SCI - Service Corporation International: Negative Scenario Could Be Favorable For This Industry Consolidator

2023-09-22 12:50:45 ET

Summary

- SCI operates in the stable and fragmented deathcare sector. In this industry, it is the dominant player.

- American society is transitioning toward preferring cremation over burial. This affects funeral homes and will offer an acceleration in the consolidation process of the sector.

- The current valuation offers attractive returns, even considering a rather negative scenario.

Investment Thesis

I have decided to give a 'buy' rating to Service Corporation International ( SCI) because, although funeral homes tend to face challenges during recessions, the market has already factored in a negative scenario in the share price. Additionally, the problems this sector is facing could present an opportunity for SCI to consolidate this fragmented industry.

In this article, we will discuss the natural competitive advantages that arise from operating funeral and cemetery services, the challenges in the sector, and how SCI could capitalize on them.

Business Overview

Service Corporation International is a well-known funeral and cemetery services company based in the United States. It is one of the largest providers of funeral, cremation, and cemetery services in North America. The company operates under various brand names, including Dignity Memorial, and offers a range of services related to funeral planning, pre-arrangements, cremation, burials, and memorialization.

Operating a business in the funeral and cemetery services industry can come with several competitive advantages, for instance, it's a sensitive and regulated industry at both the federal and state levels. While this can cause headaches for established funeral homes, it is also a large barrier to entry that prevents numerous competitors from entering. This is why in many areas, there usually be limited competition, especially if you operate in a smaller town or rural area that can give your business a strong position in the local market.

Furthermore, demand is highly stable and predictable; after all, death is a natural part of life and is inevitable. In 2021, the number of annual deaths in the US reached a peak of almost 3.5 million . Although this figure was significantly impacted by COVID-19, the reality is that it is a number that has consistently grown due to the increase in the American population and the rising number of people over 65 years of age.

National Center of Health

An Industry Consolidator

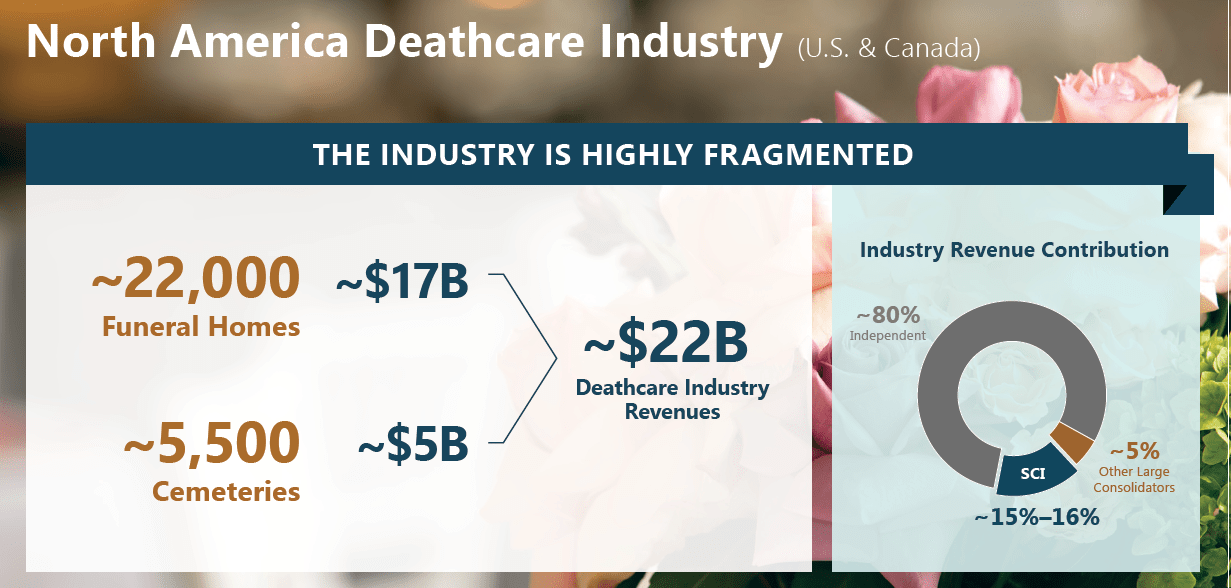

The funeral home market in North America is quite fragmented, with an estimated 19,000 in the United States and 22,000 in the US and Canada combined. Since its inception, SCI recognized this and decided to implement a strategy of acquiring these small, independent businesses through debt, with the intention of later integrating them into its operations to reduce costs through economies of scale. As a result, it currently owns 1,500 funeral homes, which represent 7.5% of the market share in terms of locations and approximately 15% in terms of revenue.

