ACXP - Seres Therapeutics: Still Work To Do Before Realizing Its Potential

2023-05-22 14:49:12 ET

Summary

- SER-109 (Vowst) was recently approved by FDA and will be launched in June with the Nestle commercial team.

- Most of the pipeline has failed in clinical trials.

- There is one active, albeit early stage clinical program, SER -155.

- The company burned an astounding $70 m in cash last quarter and had a net loss of $250.2 million for the full year of 2022. The company recently took on $250 m in debt.

- Investors should focus on the big picture and the company's line of sight to profitability.

Summary

Recently, investors have seen the share price of Seres Therapeutics ( MCRB ) fall after an FDA approval. While I rated Seres a buy in an article in 2020 before the phase 3 SER-109 readout, my enthusiasm for the company has diminished. The buy recommendation was based on a logical explanation for why 109 could succeed and more broadly on the enormous potential of the pipeline which had multiple shots on goal and a strong scientific rationale. The stock surged from $3 to $30 but that move likely reflected a positive view of not just SER-109, but of the company’s ability to replicate their success in other indications. Subsequently, those assets, including the most commercially important assets, have failed in the clinic. Currently the company has a commercial product with an excellent profile which they own 50% of, a high cash burn, $250m in recent debt and a pipeline with a single early stage asset being tested in the clinic. While the science and potential is exciting, the company is in the early stages of translating the science into transformational products.

SER-109 (VOWST)

Seres has successfully developed an oral microbiome therapy for the prevention of recurrent C. difficile infection ('CDI'). Vowst was recently approved by the FDA with a prescribing label which is broad allowing physicians discretion as to how many recurrences a patient must experience prior to use. Given the excellent safety and efficacy profile, physicians will likely be enthusiastic prescribers and happy to have an additional tool for challenging cases. Physician awareness of the product is likely high due to publication of phase 3 data in NEJ.

Seres’s management suggests there are approximately 156K recurrent CDI cases annually. Seres will share profits and losses with Nestle Health 50/50 and analysts suggest there may be a $1B market opportunity at peak.

Recent changes in guidelines recommend increased use of fidaxomicin rather than vancomycin, which may reduce the number of CDI recurrences. (Fidaxomicin has a higher sustained cure rate than vancomycin.) Thus, the actual number of cases (156k) should theoretically be lower. In addition, given the treatment guideline changes, insurers are more likely to cover fidaxomicin ($4000 per course).

Insurers may require pre-authorization and step therapy for Vowst due to pricing ($17.5K/treatment course) and attempt to reserve use for more refractory cases. The commercial team will need to work with payers to obtain reimbursement as well as communicate the process to physicians.

While Nestle (NSRGY) is a large and successful company, they are a consumer goods company and a food manufacturer primarily rather than a major US pharma company such as Bristol-Myers (BMY), Pfizer (PFE) or Merck (MRK). The marketing strategies used in the highly regulated, complex pharmaceutical space are unique. Major pharma companies have teams with extensive experience negotiating with payers and navigating the complex reimbursement and distribution process. While Nestlé is a terrific company, they may not be a partner who brings the extensive experience and infrastructure that a major pharma company would bring to the launch of a new class of drug.

Nestlé is taking a write down after purchasing Aimmune after sales of Palforzia were disappointing. Nestlé CEO Mark Schneider as quoted in Barron’s said they plan to sell their recently acquired Aimmune after difficulties commercializing the product. “It was much, much harder to get the patient takeup that we had anticipated, and that we felt was expected because of the strong underlying medical need.”

Analysts had projected peak Palforzia sales of $1B but clearly this was too optimistic. The drug appears to be more of a niche product and high pricing may have also hindered uptake. While it does appear Seres may have a product which may fare better commercially due to the profile, this example highlights the difficulties and uncertainties Nestlé faced when launching a prescription product.

