TDOC - Sharecare: Cheap For A Reason

2023-03-24 04:08:13 ET

Summary

- Sharecare is an American Digital Health platform started by the founder of WebMD.

- Sharecare has the potential to excel in healthcare due to its capabilities in AI.

- Yet, Sharecare operates in a very competitive field and is smaller than telehealth companies like Teladoc.

- Sharecare's healthcare content strategy is unique and may provide shareholders with significant cash flows in the coming years.

Sharecare ( SHCR ) is an American digital healthcare platform that was listed on the stock market through a reverse merger with a SPAC entity. The CEO and co-founder, Jeff Arnold, founded WebMD, a human health and well-being website.

Overview

The digital healthcare platform provides various products, including Population Risk Stratification, benefits navigation and healthcare navigation, medical records services, mindfulness/wellbeing programs, remote patient monitoring and telehealth, amongst many others.

One of the key components of Sharecare's business model is its focus on personalization. Another key aspect of Sharecare's business model is its focus on data and analytics. By leveraging the vast amounts of data generated by its users, the company is able to gain valuable insights into health trends and behaviors. This data can then be used to improve the platform's offerings and inform healthcare providers and policymakers.

Essentially Sharecare provides a platform to monitor all personal health in one place. Sharecare's clients include customers, enterprises but also providers.

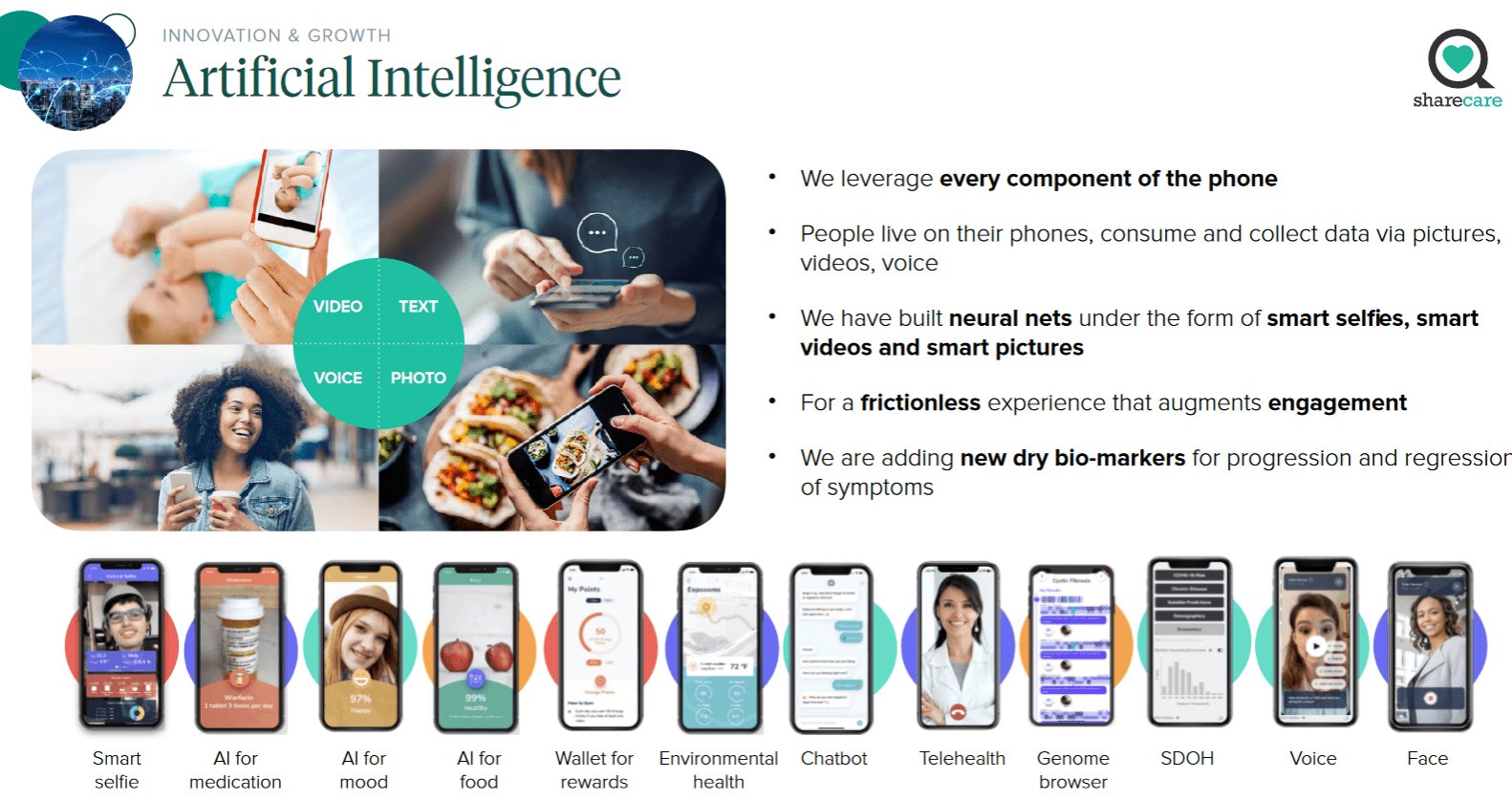

AI

While Sharecare boasts significant AI capabilities in its company, some of its consumer health data is mainly derived from the manual input of its users and not actual tests. While this is a hassle for people to fill in, it also leads to significant quality issues for any AI or Data Science capabilities on the platform. Other data on the platform are mainly derived from medical records and devices - probably more valuable for training AI models.

