SRTS - Sensus Healthcare: I'm Skeptical Of Management's Optimism Ahead Of Q2 Earnings

2023-07-31 01:41:02 ET

Summary

- Sensus Healthcare's stock has been highly sensitive to its earnings reports, with consistent sell-offs following each less-than-stellar quarterly earnings release.

- Sensus has recently shifted into negative operational cash flow, and its lack of recurring revenue suggests a lack of a sustainable strategy for preserving or generating cash.

- Management's optimism raises investor expectations, but without clear evidence of a successful turnaround strategy, it puts additional pressure on the company to perform.

Introduction

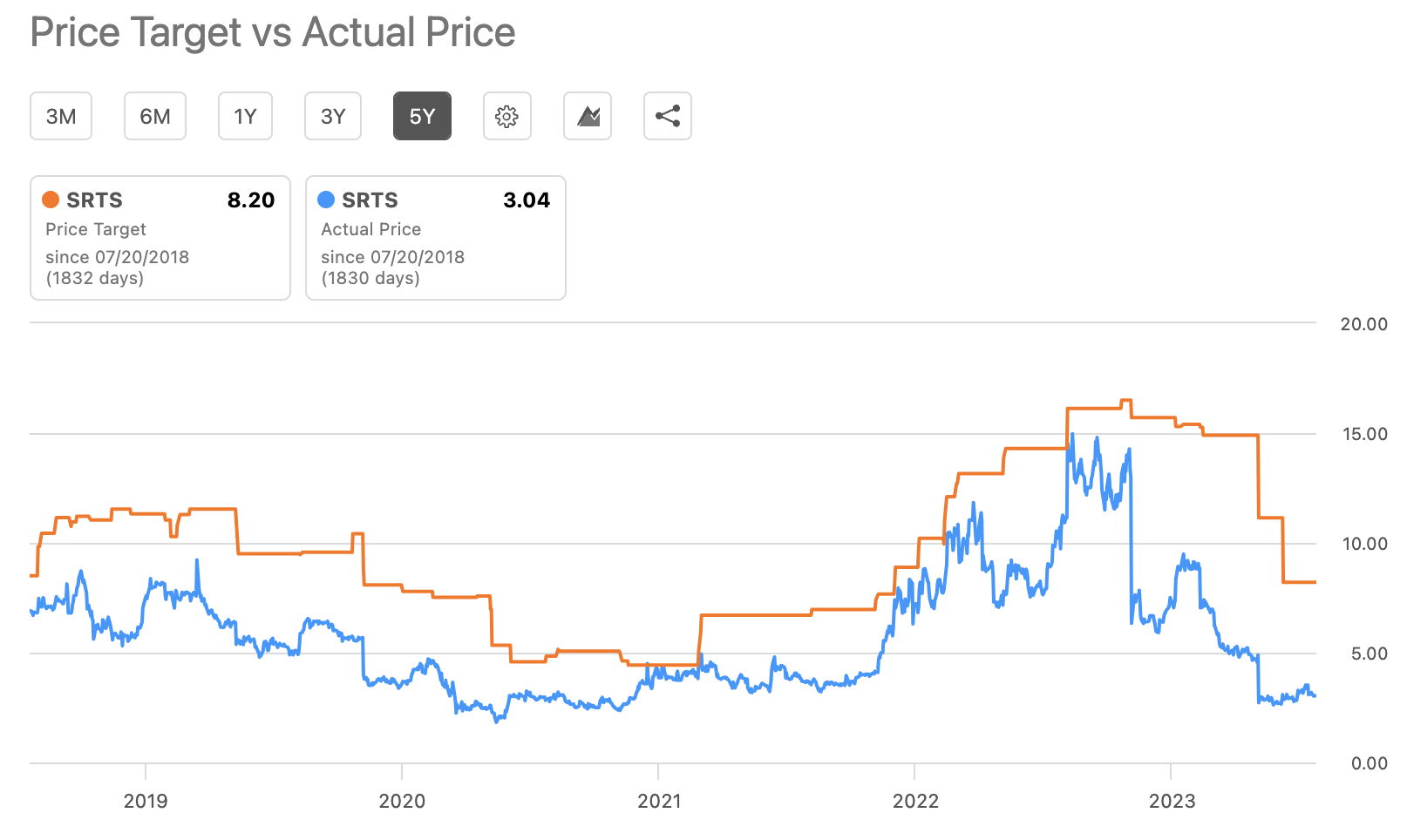

Sensus Healthcare ( SRTS ) has faced significant challenges in the past, from temporary disruptions to low market sentiment in the face of strong performance and stability. In the past few months, despite being consistently awarded Buy ratings from both Seeking Alpha and Wall Street analysts, the stock continues to plummet. The stock has plummeted over 60% while the medical instruments industry increased by 12%. The stock dropped by 44% on May 3rd alone following the release of the company's Q1 earnings report. This parallels several other 1 day drops in the company's history, primarily driven by past quarterly earnings that failed to meet expectations. Investors sold at much higher volume following the Q3 earnings than the selloff following the Q1 earnings. Notably, investors did not sell off following robust Q4 earnings. If we take a look at the price target vs actual price graph, it is evident that the company historically underperforms its price target and is consistently overvalued by analysts. This may be the primary cause for the stock's downward trajectory and its consistent selloffs at the release of earning reports. As of July 30, 2023, the stock is trading at $2.89 per share with a market cap of over $47 million. While the stock is very cheap right now, I am not sure this signals a buying opportunity.

{kind=link}

Sensus' stock is very sensitive to press releases as investors have sold at large amounts following less than stellar earnings reports. The selling pressure has been remarkably high, and without management addressing these concerns, shareholders are left feeling increasingly stressed and uncertain about the potential high volumes of selling persisting into the future. Meanwhile, Joseph Sardano has repeatedly stressed the importance of not going into debt nor issuing new capital that would dilute existing shareholders. Given these aspirations, the company has effectively maintained a robust balance sheet with very low debt levels and a consistently favorable working capital ratio over the recent quarters. In the past few months, the company's stock price declines may not have been justified given the strong performance in these areas, Sensus has not been performing the best on the operational front.

