SCI - Service Corporation: Still Attractive Despite A Return To Normalcy

Summary

- After a couple of great years caused by the COVID-19 pandemic, Service Corporation International is seeing its financial performance pull back some.

- This may be disappointing to some investors, but the company remains a quality enterprise and its long-term picture should be positive.

- Shares aren't the cheapest, but they do likely offer some upside from here.

One of the first five companies I ever bought shares in was Service Corporation International ( SCI ). I find it cool that my birth as an investor began with a stock that often deals with the end of so many other things. Recently, things have not been going exactly great for the company, either from a fundamental perspective or from a share price perspective. Since the middle of last year, the stock has pulled back some, driven by a reduction in revenue, profits, and cash flows. For sure, shares of the business are not exactly cheap. But they do look fundamentally appealing for what is and should be, in the long run, a fairly stable enterprise if managed appropriately. Given my belief in what the future holds for the business, I would make the case that shares offer enough upside potential to justify a soft ‘buy’ rating on the stock at this time.

Underwater… I guess underground

Back in the tail end of July of 2022, I revisited my bullish thesis on Service Corporation International. Leading up to that point, the company had done quite well over the prior few years. Unlike many other firms, it was benefiting from the COVID-19 pandemic. Given that it operates funeral homes and cemeteries, and owns other related assets, this shouldn't be much of a surprise. But by that point in 2022, the firm was experiencing a bit of difficulty when it came to profits. This caused the stock to not be as cheap as it was previously. But even with that factored in, I felt as though it offered investors enough potential to warrant a ‘buy’ rating. Since then, things have not gone exactly as I thought they might. While the S&P 500 is up 0.4%, shares of Service Corporation International have seen downside of 4.7%.