The acquisition of Palo Alto-based Doc.AI has made Sharecare's position in the AI space more legitimate.

A successful AI strategy is necessary for Sharecare's stock to experience significant returns: turning its data into advanced health insights. It seems like the best approach to differentiate from the competition and leverage its existing data and positions in the healthcare market.

But it is one thing to have capabilities. Another is to turn them into value for the shareholder and the end-client.

{kind=link}

Content

A less talked about but very vital part of Sharecare's strategy is its vast health content. It seems that content is a big money maker and engagement driver on the platform. The success and traction in this niche are obviously related to the co-founder's history at WebMD. I can see the benefits of a digital health platform providing users with high-quality health content. Sharecare has 265K pieces of health content that are NCQA accredited.

Content on the platform is very useful for users in learning how to manage their health and well-being. The content is so popular that pharmaceuticals want to pay for content:

And what's nice about Sharecare is we generate approximately $80 million a year off our content. So we get hired by pharmaceutical companies, and they come to us and say, how do we -- can we access your 115 million member database? And can you help us activate people say that might have fiber myalgia to look at your award-winning content and go to their doctor and have a conversation with them. And so that part of our business underwrites all our content development, which then we turn around and fuel our enterprise experience. So that's how we create this really personalized experience." ~Sharecare CEO during JP Morgan Healthcare Conference

How do media companies make money? By being able to distribute content to lots of users, the cost of content decreases. It's a game of scale. Healthcare content is probably quite expensive as it has to be verified for correctness. But Sharecare has a lot of content creators who make content for free. And Sharecare has life sciences paying Sharecare to make content for its enterprise clients. It is logical to speculate that this part of Sharecare is very profitable.

Sharecare can match people with relevant content as it has enough knowledge about their medical needs and status. This lowers the price of content significantly and makes it so that Sharecare can profitably distribute high-quality content at a low price.

But.

Telehealth

Sharecare has, in recent years, expanded the offering of telehealth services to its users. I note Teladoc, Amwell, and Included Health, amongst multiple others, are far more scaled in telehealth.

I find that expansion worrisome as I am very uncertain whether Sharecare can profitably expand further in the telehealth niche.

Logically large telehealth firms can also provide health content like Sharecare. They can distribute this content to much more users. I think Sharecare has to expand its telehealth capabilities to remain relevant in the competitive landscape; it is the only way to compete with the telehealth companies that want to do everything healthcare related for the employer.

And if we think about it. Sharecare's content strategy seems to be a significant cash cow which will obviously attract competition with scale trying to imitate that.

Maybe Sharecare can differentiate itself from the telehealth industry. But I am very hesitant about that.

Telehealth companies are a significant risk to Sharecare's story.

Recession

With inflation significantly on the rise, economic growth slowing down and more focus on profitability and cash flow generation at companies -- the environment for Sharecare has worsened. Equity Research Analysts are estimating revenue growth rates in the double digits from 2022; I find this very optimistic I will not be surprised when Sharecare sets negative or low growth rates in the coming years.

Let's look at the history.