Service Corporation International

{kind=link}

Despite the factors mentioned earlier, such as the increase in deaths and the growing number of elderly people, the sector has experienced an annual decrease of 0.7% since 2004 . This contrasts greatly with what one would expect in the market, as there is an increasingly greater demand, which should be reflected in the number of funeral homes providing the supply.

Cremation over Burials

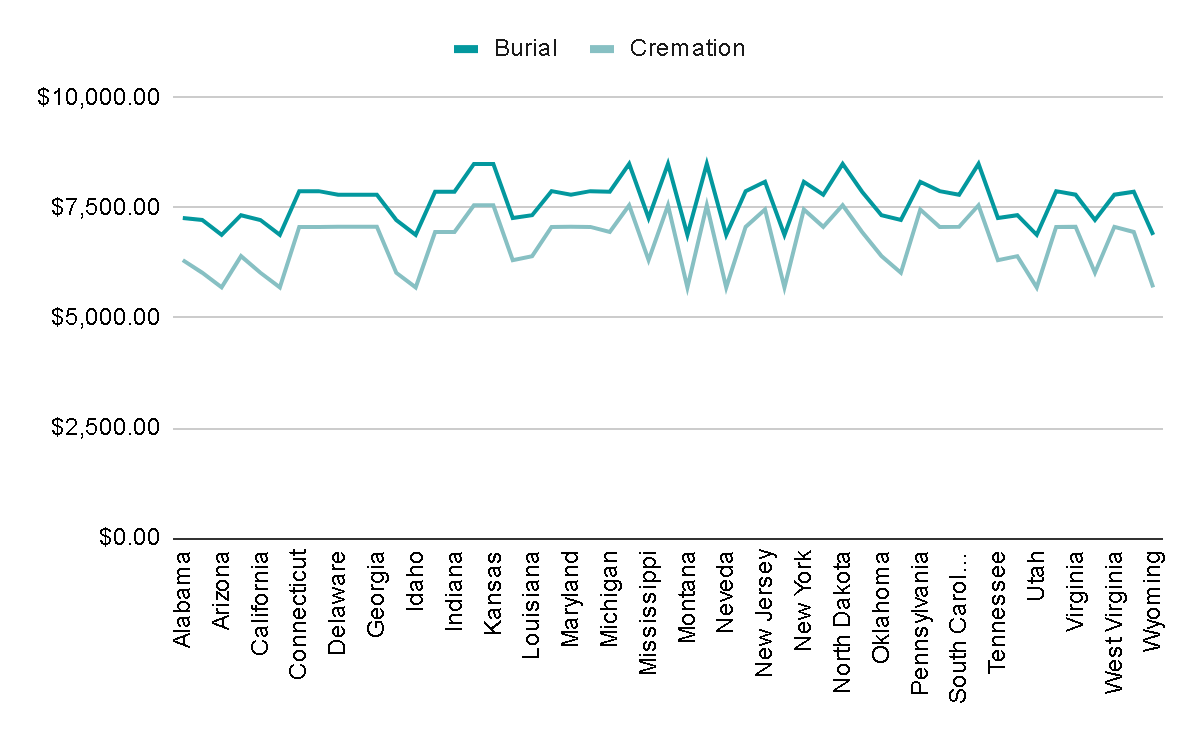

One possible explanation for this decrease could be the rising popularity of cremation over burial. In 2015 , more Americans began to prefer cremation over burial for the first time, and projections for 2030 suggest that close to 70% of the population will choose cremation over burial. Cremation offers several advantages - it is typically more flexible, does not require dedicated funeral spaces (which are increasingly scarce in highly urbanized areas), and, above all, it is more cost-effective than burial.

Cremation is generally less expensive than traditional burial, as it eliminates the need for a burial plot, casket, burial vault, and other associated expenses. This makes it a more affordable option for many families. In the United States, the average cost for a burial is approximately $7,600, while the average cost for cremation is around $6,700.

