AMKAF - SFL Corporation: A Preview Of Q2 Earnings

- Earnings and cash generation are fairly stable for SFL with their $3.6 billion backlog.

- 73 consecutive quarters of dividend solidifies SFL's track record of giving back money to shareholders.

- Fairly high leverage might see higher interest costs for SFL going forward.

- Management will continue to proactively recycle capital and take advantage of opportunities to buy and sell assets.

SFL logo ((SFL))

Investment thesis

In March this year, I concluded that despite a 20% rise in share price, SFL Corporation Ltd. ( SFL ) still offered investors good value

At that time, the share was worth USD $9.96 and is now trading at about the same level.

However, SFL will soon come out with their Q2 financial results, and we will consider aspects that could influence their earnings going forward.

Financial Commentary

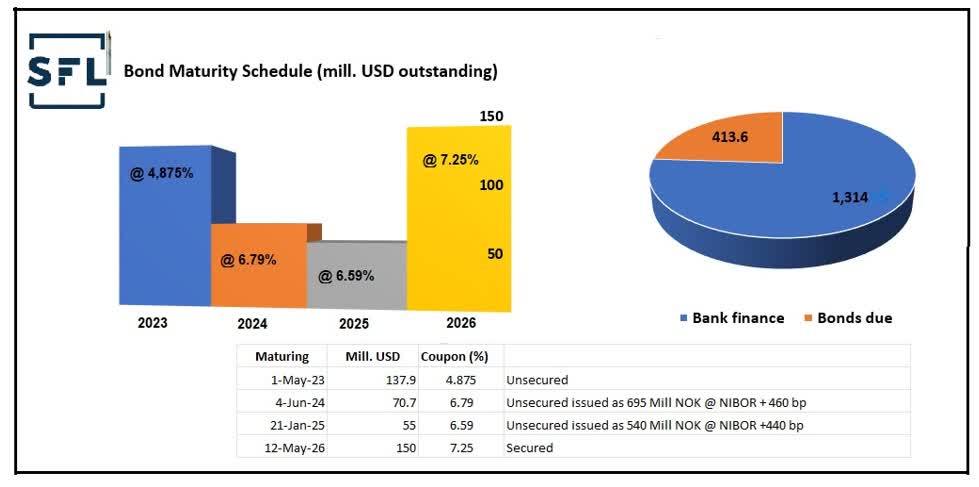

One question I do ask myself is if servicing their debt in a rising interest rate environment will impact SLF's earnings much.

The average interest rate cost of their financing is 5.23%

For every 1% increase in interest costs to the company, the earnings reduce by USD $17.3 million

The effect of these changes might be lower as the company does extensively use interest rate swaps and other derivative instruments that they enter into.

Here is a profile of the debt.

{kind=link}

From my experience, the bank financing is done on a ship-by-ship basis as each ship is mostly owned in a separate company established for the only purpose of ownership of that particular ship. This comes in the form of a mortgage, much like what you may have on your house, where the bank has collateral in the asset.

Initially, we will not see much change in their interest costs, but it is worth monitoring as their bank debt is considerably larger than bonds with fixed coupons.

The remaining Capex is approximately USD $240 million on the 4 LNG-powered car carriers which are under construction. Two of them should be delivered to SFL in Q2 and Q3 of next year commencing 10-year charters at about USD $27,800/day to Volkswagen Group. The other 2 ships will come in 2024 and will go on charter to NYK. SFL plan to finance the balance payments through senior financing.

Business development

- Container vessels

With 53% of EBITDA coming from the liner companies, it is clearly the most important segment for the company. The weighted average charter term of the container ships is as much as 7.3 years and its backlog is now USD $2 billion.

Therefore, the spot market for containerships is not crucial. None of their container ships are coming off charter this year or next year. The earliest is in 2024 when as many as 10 ships are coming off charter.

Presently, the freight rates for container transportation remain at historically high levels. This, combined with restrictions on the movement of people in China from the pandemic, will continue to make it challenging for all supply chain logistics. Trade experts believe that freight rates will remain high at least up to the middle of 2023.

A.P. Møller - Mærsk A/S ( AMKAF ), which is SFL's largest customer contributing 32% of the revenue in 2021, has just come out with their Q2 results . They are doing exceptionally well, delivering strong results driven by the continuation of the exceptional market situation with congestion in global supply chains leading to higher freight rates.

It has continued longer than they had initially anticipated. Consequently, they upgraded their full-year guidance for 2022 of achieving free cash flow for the full-year 2022 to above USD $24 billion. It was guided previously to be above USD $19 billion.

Good times should continue in this sector.

- Bulk (dry and wet)

Golden Ocean Group ( GOGL ), which is now the only Fredriksen-controlled company on their list of customers, is doing very well, although the spot market for large dry bulk has come off on fear of a reduction in iron ore shipments.

The eight Capesize ships will keep earning good money for SFL, but I do not foresee much profit sharing at this moment from these vessels.

Apart from these Capesize ships and one Kamsar max on charter to Sinochart, they own 5 Supramax vessels trading in the spot market.

