SGBAF - SES And Viasat: 2 Mergers To Challenge Elon Musk's Starlink

2023-04-06 04:57:25 ET

Summary

- There is a consolidation going on in the satellite communications market as operators have to take on challenges constituted by disruptors, one of which is Starlink.

- Elon Musk's company has surely impressed by its agility, but incumbents Viasat and SES S.A. are also taking action by merging with Inmarsat and Intelsat, respectively.

- While the Viasat-Inmarsat deal is under regulatory scrutiny, there have been intensive talks concerning an SES-Intelsat merger.

- The incumbents' advantage is that they do have government business, and, this is a factor I consider when valuing.

- In addition, there are the device-to-satellite and inflight WiFi markets, but it is also important to be aware of the risks.

The UK’s Competition in Markets Authority has cleared Viasat’s (NASDAQ: VSAT ) acquisition of London-based Inmarsat finding that the deal would not substantially reduce competition for providing WiFi on planes. In response, shares have gained as shown in the orange chart below, and, to a higher degree than Luxembourg-based satellite operator SES S.A. ( OTCPK:SGBAF ) whose merger talks with Intelsat S.A., to create Europe’s largest satellite play has intensified considerably.

This thesis aims to elaborate on the reasons behind consolidation in the satellite communications industry, and how it will help incumbents (traditional service providers) to challenge Elon Musk's Starlink. For this purpose, I will also touch upon the technology side and detail the two emerging markets which are satellite-to-device and inflight WiFi.

The Logic for Consolidation

New features now allow devices, such as Apple's (NASDAQ: AAPL ) iPhone 14 to send messages directly via satellite. Despite being limited in terms of speed, this technology has the advantage of working everywhere, including areas not covered by traditional cellular networks. While this does not necessarily represent a breakthrough as satellite phones have been around for years, this latest innovation in the mobile industry to enable satellite emergency calls, from a mere smartphone (instead of a specialized satellite phone) could eliminate dead zones and complement cellular networks which remain the preferred means of connecting to the internet in locations deprived of WiFi. Noteworthily, Apple has forged a partnership with satellite operator Globalstar ( GSAT ).

Along the same lines, the mobile network operator T-Mobile (NASDAQ: TMUS ) announced an alliance with SpaceX's ( SPACE ) subsidiary Starlink ( STRLK ). Moreover, Samsung (SSNLF) also working on a satellite-enabled Galaxy.

In addition to SpaceX and Globalstar, and as I have covered in my publications, AST SpaceMobile ( ASTS ), EchoStar ( SATS ), Viasat, and Iridium ( IRDM ) are working in the same direction, as well as others like Lynk Global , and Sateliot. Add to these state-backed China Satellite Network Group which may provide services for Huawei's Mate 50 which is already satellite-ready, and you have a market where the aim is not necessarily profitability but longer term objective like rapidly gaining market share, possibly with the support of governments.

At the same time, there are deep-pocketed players like OneWeb ( backed by the British government, Bharti Enterprises, SoftBank ( OTCPK:SFTBY ), Eutelsat ( OTCPK:EUTLF ), or Starlink which may be benefiting from lower capital costs because parent company SpaceX launches satellites.

In these circumstances, in a global economic context no more favored by abundant liquidity since most central banks are tightening monetary policy, the best choice available to incumbents like Viasat and SES S.A. is to consolidate. This is further justified by their net debt exceeding their market cap, signifying that, unlike many tech companies forming part of the Nasdaq, they are far from being cash rich enough to generate organic growth.

Comparison of Key Metrics (www.seekingalpha.com)

As a matter of fact, Viasat is building three satellites at a total cost of over $2 billion this year, with expenses only likely to decrease in 2024, while for CES, it was €950 million in 2022, and expected to come down to €360 million only in 2026.

Detailing Each Potential Merger

Looking at ViaSat's weak cash position above, this should be remedied through the sale of its Link 16 Tactical Data Links business to L3Harris ( LHX ) resulting in cash proceeds of about $1.8 billion net when the deal closes in H1-2023. As a result, the net leverage of the combined Viasat and Inmarsat entity will also be reduced, with the company now expecting to be free cash flow positive, after the $7.3 billion acquisition.

Additionally, with an estimated $1.4 billion of synergies and $4.1 billion of revenues (figure below), the merger would create a $8.3 billion entity with 19 satellites in service and 10 under construction.

{kind=link}

ViaSat-Inmarsat Merger details (investors.viasat.com)

As for the SES-Intelsat merger, according to Bloomberg, if the transaction were carried out, it would give birth to a group valued at $10 billion .

Moreover, SES's revenues for 2022 amounted to $2 billion with over 70 satellites circling the globe both in GEO (Geostationary Earth orbit) and MEO ( medium Earth orbit). As for Intelsat, revenues peaked at $526.1 million in 2021. For recall, the company emerged from bankruptcy as a private company in 2022, after being restructured and reducing its debt to $7 billion from about $16 billion. The company has a fleet of over 50 satellites, with the table detailing the key metrics for a potential SES-Intelsat merger.

| Combined SES-Intelsat Metrics |

| Details |

| 1 |

| Market Value |

| $10 billion |

| 2 |

| Combined Revenues |

| $2.5 billion |

| 3 |

| Total number of satellites |

| 120 |

| 4 |

| Orbits |

| GEO and MEO |

Thus, with over 120 satellites located both in GEO and MEO, the combined entity will have much larger coverage compared to only 19 satellites for Viasat-Inmarsat, which, on top are only in GEO. By comparison, the Starlink fleet consists of over 3,580 small satellites in LEO or Low Earth Orbit.

