ST - Sensata Technologies: IoT Sensor Market Growth And M&A Imply $73 Price Target

2023-04-27 14:56:39 ET

Summary

- Sensata Technologies Holding is a global industrial technology company that develops, manufactures, and sells sensors and rich sensor solutions, components, and electrical protection systems, among other products.

- It is also worth noting that the IoT sensor market size is expected to grow at a CAGR of close to 28% from 2021 to 2030.

- Sensata appears to buy targets for obtaining new technologies and capabilities.

- Xirgo Technologies, LLC, Elastic, SmartWitness Holdings, Inc., and Dynapower brought new types of data insights to transportation and logistics customers as well as sensor-based insights.

Sensata Technologies Holding plc (ST) operates in growing markets like the IoT sensor market, and has exposure to very different sectors and a large portfolio of products. I believe that further electrification of the economy and growth of the demand for electric vehicles will likely bring revenue growth expectations. Besides, under my DCF model, further efficiency, successful integration of the recent targets acquired, and more demand from companies' leading operations of light- through heavy-duty vehicles could bring significant FCF generation. My financial model implied a valuation of $73 per share.

Sensata Technologies Offers Many Products, And Benefits From The EV Industry And The Electrification Of The Economy

Sensata Technologies Holding is a global industrial technology company that develops, manufactures, and sells sensors and rich sensor solutions, components, and electrical protection systems among other products.

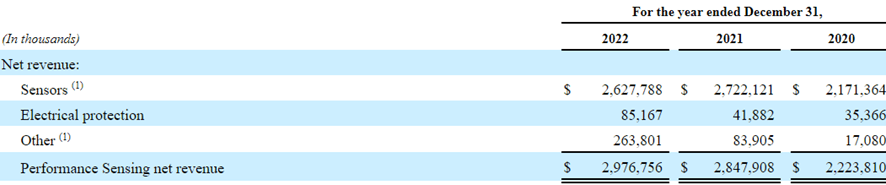

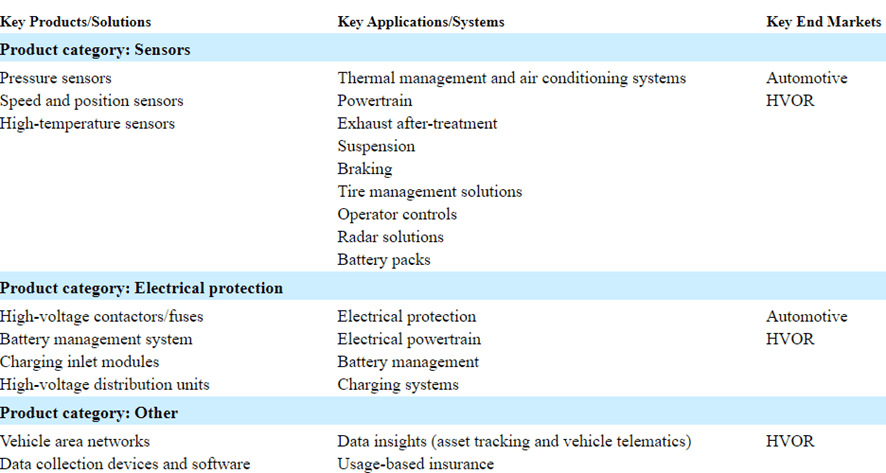

Its sensors are used by clients to translate a physical parameter into electronic signals to act on their products and solutions. Most revenue comes from the sale of sensors, however the company offers a long list of other devices and technologies.

{kind=link}

{kind=link}

In addition, its electrical protection portfolio includes switches, fuses, battery management systems, inverters, energy storage systems, high-voltage distribution units, controllers, and software. The customers of the company's products include original equipment manufacturers and multinational companies, and the company has long term agreements with its clients. Sensata seeks to help its clients comply with regulatory mandates and consumer demand to make their products safer, cleaner, more efficient, electrified, and connected.

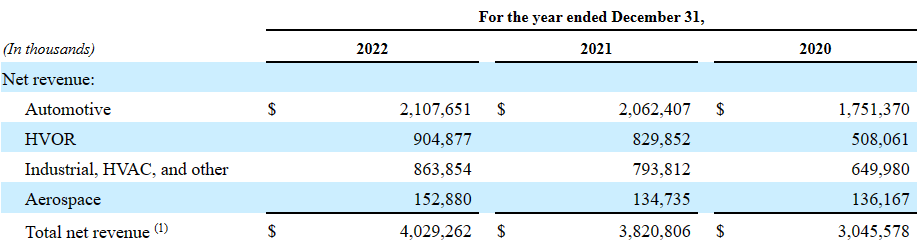

Sensata derives a significant portion of its revenue from sales to the automotive end market, while also selling products and solutions to end users in various industries, end markets, and geographic regions. The increase in sales growth mainly in 2020 was quite significant.