{kind=link}

Author - SEC EDGAR Data

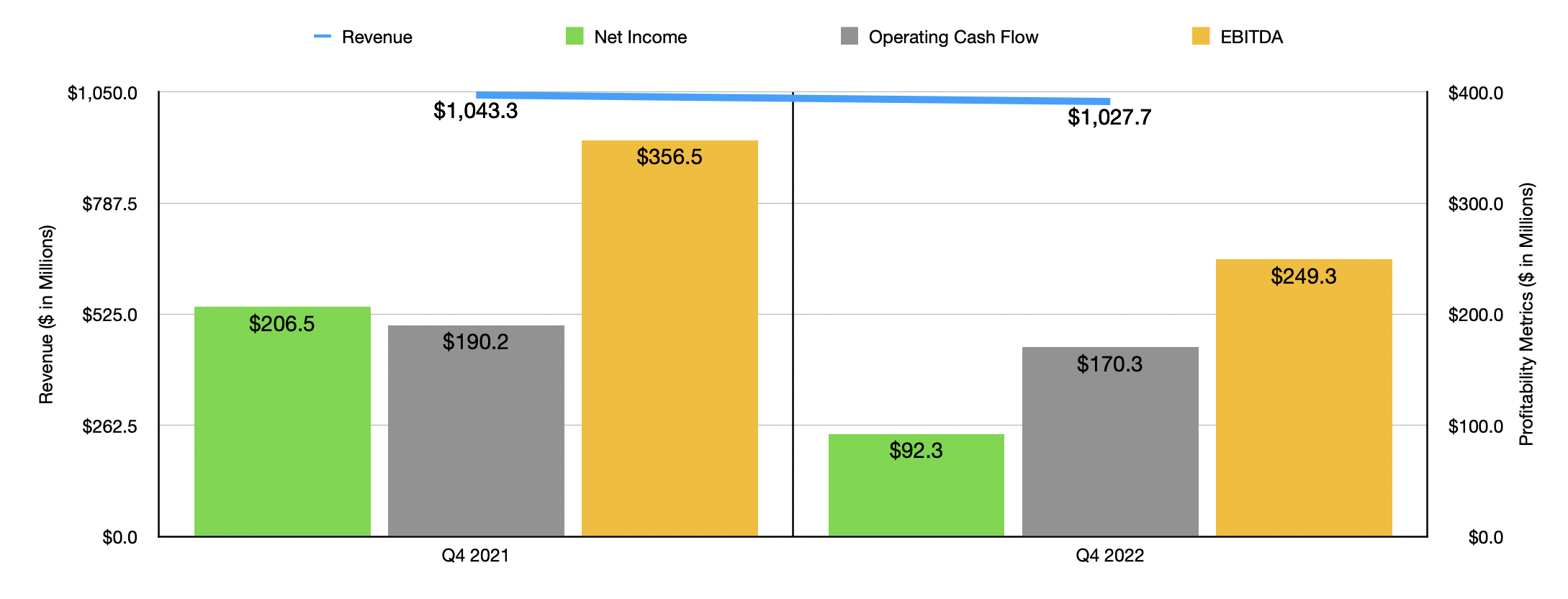

At the end of the day, this downside really has to do with recent financial performance achieved by management. Consider how the company performed in the final quarter of its 2022 fiscal year. Sales came in during that time at $1.03 billion. That's 1.5% lower than the $1.04 billion the company reported only one year earlier. This drop was driven by weakness across multiple areas of the business. core revenue under the funeral side of the business fell from $507.7 million down to $488.5 million. This was driven largely by a decline in at-need revenue, which fell from $329.3 million to $311.3 million. The company suffered from a decline in the comparable number of funeral services performed from 54,383 down to 49,395. This was offset some by a modest increase in the comparable funeral average revenue per service. Under the cemetery side of the business, core revenue actually increased. This was largely driven by growth in the firm’s recognized pre-need property revenue. Once again, at-need revenue for the company fell. This all largely relates to the fact that the COVID-19 pandemic has been essentially over for some time now.

The drop in revenue for the company brought with it a decline in profits. Net income dropped from $206.5 million in the final quarter of 2021 down to $92.3 million in the final quarter of 2022. Naturally, some of this pain was driven by the decline in sales. But there were other factors as well. The company's gross profit margin shrank from 31.6% down to 27.3%. On its own, this decline accounted for $44.2 million in missed pre-tax profits. Higher inflationary employee-related and maintenance costs hit the company on this front. On the funeral side of the business, the firm suffered from increased energy costs as well, while the cemetery side of the enterprise had to contend with higher merchandise costs. Another big pain for the business was a surge in its corporate general and administrative expenses. These shot up from $40.8 million to $107.9 million. This change was driven in large part by a $64.6 million estimate for an immaterial preliminary settlement in a private litigation matter in Florida. Without this, the company's bottom line would have been far better. Even so, other profitability metrics took something of a hit as well. Operating cash flow declined from $190.2 million down to $170.3 million. Meanwhile, EBITDA dropped from $356.5 million down to $249.3 million.

