SFT - Shift Technologies: Cheap For Good Reason

2023-03-26 04:51:47 ET

Summary

- Shift Technologies is in the middle of a strategy pivot while staring down significantly decreased revenues.

- It is facing an uphill battle on gross margin as used car prices have continued to decline, and this shrank to less than 1% in the most recent quarter.

- Being neither profitable nor cash flow generative, Shift is in a tough place at the moment - and its price reflects that.

- If management can move the needle on certain core variables, there could be something here - but there isn't just yet.

Overview

Shift Technologies ( SFT ) is an online car retailer akin to Carvana. Founded in 2013, the company has grown throughout the previous decade and first entered the public markets via SPAC merger in Q4 2020. The company’s business model is similar to Carvana’s although different in one important aspect: it does not provide direct to consumer financing. Instead, Shift offers auto loans through its lender network. This keeps the balance sheet of the firm much lighter and as such can be considered more of an auto retailing ‘pure play’ without the financing component.

{kind=link}

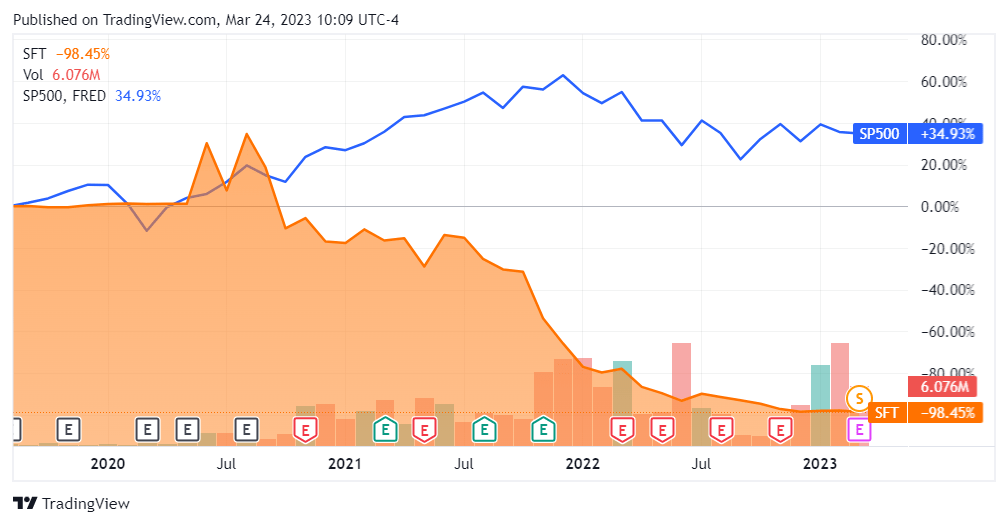

Shift Technologies has depreciated significantly since entering the public markets, underperforming the S&P500 Index roughly 3-to-1. Note the numbers in the chart reflect its recent 10-1 reverse stock split; while it traded in the $10-$11 range during its public debut, this number shows up as $100 given the mathematics around the reverse split. Having been a penny stock, the firm had to reverse split its shares in order to maintain listing requirements on the NASDAQ (at least $1 share price to stay listed). As of this article, its shares are trading at $1.53.

{kind=link}

While the used auto market has indeed faced significant turmoil over the last year, this stock is certainly sold off and may present an opportunity. This article will review the company’s financials and present valuation in order to determine if this is the case.

Financials

First off, we must note that Shift Technologies is a growth company that is not yet profitable. Indeed, the firm has posted what appears to be an accelerating net loss, with the latest quarter being the largest loss yet seen.

{kind=link}

Against this backdrop we can see that revenues have also been quite volatile. While posting significant growth for most of the last 10 quarters, Shift saw its most recent quarterly revenue number decline to a level last seen in Q2 of 2021.

{kind=link}

Throughout this period the company has been squeaking out a thin gross profit, notably keeping this number positive in the wake of recent difficulties within its operating market.

