SRG - Seritage: Nearing The Finish Line

2023-08-19 22:28:02 ET

Summary

- Seritage Growth Properties reported Q2-2023 results which were loaded with asset sales.

- Cash burn still remains high, and the impairment did not help inspire confidence in the terminal value.

- We examine how our previous suggestion worked out and give you three ways to outperform Seritage again.

The Seritage Growth Properties ( SRG ) saga has been a fascinating one to follow over the years. It would be fair to say that no Class B mall developer would get even a quarter of the attention that SRG managed to muster. That hype was built on none other than Warren Buffett having made a small personal investment in the common shares and his company, Berkshire Hathaway ( BRK.B ), extending a loan to SRG.

The longer term plans have not worked out for obvious reasons. SRG was replacing a Class D tenant (the now defunct Sears), with Class C tenants in Class B malls, using exceptionally large amounts of capex. Bulls bought into this model, while malls were falling into bankruptcy on a regular basis.

Fascinatingly, even after its announcement to finally just go for a straight liquidation , the stock has made little progress. Well, if you bought at the lows on the day of the announcement, you are up 30%.

If you bought the next day, you are down 27%.

On our last coverage we suggested that the stock remains a hopeless trap as it grapples with the reality of the hostile real estate climate. We recommended that you stay out of SRG and go with AvalonBay Communities Inc. ( AVB ) instead.

So at $8.30 a share, sure, you can argue there is upside. But keep in mind that this is very poor related to the risks. At the midpoint you might make 35% from here. You would make a similar amount by buying AVB, if it just returned to its August highs. AVB has an A rated balance sheet and you have a solid 4% yield here. There are many ways to make money in real estate today and SRG represents a poor choice with very limited upside and significant downside

Source: No Returns For The Weary

AVB delivered total returns of 19% above that of SRG at close to a 45% annualized clip.

We update our views with the recently released Q2-2023 results.

Q2-2023

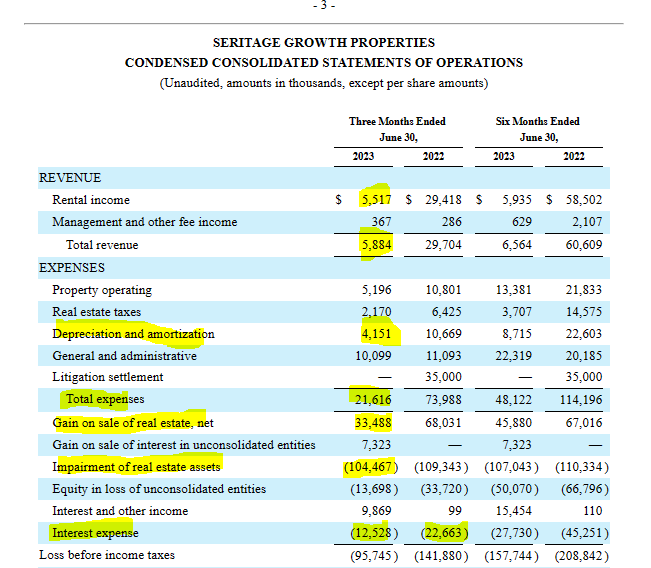

SRG's revenue dropped by 80% when compared to 2022. This number was still a big jump from Q1-2023 where its revenues at almost gone down to zero. New leases signed increased the quarterly run-rate to almost 9x the amount seen in Q1-2023. Cash burn before interest expenses remained high as the company went through $11.58 million.

{kind=link}

SRG Q2-2023 10-Q

What did help the bulls was that SRG did manage to push through almost $300 million of asset sales during the quarter and another $68.4 million subsequent to quarter end. The interest expense highlighted above is from the weighted average loan balance during the quarter and should move substantially lower in Q3 and Q4. Alongside that good news, we saw that the premier property Aventura, got hit with a large impairment loss.

During the quarter ended June 30, 2023, due to increasing development and construction costs and deteriorating market conditions, the Company recognized a $101.5 million impairment on its development property in Aventura, FL. In accordance with GAAP, the impairment was recognized as a result of the carrying value of the asset exceeding the undiscounted cash flows over the estimated holding period. The amount of the impairment is determined by applying a discount to the projected cash flows and writing down the carrying value to the discounted current fair value.

