SHY - September Labor Report Preview: Full Employment To Infinity

2023-10-03 13:00:36 ET

Summary

- The Fed projects full employment "to infinity" with unemployment rates of 3.8% for 2023 and 4.1% for 2024 and 2025, and 4% for 2026 and beyond.

- The U.S. is facing a major labor shortage due to aging demographics and deglobalization trends, expected to keep interest rates "higher-for-longer."

- Most new jobs created have been created in the non-cyclical health sector, which does indicate the strength of the economy, rather supporting the demographic trend.

- The healthcare sector could be a potential defensive buy, but the valuation is still too high.

Infinity is the concept of something that has no limit or end.

The labor shortage

The most important information that came from the September FOMC meeting is the projection for the unemployment rate in the Summary of Economic Projections.

The Fed essentially projects full employment in the foreseeable future with the unemployment rate 3.8% for 2023 and 4.1% for 2024 and 2025, and 4.0% for 2026 and longer term. This is essentially full employment to infinity - no end or limit.

September FOMC

Note, the Fed projected earlier in 2023 that the unemployment rate would increase to 4.5% by the end of 2023 due to the effects of the monetary policy tightening. In fact, the Fed Chair Powell specifically warned that there has to be some "pain" in the labor market to ease the inflationary pressures.

So, this is a major turn in the Fed's projections, that possibly fell under the radar. But it is the most important revelation from the recent FOMC meeting.

So, why is the Fed expecting the unemployment rate to stay at 4% level - despite the sharp monetary policy tightening, and the expectations to keep interest rates "higher for longer". The explanation is: the U.S. is facing a major labor shortage over the foreseeable future.

Specifically, there are two major trends that will likely keep the U.S. labor market tight. First, it's the demographics. The aging population and the coming wave of retirements is reducing the labor force. Second, the unfolding trend on deglobalization is causing an increase in the labor demand and as some jobs are on-shored, and also due to stricter immigration laws which are likely reduce the inflow of legal immigrants.

Thus, due to the demand and supply pressures, the U.S. labor shortage is likely to persist, and that's what the Fed is acknowledging. But, that's not good news for the financial markets, as the wage growth is likely to keep the service inflation elevated, and thus require higher interest rates, and specifically real interest rates.

Job openings

The U.S. Bureau of Labor Statistics just released the JOLTS data for the month of September, which was a highly anticipated number due to the fact that the August JOLTS data showed a large drop in job openings.

Note, the soft-landing narrative is based on the prediction that the job openings would sharply drop without causing an increase in the unemployment rate - thus without a recession. Thus, the Fed would be able to cut the interest rates, which would be positive for the stock market.

However, the JOLTS data for September showed a sharp increase in the job openings, to nearly 10M. This shows that the labor market is, in fact, still very tight - it provides the support for the labor shortage thesis.

{kind=link}

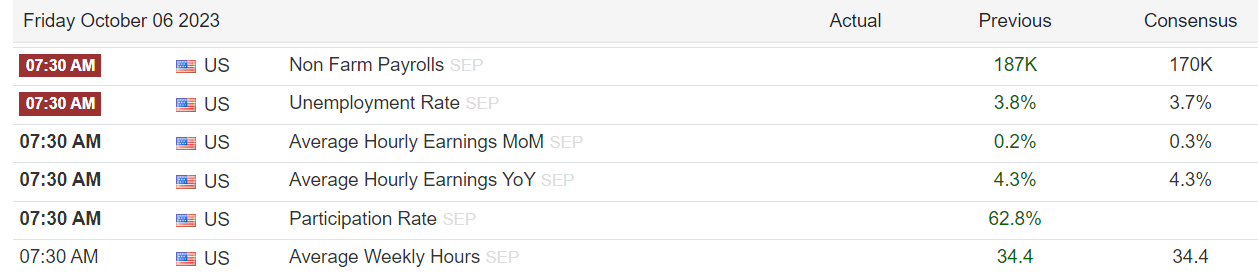

The September payroll report

The U.S. Bureau of Labor Statistics will release the labor report for September on Friday. These are the consensus expectations:

{kind=link}

The market expects that the non-farm payrolls would continue to slow, adding 170K new jobs in September, down from 187K in August.

The unemployment rate increased to 3.8% in September, but mostly due to the increase in the labor force - more people looking for jobs. This trend, if continues, would be positive, as higher supply of workers reduces the labor shortage. However, the market expects that the unemployment rate will drop to 3.7% in September.