This shift in trend could be one reason why small funeral homes may encounter challenges due to reduced demand, leading some to close or sell their businesses to large consolidators, such as SCI itself.

{kind=link}

Key Ratios

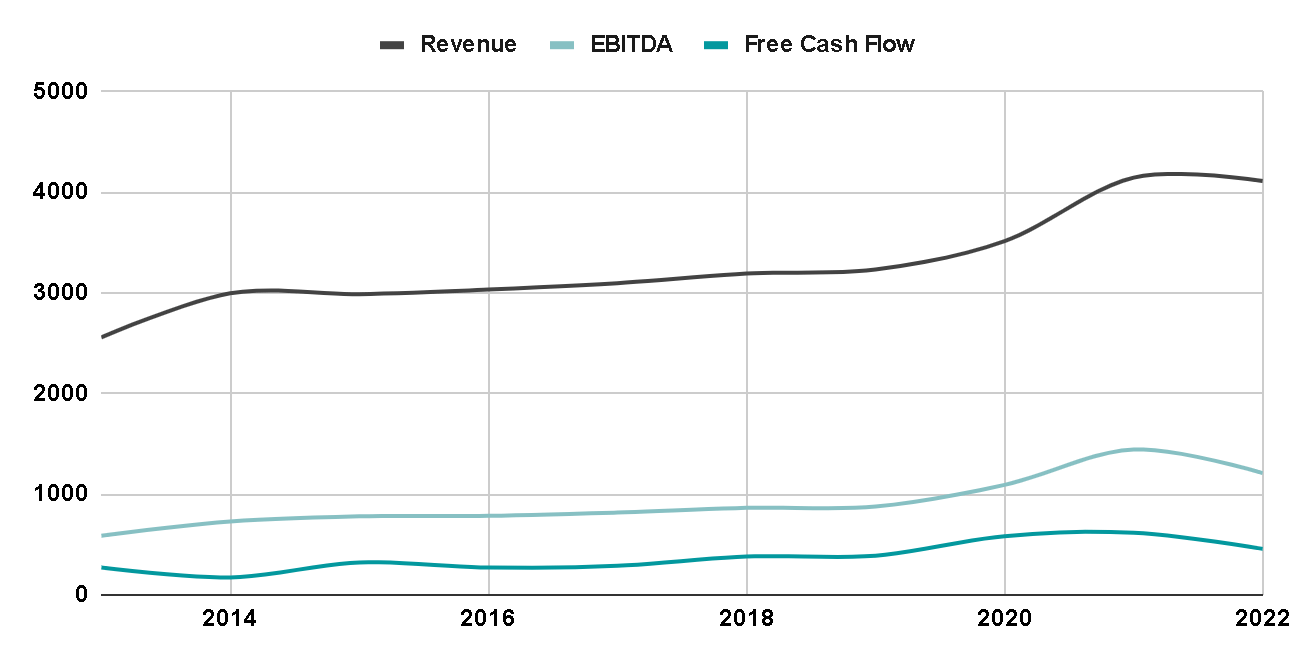

The company's growth has been slow, but stable over the last decade. Revenues grew at rates of 5% annually while EBITDA grew at 8% CAGR. This could be explained by the increase in scale that has occurred during these years. As a major player in the industry, SCI can leverage its scale to negotiate better deals with suppliers and achieve economies of scale in its operations, reducing costs per service.