While Palforzia may have had negative product features which impacted its uptake, Vowst’s oral administration appears to be a key product feature. Patients are likely to prefer oral administration over competitor Ferring (Rebiotix’s) Rebyota which requires rectal administration. But, longer term there may be other oral treatments similar to Vowst which offer meaningful competition.

Pfizer has invested in Vedanta which is advancing VE303 into phase 3 trials. In phase 2, VE303 showed comparable efficacy to SER-109 in preventing recurrent CDI. Vedanta has a manufacturing process which does not require donor stool and this may result in low costs. Prescribing of a microbiome therapeutic could potentially become more routine in CDI if pricing was more favorable for payers. Vedanta recently secured over $100 m in funding, and if trials are successful, an approved product could be on the market within 3 years. More broadly, this funding also suggests that others view the market opportunity in CDI to be significant enough to fund development of a similar therapeutic.

Longer term, Seres’s commercial efforts could be derailed if more effective antibiotics are developed. Vancomycin was developed in the 1950’s and fidaxomicin was approved in 2011. There has been little innovation in this indication. Currently, there are companies including Crestone (private) and Acurx ( ACXP ) which are running clinical trials and attempting to develop more effective antibiotics. Acurx’s phase 2a trial, “demonstrated 100 % clinical cure at end of treatment and 100% sustained clinical cure in patients with C. difficile Infection.” There were only 10 patients treated in this initial study but data from a larger phase 2b trial is anticipated to be released in 2023. Vowst is indicated to prevent recurrences, which may be quite uncommon if a highly effective antibiotic is eventually approved and widely available.

For now, Vowst has key advantages over existing products and meets a true unmet need but the treatment landscape can change dramatically. Seres has an opportunity to establish Vowst and secure market share before there may be new entrants to the market.