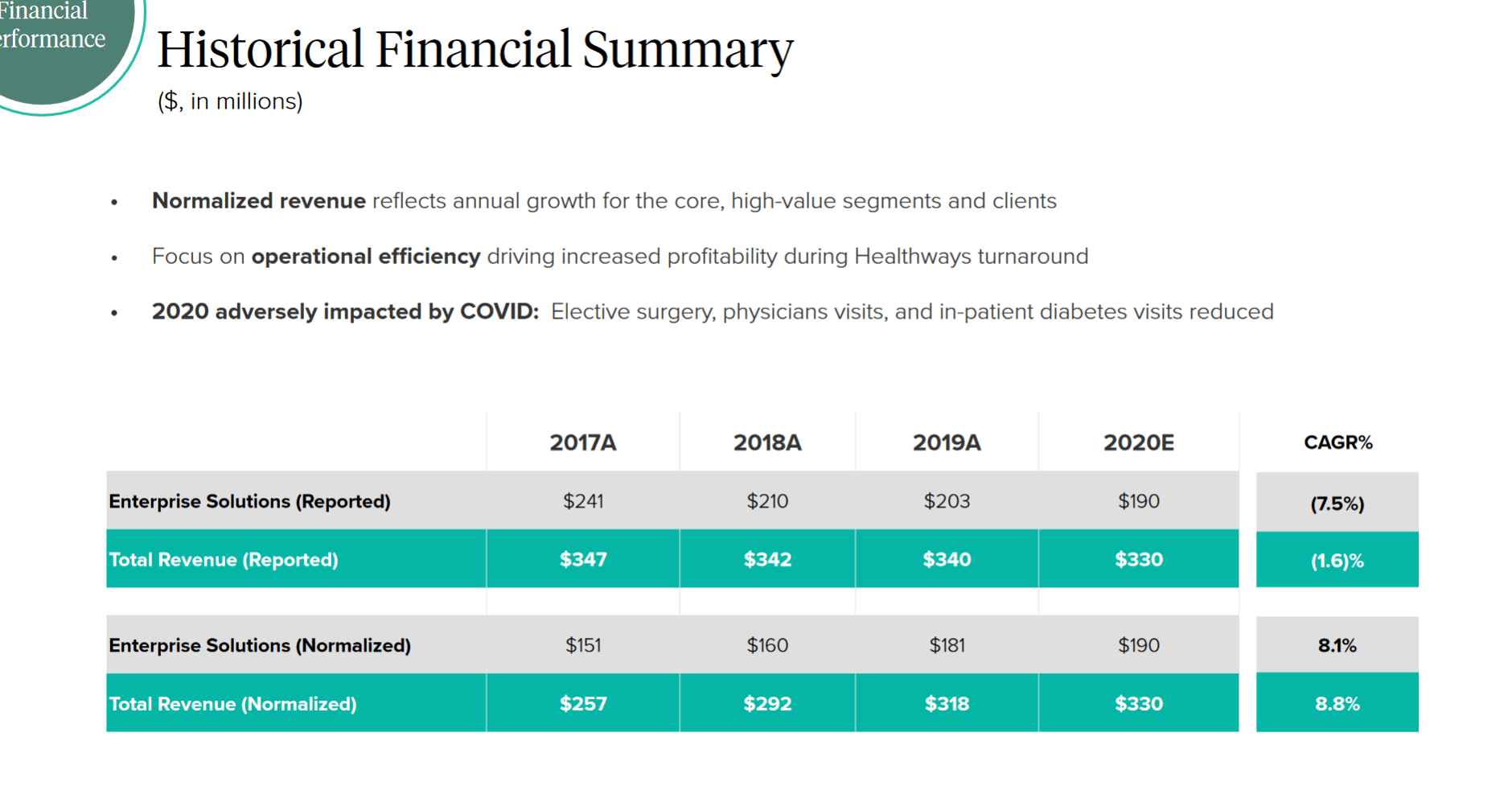

There was negative revenue growth from 2017 to 2020 -- resulting in a CAGR of -1.6%.

Even their normalized growth in the same time period - however that is calculated - was 8.8% CAGR.

Compare that to Teladoc Health ( TDOC ): which grew at much higher percentage rates while being much more scaled. In terms of absolute growth, Teladoc dwarfs Sharecare. Reality.

Also compare to that to Hims & Hers Health ( HIMS ) - whose growth this year is unparalleled with 94% YoY. That's traction.

If scale means anything in this industry -- and I think it does -- this does not bode well for Sharecare. It is logical that Sharecare sells at a significantly lower revenue multiple than Teladoc and Hims and Hers Health.

My problem is that Sharecare has so many different vehicles that can drive growth it is difficult to gauge the company's strength in each. That can be a surprise factor.

{kind=link}

Valuation

Sharecare has $202 million in cash and cash equivalents and no debt but $58 in preferred stock. With a market cap of $809 million, the EV is $547 million. Revenue for the last twelve months is $437 million implying Sharecare is selling at 1.25 times EV/Revenue while Teladoc Health sells at 1.94 and Hims and Hers Health at 3.5.

In the last twelve months, cash burn was at $123 million, and free cash flow was -$66 million. Liquidity can be problematic, and an equity or bond raise can happen in the coming years if cash burn continues.

Yet analysts are estimating EBITDA margins to expand to 7.8% by 2024.

At the current revenue multiple, that implies 13 EV/EBITDA. A cheap valuation for a company positioned in a market with significant secular growth trends.

With low capex that EBITDA should imply a positive cash flow.

I think the valuation is appealing. But I am uncertain about the sustainability of its competitive position -- so I do not find the valuation buy worthy as of writing.

Takeaway

Sharecare has an intriguing plan to digitize healthcare and improve people's lives. But I find that the company's solutions are all over the place while the company seems subscale compared to the major telehealth players. Content and AI seems like the most legit way to differentiate itself from the competition, yet I am not convinced about that investment case so I put a neutral rating on the stock.

For further details see:

Sharecare: Cheap For A Reason