{kind=link}

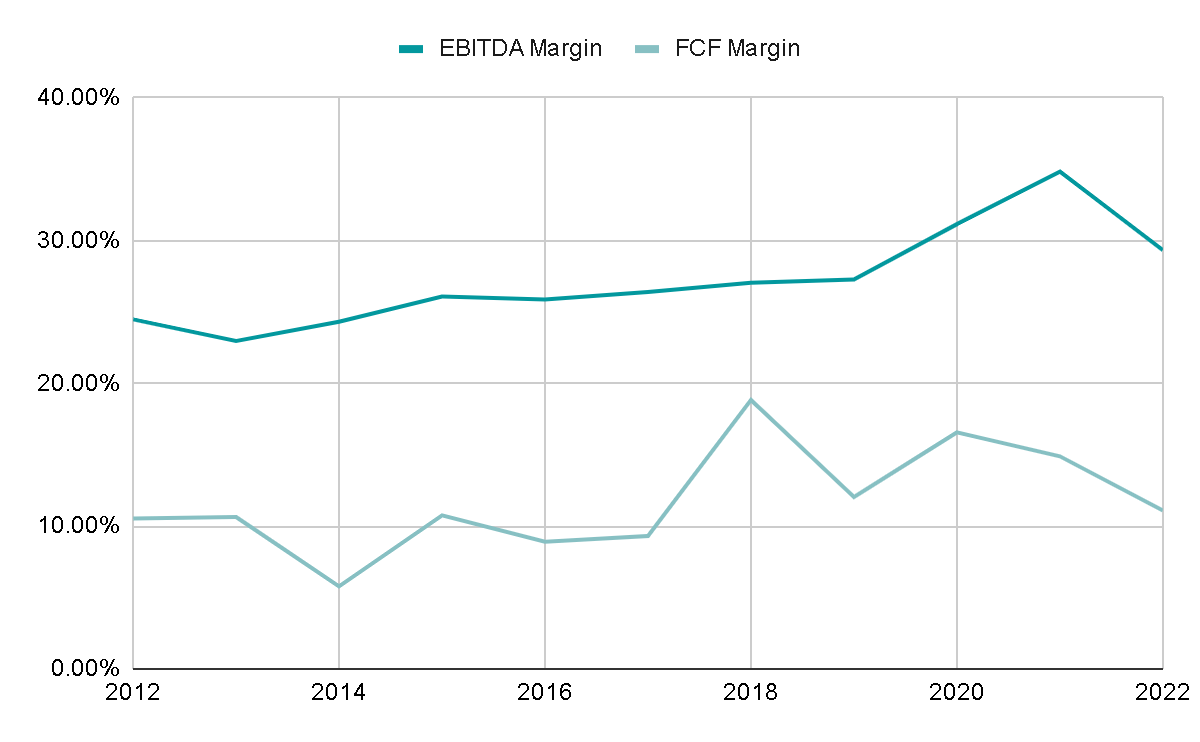

In the following image, you can better see this increase in the margins mentioned above. On average, the company has maintained EBITDA margins of 27%, although in recent years it has been around 30%, while the FCF Margin has been around 12%.