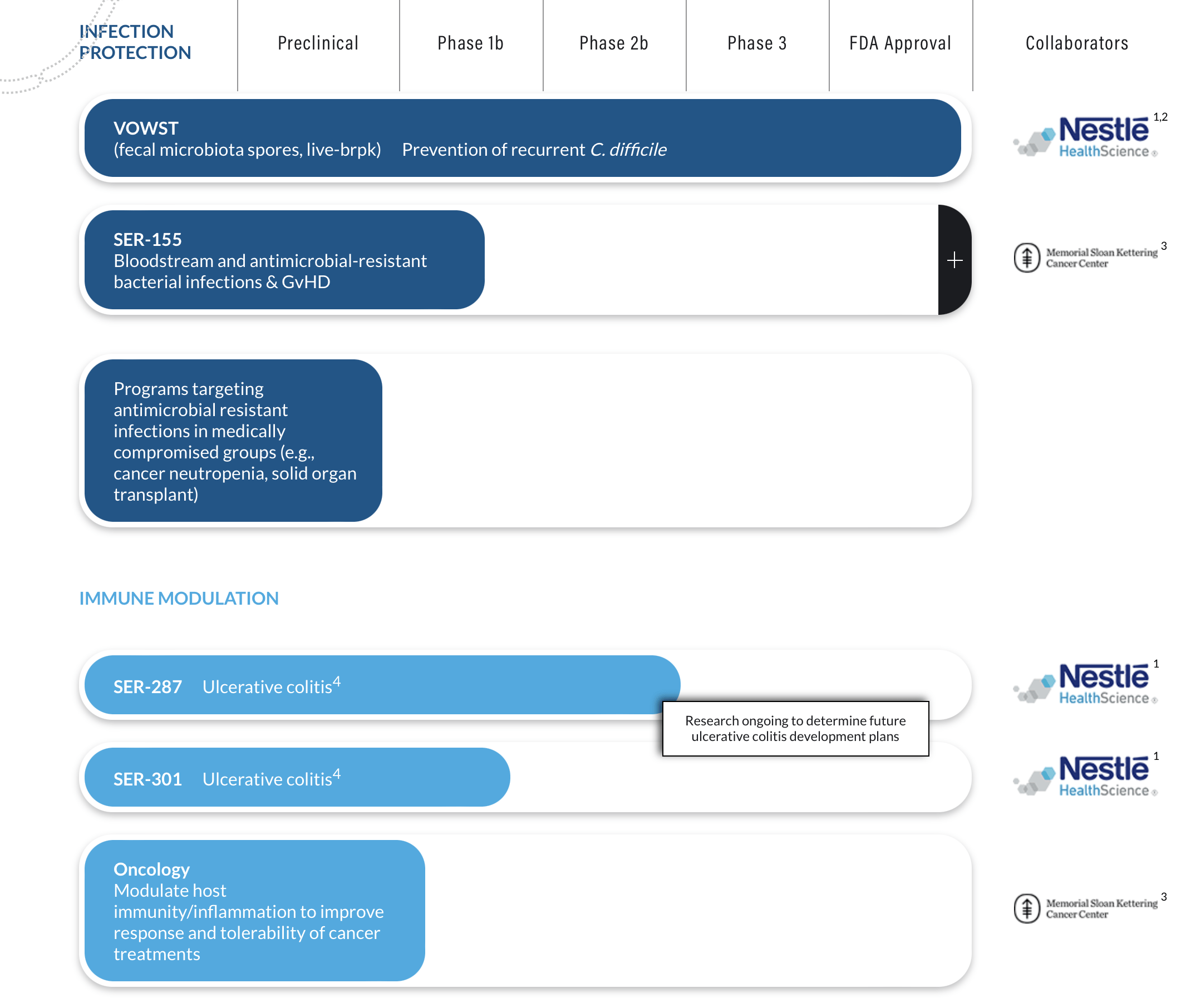

The Pipeline

Back in 2020, Seres had four clinical stage programs. Three of the four programs failed in the clinic. This should not be overlooked and is a poor outcome even in an industry where clinical failures routinely occur.

A ‘broad preclinical portfolio” and no late stage assets is not something investors should be pleased to see in a commercial stage company. It can be a sign that a company’s R & D efforts have a poor return.

It is also critical to note that the assets that failed were in lucrative indications. Improving the efficacy of check point inhibitors would be an enormous break through in oncology and transformational for a company such as Seres. Seres discontinued development of the melanoma program without releasing efficacy data. There is no asset listed in their pipeline despite listing oncology as part of their pipeline. Investors appear to be investing in the concept of an application in oncology rather than a specific asset at this point.

UC is a disease where existing treatments have both a poor safety profile and a low efficacy rate. There is a true unmet need for better treatments. In July of 2021, SER-287 failed to demonstrate any evidence of efficacy as measured by inducing remission in patients with ulcerative colitis (UC). In fact, in my view, there were no promising signals on primary or secondary endpoints including endoscopic improvement, endoscopic remission or symptomatic remission.

The company touted its next generation therapeutic, SER-301 which had bacterial species capable of an anti-inflammatory effect. Iteration is common and multiple attempts in the clinic are sometimes required. In SEC filings, the company described the changes. “SER-301 was optimized relative to SER-287 to incorporate bacterial strains that engrafted across the majority of patients in our previous trials, and strains that were associated with positive clinical outcomes and the modulation of key microbial-associated metabolites.” Unfortunately, SER-301 also failed. It did not induce clinical remission in any of the 15 patients which were enrolled despite engraftment.

In my view, the company should consider testing a microbiome therapeutic along with SoC rather than as monotherapy given the results. Dysbiosis of the gut microbiome may be only one part of this complex disease. SER-287 and SER-301 appear to have absolutely no impact clinically as monotherapy despite the company citing their assessment that, “SER-301 demonstrated pharmacological properties consistent with its design.” UC is a much more complex disease which is poorly understood relative to rCDI and it is not entirely surprising to see greater difficulties developing therapeutics.

