ST - Sensata Technologies: Robust FCF Attractive Valuation Ahead Of Q2 Earnings

2023-07-10 13:15:06 ET

Summary

- US vehicle sales increased by over 20% month-on-month in June, which is positive for auto equipment producers such as Sensata Technologies.

- ST is a leading manufacturer of sensors and controls, with potential growth in its Automotive segment due to the rise of electrification and AV technology.

- Despite a lukewarm chart, ST's low valuation, solid free cash flow, and robust auto sales make it a promising buy, with the potential for an earnings beat in the near future.

- I highlight important price levels on the chart to watch ahead of Q2 earnings on the 25th.

There was good news in the Industrials sector earlier this month. According to Wards, total US vehicle sales, on a seasonally adjusted annual basis, ticked higher from May levels, up better than 20% month-on-month. That is good news for firms exposed to the production of auto equipment, including Sensata Technologies ( ST ).

While just a part of the company's overall operations, I assert that the firm may produce solid earnings results later this month. I have a buy rating on ST for its low valuation and solid free cash flow, though the chart is just lukewarm.

Auto Sales Rise In June

Goldman Sachs

According to Bank of America Global Research, ST is a specialized manufacturer of customized sensors and controls. ST manufactures products for specific customer applications and systems such as air conditioning, braking, exhaust, fuel oil, tire, operator controls, and transmission in automotive and heavy vehicle and off-road systems, as well as industrial applications, including aircraft, refrigeration, material handling, telecommunications, and heating, ventilation, and air conditioning systems.

The Massachusetts-based $6.8 billion market cap Electrical Components and Equipment industry company within the Industrials sector trades at a moderate 18.4 trailing 12-month GAAP price-to-earnings ratio and pays a low 1.0% dividend yield, according to Seeking Alpha. Ahead of earnings later this month, implied volatility is not all that high at 29% while its short interest percentage is low at 1.4%.

Back in April, Sensata beat earnings estimates but also guided its Q2 lower. Shares fell in response but found support on the chart in the days after the release. Digging into the profit picture, Q1 operating EPS came in at $0.92, topping the consensus by a nickel on $998 million of quarterly revenue, up just 2.3% on a year-on-year basis. ST produced much better cash flow in Q1 2023 compared to the same quarter last year and free cash flow summed to $60 million compared to just $11.6 million in Q1 2022. The management team's Q2 outlook was what drove the stock down. Adjusted EPS was seen in the $0.88 to $0.98 range versus consensus of $0.95.

But the company is an established leader, at least in the US, for the manufacture of sensors and controls, with exposure to the Internet of Things. I like its growth potential from its Automotive segment as electrification and AV technology continue to gain traction. Moreover, with recently reported robust auto sales, I think earlier guidance was too conservative, so an earnings beat may be on the horizon. Of course, macroeconomic conditions are a key risk in the second half as well as any possible litigations regarding emissions.

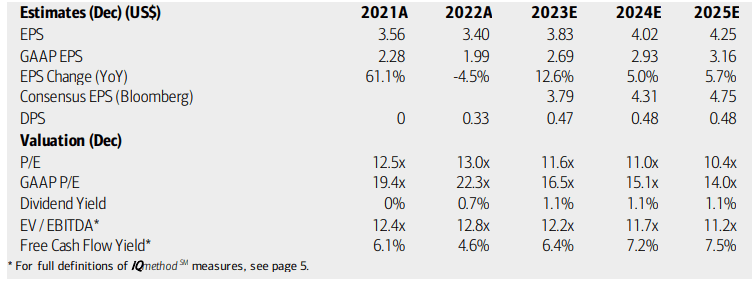

On valuation , analysts at BofA see earnings rising at a solid pace this year before per-share growth eases to the 5% to 6% range in the out year and in 2025. The Bloomberg consensus outlook is more sanguine on EPS estimates in 2024 and 2025. With a low-teens operating P/E and a below-market EV/EBITDA ratio, shares appear to be a solid value. And while dividends are not expected to grow quickly over the coming quarters, Sensata's free cash flow yield is impressive at 7% and overall profitability is robust.

Sensata: Earnings, Valuation, Dividend, Free Cash Flow Forecasts

{kind=link}

ST currently trades at a significant 23% discount to its long-term forward operating earnings multiple. 11.6 is also 32% cheaper compared to its sector median. If we assume a normalized EPS figure of $4 over the coming four quarters and use a moderate 15 P/E, then the stock should be near $60. Given its market positioning and solid free cash flow, I assert a higher valuation is warranted.