{kind=link}

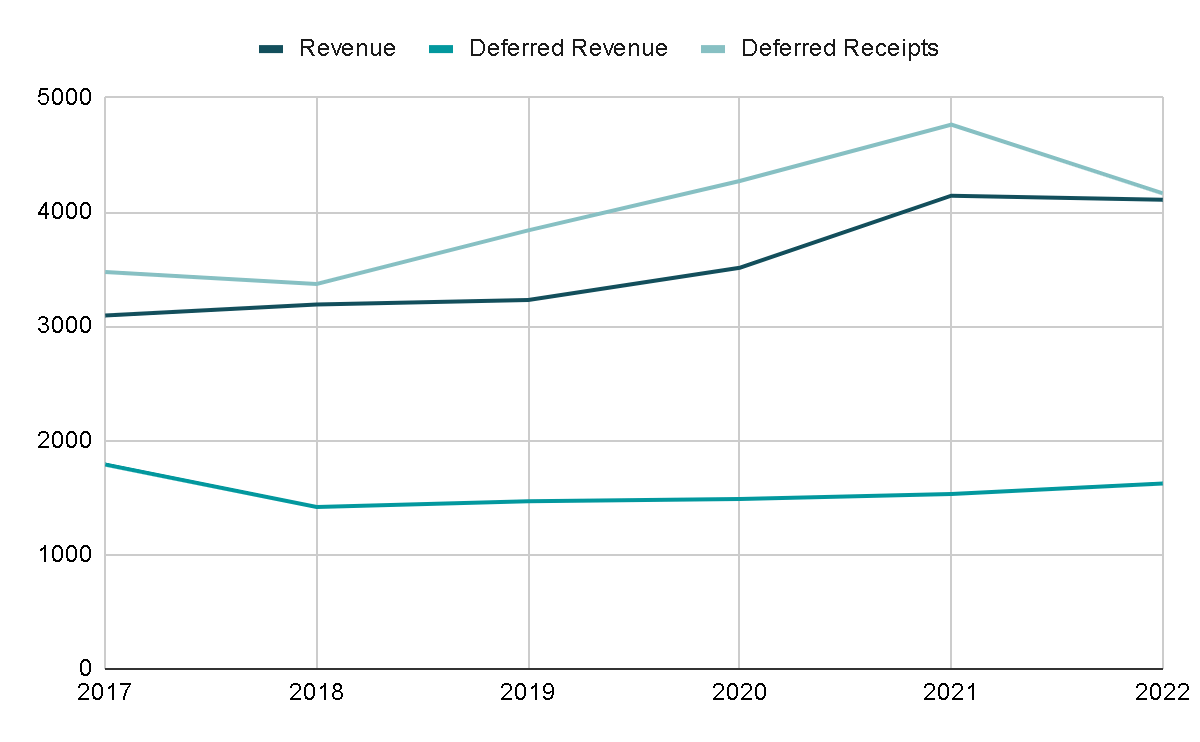

It is important to mention that SCI has deferred revenue and deferred receipts on its balance sheet. These are recorded as liabilities and represent money that has been received but has not yet been recognized as income because the service has not been performed.

Deferred receipts represent cash received in advance of providing goods or services. This can result in improved cash flow for the company, providing it with funds that can be used for various purposes, such as investing in the business or paying down debt. Also recognizing revenue over time rather than all at once can result in more stable and predictable earnings, which can be appealing to investors.

{kind=link}

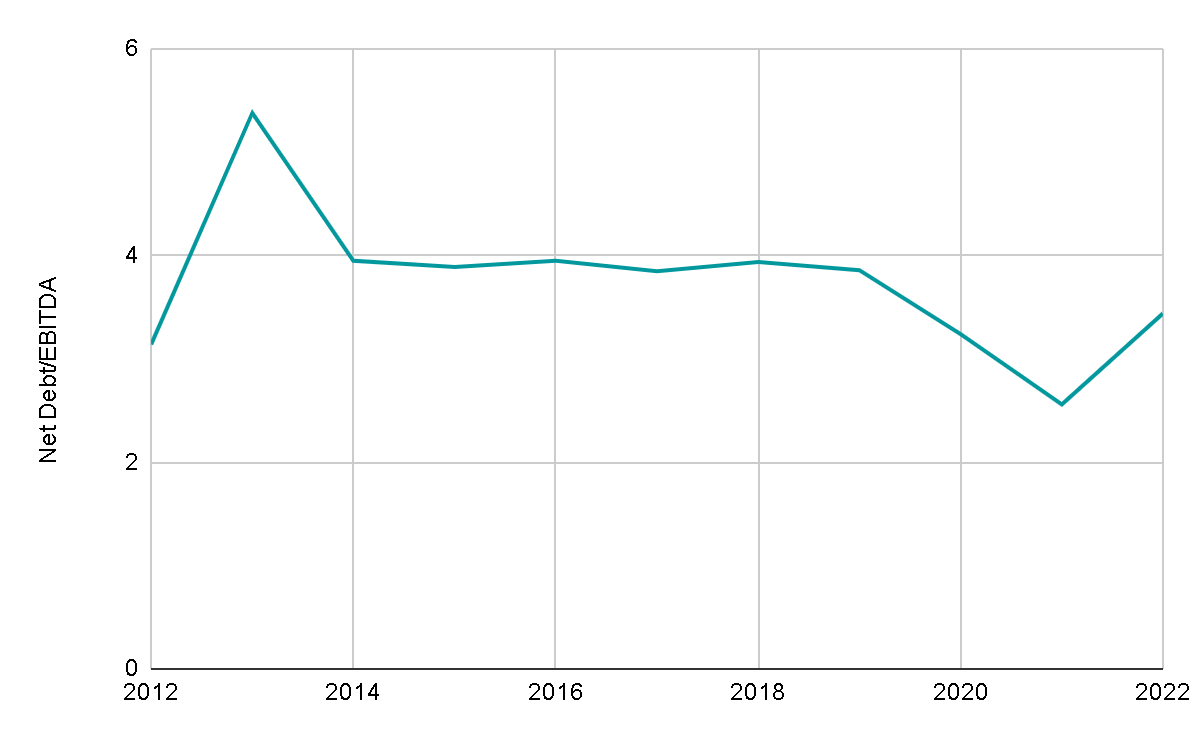

The company typically maintains Net Debt/EBITDA ratios between 3x and 4x. The ten-year average is 3.75x, and at the end of FY2022, it was 3.45x.