Note the Fed sees unemployment at 3.8% in 2023, so any significant deviation to either well below 3.7% or above 3.9% would be market moving news, again depending on the labor force growth. A higher labor supply is good - so this puts the spotlight on the labor participation rate, it should increase from 62.8%.

On the inflation front, the market expects an uptick in the monthly wage growth from 0.2% to 0.3%, and the wage growth to stay at 4.3%. This is still elevated, and the wage growth needs to fall to the 3.5-3.7% level to be consistent with the 2% inflation target.

Digging deeper - the effect of health sector

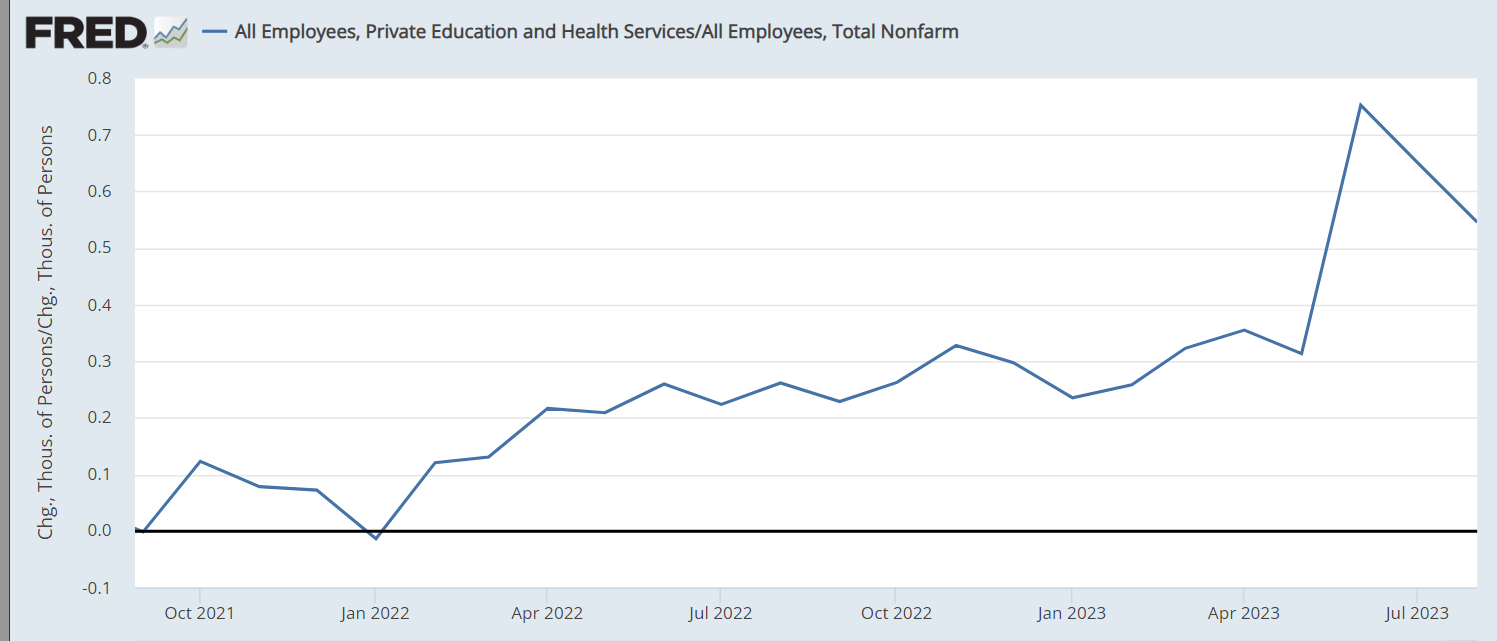

But when you dig deeper and analyze what's really keeping the labor market tight, you realize that it is mostly the health sector, which is non-cyclical, and thus it does not tell us much about the health of the economy.

Specifically, for the month of August, out of a total of 187K now jobs created, 102K came from the health and education sector, which is 55% of all new jobs created.

If you look at the same statistic over the last year, you notice that health and education sector provided about 20-30% new jobs created from April 2022 to April 2023. During the summer of 2023, we see a sharp spike - in June over 70% of new jobs came from health and education, and this number held over 50% since.

What does this mean? As job creation in cyclical sectors slows, the non-cyclical health and education sector continues to be strong. Why? Demographics. The ageing population requires more health services, and this is the trend likely to continue.

