SFBS - ServisFirst Bancshares: Too Lofty For My Money

2023-10-09 11:58:23 ET

Summary

- ServisFirst Bancshares is a small bank trading at high multiples, making it an expensive investment opportunity.

- The bank has experienced growth in loans, deposits, and assets, but also has a high exposure to uninsured deposits.

- While the bank has shown positive revenue and profit growth, recent weakness and a high valuation make it less attractive compared to other prospects.

Thanks in large part to the banking crisis that occurred earlier this year, I have succeeded in finding a number of fairly attractive and very attractive banks. But not every player that I have come across has been a solid opportunity. While the quality of some of the companies in question might be high, the price paid for that quality is sometimes too high. A great example of this can be seen by looking at ServisFirst Bancshares (SFBS), a fairly small bank that is trading at lofty multiples relative to many of the other players that I've seen out there. Although the quality of the company is nothing to scoff at, I do not see a compelling reason to be optimistic about future price appreciation.

An expensive bank

Before we get into the rationale behind my thinking, it would be helpful for those who have not followed this enterprise to understand a bit about what it does and how it operates. In short, ServisFirst Bancshares is a bank holding company that is based out of Birmingham, Alabama. Through its banking subsidiary, it operates 32 full-service banking offices spread across Alabama, Florida, Georgia, North Carolina, South Carolina, and Tennessee. It also has loan production offices in Florida. Just like most commercial banks, ServisFirst Bancshares engages in a variety of traditional banking services.

Examples include, but are not limited to, accepting deposits, originating commercial loans, originating commercial real estate loans, construction and development loans, residential real estate loans, and even providing various consumer loans for those who qualify. Examples of the consumer loans would include end uses like vehicle financing, home equity loans, and more.