Now, it is not only a matter of having more satellites here, as GEO satellites cover relatively larger geographical areas, with only three of them being needed to cover Earth. In the same way, fewer MEO satellites are required to cover an area compared to LEO. Furthermore, being located nearer to the earth, LEO satellites provide lower latency for communications purposes, but they have to move faster and cover much wider distances compared to those in higher altitudes, making their lifetime shorter. Also, in a sense, they are less efficient as they traverse unpopulated areas like oceans, deserts, and forests where there are few subscribers.

Therefore, there are many dynamics at play here including ground-based stations, and relays whereby GEO and LEO satellites can work together, and while it may appear that traditional players may have been outpaced by Starlink with its disruptive technology and agile business model, the merger initiatives indicate that they are not sitting idle. Looking deeper, consolidation is also indicative of the upheavals that are shaking the space sector, as SES and Intelsat are among the main incumbent satellite operators, faced with a declining TV broadcasting channel market, as fiber-to-the-home has expanded its reach globally.

Consequently, it is crucial to adjust the strategy to switch to the more lucrative satellite-to-device internet connectivity and in-flight WiFi services markets.

Valuing the Two Stocks In Light of Consolidation

Interestingly, the Apple-initiated satellite-to-device market which did not have any subscribers last year should see this number increase anywhere from 25 million to 330 million by 2030, implying millions of dollars in revenues.

Then there is the booming market constituted by the in-flight WiFi services where the industry key players Inmarsat, Intelsat, SES, Viasat, and Eutelsat already play a key role, but new entrants such as Starlink and SmartSky are starting to make their presence felt. Valued at $7.79 billion in 2022, this market should reach $8.77 billion by the end of this year.

Initially reserved for business class, but democratized to others in the cockpit as a result of people becoming addicted to their smartphones for surfing the internet, answering emails, or watching a streaming film, inflight WiFi should gradually become a reality for all passengers as airlines invest money to equip their planes with specialized modems which can communicate with satellites.

Thus, having at their disposal two markets and with more scale, the two stocks should be valued accordingly.

In this respect, Starlink which has recently exceeded the 1 million users mark and is now free cash flow positive , has to rely on retail consumers or subscribers like you and me. In contrast, in addition to catering to individuals, the incumbents Viasat and SES have government-related businesses on which they can rely for a stable income stream, while potentially growing through M&A. This is one of the reasons that they remain investible despite Starlink's rapid growth and OneWeb's positioning.

Furthermore, in case Starlink goes public as I will detail below, the two companies are likely to garner more public attention, in the same way as Silicon Valley IT companies. In this case, their forward price-to-sales metrics are both undervalued with respect to the IT sector's 2.7x .

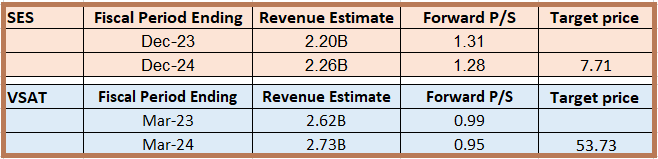

Adjusting for a P/S of 1.5x for both, I obtain a target of $7.7 (6.58 x 1.5/1.28) for SES based on its share price of $6.58, and applying the same formula to Viasat, I come up with $53.73 (34.03 x 1.5/0.95) based on its stock value of $34.03.

{kind=link}

Table prepared using data from (www.seekingalpha.com)

I have chosen a P/S of 1.5x for both as firstly, Viasat is closer to a merger whereas SES is at the discussion stage and deserves to be better valued. This is the reason, I have applied a higher multiple of 58% to its share price compared to only 17% for SES since it already carries a higher valuation despite its slower revenue growth. This said I have not assigned a higher valuation to Viasat, as it will see its revenues decline by approximately $400 million for fiscal 2024 due to the sales of the Link 16 TDL business.

Concluding with Caution

This thesis has shown that by merging operations, incumbents can add to existing capacity in order to support new market verticals while spending relatively less Capex as in both cases the total number of satellites is higher. Scaling up is also viewed as a solution to better compete with Starlink.

This said some may prefer to wait for Viasat to execute its combination with Inmarsat and for the talks between SES and Intelsat to materialize into a deal before investing. In addition, satellite operators depend on suppliers and rocket launchers which means that there can be delays in adding capacity. This may cause the stock to be volatile.

Therefore, this is not an investment without risks, and another strategy is to wait for Starlink's IPO given that Elon Musk may be needing money after acquiring Twitter and having to refund creditors as the tight monetary policy dries up liquidity from the system. Finally, unlocking value through consolidation is pretty much on the agenda, namely with Eutelsat planning to merge with OneWeb as it expands from higher altitude to lower orbit satellites.

For further details see:

SES And Viasat: 2 Mergers To Challenge Elon Musk's Starlink