SRG - Seritage: Intriguing Assets And Fascinating CEO

2023-11-11 02:50:47 ET

Summary

- Seritage, a former REIT that owns former Sears and Kmart locations, has undergone significant changes under the leadership of CEO Andrea Olshan.

- Olshan has sold around $1.3 billion of assets and paid down a significant portion of the company's outstanding loan.

- Under new CEO Andrea Olshan, Seritage changed its tax status, is liquidating assets, and paying down debt.

- Potential for over 100% upside with limited downside risk.

Seritage ( SRG ) is a former REIT that owns former Sears and Kmart locations. I first looked at it when Sears spun out the REIT in 2015 . Originally, SRG owned 235 Sears and Kmart locations and stakes in JV's of 31 others. The company raised debt to pay Sears for a sale leaseback back of the portfolio.

Initially, all but 19 of the properties had Sears as the tenant. The original concept was that value could be extracted by repurposing or redeveloping many of these properties. On the surface, this thesis had some merit and attracted some notable early investors such as Warren Buffett, who was the third largest shareholder for a time. A much more controversial investor, Eddie Lampert, is currently the largest shareholder. I stayed away from the name for a number of reasons. I felt the original portfolio was too complicated to analyze given the scale and large variance in quality. Moreover, Sears was a mess at the time and my general rule is if I think a company might file for bankruptcy, don't own anything related to it until the smoke clears.

Lastly, Lampert earned himself a questionable reputation as chairman of Sears from 2005 and as CEO from 2013 until its bankruptcy. Perhaps it's unfair to blame Sears's bankruptcy entirely on Lampert, but he definitely shoulders a good chunk of the blame given its capital spending and capital return policies during the thirteen years he was Chairman and five years he was CEO. I believe the Sears bankruptcy hurt Lampert's reputation enough that many investors wouldn't go near any company where he had managerial influence. Lampert was Chairman of SRG from its spin until March of '22.

It turned out my initial fears were justified. Sears filed for bankruptcy in October, 2018, by which time Sears was the primary tenant on about half of the properties and paid a little less than half of the ABR (annual base rent). All Sears leases were terminated about two years after that bankruptcy filing. Meanwhile, in its years leading up ending its relationship with Sears, the company never managed to create much value from redeveloping/repurposing/realigning its portfolio. One can see that lack of value creation in its cash flows. Ultimately, cash flows, particularly for REITs, are where the rubber meets the road.

all numbers in millions

| 2016 |

| 2017 |

| 2018 |

| 2019 |

| 2020 |

| Cash from Operations |

| $110 |

| $60 |

| $55 |

| $58 |

| -$47 |

| Disposal of Fixed Assets |

| $61 |

| $221 |

| $142 |

| $332 |

| Property Improvements |

| -$66 |

| -$243 |

| -$314 |

| -$247 |

| -$247 |

| Change in Investments |

| -$9 |

| -$38 |

| -$27 |

| -$63 |

| -$63 |

| Change in RE Interest |

| 0 |

| $257 |

| 0 |

| $20 |

| $20 |

| Total |

| $36 |

| $97 |

| -$65 |

| -$358 |

| -$5 |

I stopped the above table at 2020 for a reason. Clearly, the five-plus years as a public company were not leading to major value creation for shareholders. Therefore, in early 2021, the company scored a remarkable coup by getting Andrea Olshan to take over as CEO.

The Andrea Olshan Factor:

Andrea spent the previous seventeen years at Olshan Properties, the real estate firm founded by her legendary father. It's quite a portfolio. From that company's website , Olshan Properties and its affiliated companies own and/or manage over 13,000 multi-family residential units, 12 million square feet of retail and office space, and 1,447 hotel rooms.

Andrea was CEO of Olshan, having repositioned a number of assets in that large portfolio, when she left to take the top job at Seritage. She very quickly pivoted the business. About a year after taking over, she changed the company's tax status from a REIT to a c-corp to gain operational flexibility and better use the company's deferred tax assets (which currently stand at $201 million). By the summer of 2022, the company got shareholder approval to liquidate the company through asset sales and then perhaps selling the corporation (buyers for the whole business were solicited. None stepped forward to buy the company with the nearly 200 properties.)

Selling Properties and Paying Down Loan Balances:

Since taking over, Andrea and her team have sold around $1.3 billion of assets and paid down over 3/4's of a $1.6 billion loan outstanding to Berkshire Hathaway. As of quarter end (9/30), the company had $400 million of debt and $115 million of cash.