Although this might seem high, the company has a strong history of managing debt even in challenging environments, as demonstrated during the financial crisis of 2008. Moreover, because it operates in a highly predictable business and typically receives cash in advance, it is easier to anticipate potential crises and make informed decisions based on this predictability. In the Q2 2023 conference call , they commented that they expected to maintain the ratio in a range of 3.5-4x EBITDA.

{kind=link}

Valuation

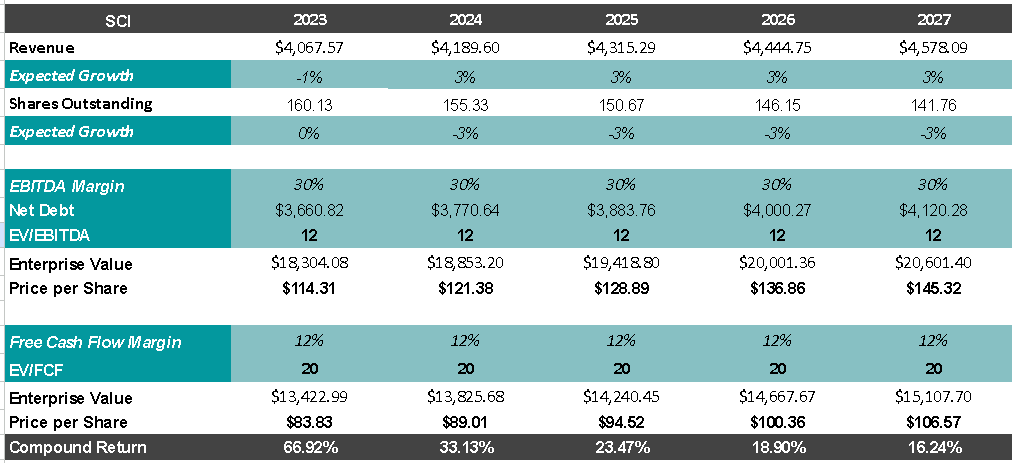

For the valuation, I will consider analysts' expectations for FY2023. They anticipate a 1% decrease in revenues, which is reasonable given the current macroeconomic situation. If the situation resolves itself during this year, I estimate that for the coming years, revenues can grow by 3% annually while maintaining profit margins similar to those of FY2022.