{kind=link}

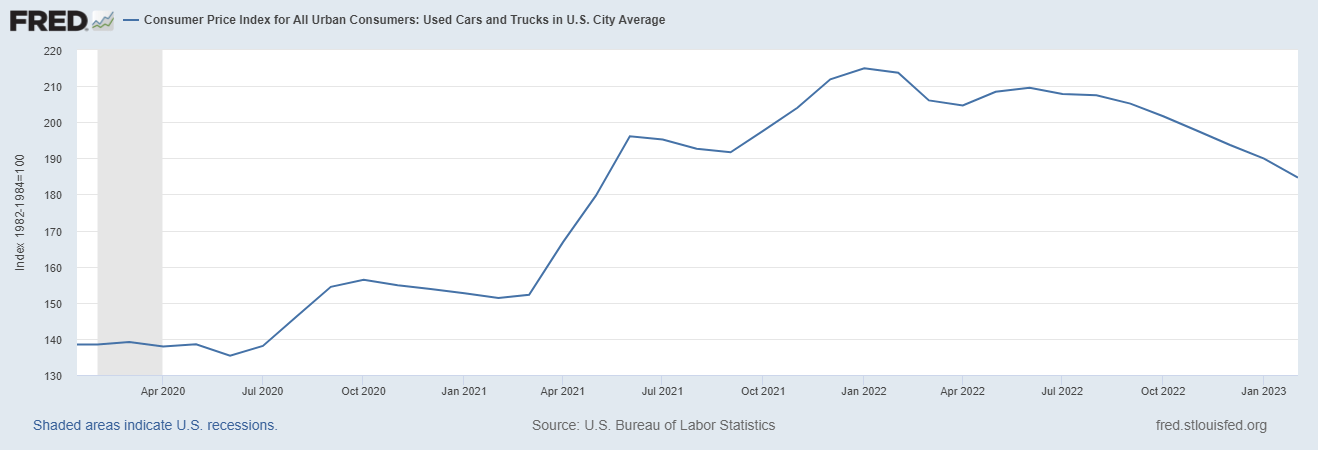

Nonetheless gross margin has not been particularly high. As expected the firms gross margin is tightly correlated to used car prices, which peaked in Q1 2022 and have been declining since. This has resulted in a much tighter gross margin for Shift over the last year, with the firm having to spend over 90 cents per dollar of revenue on a gross basis.

{kind=link}

{kind=link}

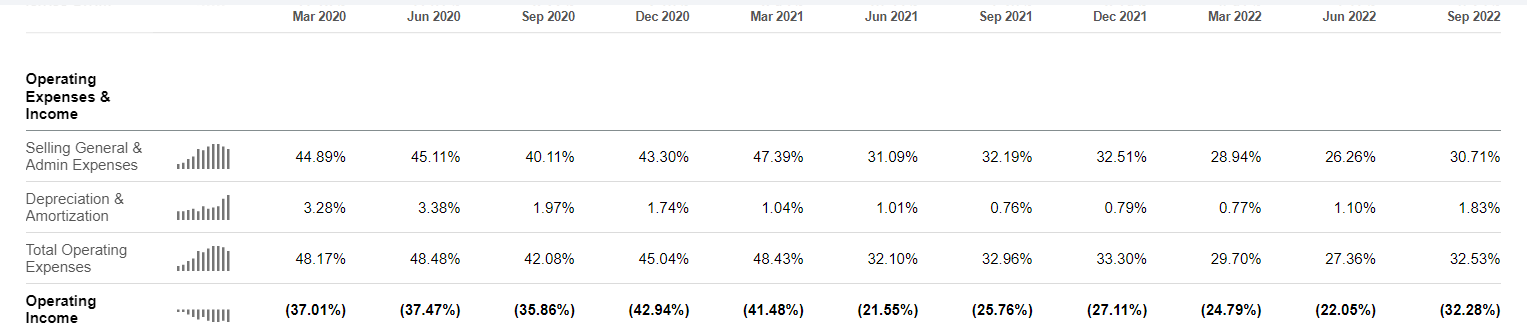

The low and declining gross margin here doesn’t leave much room for the company to actually generate a profit, as seen above. Furthermore Shift was not able to generate a positive operating income even when it was working with higher used car prices; this figure has grown significantly worse over the last year as well.