{kind=link}

Demand for these products and solutions is influenced by various factors such as industry, market, and geographic conditions. General net income is subject to fluctuations in foreign currency exchange rates and the net effect of acquisitions and divestitures. In general, the company operates in multiple industries and geographic markets, and seeks to maintain a steady stream of revenue through its diversification.

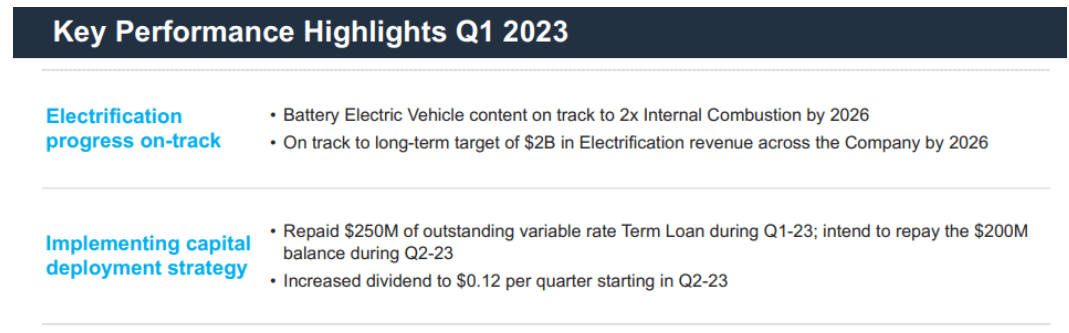

In the last quarterly report , management mentioned a few revenue catalysts for the next three to four years. For instance, Sensata is expected to benefit from the increase in demand for battery electric vehicles and the electrification progress of other industries. The company believes that the market for its Electrification revenue could stand at close to $2 billion by 2026.

Source: Quarterly Earnings Report

{kind=link}

The numbers for Q1 2023 were not very impressive, but investors may want to have a look. Revenue growth increased q/q close to 2.3%, with 14% increase in adjusted net income and double-digit adjusted EPS growth.

Source: Quarterly Earnings Report

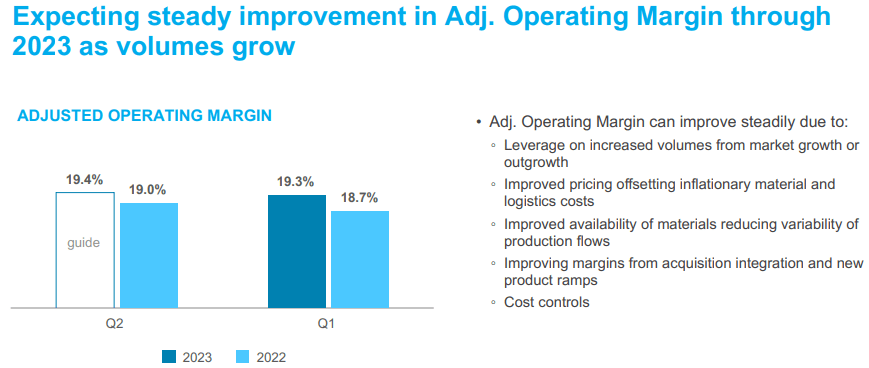

With that about the previous results, I believe that the most interesting was the guidance given by management for 2023. I believe that the long term forecasts of many analysts will likely increase considering the guidance. Sensata believes that adjusted operating margin could increase driven by cost controls, new production ramps, acquisitions, and improved availability of materials.

Source: Quarterly Earnings Report

{kind=link}

Q2 2023 guidance included adjusted net income growth close to 6%-17%, adjusted EPS growth of around 6%-18%, and small revenue growth.