{kind=link}

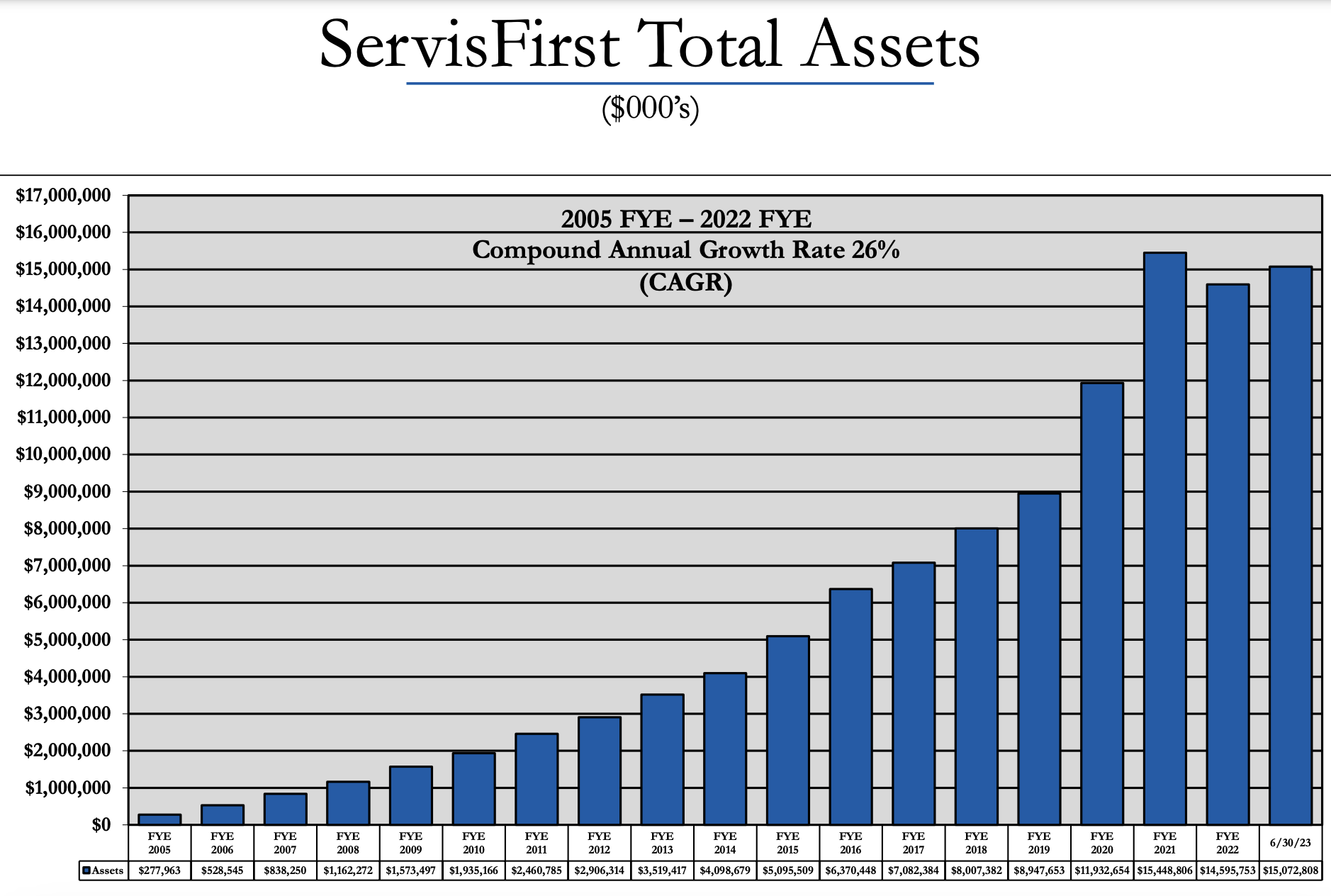

While the banking industry may not seem all that interesting from a growth perspective, management does take pride in how fast they have succeeded in growing the company. Using both organic means and acquisitions, the institution has succeeded in growing its total assets at a 26% annualized rate between 2005 and 2022 . The last three years of that window of time have seen assets virtually flat line. But then again, these have been difficult and uncertain economic times.