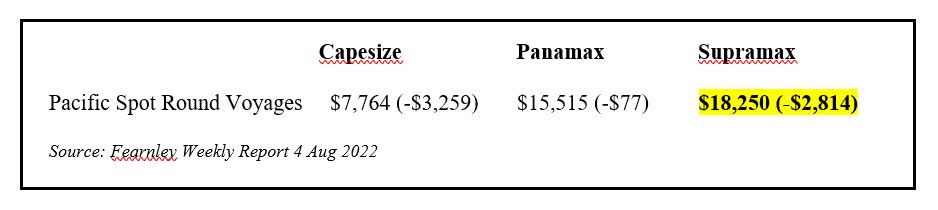

The spot market for dry bulk took a beating last week. Nevertheless, the freight market for these Supramax vessels has held up well in comparison to the larger Capesize ships.

Supramax vessels trump the spot market (Data from Fearnley, graph by author)

{kind=link}

SFL's Supramax vessels generated approximately $8.0 million in net charter hire during Q1 this year.

It could be tempting to take the opportunity to sell the vessels now that the market is good.

{kind=link}

These five Supramax vessels are built at Xiamen Shipyard in China and delivered to SFL between 2009 and 2012.

I would estimate the market value for these vessels to be between USD $17 million and USD $19 million per vessel, based on the fact that the last transactions of similar vessels and age. On the 30th of July, shipbrokers reported that "Theresa Oetker" 58,018 deadweights built in China in 2010 changed hands at USD $17.2 million.

However, there is one problem with this, and that is the fact that these vessels were valued in SFL's books as of the end of 2021 at USD $103 million, which they rightfully estimated in their annual report to be about USD $18 million higher than charter free market prices.

Therefore, SFL will most likely continue to enjoy the high earnings they get before a sale would take place.

When it comes to its tankers, its fleet is on period charter so there is little change to earnings. The only exceptions are two older Suezmax vessels that trade in the spot market.

In Q1 those two ships generated a net charter income of USD $2.3 million. I expect this will remain the same, or slightly higher.

There is optimism in the tanker market which is reflected in higher prices for vessels.

Although the older VLCC has now been sold, SFL still has great ties to Frontline ( FRO ). That could bring in new deals in the future.

Frontline is doing what they have done since it started, namely merging or just acquiring other companies. The merger between Frontline and Euronav ( EURN ) will now go ahead, and there could be some new opportunities in the future for long-term charters with Frontline which will soon control a large fleet of 136 vessels.

- Offshore assets

SFL is no longer tied to the future of Seadrill (SDRLF), although that might not be as bad as some think, as Seadrill basically converted most of its debt into equity and is now a lot stronger financially. Although with a lot of new shares issued.

SFL will be looking at what kind of time charter earnings they can get for the Harsh Environment semi-sub drilling rig "West Hercules" after its special survey which will be done early next year.

West Hercules ((SFL))

The rig is presently only earning USD $60,000 per day on bareboat. But positive market development for these Harsh Environment rigs operating in the Norwegian sector has charterers paying over USD $300,000 for such rigs on time charter.

After discussing with fellow author Henrik Alex, who is doing an excellent job in covering some of the offshore drilling companies, such as Transocean (RIG), where he recently came out with a strong buy call, we can estimate the new potential bareboat rate.

We can look at the costs of Opex from Oddfjell Drilling's fleet as a guide as to what the operating costs per day will be, as they will also manage the rig for SFL.

From this, I would estimate that the daily Opex for "West Hercules" to be in the range of USD $150,000 to USD $175,000 per day.

Since the time charter rate is basically the bareboat rate plus the Opex, we should get a bareboat rate of approximately USD $125,000 to USD $150,000 per day, which is much better than what they are earning now. This will only start next year and not influence the next two quarters, but it is good to know that shareholders can hope for an improved contribution from this asset next year onwards. I was positive about these assets back in September last year.

It would be useful if can get some guidance from SFL as to the estimated cost of the special survey.

With regards to the other rig, "West Linus," it is on charter up to the end of 2028 under an indexed linked market rate adjusted twice a year. The prospects for more drilling under this program are quite good as the Ministry of Petroleum and Energy of Norway has extended production licenses for the Ekofisk from 2028 to 2048.

With less oil and gas flowing from Russia to the continent, the EU is putting pressure on Norway to fill some of this gap.

Expectations for Q2 results and my conclusion

SFL's Q2 results are expected to come out on August 18 before the market open.

I think Q2 of 2022 will be in line with the previous quarter. There might be some small changes due to the profit-sharing portion from fuel savings and from potentially higher earnings above threshold rates on some of the vessels.

The Capesize vessels on charter to Golden Ocean only generated USD $100,000 in profit sharing and with the lower market, I do not expect any profit sharing from them in Q2.

If we look at the spread in fuel costs, it is now wider than what it was earlier this year.

Fuel spread - Fearnley Weekly Report 4 Aug 2022 (Fearnley Weekly Report 4 Aug 2022)

{kind=link}

In Q1, the liner ships generated USD $4.4 million of profit share from fuel savings, so it could be somewhat higher in Q2.

The sale of vessels, such as the 1,700 TEU container vessel "MSC Alice" should record a gain of about USD $2 million in Q2 plus another USD $2 million on the sale of the two old VLCCs.

EPS was USD $0.37 in Q1 this year and it is hard to predict what the EPS in Q2 will be as accounting figures often have impairments and adjustments that do not affect movements in the cash flow.

The dividend bumped up by 10% in Q1 so it will most likely stay unchanged, in my opinion.

SFL still presents good value and my Buy stance remains intact.

For further details see:

SFL Corporation: A Preview Of Q2 Earnings