Below is the pipeline on the company’s website. Given SER-287 and SER-301 failed in the clinic, in my view, it may be misleading to investors to list these assets as phase 1 and 2. It has been close to two years since the SER-287 readout and the company has not been able to outline a specific path forward. SEC filings state the company is conducting, "preclinical studies to inform next steps for further development in UC and IBD more broadly.” Seres notes that there is "potential for biomarker-based patient selection in Ulcerative Colitis,” This information lays out a concept for how they could proceed but does not identify a specific asset or a protocol for a future clinical trial. Currently, in my view, the only tangible things an investor has are 2 data sets in UC which showed not a hint of efficacy.

{kind=link}

SER-155

After reviewing the corporate presentation, the company appears to have shifted to focusing on “advancing opportunities in infection protection” for which they have multiple pre-clinical assets. Seres is developing SER-155 for patients who have undergone allogenic hematopoietic stem cell transplantation. The treatment goal is to reduce the risk for bloodstream infections, GvHD, and mortality. Data is due in mid-2024 and could establish proof of concept for this approach.

Finances

Seres ended the first quarter of 2023 with $ 106.5 million in cash and expects to receive a $125m milestone from Nestle. While most companies have scaled back spending given higher interest rates and a more challenging financing environment, Seres reported a net loss of $71.2 million for the last quarter which increased from $56.6 million for the same period in 2022. This is an extraordinarily high spend rate and at this rate this cash ($106 m + $125 m) could be gone within 12 months.

The quarterly press release did not provide an estimate of cash runway but the need for an additional raise is a possibility. Recently, Seres took on $250 m of debt which was likely needed to extend their cash runway and may be used to pay off their existing debt.

In June of 2022, Seres raised $100 m at $3.15 a share. In contrast, in 2020, before the failure of multiple assets, the company raised at $21.50 a share. The vastly different pricing may reflect a different funding environment but may also reflect institutional buyers perceptions of the value of the only remaining late stage asset, SER-109.

It is also notable that after the pipeline failures, AstraZeneca (AZN) which had partnered and funded research in oncology ended their collaboration with Seres.

Conclusions

While I see enormous potential for microbiome based therapeutics, investors should take a broad view of the company, its track record, its current pipeline as well as its financial position. Critically, investors should stay objective. Seres, in my view, has some positive and negative aspects which investors should consider.

Vowst is a safe, effective therapeutic and will likely be commercially successful. CDI is a sizable indication and analysts consensus suggests the possibility of $1B in peak sales. It will take time to obtain insurance coverage and establish market share. Commercialization is a costly endeavor and costs will likely exceed revenue for a significant time period. Longer term, there may be competitors and shifting market dynamics which may also impact the commercial opportunity.

Seres is spending approximately $250 m/ year and given their 50% share in profits and losses with partner Nestle Health Science, the company is likely many years from profitability. There will also be $250 m in debt that needs to be repaid and significant interest charges.

Investors may look at the pipeline page of the website and see multiple programs including in oncology and UC. But, in reality, the company has no late stage pipeline assets where proof of concept has been established. In fact, Seres has only one asset actively being tested in the clinic, SER-155, which is in a niche indication and in phase 1 testing. Investors taking an objective view should also consider the lack of a clear plan to move forward in UC and oncology after substantial time has elapsed and in light of the poor data sets produced to date.

At the end of the day, biotech companies need to translate scientific insights into revenue generating products. Investors should expect a return on their invested capital. Evaluating a company’s track record for returns on investments in R&D is prudent. Seres does not shine in this respect. 3/4 assets generating data sets which show no efficacy signal should be highly concerning to investors.

The $600 m market cap may be appropriate for a cash burning company with substantial debt, a sparse pipeline and a 50% share of a $1B peak sales asset which is years away from peak sales.

Despite the exciting news of the Vowst approval, more broadly, the company is in the early stages of translating the science into transformational products. Their success has been limited. Seres has a lot of work to do to before they realize the true potential of microbiome-based therapeutics beyond rCDI. Thus, the hold rating.

For further details see:

Seres Therapeutics: Still Work To Do Before Realizing Its Potential