Source: Quarterly Earnings Report

Beneficial Expectations With Double-Digit Net Income Growth

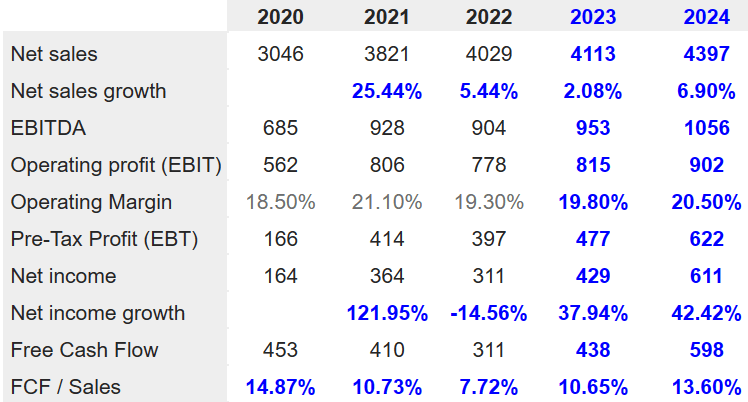

I believe that the investors may want to have a look at the expectations from other analysts. I believe that they are optimistic. 2024 net sales are expected to be $4.397 billion, with net sales growth of 6.9%, 2024 EBITDA of $1.056 billion, and net income of $611 million. It is worth noting that net income growth is expected to be close to 42%. Besides, 2024 free cash flow would stand at $598 million with FCF/Sales margin of 13%.

{kind=link}

Balance Sheet Includes A Significant Amount Of Debt And A Lot Of Goodwill

The balance sheet includes a large amount of goodwill from acquisitions that seem to be financed by a significant amount of debt. Sensata appears to buy targets for obtaining new technologies and capabilities. Xirgo Technologies, LLC, Elastic, SmartWitness Holdings, Inc., and Dynapower brought new types of data insights to transportation and logistics customers as well as sensor-based insights.

With the acquisitions of Xirgo Technologies, LLC and SmartWitness Holdings, Inc., we expanded our capabilities to provide data insights to transportation and logistics customers through telematics, video telematics, asset tracking devices, and other cloud-based solutions. In addition, the fiscal year 2022 acquisition of Elastic M2M, Inc. augments our cloud capabilities critical to delivering actionable sensor-based insights, an increasingly important capability in this fast-growing industry segment. Source: 10-k

{kind=link}

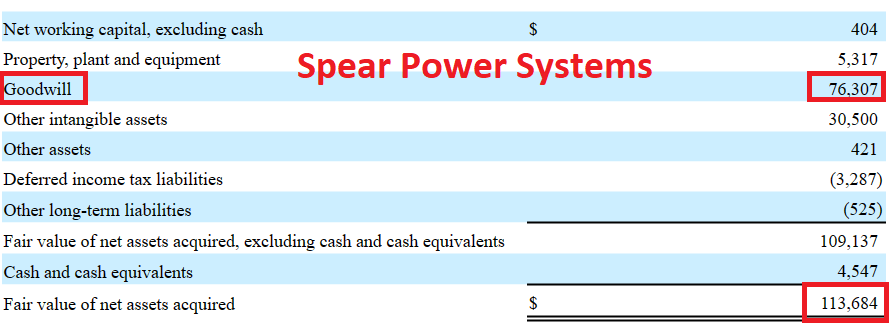

I believe in having a close look at the financials of targets. For instance, Spear Power Systems included a significant amount of goodwill. The fair value of the net assets acquired stood at $113 million, and the goodwill was equal to $76 million. It means that Sensata expects a lot of business growth from Spear.

We acquired all of the equity interests in Spear Power Systems ("Spear"), a leader in electrification solutions that supports our newly established Clean Energy Solutions business unit, for an aggregate purchase price of $113.7 million, subject to certain post-closing items, including a contingent consideration arrangement whereby we may be required to pay up to an additional $30.0 million to the selling shareholders. Source: 10-k

{kind=link}

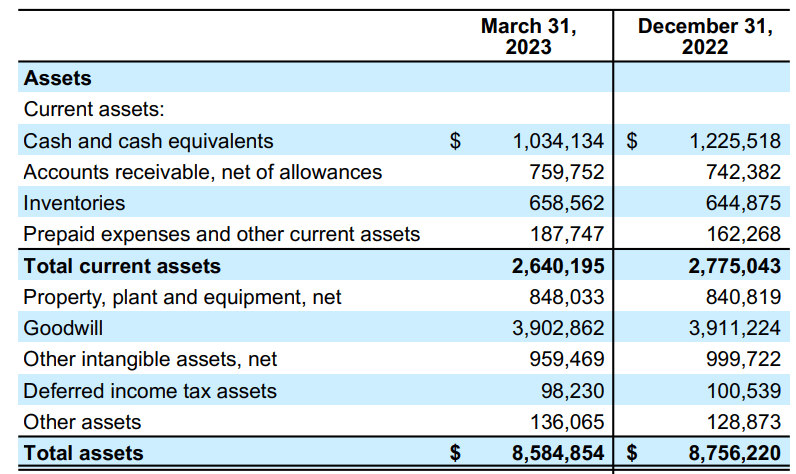

As of March 31, 2023, Sensata reported cash and cash equivalents of $1.034 billion, accounts receivable close to $759 million, inventories of $658 million, prepaid expenses close to $187 million, and total current assets worth $2.640 billion.

