VTI - Shades Of 2007

2023-08-15 11:37:01 ET

Summary

- Signs of a major economic contraction were present in 2007, with the housing market under duress and the Federal Reserve having raised interest rates significantly.

- Few anticipated the contagion risks in the residential real estate market, leading to a meltdown in equities and the worst economic crisis since the Great Depression.

- A similar situation could be developing in commercial real estate, raising concerns of a new crisis that could trigger a recession and a bear market for equities.

- How this scenario could play out and how I am hedging my portfolio for this possibility are discussed below.

Maybe history wouldn't have to repeat itself if we listened once in awhile .”? Wynne McLaughlin.

In hindsight, in 2007 there were plenty of signs that a major economic contraction was on the horizon. The economy was just starting to feel the full impacts of Federal Reserve's monetary tightening that took the Fed Funds rate from one percent in June of 2004 all the way up to 5.25% by June of 2006. Parts of the housing market, especially sub-prime, was under considerable duress.

Investors were also anticipating a " pivot" from the central bank, which occurred in September of 2007 amidst assurances that the subprime crisis was contained one month earlier, and that the larger economy would skirt a recession. Sound familiar? Few imagined the risks contained in the residential real estate market or their downstream impacts on the financial system, the markets, and the economy. The result was a meltdown in equities and the worst financial crisis since the Great Depression.

As Mark Twain famously quipped, " History doesn't repeat itself, but it does rhyme, " and a situation is developing in commercial real estate that certainly seems to have shades of 2007. Could this develop into a new real estate crisis that tips the economy into a recession and brings on the next bear market for equities?

I have written recently about the collapsing values in some sectors of real estate, especially office properties in major cities.

As much as 40 percent of the core of retail and office corridors in the nation's cities could be rendered obsolete. An estimated $800 billion worth of real estate could be wiped out ."

The headline above I noted in that article was from a recent McKinsey & Co. report that I believe got way too little attention in the financial press and is still being discounted by investors in my opinion.

In the subprime crisis of some 15 years ago, mistakes were made that look lubricious in hindsight. Banks lowered their credit criteria for mortgage loans and gave mortgages to individuals with little to no money down, and in some cases, without basic income verification. These banks believed they would be insulated from credit risk by packaging these loans and then selling them in the credit markets via securitization.

Many homeowners also took out loans they could not afford as they believed they could " flip" them quickly for a profit in a housing market that had done nothing but go higher for years. Investors believed assurances from the Fed and the talking heads on CNBC who said the big spike in delinquency rates in subprime would not significantly impact other areas of the financial system, not fully understanding the counterparty, derivative or contagion risks. Investors largely chose to not take prudent actions to hedge their portfolios until it was too late.

Deja vu all over again? Commercial real estate owners, especially on but not limited to office properties, appear to have made two huge mistakes in hindsight. First, they did not fully factor in how technology was enabling more and more people to effectively work from home and how in time that would diminish the need for office space. To be fair, this emerging trend was turbo charged during the pandemic, an outbreak that resulted in global wide lock downs that few could predict.

The massive expansion of the virtual workforce that was triggered by this event over the past few years has resulted in a huge increase in the office vacancy rates in cities like Chicago , New York , and San Francisco . Office vacancy rates in most major cities sits at north of 20% and are at record highs in places like Los Angeles . This will only get worse as leases expired and corporations and companies continue to shrink their commercial real estate footprint.

The second mistake many commercial real estate property owners made across all real estate categories was assuming that the ultra-low interest rate environment of the past decade in a half would remain in place for the foreseeable future. This is important because loans on commercial real estate loans don't run 30 years like on most residential mortgages. They typically are of a duration of five to seven years, with construction loans typically running two to three years.

Commercial real estate or CRE loans that typically carried interest rates in the four to six percent range now will need to be rolled over at twice those rates thanks to most aggressive monetary policy by the Federal Reserve since the days of Paul Volcker. This has resulted in a 525bps hike in the Fed Funds rate since March of last year and we may or may not be on pause right now for future rate hikes.

Given many office and some other properties are selling or have a realistic appraisal at 60 cents on the dollar or worse in many major cities, this leaves many CRE owners " under water" with no equity left in their underlying collateral. When debt maturities come due, many will do the same thing so many homeowners did in the financial crisis, just walk away and turn in the keys. This will put additional pressure on CRE values.

The $64,000 question for investors is how much contagion this will introduce to the broader markets and economy. The most obvious impacts are to the regional banks given they originate approximately 70% of CRE loans in the country. Default rates for commercial backed mortgage securities or CMBS on office holdings hit five percent in July according to Trepp. This is up from just 1.6% at the start of the year and 2.8% in April. Overall CMBS default rates rose 51bps in July from June on all CMBS.

Increasing delinquency and write-off rates will force the regional banking system to implement even more stringent credit criteria, which could trigger a " credit crunch" in some parts of the economy such as small business which relies heavily on regional banks for credit facilities.

Moody's recently downgraded its credit ratings across multiple regional banks. Fitch just warned it may have to put downgrades on dozens of banks if conditions continue to deteriorate, after recently downgrading its rating on U.S. sovereign debt.

The country experienced the second, third, and fourth largest bank bankruptcies in U.S. history earlier this year. This was largely due to duration risk on these banks bond portfolios, which still is a headwind to a good portion of the banking system. Add in worsening default and write off rates, and there seems a good possibility that additional banks will eventually share the fate of Silicon Valley, Signature and First Republic Banks.

{kind=link}

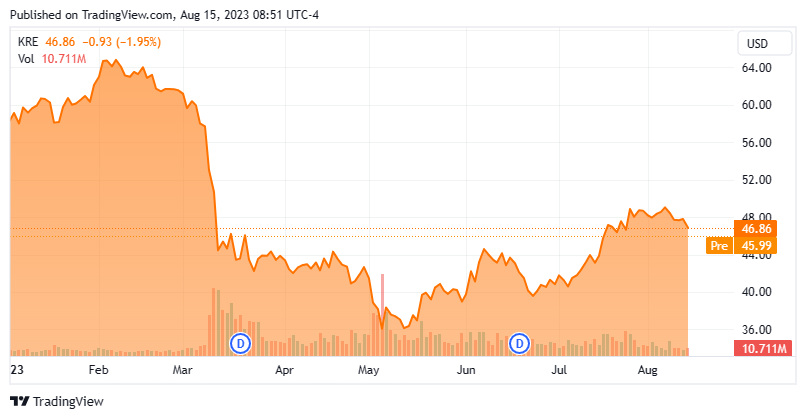

I have spent the last month or two establishing a decent position of long dated bear put spreads against the SPDR® S&P Regional Banking ETF ( KRE ), as I think regional banks will retest their lows hit earlier this year in the aftermath of previous bank failures.

I have also been building a decent size bear put spread position in both the SPDR® S&P 500 ETF Trust ( SPY ) and the Invesco QQQ Trust ETF ( QQQ ). Volatility and option premiums are both quite low to implement this risk mitigation strategy.

This echoes a strategy (on a much smaller scale, of course) of " Big Short " hedge fund manager Dr. Michael Burry. He is known for accurately predicting the subprime mortgage crisis and making a fortune doing so. Much like Dr. Burry, I see " Shades of 2007" and plan to profit if volatility and the potential for contagion rise in the months ahead. More importantly, this is a nice hedge against the rest of my portfolio which consists of approximately 50% of short-term treasuries and 40% to 45% in covered call holdings.

The problem with the idea that history repeats itself is that when it isn't making us wiser it's making us complacent .”? Lisa Halliday.

For further details see:

Shades Of 2007