{kind=link}

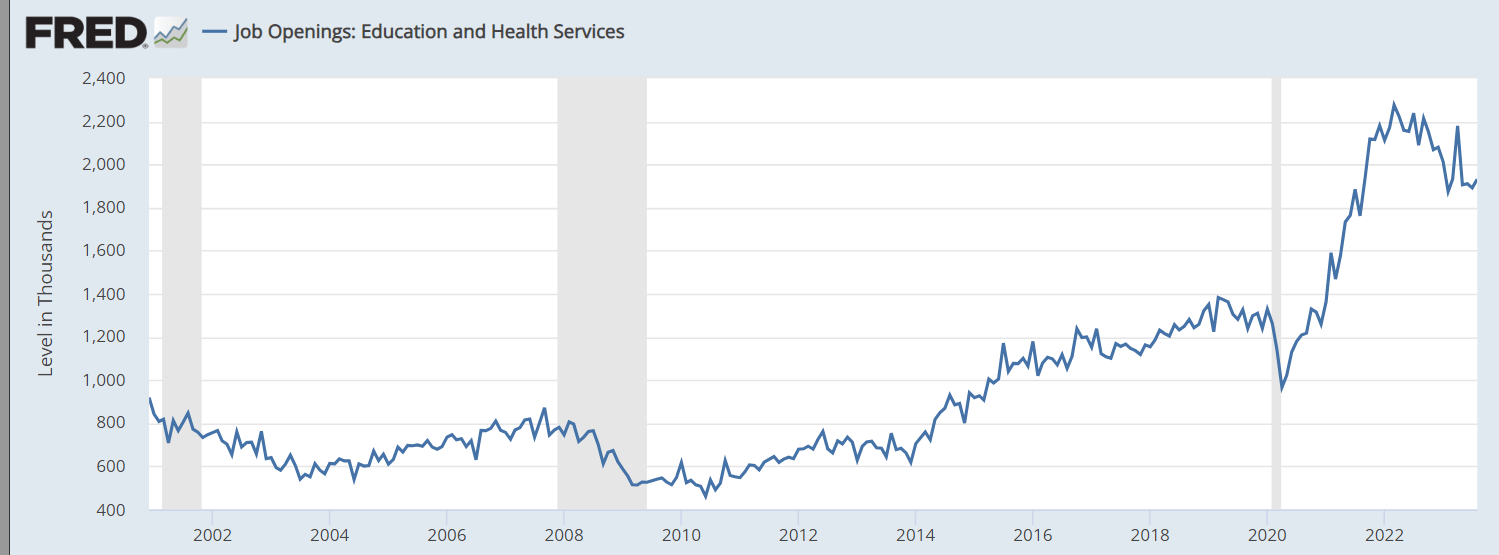

Also, when you look at the JOLTS data, you also see that there are almost 2M job openings in the health and education sector, which is well above pre-pandemic levels of about 1.2M - and 20% of all job openings. At the peak, there were around 2.2M job openings in the health and education sector, so there is some easing in demand, but not sufficiently enough.

{kind=link}

Implications

The Fed acknowledges that there is a persistent labor shortage in the U.S., which will likely require the interest rates to be "higher for longer." However, it appears that the labor shortage is concentrated in the non-cyclical sector, health and education. A potential recession is not going to reduce the need for health services of the ageing population. Thus, the labor report can be misleading in gauging the health of the cyclical economy.

The September labor market report is likely to continue to show steady but slowing job creation, but if the new jobs created are mostly from the non-cyclical health and education sector, that's not necessarily good news for the economy and the stock market ( SPY ).

The JOLTS report likely cements the Fed hike in November or December, and the futures markets are now pricing about 50% of the additional hike in December. This is also not good news for the stock market - the coming 5.66% interest rate on short-term cash ( SHY ) will be too attractive to ignore.

Is the healthcare sector ((XLV)) a buy?

The more specific question, based on this report, is whether the Healthcare Sector represented by Health Care Select Sector SPDR® Fund ETF (XLV) is a buy at this point. The demand for health services is high - that's based on the job openings in the health sector - almost 2M job openings. The demand for health services will continue to be high due to demographics.

The healthcare sector is considered a defensive sector - that's what you buy before a recession. However, at this point I see the healthcare sector still a bit overvalued, with the 2023 P/E ratio of 18.3. Analysts expect the 2024 earnings to grow at 13% for 2024. The dividend yield of 1.65% is also not that attractive, especially given the short-term interest rates.

Given the business cycle investing strategy (buy defensive sectors before a recession), I view XLV as a potential buy, but not yet, the valuation is still too high, so I'm neutral for now.

Tactically, XLV is in a range, possible breakout could be a buy point, but I suspect that breakdown sub 120 is more likely as the P/E multiple contracts, at which point I will reevaluate the buy.

For further details see:

September Labor Report Preview: Full Employment To Infinity