{kind=link}

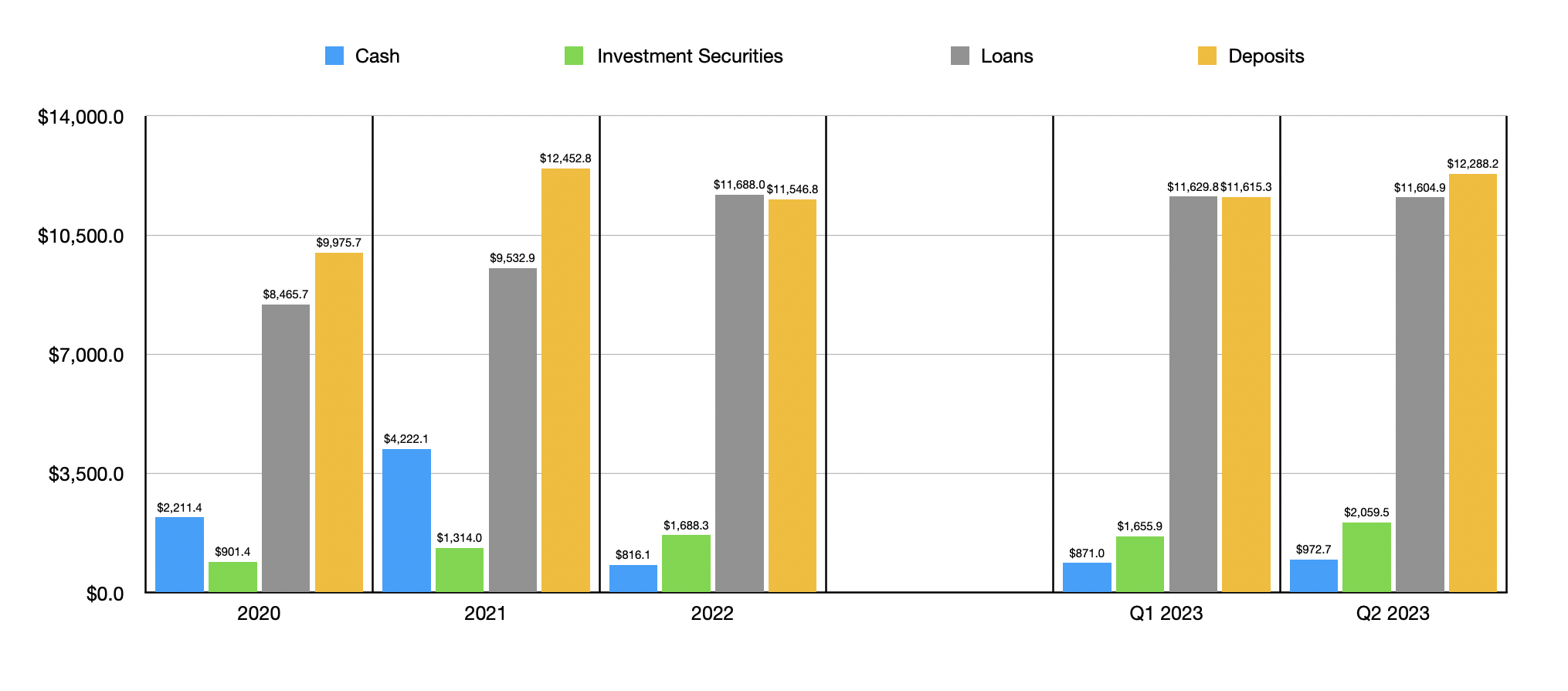

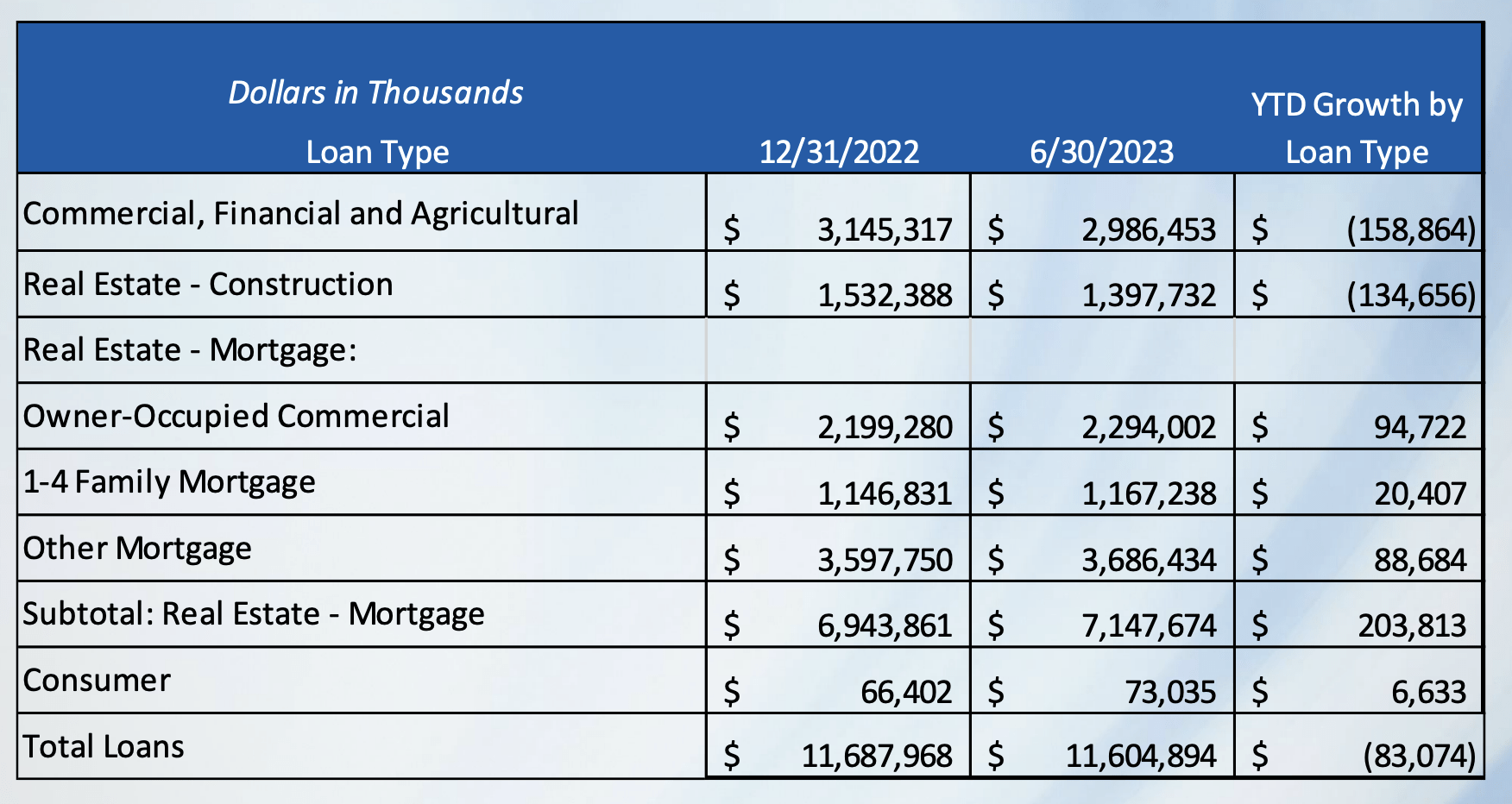

Although the total value of assets for the bank may not have increased much, the value of loans on the company's books definitely has. Loans went from $8.47 billion in 2020 to $11.69 billion in 2022. We have seen a bit of downside since then, with the value of loans dropping to $11.60 billion as of the end of the second quarter this year. A whopping 61.6% of the loans on the company's books fall under the real estate mortgage category. The largest chunk of that would be the ‘other mortgage’ category, at about $3.69 billion, or 31.8%. I understand that one thing that investors are worried about at this time is exposure to office properties. The good news here is that, while office exposure has increased in recent years, it still only comes out to roughly 3.6% of the bank’s loan portfolio.

{kind=link}

Outside of loans, there are other assets that investors should be aware of. Cash and cash equivalents would be one. After peaking at $4.22 billion in 2021, cash quickly plummeted, hitting $816.1 million last year. But since then, it has increased slightly to $977.7 million. Meanwhile, securities that the company owns have increased. These grew from $901.4 million to $1.69 billion over the span of three years. Growth continued into the current fiscal year, with the total value of securities hitting $2.06 billion at the end of the second quarter .

