SRG - Seritage Growth Properties: A Promising Turnaround Post-Sears Spin-Off

2023-11-07 03:16:56 ET

Summary

- Seritage Growth Properties adeptly capitalizes on its leasing model in flourishing markets like California, Florida, and Texas.

- Strategic financial maneuvering, such as prepaying its term loan and property sales, fortifies SRG against potential economic adversities.

- Despite challenges from its Sears Holdings spin-off origin, support from Berkshire Hathaway and reduced redevelopment costs indicate a potential turnaround for SRG.

- My adjusted EBITDA estimate suggests a "buy" rating with a price target of $10.14 per share, indicating a 29.6% upside underpinned by SRG's strategic debt management and asset liquidation initiatives.

Seritage Growth Properties (SRG), a promising self-administered REIT, adeptly capitalizes on its leasing model to bolster revenue, particularly in flourishing markets like California, Florida, and Texas. This adeptness is reflected in the favorable lease rates within its multitenant retail assets portfolio. Strategic financial maneuvering, such as prepaying its term loan and property sales directed at debt reduction, fortifies SRG against potential economic adversities. In my opinion, a pivotal element of SRG's valuation lies in the adjusted EBITDA I have computed, which adeptly mirrors operational capabilities by sidelining impairment losses. My valuation framework advocates a "buy" rating and suggests a price target of $10.14, projecting a 29.6% upside-a potentially rewarding prospect for investors. This assessment is underpinned by SRG's demonstrated fiscal prudence and its encouraging leasing tactic amidst a challenging real estate market.

Business Overview

Seritage Growth Properties operates as a self-administered and self-managed Real Estate Investment Trust ((REIT)), primarily dealing in the acquisition, management, redevelopment, and leasing of retail and mixed-use properties. SRG's expansive property portfolio across several states, especially in high-growth markets like California, Florida, and Texas, forms the cornerstone of its revenue generation strategy. By focusing on leasing, particularly in regions with favorable demographics and demand, the company appears to be on a solid footing to maintain a robust revenue stream. The strategy of further leasing the built retail footprint and densifying excess parking land through the addition of NNN pad sites seems an astute way to enhance shareholder value.

Notably, SRG started as a spin-off from the financially troubled Sears Holdings, inheriting a challenging business environment. This situation was exacerbated over time, especially with the financial obligations tied to its redevelopment efforts to transition from Sears and Kmart stores to new tenants, which was a costly and time-consuming endeavor. Berkshire Hathaway extended a $2.0 billion lifeline loan to SRG in 2018, recognizing the potential value in Seritage's asset portfolio, which was crucial, especially after Sears Holdings declared bankruptcy. The COVID-19 pandemic in 2020 further strained SRG's finances, but by early 2022, some repayment on the Berkshire loan was made, yet a substantial balance remains. An extension agreement for the loan repayment deadline to July 2025 has been negotiated. Despite the hurdles, the support from Berkshire Hathaway, alongside a reduction in redevelopment costs and materializing contracts, signals a potential turnaround for SRG.

Revenue and Strategic Profile

The company's revenue streams are chiefly derived from leasing its vast portfolio of properties, which, as of the latest data, encompasses interests in over 97 properties. This extensive portfolio indicates a broad market reach within the domestic real estate sector, particularly in the retail and mixed-use property segments. SRG operates its real property business via its working partnership, Seritage Growth Properties, L.P. Essentially, SRG is the entity that invests in the partnership, which in turn engages in real estate activities. This structure allows SRG to manage and operate its real estate assets through the partnership, ensuring a structured approach to its real estate business operations. The company's strategic approach highlights a forward-thinking mindset aimed at long-term value creation by identifying densification and redevelopment opportunities based on demand and demographic analytics. This strategy is further balanced by the initiative to monetize non-core assets, which addresses the need for immediate revenue generation while still eyeing future growth. A well-structured operating model has been adopted through partnerships, ensuring organized management and optimal operation of its real estate assets. Additionally, as of June 30, 2023, SRG showed a 73.0% leased rate in the multitenant retail assets portfolio, indicating a significant opportunity for additional revenue generation through leasing.

In my view, the diversified nature of Seritage's assets , spread across retail and mixed-use properties, positions it well to tap into various market segments, potentially mitigating risks associated with market fluctuations by balancing the performance of various property types. This diversification, coupled with many properties under management, hints at a significant scale of operations. However, SRG's net quarterly losses to common shareholders have increased at a concerning 49.3% CAGR since December 2020. Over this period, net quarterly losses for common shareholders deepened from $35.6 million to $96.9 million. This trend suggests that despite its size and market position, profitable revenue generation has been a challenge.