The Company will continue to evaluate its portfolio, including its development plans and holding periods, which may result in additional impairments in future periods.

Source: SRG Q2-2023

Investors tend to disregard these non-cash charges, but they tend to point to problems in case of real estate companies. Here, they likely reflect high labor and other inflationary headwinds. Expanding cap rates are also playing a role as risk-free rates are way higher than 1 year back.

Outlook

SRG is a liquidation story coming to a conclusion.

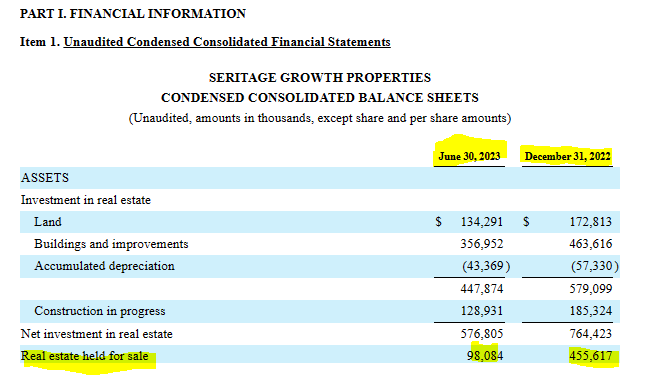

While the deals have been done in a fast and furious manner over the last 4 publicly reported quarters, we think this is now coming to a crawl. We see the real estate held for sale as a good indicator of what will happen 2-3 quarters out and that well has been drying up.

{kind=link}

SRG Q2-2023 10-Q

SRG still has approximately $475 million of net debt to get through before it starts paying anything to shareholders.

SRG Q2-2023 10-Q

Overall cash burn is still high relative to SRG's tiny market capitalization. Property and corporate level bleed will likely be close to $20 million a quarter. Capex has been about $50 million for first half of the year.

SRG Q2-2023 10-Q

This run-rate is obviously an improvement from the amount the company spent during its peak days.

SRG 10-K 2019

But the $100 million annualized run-rate is still pretty high for SRG's $446 million market capitalization.

Verdict

We think the next two quarters will prove our earlier thesis that SRG is selling the easiest parcels first and it has wildly overestimated the net liquidation value of the company. That is the key reason it did not receive any offers to buy the entire company, even when real estate conditions were far better. Asset sales should slow remarkably as we get into Q4-2023 and bulls better hope that they are right about both the pace and the price of sales. With AVB having delivered a solid relative outperformance we are not ready to hang with the same horse against SRG.

We think over the next 12 months there are three ways you can outperform SRG stock returns.

One way would be to stay in cash and collect a cool 5.5% risk-free. For those looking for a SRG specific play we would suggest the SRG preferred shares ( SRG.PR.A ). With a 7.32% yield today and about a 4% upside to par you have a good return profile to liquidation over the next 18-36 months. Finally, our strategy of refusing to buy into the promised rainbow and repeatedly selling lottery tickets also works once again. We are referring to our previous ideas of selling covered calls into high volatility events for SRG. Today the implied volatilities have died down but you probably could get about $0.85 for the January 2024 calls.

Author's App

Granted that today you are really not getting the kind of buffer you got the last time we suggested a covered call.

Author's App, Previous Trade Idea

But if you add up all these premiums, you probably would be in a far better position than simply waiting with bated breath for the upside capture. At present our best guess for the range of liquidation value for the company is between $6.00 and $13.00. This is down from our last range of $8.00-$14.00. That range was also lowered from the one previous to that ($10-$18). Our assessment comes from what we see as extremely troubling trends for commercial real estate with bank lending standards tightening at a rapid clip and leading economic indicators continuing to weaken.

Michael A Arouet

Net Quantitative tightening is back with a vengeance.

Jim Bianco

We would stay out of the common stock as the risk-reward is just not set up right.

For further details see:

Seritage: Nearing The Finish Line