{kind=link}

Author - SEC EDGAR Data

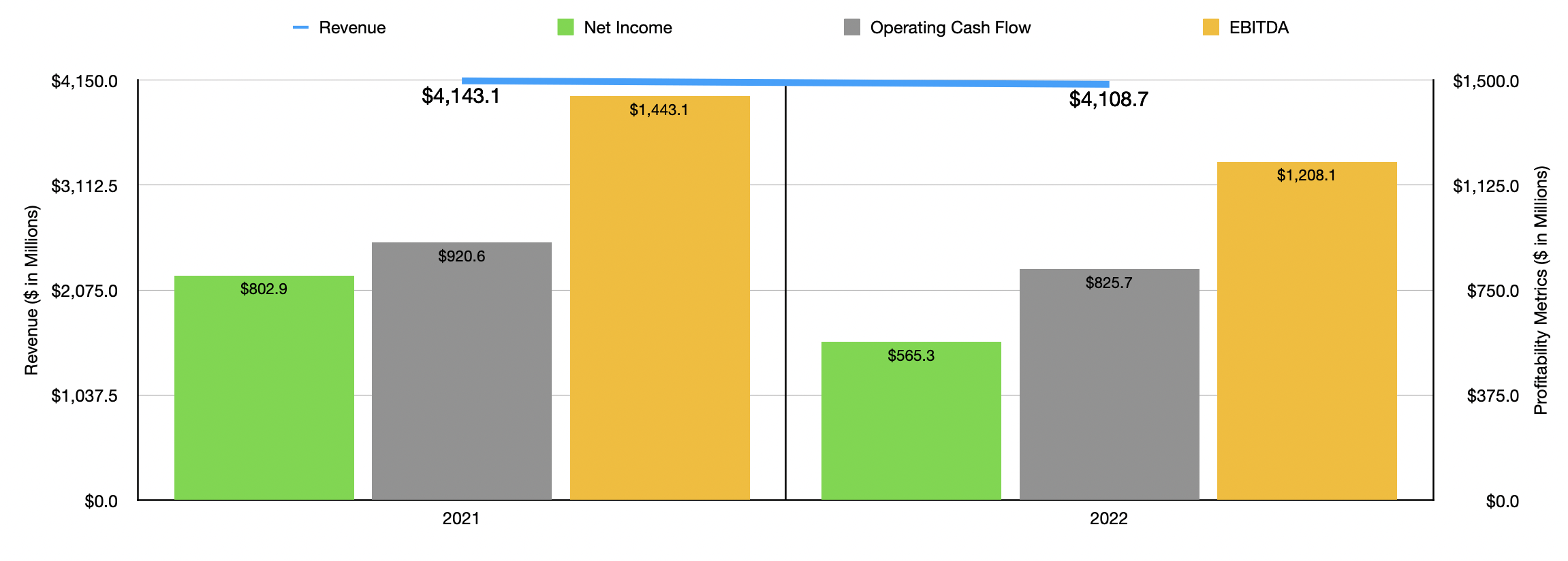

The final quarter of 2022 was not the only weak spot for the business. The firm also experienced pain throughout 2022 in its entirety. The same factors driving weakness in the final quarter of the year caused overall revenue for the business to drop from $4.14 billion in 2021 down to $4.11 billion in 2022. Net income fell even harder, plunging from $802.9 million down to $565.3 million. We saw operating cash flow shrink from $920.6 million to $825.7 million. And finally, EBITDA for the business fell from $1.44 billion down to $1.21 billion.

Management has provided some guidance when it comes to the 2023 fiscal year. They currently anticipate earnings per share of between $3.45 and $3.75. At the midpoint and assuming that the company doesn't buy back any stock, this would imply net income of $576.5 million. For full transparency, from 2021 through 2022, the company did repurchase about 5.9% of its outstanding stock. So it is possible overall net income could be a bit lower if the firm does a repeat of last year. They also estimate that operating cash flow will be between $740 million and $800 million. This range excludes the aforementioned legal charge that may need to be paid out. If we assume that EBITDA will fall at the same rate that operating cash flow is expected to, we should anticipate a reading for 2023 of $1.13 billion.