Also, with property, plant and equipment of $848 million, goodwill around $3.902 million, and other intangible assets of $959 million, total assets stand at $8.584 billion. The asset/liability ratio is more than 1x, so I believe that Sensata reports a stable financial valuation.

Source: Quarterly Earnings Release

{kind=link}

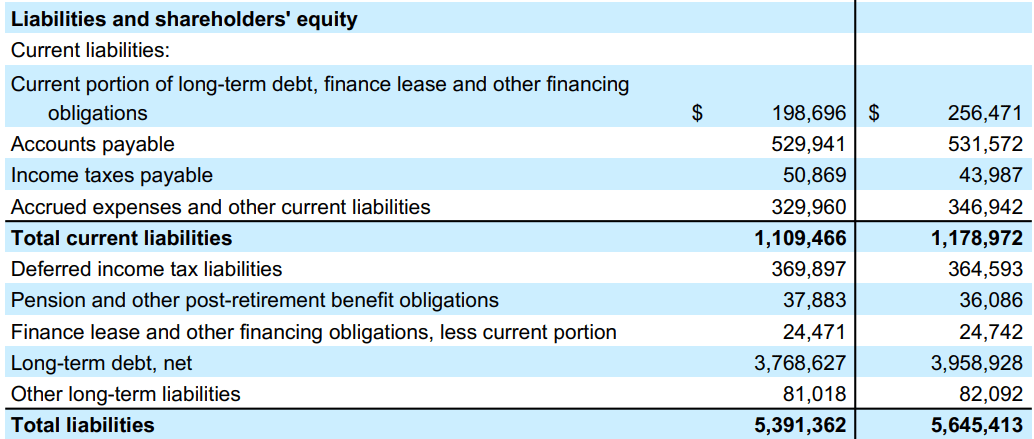

I believe that the total amount of debt is not small. However, if FCF expectations are finally true, I believe that Sensata will likely reduce its debt, and shareholders will likely receive excess cash. Current portion of long-term debt, finance lease, and other financing obligations stand at $198 million, with accounts payable of $529 million, income taxes payable close to $50 million, and accrued expenses and other current liabilities of $329 million.

Also, with pension and other post-retirement benefit obligations close to $37 million, finance lease and other financing obligations of $24 million, and long-term debt close to $3.768 billion, total liabilities are equal to $5.391 billion.