Source: Q2 2023 Financial Supplement

The underlying asset base and market scope present a substantial platform for revenue generation through leasing and property management services. Yet, the declining earnings trend does cast a shadow on the company's ability to capitalize fully on its assets to bolster its revenue profile. The management facet encapsulates a broad spectrum of activities such as acquisition, development, redevelopment, leasing, and occasionally selling these properties, preserving their value, ensuring they are leased out, and generating revenue.

SRG's Balancing Act in Debt Management and Asset Sales

SRG has strategically moved by prepaying $80 million towards its $1.6 billion term loan, displaying prudent financial management amid a challenging real estate market. This action, significantly reducing annual interest expenses, showcases SRG's effort to better its financial standing, driven by notable asset sale proceeds. However, the concern lies in the sustainability of such asset sales, crucial for SRG's plan to clear most of its debt by year-end.

The SRG's 10-Q for Q2 2023 showed it continued with the sale of properties and debt reduction. Key highlights include selling 127 properties since March 2022, generating about $1.4 billion, and reducing the term loan balance by $960 million. Sales in this quarter contributed $295.4 million, and 54 properties were sold year to date. The net loss stood at $96.9 million, with a total net operating income of $3.0 million. The report also details leasing activities, premier mixed-use projects, and financial adjustments like the $104.5 million impairment on four assets. This could be concerning, but I think overall, the story is of a continued wind-down of its assets and debt, potentially leading to a debt-free cash cow, albeit a smaller entity. Moreover, SRG reported a GAAP net loss of $96.9 million for Q2 2023, which, although disappointing, is still a marginal improvement over Q2 2022's net loss for common shareholders of $111.9 million.

Source: Q2 2023 Financial Supplement

SRG's prudent approach to debt management, showcased by the early repayment of its term loan, has yielded substantial interest savings, marking a meaningful step toward financial stability. This action has further extended the corporate term loan's tenure until July 31, 2025, providing SRG a financial buffer amidst a challenging real estate landscape. The annualized interest savings amounting to $56.0 million since the close of 2021, along with the gross proceeds from asset sales, embody a solid financial strategy.

However, the reported net losses in Q2 2023 alongside a high cash burn rate are concerning. The uncertain real estate market conditions compound these concerns, possibly affecting the targeted timeline for asset liquidation to service the term loan. This could, in turn, delay the ambitious objective of commencing shareholder distributions post-mid-2024. Despite such adversities, in my opinion, the juxtaposition of SRG's strategic debt management against a turbulent real estate market displays a broader narrative of resilience and a structured approach toward navigating market volatility. Yet, the inherent risks associated with an aggressive asset liquidation and debt repayment strategy cannot be dismissed.

Adjusted Valuation Analysis

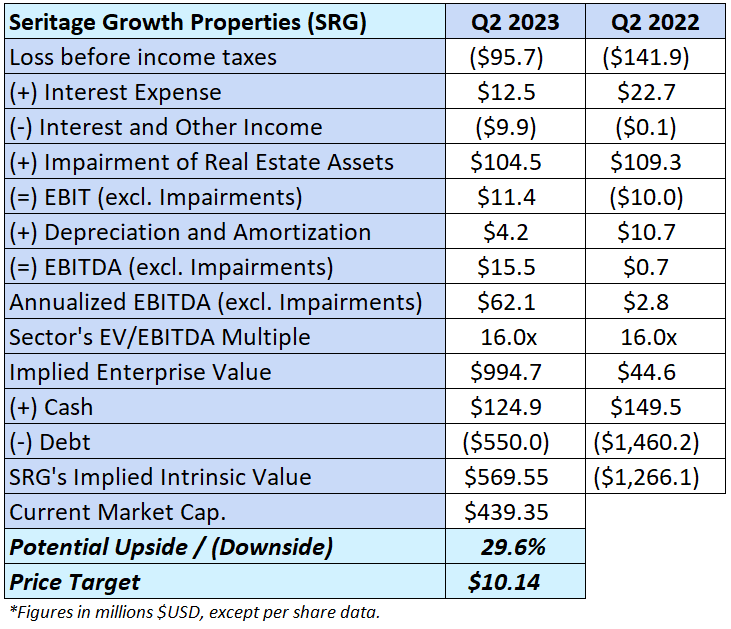

In the latest quarter , SRG witnessed a decline in total assets by $673.75 million, bringing it down to approximately $1.17 billion, while its total liabilities lessened by $512.87 million. This scenario, where assets are dwindling faster than liabilities amidst quarterly losses, raises concerns. A notable contributor to this situation is the hefty impairment losses amounting to $104.47 million for the quarter, a trend also observed in Q2 2022. This reiterates that there might be an overvaluation of SRG's assets. With the ongoing challenging real estate market coupled with SRG's debt reduction endeavors, further impairment losses could be on the horizon.