ST: Mixed Valuation Metrics, But Attractive Earnings Multiples

Seeking Alpha

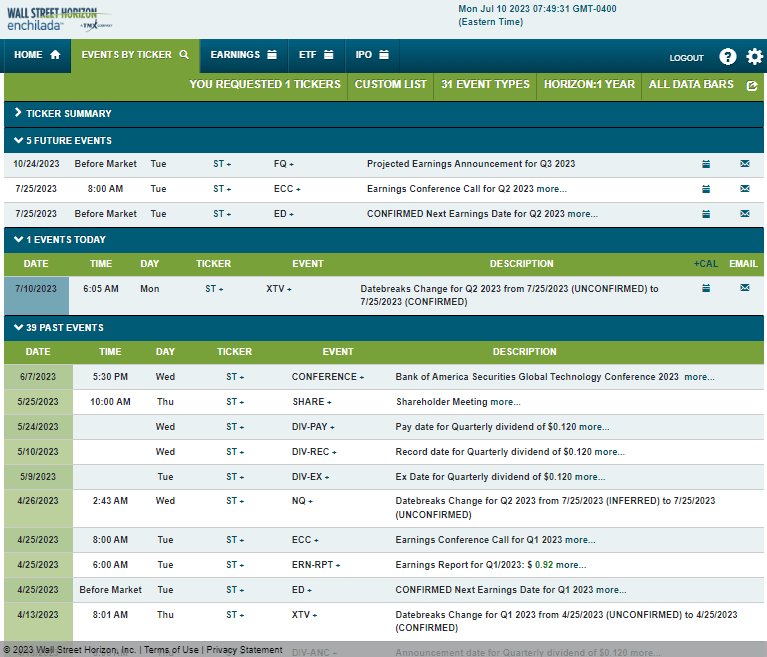

Looking ahead, corporate event data provided by Wall Street Horizon show a confirmed Q2 2023 earnings date of Tuesday, July 25 BMO with a conference call immediately after the results hit the tape. You can listen live here . No other volatility catalysts appear on the event calendar.

Corporate Event Risk Calendar

{kind=link}

The Technical Take

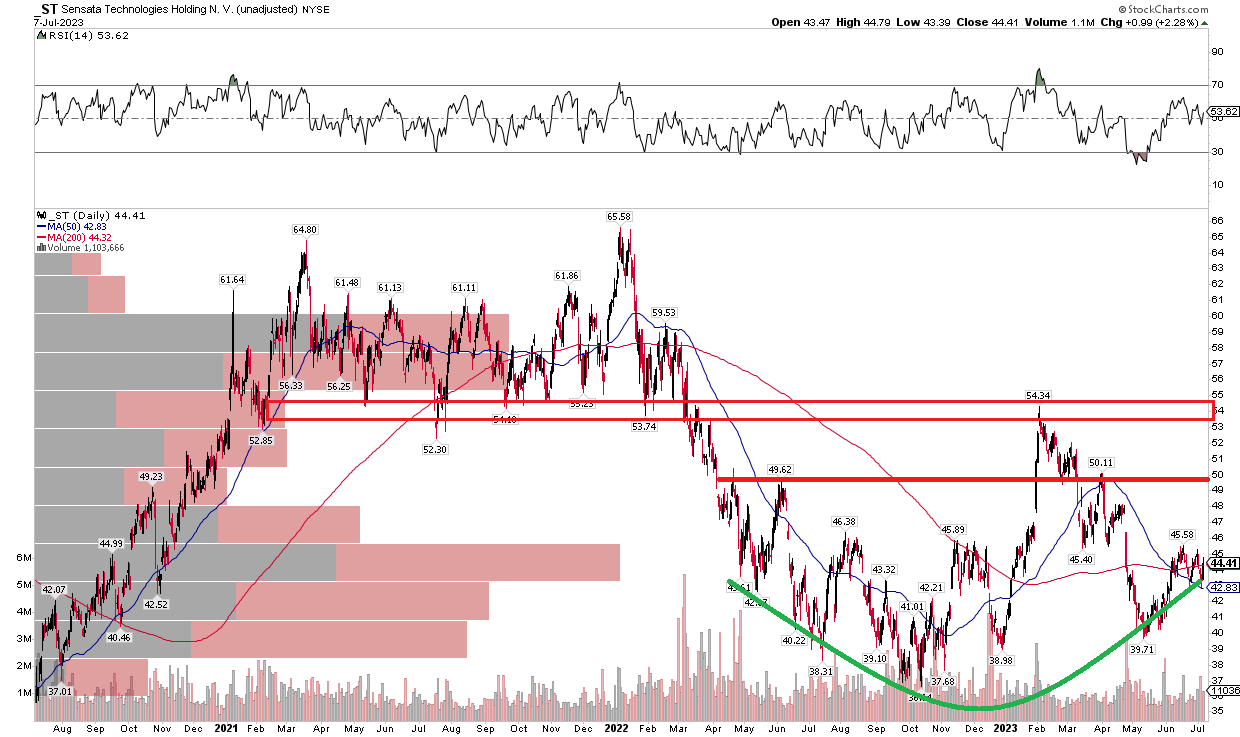

With shares undervalued in my view, the chart situation is not quite as optimistic, but there are some reasons for the bulls to hope. Notice in the graph below that shares are putting in a bearish to bullish rounded bottom pattern. This reversal signature is a bit messy, however. I see several layers of resistance.

First, the $45 to $47 zone is where the stock peaked in August and November last year, and there is a modest gap from late April that may be problematic. Next, the June 2022 and April 2023 high near $50 was met with selling pressure. Finally, the old range lows from its 2021 trading area rejected a rally try back in Q1. Support, though, is apparent near $39. With a flat 200-day moving average, the long-term trend is neutral and there is ample volume by price in the $38 to $45 area.

Overall, there are higher lows off the October 2022 bottom, but it is not a convincingly bullish view.

ST: Bullish Rounded Bottom, But Several Resistance Layers

{kind=link}

The Bottom Line

ST's valuation makes it a buy while the technical scream hold. Overall, I will weigh the fundamentals and valuation higher, making Sensata a buy.

For further details see:

Sensata Technologies: Robust FCF, Attractive Valuation Ahead Of Q2 Earnings