{kind=link}

Author - SEC EDGAR Data

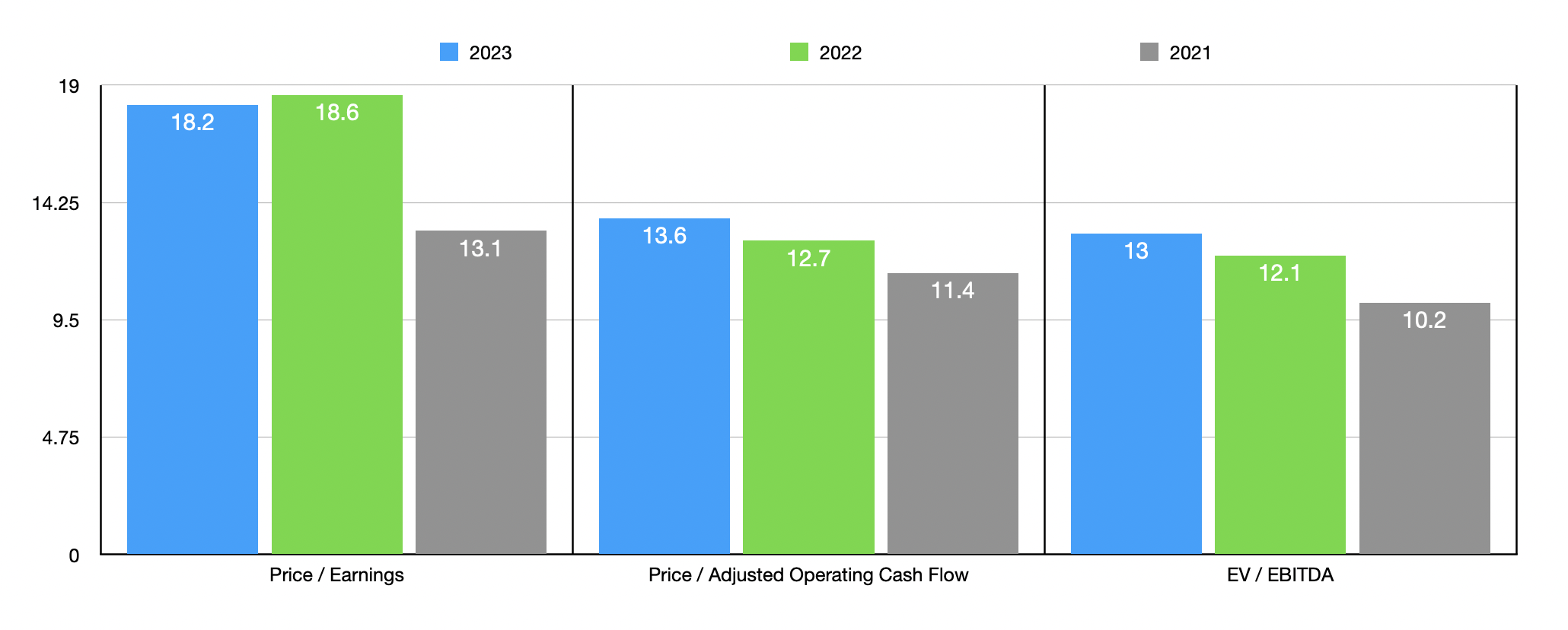

Based on the data provided, I was able to easily value the firm. As you can see in the chart above, I provided valuation data for the 2021 and 2022 fiscal years, as well as on a forward estimated basis for 2023. On a price-to-earnings basis, the stock does look a bit lofty. But when it comes to cash flow, shares look attractive enough to warrant some attention. As part of my analysis, I compared the data from 2022 to the data from three other deathcare businesses. On a price-to-earnings basis, the two companies that had positive results had multiples of 13.1 and 16.3, respectively. In this case, Service Corporation International was the most expensive of the group. Using the price to operating cash flow basis, the range was from 8.8 to 20.2. And when it comes to the EV to EBITDA approach, the range is from 10.5 to 36.5. In both scenarios, two of the three firms were cheaper than our target.

| Company |

| Price / Earnings |

| Price / Operating Cash Flow |

| EV / EBITDA |

| Service Corporation International |

| 18.6 |

| 12.7 |

| 12.1 |

| Carriage Services ( CSV ) |

| 13.1 |

| 8.8 |

| 10.5 |

| Matthews International ( MATW ) |

| N/A |

| 9.9 |

| 36.5 |

| Hillenbrand ( HI ) |

| 16.3 |

| 20.2 |

| 10.8 |

Takeaway

From what I can see, Service Corporation International is a solid company that is likely to continue to do well in the long run. The firm benefited significantly from the COVID-19 pandemic. The pandemic is essentially over, and this is good for everybody else, but bad for Service Corporation International. Relative to similar firms, we don't have much to work with. But on the whole, the company is priced near the higher end of the scale. At the same time, we need to keep in mind that this is a high-quality firm that should continue to perform well fundamentally down the road. And because shares of the business are not exactly out of the ballpark for what you would expect for such a high-quality operator, I do believe that a soft ‘buy’ rating is appropriate at this time.

For further details see:

Service Corporation: Still Attractive Despite A Return To Normalcy