The company's recent earnings release detailed $78 million of properties that are in contract and $59 million of properties with accepted bids. Assuming those sales close, the balance sheet progression should look like:

Seritage Net Debt (Author Using Company's Quarterly Earnings)

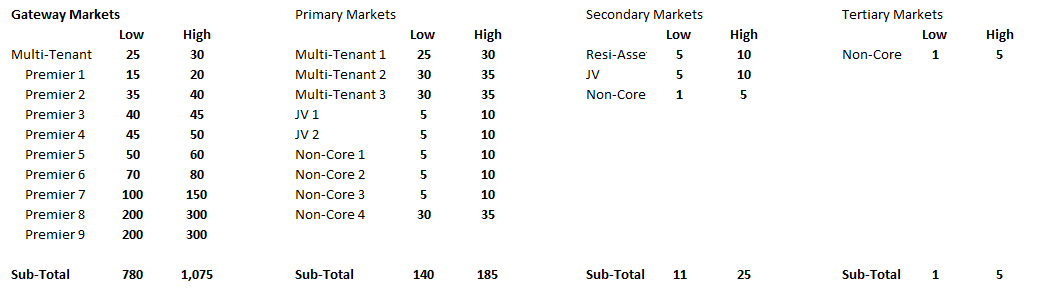

The company is on pace to end 2023 with about 25 properties (7 of which are considered "Premier" properties, which I'll discuss below). The company did a marvelous job of breaking down the remaining portfolio values this past quarterly earnings report. They laid out a range of values by property type and market type.

Seritage Asset Values by Market (Author Using Company's Quarterly Earnings)

{kind=link}

Clearly the main crux of the value lies in the premier properties in Gateway markets. That said, the other properties offer plenty of value and would more than cover the remaining net debt assuming the announced and pending asset sales go through.

Adding up the above values and using the $75 million of net debt number leaves you with some compelling math, particularly for a stock that closed at $8.64 per share yesterday.

Seritage Value Per Share (Author Using Company's Quarterly Earnings)

Given the company only has $490 million ($8.72/share) of common equity value on the balance sheet, there is a clear disconnect between even the low end of the potential asset values here and the market/accounting values.

I caution that there are other factors at play here. For starters, while the company has some rents coming in and is reducing operating expenses, it does run at a deficit, run rate of about $30-40 million per year. Andrea runs a tight ship and will bring down overhead as properties are sold, but there are certain costs that are impossible to escape. The longer it takes to sell properties, the bigger of a headwind these costs will be per share. The debt and the preferreds also cost 7% in annual interest expenses. The company can pay down the debt and call the preferred shares, but until they do, that's a cash drag as well.

The good news is there is a massive hidden asset too, the deferred tax assets that the company does not currently recognize because there is no certain path of profitability. Clearly, there would be accounting gains if the company can sell the properties at the values it estimated. These deferred tax assets should eliminate most if not all of the potential tax leakage.

I think zeroing out the operating costs and the deferred tax assets and assuming conservative sale and capital return process (all cash being returned at end of timeframes) even things out and leaves the high-low values per share as fair estimates of value per share. Using the above numbers and assuming the process takes one to three years leads to extremely compelling IRR's when starting at $8.64/share.

SRG Potential IRR's (Author Using Company's Quarterly Earnings)

Obviously, the higher the sales prices and the shorter the sale process, the better the returns.

The Andrea Wrinkle:

I'm clearly an Andrea Olshan fan. I think she has a unique intellect and skill set that are a perfect fit for these assets. She's the type of executive with whom I happily park money for as long as she's willing to manage it. Those who know me know I don't say that about too many people.

Andrea is smart enough to know that she is poised to have a company with seven high convexity assets, no debt, cash in the bank, and a large deferred tax asset. That backdrop in the hands of a brilliant, talented, and driven executive can a recipe for good things. Andrea has demonstrated some of her redevelopment chops with the UTC in San Diego (signing Amazon as an office tenant) and at the Aventura Mall. Every asset is different, with different redevelopment opportunities, but remember that Andrea has overseen residential, retail, and office properties in her previous gig running her family's business. She is capable of operating in a multi-use real estate situation. The backdrop I described offers Andrea an opportunity to do some pretty creative and special things. Personally, I'd like to see what Andrea can do.

Risk:

The main risks here are the difficulties of selling real estate assets into today's interest rate and real estate lending environment and Andrea sticking around. Interest rates have been pretty high for a while now and real estate lending has been weak since the Silicon Valley debacle in March. They have been moving assets regardless.

Andrea is a key risk. She offers so much here that I think she'd be hard if not impossible to replace.

A lot of people will cite Eddie Lampert's presence as a large shareholder as something to keep an eye on. Lampert remains controversial for a lot of people, especially institutional investors, given his oversight of Sears as it spiraled into bankruptcy. He does not have a seat on the board anymore, but he holds a lot of shares. His mere presence as an influence given his stake could scare a number of investors away.

Conclusion:

I think the risk reward here is very compelling. The assets here have a lot of optionality and potential value embedded in them and I think there in extremely capable hands. In my opinion it's more a matter of how high a return on investment given sale prices and timing of sales than risk of loss. That said, there are no promises in anything, and we've seen, the market has beaten up the stock at times. Personally, I'm willing to stomach the volatility to invest in these assets and unique CEO running them.

For further details see:

Seritage: Intriguing Assets And Fascinating CEO