{kind=link}

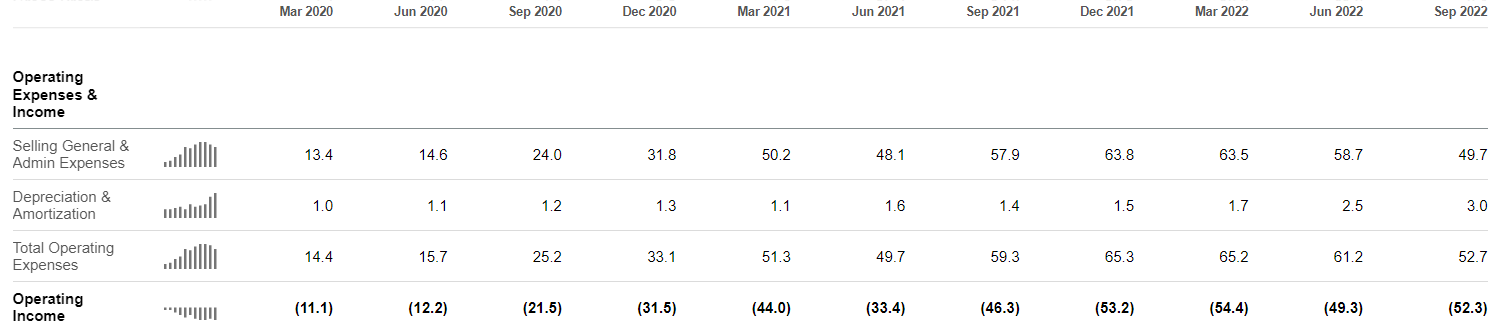

As it now stands the company is losing roughly 30 cents on every dollar of revenue that it generates. Simply put, there doesn’t appear to be enough gross margin for it to get to a positive bottom line. Management appears to have cut costs significantly in the last quarter, however, and total OpEx decreased 13.8% ($61.2M to $52.7M). In light of the revenue decline this was not enough to move the needle. Overall operating expenses still ended up higher than they had been at any point during 2022.

{kind=link}

As the company has been losing money on its operations, it is no surprise that it has seen a dwindling cash balance.

{kind=link}

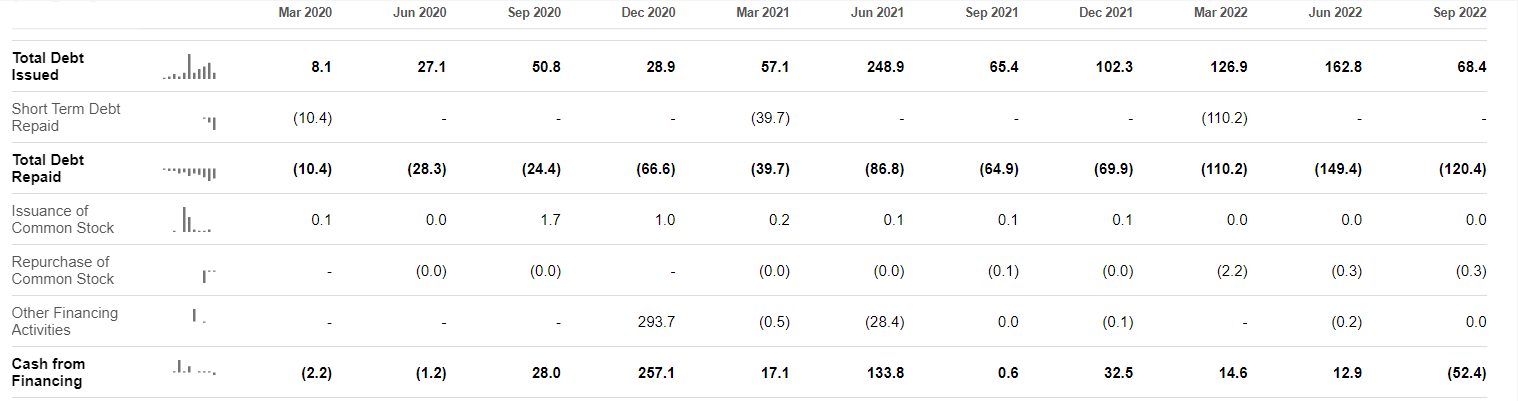

As such it has had to issue debt to continue operating, consistently receiving cash from financing since Q3 2020. Interestingly the firm actually retired $52.4M of debt in the most recent period, but it still issued $68.4M of new debt; it is simply rolling over its liabilities.

{kind=link}

Yet, Shift also appears to be able to generate some cash from its operations. This can be considered the sole bright spot of what was otherwise a difficult quarterly report for Q3 2022. I will be paying attention to this number in particular to see how the firm evolves in response to current conditions.

{kind=link}

Overall these numbers speak to a company that is streamlining itself in response to evidently lower sales volumes; this is in line with what management has stated in its most recent filing.

{kind=link}

The proof of whether this will work or not has not yet materialized.

Valuation

This company is trading quite cheaply on a sales basis, at a whopping 98% discount to the consumer discretionary sector. Since the firm is not yet profitable or cash-generative, that’s the only sensible valuation metric that we have for the time being. The market does not seem to be pricing in a very good future for this stock.

{kind=link}

Conclusion

It remains to be seen whether management can turn this company around within the new economic environment. It is an uphill battle as the firm has not previously had the chance to be profitable or cash-flow generative; it is a growth stock in a low-growth context. Additionally, I am skeptical of this happening in the near term as there is simply very little gross margin to go around, although the company is continuing to reduce its fixed cost footprint.

Used car prices continue to decline, however, and this is an ongoing pressure on the firm’s business model. In the next earnings report (out in less than a week), I am going to be looking at cost discipline, cash from operations, and the resultant gross/net margin. If the firm can get these numbers to improve then this stock could be an opportunity, but that remains to be seen. In the absence of proven leading indicators I am going to rate this a hold for the time being.

For further details see:

Shift Technologies: Cheap For Good Reason