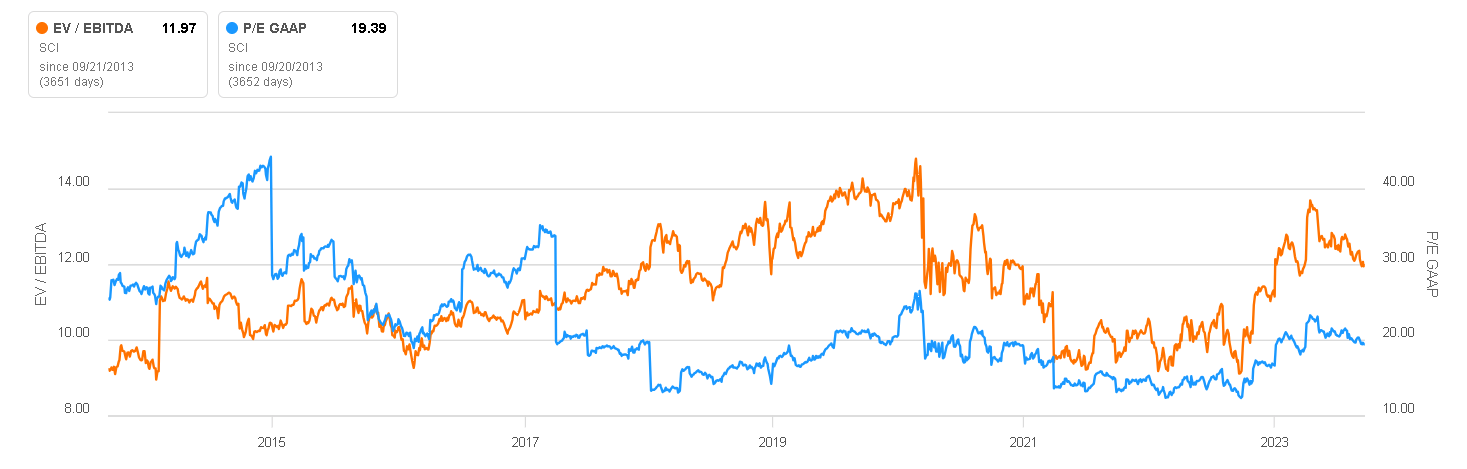

For the exit multiples, I will use the average of the last 10 years, which has been around 12x EV/EBITDA and a P/E ratio of 20. Additionally, I will consider annual buybacks of 3%, which is much lower than those carried out in recent years.

Valuation Metrics (Seeking Alpha)

{kind=link}

If these assumptions materialize, we would be looking at an annual return of 16% over the next 5 years, effectively doubling the investment in this period.

Base Scenario (Author's Representation)

{kind=link}

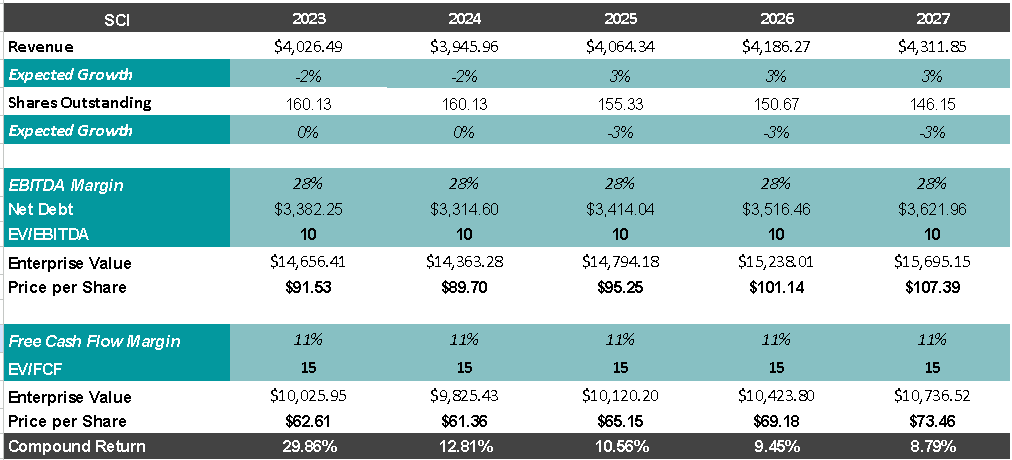

Now, I would like to make a slightly more negative scenario, since the company does not usually do well during recessions. In this scenario, I will assume that revenue decreases for two years in a row, plus the company has to stop share buybacks and margins decrease a little. This would scare the market and assign lower-than-average multiples of 12x EBITDA and P/E of 15x.

Even in this negative scenario, the company would still provide annual returns of 8% from current prices. This suggests that there is a margin of safety, and the market is already factoring in a negative scenario for SCI. This could be seen as a positive sign in case the much-anticipated recession does indeed occur.

Bear Scenario (Author's Representation)

{kind=link}

Risks

Cremation Trends: As mentioned earlier, the increasing popularity of cremation over traditional burials can impact SCI's revenue, as cremation services are generally less expensive. Managing this shift in the industry is a challenge, but it could also present an opportunity for SCI to continue consolidating the sector by acquiring independent funeral homes affected by this trend.