{kind=link}

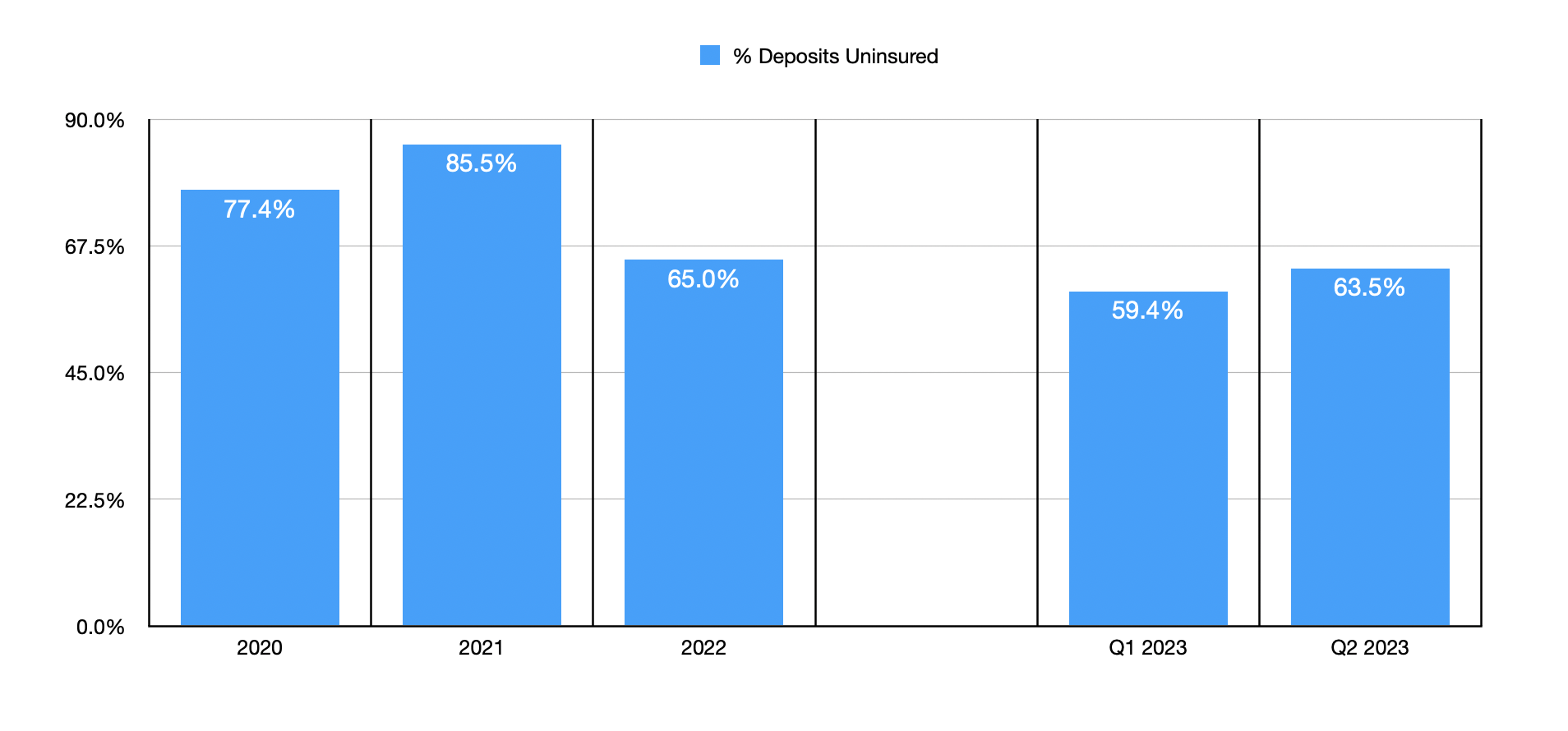

The value of deposits on the company's books has increased, too. Back in 2020, deposits came in at $9.98 billion. We have seen some volatility since then, with deposits hitting $12.45 billion in 2021 before dipping to $11.55 billion last year. They have since rebounded and, as of the end of the second quarter, they totaled $12.29 billion. There is one downside to the deposit picture for the bank, though. And this is that exposure to uninsured deposits is awfully high. At the end of the most recent quarter, 63.5% of the company's deposits were uninsured. While this is down from the 85.5% seen in 2021, it is far higher than what I am comfortable with. Typically, I look for exposure to be 30% or less. After all, it's uninsured deposit exposure that created the banking crisis earlier this year.

It's also important to point out that the company doesn't even seem to have a good idea as to what its uninsured deposit exposure truly is. This is also concerning. In its annual report for 2022, it listed its uninsured deposits at nearly $9 billion. In the first quarter, this figure was revised down to $7 billion. And in the second quarter filing of the company, management revised the 2022 figure up to $7.5 billion. This kind of volatility in estimates is uncommon, to say the least.

