SFBS - ServisFirst Bancshares: Reducing The Earnings Outlook Maintaining A Hold Rating

2023-03-18 05:13:40 ET

Summary

- The margin will likely continue to contract in the first quarter of the year following the significant deposit mix deterioration in the last two quarters.

- I'm reducing the loan growth estimate as my outlook is now worse than before.

- The December 2023 target price suggests a moderate upside from the current market price. Further, SFBS is offering a low dividend yield.

- SFBS is currently relatively safe from the ongoing banking crisis.

Earnings of ServisFirst Bancshares, Inc. ( SFBS ) will most probably be flattish this year. The margin will likely contract further in the first quarter of this year because of the recent deterioration of the deposit mix. Moderate loan growth will likely counter the effect of margin contraction and thereby support the bottom line. Overall, I'm expecting ServisFirst to report earnings of $4.60 per share for 2023, almost unchanged from the earnings last year. Compared to my last report on the company, I've reduced my earnings estimate because I've decreased both my loan growth and margin estimates. The year-end target price suggests a small upside from the current market price. Therefore, I'm maintaining a hold rating on SFBS stock.

Reducing the Margin Estimate Due to the Recent Deposit Mix Deterioration

ServisFirst Bancshares’ net interest margin dipped by 12 basis points in the fourth quarter of 2022 after surging by 38 basis points in the third quarter and 37 basis points in the second quarter of 2022. The dip in the fourth quarter was attributable to a jump in deposit costs. This was because the deposit mix significantly worsened over the last two quarters, leading to a rise in the deposit beta (or rate sensitivity). ServisFirst’s non-interest-bearing deposits dropped to 28.8% by the end of December from 39.8% at the end of June 2022. There's a chance that the proportion of non-interest-bearing deposits in total deposits will fall even further because rate hikes will incentivize depositors to chase yields. Non-interest-bearing deposits ranged from 22.5% to 24.9% from 2015 to 2019, and there's a chance that they will return to this range.

On the other hand, ServisFirst Bancshares’ assets will most probably continue to support margin expansion this year. Variable-rate loans account for 37% of the loan portfolio, as mentioned in the March presentation . Although 87% of variable loans have a floor, that floor is quite low at around 4.52%, while the average loan portfolio yield was much higher at 5.32% in the fourth quarter of 2022, as mentioned in the earnings release . Therefore, any rate hike will immediately lift the yields for at least 37% of the portfolio.

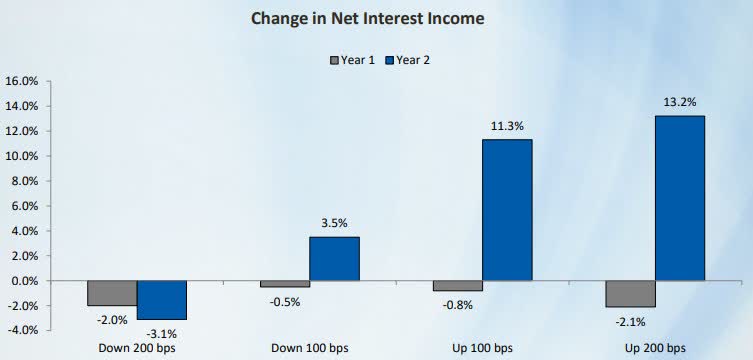

The results of the management’s rate-sensitivity analysis given in the presentation showed that a 200-basis points hike in interest rates could decrease the net interest income by 2.1% over the first year, and increase the net interest income by 13.2% over the second year of the rate hike.

{kind=link}

Considering these factors, I'm expecting the margin to dip by ten basis points in the first quarter of 2023 and then increase by 6 basis points in the last nine months of the year. Compared to my last report on ServisFirst Bancshares, I've reduced my margin estimate as the deposit mix has already worsened more than I expected.

Loan Growth Likely to Dip to Single Digits

Although loan growth slowed down in the fourth quarter of 2022, it remained at an impressive level. The loan portfolio grew by 3.6% during the quarter, which took the full-year growth to 22.6%. The management expects loan growth to fall to a high-single-digit range, as mentioned in the conference call . This target seems reasonable as elevated mortgage rates will hurt the mortgage loan segment. Mortgage loans, including owner-occupied commercial and one-to-four-family residential loans, made up 59% of total loans at the end of December 2022.

In my opinion, the strong employment situation in ServisFirst’s markets shows that loan growth is unlikely to fall too low. The company operates in several southeastern states, namely Alabama, Florida, Georgia, North Carolina, South Carolina, and Tennessee. All these states currently have unemployment rates that are low from a historical perspective.

Considering these factors, I'm expecting the loan portfolio to grow by 8.2% in 2023. In my last report, I estimated loan growth of 11.5% for this year. I've reduced my loan growth estimate as the economy is doing worse than what I previously anticipated.