Financial Performance

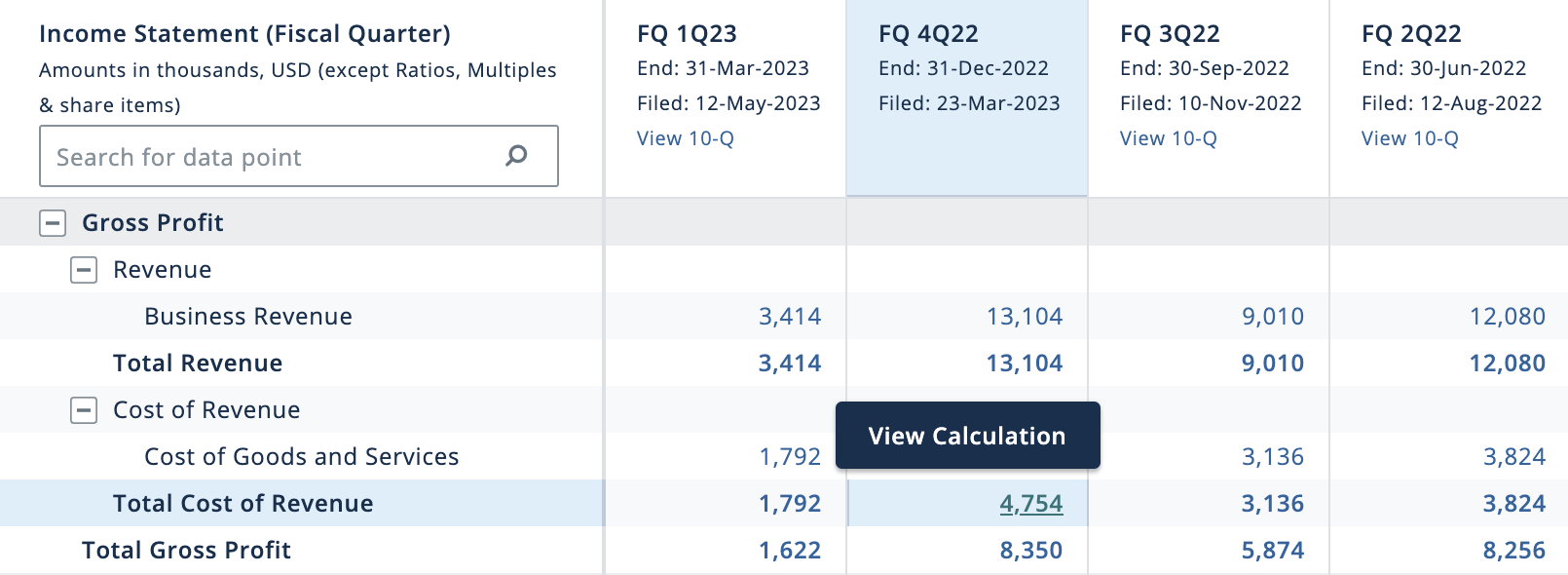

Sensus experienced its largest drop in revenue in the company's history in Q1 2023. The company reported revenue of $3.4 million, which is down 74% from the previous quarter's $13.1 million. Total profit experienced a slightly worse hit, at $1.6 million in Q1, down 80% from the previous quarter's $8.3 million. Joseph Sardano, the CEO and Chairman, attributes this disappointing performance to high inflation , which delayed many of its customers from purchasing SRT equipment in Q1. In the 2023 Earnings Conference Call , Sardano stated that "inflation has caused consumers to pull back on these expenditures, either having these procedures done less frequently or foregoing them altogether." I sense that this is a very broad statement that is used to cover up underlying factors in the company's business model that caused it to have such sporadic jumps in its revenue in the past few quarters. Inflation hit its peak of 9.1% in June 2022, and from the beginning of January to end of March 2023, inflation slowed substantially from 6.4% to 4%. Considering that inflation was much higher a year earlier, it would make the most sense for the company to experience a drop in revenue a year ago and not necessarily in Q1 2023. Despite its sharp drop in revenue in Q1 2023, the company's revenue has grown significantly throughout the years, increasing from $27 million in 2021 to $44 million in 2022. The company's profit margin also grew from 15.2% to 54.4% in the same time frame, which is notable.

{kind=link}

A Cash Burning Operation

What's most concerning is the fact that the company has been operating cash flow negative for the past 2 quarters, losing $10 million in Q4 and $6 million in Q1. Cash and cash equivalents have been steadily decreasing throughout the past 3 quarters. If Sensus continues to operate cash flow negative, it risks depleting the company's cash reserves. This could ultimately force the company to incur debt, a situation which starkly contrasts with the CEO's goal of operating debt free without diluting shareholders. While the company is currently holding ample cash, this was substantially reimbursed by the $15 million sale of its Sculptura assets to Empyrean Medical Systems in March 2022. This will give the company breathing room to have a few more cash burns in future quarters. Regardless, the company's biggest challenge is its recent dip into negative operational cash flow, following several quarters of positive operational cash flow. Sensus seems to lack a sustainable strategy for preserving or generating cash, as seen by their cash reserves falling sharply from $37 million to $19 million within just two quarters. This can be attributed to the company's rather unpredictable revenue model provided that it relies on the sale of its capital equipment, with less emphasis on generating recurring revenue. While the company earns the majority of its revenue from the sale of its SRT devices, they do employ a service contract of 10% of each machine's selling price that is paid out annually. Despite this, this revenue model with little recurring revenue is enough to deter investors or at least make shareholders skeptical of its long term consistent growth potential.