{kind=link}

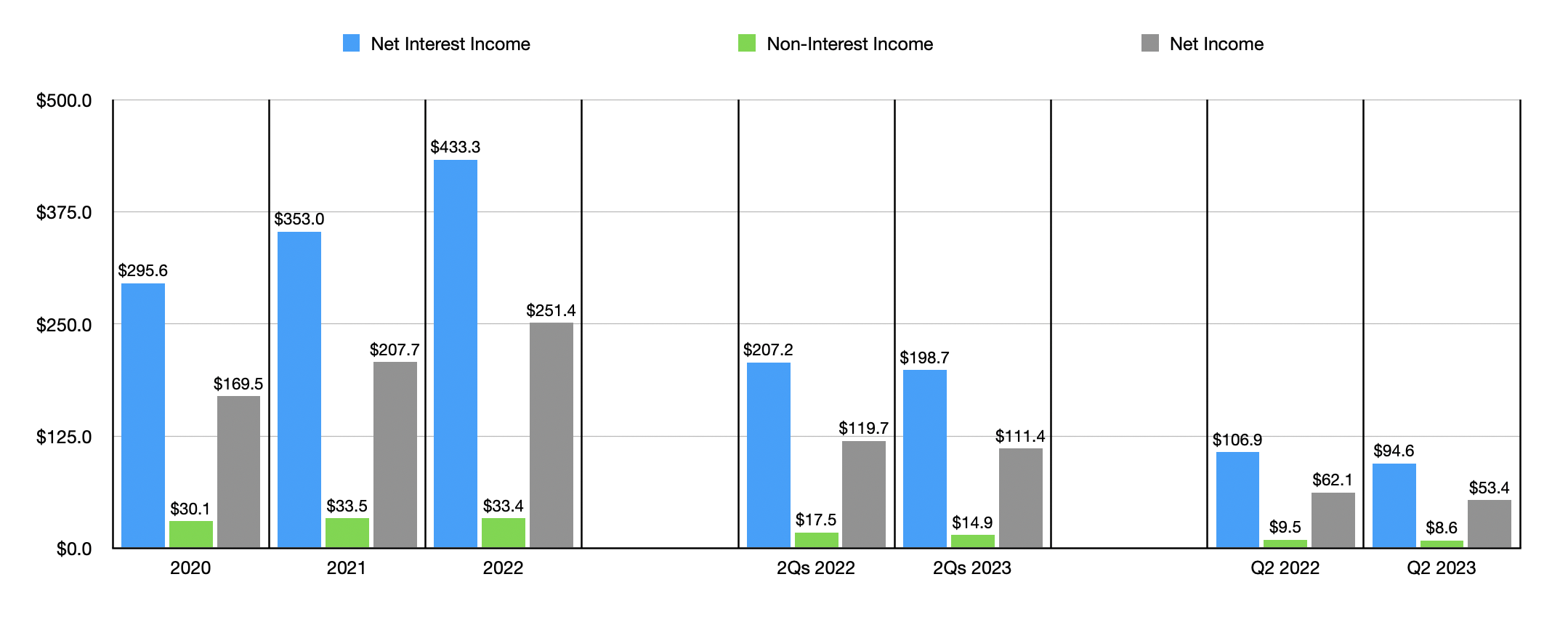

From a revenue and profit perspective, I do have mostly positive things to say about the institution. Net interest income grew from $295.6 million in 2020 to $433.3 million in 2022. Non-interest income inched up from $30.1 million to $33.4 million, while net income expanded from $169.5 million to $251.4 million. But this year, things are looking a bit different. As you can see in the chart above, net interest income, non-interest income, and net income, are all down year over year. Most of this pain was driven by a drop in assets for the company from $15.10 billion to $14.34 billion. However, it did also see a modest drop in its net interest margin.