The following table shows my balance sheet estimates.

| Financial Position |

| FY18 |

| FY19 |

| FY20 |

| FY21 |

| FY22 |

| FY23E |

| Net interest income |

| 263 |

| 288 |

| 338 |

| 385 |

| 471 |

| 516 |

| Provision for loan losses |

| 21 |

| 23 |

| 42 |

| 32 |

| 38 |

| 48 |

| Non-interest income |

| 19 |

| 24 |

| 30 |

| 33 |

| 33 |

| 28 |

| Non-interest expense |

| 92 |

| 102 |

| 112 |

| 133 |

| 158 |

| 183 |

| Net income - Common Sh. |

| 137 |

| 149 |

| 170 |

| 208 |

| 251 |

| 251 |

| EPS - Diluted ($) |

| 2.53 |

| 2.76 |

| 3.13 |

| 3.82 |

| 4.61 |

| 4.60 |

| Source: SEC Filings, Earnings Releases, Author's Estimates(In USD millions unless otherwise specified) |

In my last report on the company, I estimated earnings of $5.16 per share for 2023. I've reduced my earnings estimate as I've reduced both my margin and loan growth estimates.

Risks are Limited Despite the Ongoing Banking Crisis

In my opinion, ServisFirst is relatively safe from the current banking crisis due to the following reasons. (Readers can see this article to get a brief overview of the crisis and its timeline.)

- Both Signature Bank ( SBNY ) and SVB Financial ( SIVB ) had sizable exposure to Californian businesses. ServisFirst’s market is concentrated in southeastern states, as mentioned above. Therefore, ServisFirst appears safe from spillover effects.

- Silvergate Capital ( SI ) failed because of its crypto assets. ServisFirst has not mentioned any exposure to crypto assets or digital tokens in its SEC filings.

- Unrealized losses on ServisFirst Bancshares’ securities portfolio amounted to only $19 million, which is just 1.4% of total equity. If there is a run on deposits, like in SBNY and SIVB’s cases, then ServisFirst will have to sell its securities at a loss to repay its depositors. However, this loss is too small to have a material impact.

Maintaining a Hold Rating

ServisFirst usually increases its dividend in the last quarter of the year. Therefore, I’m expecting the company to increase its dividend by $0.02 per share to $0.30 per share in the fourth quarter of 2023. The earnings and dividend estimates suggest a payout ratio of 25% for 2023, which is close to the five-year average of 22%. Based on my dividend estimate, ServisFirst Bancshares is offering a forward dividend yield of 2.0%.

I’m using the historical price-to-tangible book (“P/TB”) and the peer price-to-earnings (“P/E”) multiples to value ServisFirst Bancshares. The stock has traded at an average P/TB ratio of 2.82x in the past, as shown below.

| FY19 |

| FY20 |

| FY21 |

| FY22 |

| Average |

| TBVPS - Dec 2023 ($) |

| 25.7 |

| 25.7 |

| 25.7 |

| 25.7 |

| 25.7 |

| Target Price ($) |

| 67.4 |

| 69.9 |

| 72.5 |

| 75.1 |

| 77.6 |

| Market Price ($) |

| 56.5 |

| 56.5 |

| 56.5 |

| 56.5 |

| 56.5 |

| Upside/(Downside) |

| 19.3% |

| 23.8% |

| 28.4% |

| 32.9% |

| 37.5% |

| Source: Author's Estimates |

ServisFirst’s P/E multiple has been quite erratic in the past. Therefore, I think it's better to take the peer average when trying to value the stock than the historical P/E average. Peers are currently trading at an average of 10.8x, as shown below.

| SFBS |

| UCBI |

| INDB |

| FIBK |

| HWC |

| UMBF |

| Peer Average |

| EPS - 2023 ($) |

| 4.60 |

| 4.60 |

| 4.60 |

| 4.60 |

| 4.60 |

| Target Price ($) |

| 40.4 |

| 45.0 |

| 49.6 |

| 54.2 |

| 58.8 |

| Market Price ($) |

| 56.5 |

| 56.5 |

| 56.5 |

| 56.5 |

| 56.5 |

| Upside/(Downside) |

| (28.5)% |

| (20.3)% |

| (12.2)% |

| (4.0)% |

| 4.1% |

| Source: Author's Estimates |

Equally weighting the target prices from the two valuation methods gives a combined target price of $61.1 , which implies an 8.1% upside from the current market price. Adding the forward dividend yield gives a total expected return of 9.8%. As this expected return is not high enough, I’m maintaining a hold rating on ServisFirst Bancshares.

For further details see:

ServisFirst Bancshares: Reducing The Earnings Outlook, Maintaining A Hold Rating