Nonetheless, I believe there's a silver lining when the impairment losses are set aside, unveiling a more favorable EBIT for SRG. By isolating the losses before taxes, adding back interest expenses and impairment losses, and deducting interest and other income, we are able to compute SRG's EBIT exclusive of impairment losses. Extending this analysis by including reported depreciation and amortization figures, we can derive an adjusted EBITDA, which, I think, provides a more accurate reflection of SRG's cash generation capability.

{kind=link}

As you can see, by applying the sector's EV/EBITDA multiple to this refined EBITDA figure and adjusting the current cash and debt balances, we arrive at an implied market cap of $439.35 million for SRG. This represents a robust 29.6% upside potential from the current levels, which, along with SRG's ongoing debt reduction, presents a compelling case for prospective investors. Hence, I infer that a "buy" rating with a price target of $10.14 per share is well-founded. This thorough analysis accentuates that despite the financial turbulence and the prevailing challenging real estate market conditions, SRG's strategic valuation and debt reduction trajectory lays a solid groundwork for a rewarding investment, underscoring a commendable return on investment prospect.

Investment Thesis Risks

SRG's investment thesis encapsulates a judicious balance of strategic foresight offset by market risks, notably within the US real estate domain, which seems poised for a correction amidst economic headwinds. An anticipated recession may thwart SRG's initiative to offload assets to curtail debt, which is its central financial strategy. Despite adept debt stewardship, the trajectory of net losses and receding earnings over the preceding five years is also disquieting. Disclosed impairment losses further exacerbate overvaluation apprehensions, which may intensify with the envisaged real estate market correction.

Therefore, success for SRG is substantially anchored on its continued asset liquidation and debt attenuation in the face of unfavorable market dynamics. Market crashes often significantly impede the strategy of leasing and monetizing non-core assets, creating a risk vector for SRG that cannot be ignored. However, it's worth noting that SRG's assorted assets in high-growth markets, coupled with a 73.0% leased rate, furnish a modicum of revenue stability.

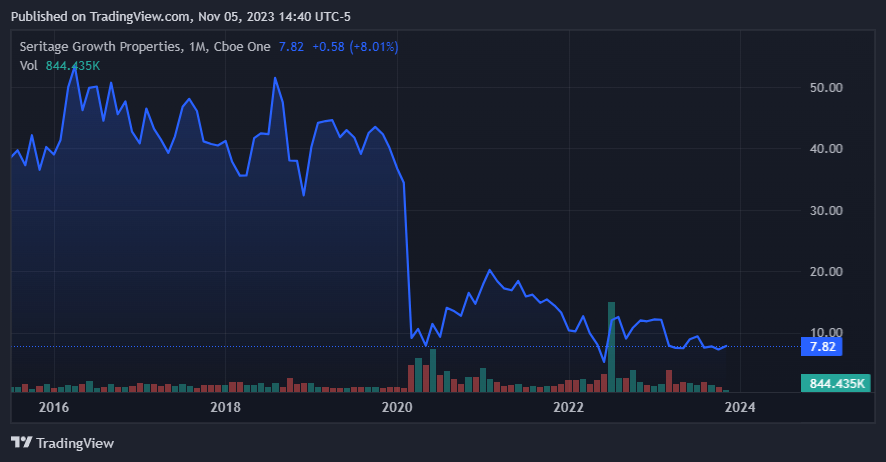

SRG's depressed valuation could be a wise entry price. (TradingView.)

{kind=link}

Conclusion

Overall, SRG's robustness originates from its proficient leasing strategy, especially within the fast-evolving markets of California, Florida, and Texas, serving as primary value drivers. The financial acumen displayed through the early repayment of its term loan, coupled with ongoing property sales to diminish debt, showcases a sturdy financial structure poised to tackle foreseeable real estate adversities. I believe the adjusted EBITDA portrays SRG in a favorable light, suggesting a "buy" rating with a price target of $10.14 per share. This implies a 29.6% upside potential. This is further reinforced by SRG's demonstrated fiscal prudence and promising leasing, collectively mitigating unpredictable real estate risks. Nevertheless, the potentially impending downturn is a formidable test of SRG's financial resilience and strategic framework. Yet, as a whole, I maintain a cautiously optimistic stance on SRG.

For further details see:

Seritage Growth Properties: A Promising Turnaround Post-Sears Spin-Off