are possible.

Data by YCharts

Senior loan ETFs also sport strong dividend yields, with the benchmark Invesco Senior Loan ETF ( BKLN ) sporting a 8.5% SEC yield, higher than that of most other fixed-income asset classes.

Fund Filings - Chart by Author

BKLN's yield is somewhat lower than that of its underlying asset class / J.P. Morgan data, because it takes some time for higher Fed rates to impact investment markets, and for ETFs to reflect that.

CLO debt ETFs also sport strong yields, somewhat dependent on their focused tranche. Those focusing on higher-quality, more senior tranches have lower yields, as expected. Do remember that senior tranches are, well, senior, so get paid first, minimizing losses.

Fund Filings - Chart by Author

Corollary of the above is that both senior loans and CLO debt ETFs have seen very strong dividend growth since early 2022, due to Fed hikes. I've excluded the Panagram Bbb-B Clo ETF ( CLOZ ) from the graph below, as the fund is too young to have a material dividend growth track-record.

Senior loan and CLO debt ETFs offer the highest dividends in the fixed-income market. These are significant benefits for the funds and their investors and, in my opinion, make them strong buys.

Extremely Low Interest Rate Risk

Both senior loans and CLO debt tranches have variable interest rates, which significantly reduces interest rate risk. Dividend growth tends to be swift and strong when the Fed hikes, as can be seen above. Performance tends to be quite strong too, as has been the case for most these ETFs since early 2022, when the Fed started to hike.

CLOZ is a much younger fund, being created in early 2023, and it also has outperformed since inception.

Both senior loans and CLO debt ETFs have extremely low interest rate risk, leading to outperformance when rates rise. As the Fed has significantly slowed down / paused the pace of hikes this is unlikely to benefit investors in the short-term, but it is undoubtedly a long-term benefit.

Value Proposition and Investment Thesis

Putting aside all issues of tranches, credit risk, and complexity aside, both senior loans and CLOs have similar value propositions and investment thesis. Both offer investors strong, growing dividends, are variable rate, have extremely low interest rate risk, and have outperformed these past two years. This is a strong value proposition and make these investments very similar to each other.

Senior Loans versus CLO Debt - Key Consideration

CLO debt tranches have lower default rates than senior loans. As a reminder, senior loan default rates currently stand at 0.85%, versus only 0.02% for BB-rated tranches. Longer-term default rates for both are higher, but senior loans remain much riskier.

S&P

CLO debt yields are very strong for their credit risk, with investment-grade BBB-rated tranches yielding slightly more than high-yield corporate bonds. BB-rated tranches yield a lot more.

Fund Filings - Chart by Author

From the above, it seems that CLO debt ETFs have outstanding risk-return. There is a catch, however, with most CLO debt ETFs trading with more volatility than expected. JAAA, for instance, is about 4x more volatile than t-bills, even though both have comparable credit and interest rate risk.

Overall volatility is still quite low for these ETFs, however.

In my opinion, CLO debt ETFs are stronger investment opportunities than senior loan ETFs, due to their comparatively low credit risk, and outstanding risk-return profile. Still, these are broadly similar securities and funds, with similar value propositions.

Conclusion

Senior loans and CLO debt tranches both offer investors strong, growing dividends, are variable rate, and have outperformed since early 2022. In my opinion, both are strong investment opportunities, and buys.

For further details see:

Senior Loans Or CLO Debt, Which Is Best For Income Investors And Retirees?