Valuation

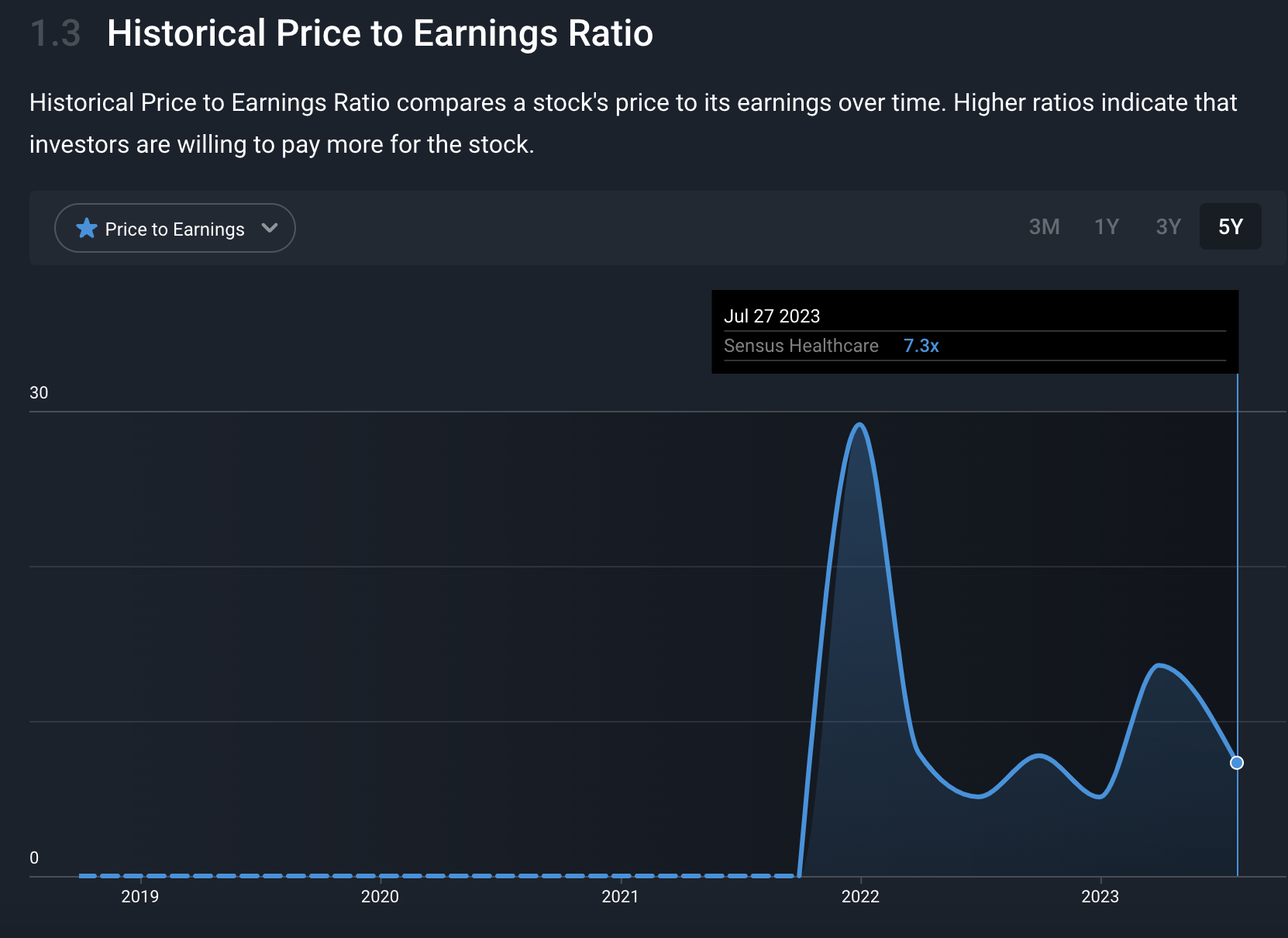

Seeking Alpha assigns Sensus a valuation grade of A+. Sensus has a solid P/E ratio of 7.57x, compared to the US market average of 23.46x. Sensus' P/E ratio is especially favorable given that the US medical equipment industry's ratio is 86x, suggesting that the company is not only undervalued compared to the broader market, but especially so to its industry competitors. While I would have anticipated its P/E ratio to be slightly higher, especially after its disappointing revenue performance in Q1, its ratio actually dropped 46% from 13.6x to 7.3x from the beginning of Q2 to now. Moreover, every other multiple, including EV/Sales, EV/EBITDA, P/S, and P/B, are all significantly below the sector median. Below is a graph of Sensus' P/E ratio throughout the past 5 years. However, it's disconcerting that Sensus has maintained a significantly lower P/E ratio since mid-2022, while its stock price has plummeted over 80% from its peak in August 2022.