{kind=link}

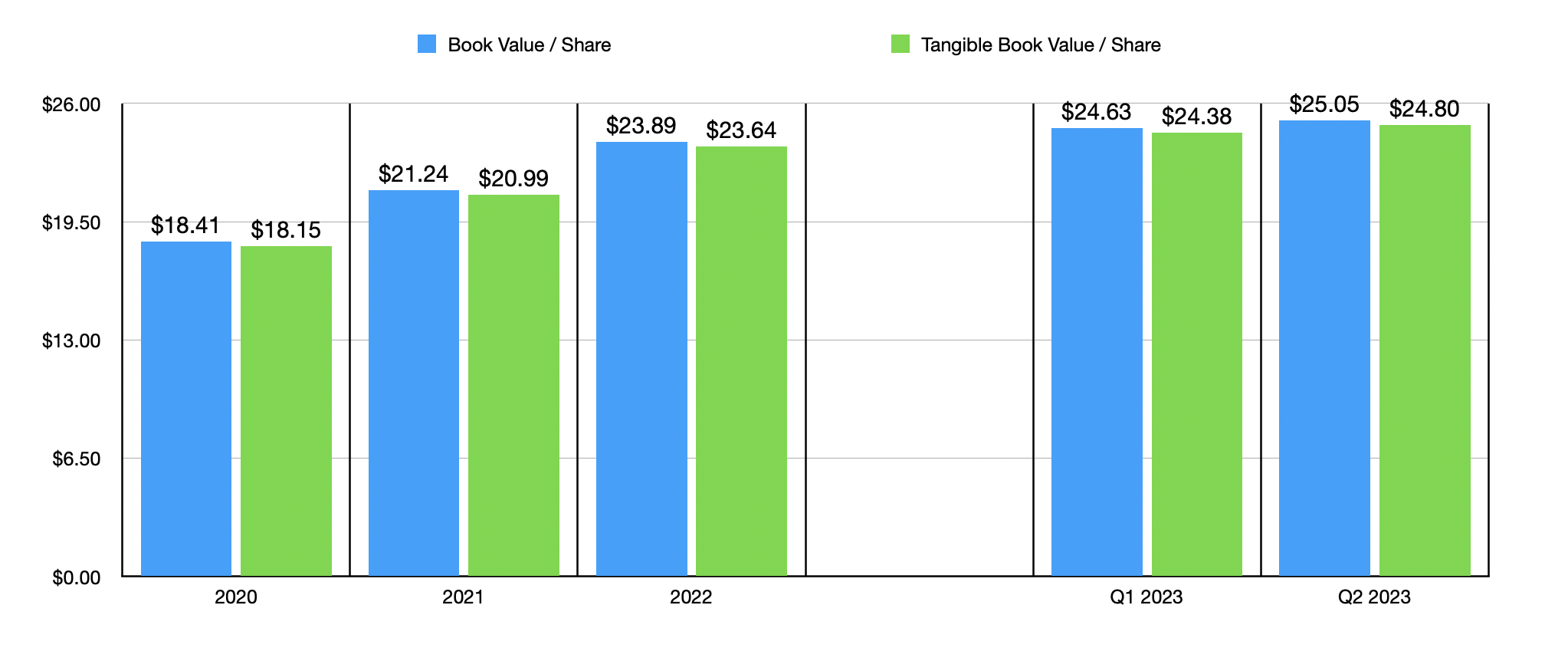

Even though this year is not looking to be the best, the book value per share and the tangible book value per share of the bank have continued to increase. At the end of last year, the firm's book value per share was $23.89. That has since grown to $25.05. Meanwhile, the tangible book value per share has grown from $23.64 to $24.80. This is definitely great to see. However, the bank is trading at 2.08 times its book value and 2.10 times its tangible book value as of this writing. That is quite a bit higher than what I typically see in this space. Meanwhile, using results from last year, the bank's price to earnings ratio is 11.3. I have seen readings higher than this before. But right now, the average in the space is about 10.4, while many of the banks that I have looked at are trading at ranges of between 6 and 9.

Takeaway

At this moment, I recognize that ServisFirst Bancshares is a solid financial institution. However, there's a lot that I don't like about it. I don't like the uninsured deposit exposure. I don't like how pricey shares are, both on a price to book basis and a price to earnings basis. Recent weakness is not unexpected, but it's definitely unwanted. And when you add all of this together, I believe there are better prospects to be had at this time.

For further details see:

ServisFirst Bancshares: Too Lofty For My Money