Source: Quarterly Earnings Release

{kind=link}

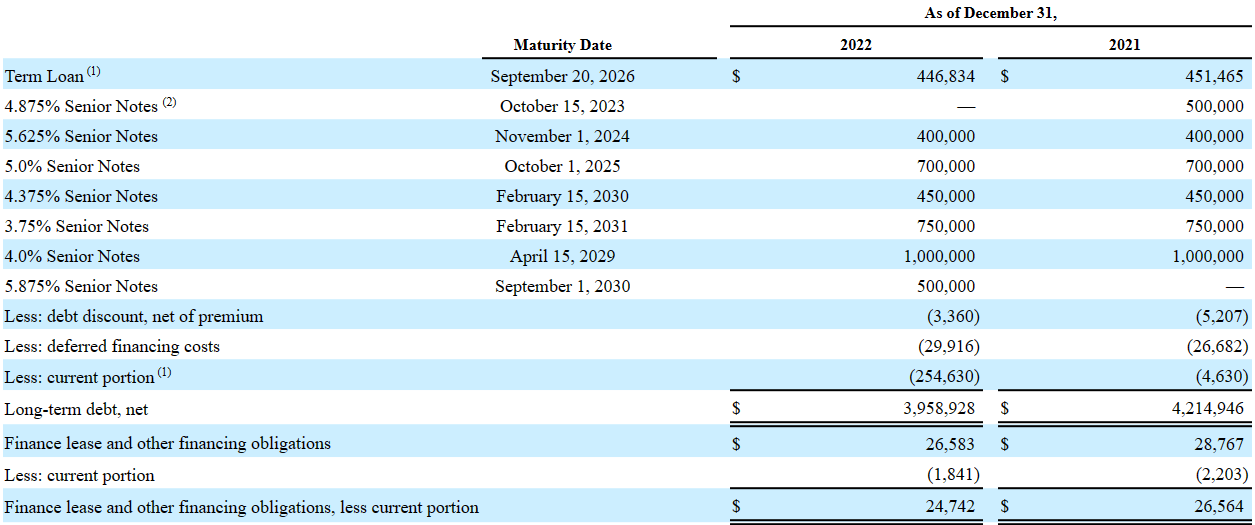

In this case, it is worth noting that most debt agreements mature from 2024 to 2029. In my view, in the next six years, Sensata will most likely be able to negotiate with other debt holders.

{kind=link}

My Assumptions And DCF Valuation

Under my DCF model, I expect that Sensata will successfully leverage material growth drivers to deliver innovative products that create valuable business insights for its customers and end users. In my view, further improvements and expansion of the market share in electrified platforms and implementing IoT solutions in vehicle fleets will improve revenue expectations. Under the previous conditions, I included in my DCF model CFO, FCF, and net income growth according to the IoT market growth, which is expected to be close to 26.1% from 2022 to 2030. It is also worth noting that the IoT sensor market size is expected to grow at a CAGR of close to 28% from 2021 to 2030.

The global Internet of Things market size was valued at USD 544.38 billion in 2022 and is projected to grow from USD 662.21 billion in 2023 to USD 3,352.97 billion by 2030, exhibiting a CAGR of 26.1% during the forecast period. Source: Internet of Things [IoT] Market Size, Share & Growth by 2030

The global Internet of Things sensors market size was USD 15.78 Billion in 2021 and is expected to register a revenue CAGR of 28.3% during the forecast period. Source: Internet of Things [IoT] Market Size, Share & Growth by 2030

I also assumed that improving efficiency and productivity will bring better cash flow statements and FCF margins. In this regard, I assumed that Sensata will successfully expand its business, and accelerate market share in areas that will experience high growth in the future. It is focusing on offering highly customized products at relatively low cost and staying ahead of emerging technology trends.

Besides, I also assumed that Sensata will likely receive more demand as new innovations are brought to the market. I believe that certain products will most likely receive more attention than expected, which will likely bring unexpected sales growth. In particular, I am quite optimistic about expected growth in the operations of light- through heavy-duty vehicles. In this regard, the company commented the following in the last annual report.

Business is significantly transforming the industries in which we operate and are creating greater secular demand for our current and new innovative products, resulting in growth that exceeds end market production growth in many of the markets we serve, a defining characteristic of our company. Source: 10-k

This is driven by the need for smarter and more connected sensors and equipment that collect, analyze, and provide insights into the operations of light- through heavy-duty vehicles to improve its operations, making it more productive and efficient. Within IoT, our principal area of focus is the Sensata INSIGHTS business, in which we deliver data insights across heavy, medium, and light vehicle fleets. Source: 10-k