{kind=link}

Growth Initiatives

Sensus has recently partnered with MIS Healthcare to expand its addressable markets. The company announced in early July that they had planned to distribute its SRT devices to the United Kingdom and Ireland. A few days ago, the company completed its first SRT system installatio n in a hospital in Ireland. This occurred just 3 weeks following the announcement of the partnership with MIS Healthcare, and it seems that the company truly is acting on its plan to expand in to the UK and Ireland. Sensus has already seen progress in its initiative to expand into new Asian territories in the first quarter, having shipped a total of 3 SRT systems to Asia, 2 in China and 1 in Taiwan. Echoing its expansion aspirations in Europe, the company holds high hopes of selling over 10 SRT systems throughout 2023. Overall, Sardano expects to ship over 60 SRT systems throughout 2023. In its first quarter conference call , Sardano expressed that the main limitation the company faces is "convincing [patients that] SRT is still a very, very good investment." They must prove that the company's SRT technology outperforms existing solutions, especially considering that patients are already reimbursed by US healthcare entities like CMS, Medicare, and Medicaid. There is still the concern that dermatologists have not fully realized the potential benefits of SRT systems, and to increase visibility and credibility, the company has been focusing extensively on marketing and educational initiatives. They've increased their presence at key conferences as well as smaller regional conferences. The company spent over $2 million on marketing expenses, compared to $1.2 million in Q1 2022. While I am not taking management's words at face value, there is still the possibility that these initiatives prove effective in the long run. If the company beats expectations in Q2, I would hope that the company provides clear guidance on what exactly is catalyzing this growth. If more SRT systems are sold in Ireland and the UK within Q1, then this is a great sign of a potentially untapped market that Sensus can capitalize on, and I would recommend shareholders to hold onto their positions. Moreover, it is important to note that Sensus is an illiquid micro-cap, with a low trading volume of 45,415, that may make exiting a position difficult. Ultimately, the company's best bet is to focus on international markets.

If management is so confident in the company's ability to turnaround in Q2 and throughout 2023, then a stock buyback would be beneficial in instilling confidence in the company's future performance. The last time the company repurchased stock was in March 2022, of $3 million. However, the stock has dropped nearly 75% since, and a stock repurchase sometime in 2023 will likely be necessary to prevent another unjustified selloff. Despite this, Sardano has also made it known that he is looking towards M&A opportunities to potentially act as an outsourced sales force, similar to their current partnership with MIS Healthcare and SkinCure Oncology.

Bottom Line

If the poor performance in Q1 is really due to inflationary concerns as Sardano attributes it to, then revenue should experience a dramatic rebound as inflation has slowed significantly recently and will continue to slow. This should not be a major headwind, and I do not think this is a valid reason for the company to solely base their top-line performance off of. While Sardano and the management team have expressed optimism in its latest conference call, this will only further bolster shareholders expectations, putting more pressure on the company to follow through. Moreover, the little amount progress from the TDI and Silk projects does not help its case. Analysts and management have put a significant amount of pressure on the company to perform, and if future earnings reports consistently fall short of these projections, it's likely that selloffs will continue. Even when the company experienced a strong rebound in Q4 following a sluggish Q3, the stock remained stagnant. It seems that the company has to demonstrate substantial growth quarter by quarter to see any upward movement in the stock price. Yet, a slight miss on its quarter earnings will crash the stock.

As mentioned earlier, Sensus is adamant in rejecting the possibility of going into debt or issue issuing new shares, but a stock buyback is what the company needs right now. Unfortunately, we heard no sign of this in its Q1 conference call. Especially in a market where investors favor companies with growth through recurring revenue, constant stream of press releases, with little hiccups in top line growth, guidance from management on the shareholder front is even more pressing. I'm afraid the company's Q1 earnings took a hit on the company that will be difficult to restore investor sentiment. Ultimately, there is no doubt that Sensus is a profitable, undervalued, and financially healthy company. However, with its unprecedented volatility, I recommend investors to not hold onto their shares. I am eagerly anticipating the company's Q2 results and earnings report due on August 3rd. Given notably lower revenue projections for Q2, I cannot say with certainty that the company will surpass or fall short of these estimates. Nevertheless, I am anticipating that this will not be favorable among shareholders, many of whom are expecting a full rebound, similar to the recovery from Q3 to Q4.

{kind=link}

For further details see:

Sensus Healthcare: I'm Skeptical Of Management's Optimism Ahead Of Q2 Earnings