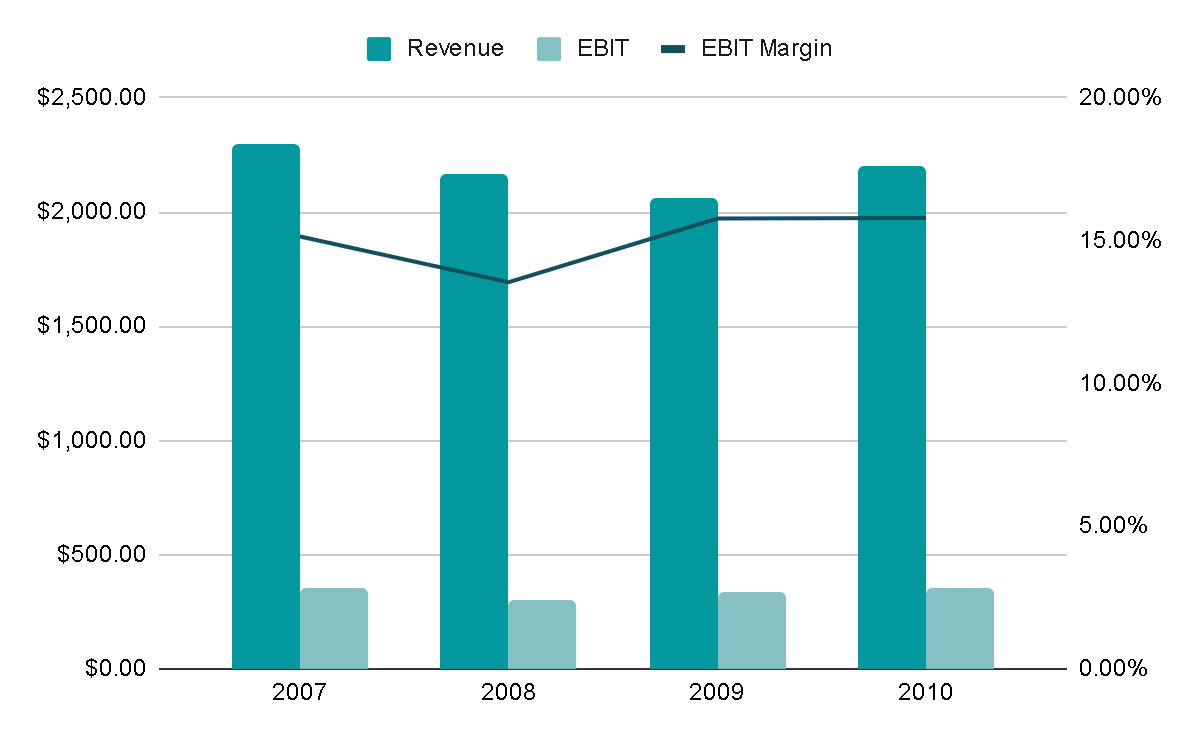

Economic Factors: SCI's business is sensitive to economic conditions. Economic downturns can lead to reduced demand for funeral and cemetery services, as families may opt for less expensive options or delay funeral arrangements. An example of this is the company's experience during the 2008 financial crisis. Between 2007 and 2010, revenues decreased by 4% in total, and in 2008, the EBIT margin was reduced from 15% to 13%. The company later returned to its typical growth rate and margins, but this illustrates that during a recession, SCI's revenues could be affected.

Revenue During 2008 (Author's Representation)

{kind=link}

High-Interest Rates: This can impact SCI in terms of its financing costs. If SCI carries debt, higher interest rates can increase its financing costs, potentially reducing profitability. In a company with such high leverage ratios, this is even more concerning. Additionally, high interest rates can discourage consumer borrowing, which might affect families' ability to finance funeral expenses or pre-need contracts, potentially impacting SCI's revenue.

Final Thoughts

There is a shift in the industry toward cremation, and this will undoubtedly impact funeral homes. However, I believe that this could prove to be a favorable scenario for industry leaders like Service International Corporation to further consolidate this fragmented market. After all, when an industry faces challenges, new competitors are less likely to emerge, and existing competitors may shrink over time.

It's also important to note that the funeral and cemetery services industry remains relatively resilient to economic downturns compared to many other sectors because death is a natural part of life, and funerals are often considered essential services. Therefore, the fact that the market is already factoring in a negative scenario in the share price seems extremely positive to me. From this perspective, the downside appears to be controlled, and the risk of significant losses is lower.

Considering all of this, I believe SCI is in an attractive position for a buy-and-hold investment over the years. I would give it a 'buy' rating and would even be tempted to consider it a 'strong buy' if it weren't for the potential impact of a recession on its income.

For further details see:

Service Corporation International: Negative Scenario Could Be Favorable For This Industry Consolidator