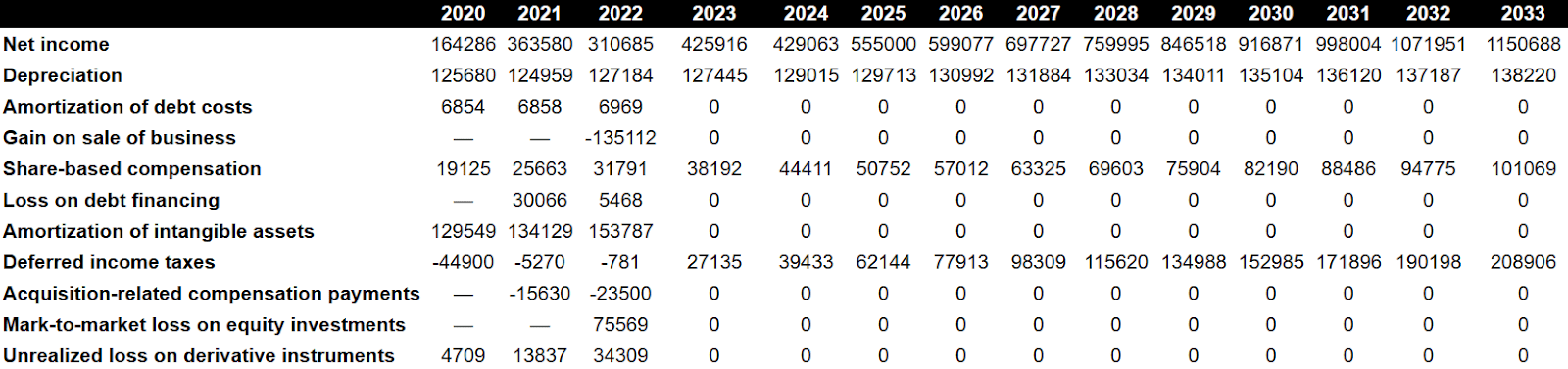

My financial forecasts include 2033 net income of $1.150 billion, depreciation of $138 million, deferred income taxes of $208 million, changes in accounts receivable of -$370 million, inventories of -$259.5 million, and changes in prepaid expenses and other current assets close to -$143.5 million. I believe that my figures are pretty much aligned with changes in accounts payables, changes in inventories, and working capital growth seen in the past. In my view, my financial forecasts are conservative.

{kind=link}

Besides, with changes in accounts payable of -$42.5 million and income taxes payable close to $187.5 million, 2033 CFO would stand at $974.5 million. If we also include capex of -$139 million, 2033 FCF would stand at $835 million.

Source: My DCF Model Source: My DCF Model

{kind=link}

{kind=link}

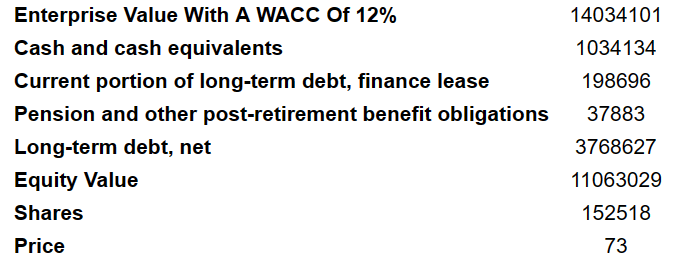

If we assume an EV/FCF of 50x, the terminal FCF would be close to $41.85 billion. Besides, with a WACC of 12.5%, I obtained an enterprise value of $14.034 billion. Adding cash and cash equivalents of $1.034 billion, current portion of long-term debt, finance lease of $198 million, pension and other post-retirement benefit obligations of $37 million, and long-term debt of $3.7685 billion, the equity value would be $11.0635 billion. Finally, the fair price would be $73 per share.

Source: My DCF Model Source: My DCF Model

{kind=link}

{kind=link}

A Lot Of Small Competitors As Well As Large Players And Many Risks

The company competes with several independent vendors. The most important competitive factors are product performance, quality, service, reliability, manufacturing footprint, and business competitiveness. In my view, the company stands out for its ability to design and produce custom solutions globally, breadth and scale of product offerings, technical expertise and development capabilities, customer service and responsiveness, and commercially competitive offering.

In the Sensing Solutions category, the company competes with divisions of large multinational industrial corporations and smaller companies competing in specific markets, with the key competitive factors being product performance, quality, and reliability.

I believe that the largest risks would come from failed acceptance of new products and innovations. If managers from the EV and aerospace industry or industrial players fail to understand why the products would improve their efficiency, future revenue growth would likely decline. As a result, I believe that investors would most likely dump their shares.

Besides, I believe that lack of components and raw materials or increase in their costs could bring significant decrease in the FCF margins. As a result, I believe that the expectations of investors would decline, which may lead to declines in the share price.

I would also pay special attention to data privacy. New laws in Europe or the United States could question whether the company needs authorizations from employees and independent drivers to deal with their information. If Sensata has to invest more money in capital expenditures or lawyers in the near future, I believe that net income growth expectations would most likely decrease.

Recognition of goodwill or impairment of intangible assets in this case is quite important because Sensata reports a lot of intangible assets. Impairment of goodwill could bring declines to book value per share.

Finally, with respect to the total amount of debt, I believe that growing debt amounts may bring certain fears to equity investors. If they feel that the company received too much financial debt, the demand for the stock could decline, which may lead to lower stock prices.

My Conclusion

Sensata Technologies is a company with a solid growth and diversification strategy, focused on offering innovative and personalized solutions to its clients in multiple industries. Despite current risks, challenges, and economic instability, Sensata has a clear focus on expanding its presence in growing markets and staying ahead of technology trends. In addition, in my view, its ability to design and produce custom solutions and its technical expertise provide it a competitive advantage. Overall, the company appears to be in a strong position to continue to generate revenue and maintain its position in the industry for the long term. I do believe that the company could be worth $73 per share.

For further details see:

Sensata Technologies: IoT Sensor Market Growth And M&A Imply $73 Price Target