FOUR - Shift4 Continues Growth Ways In 2023

2023-03-31 18:00:49 ET

Summary

- Shift4 reported its Q4 and full year 2022 financial results on February 28, 2023.

- The firm provides a range of payment processing technologies and services worldwide.

- Despite a softer Q4 volume environment, FOUR has continued to grow revenue and profits.

- My outlook remains a Buy on FOUR.

A Quick Take On Shift4 Payments

Shift4 Payments (FOUR) reported its Q4 2022 financial results on February 28, 2023, missing revenue but beating EPS consensus estimates.

The firm provides various payment processing and related services to organizations worldwide.

Despite a softening Q4 payment volume backdrop, Shift4 has produced strong revenue and profit growth.

My outlook remains a Buy on FOUR.

Shift4 Payments Overview

Allentown, Pennsylvania-based Shift4 has developed an integrated payments platform serving businesses located primarily in the United States.

Management is headed by founder and Chief Executive Officer Jared Isaacman, who was previously founder of Draken International, an air services provider.

The company's primary offerings include:

-

End-to-end payment processing

-

Merchant acquisition

-

Omni-channel gateway

-

350 integrations

-

Fixed and mobile POS solutions

-

Security and risk management tools

-

Reporting and analytics

Shift4's Market & Competition

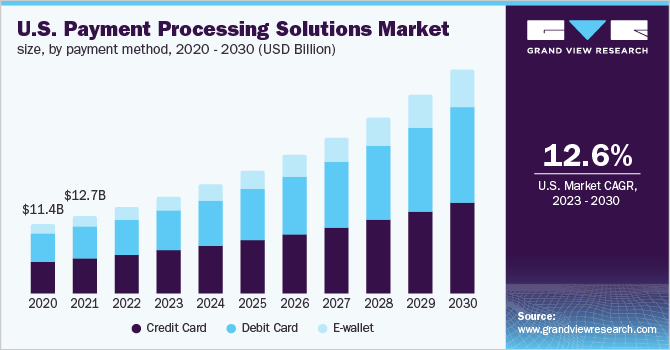

According to a 2023 market research report by Grand View Research, the market for payment processing services was an estimated $47.6 billion in 2022 and is forecast to reach $140 billion by 2030.

This represents a forecast CAGR of 14.5% from 2023 to 2030.

The main drivers for this expected growth are continued growth in the penetration of internet access and growing usage of online and electronic means for consumer and business transactions.

Below is a chart showing the historical and projected future growth of the U.S. payment processing solutions market through 2030:

{kind=link}

Major competitive vendors to Shift4 include:

-

PayPal

-

Toast

-

Adyen

-

Stripe

-

Global Payments

-

Block

-

Jack Henry & Associates

-

Paysafe Group

-

Naspers Limited

Management says its system provides payment processing and integrates with a large number of third-party 'commerce enabling' software to offer a more seamless set of solutions.

Shift4's Recent Financial Results

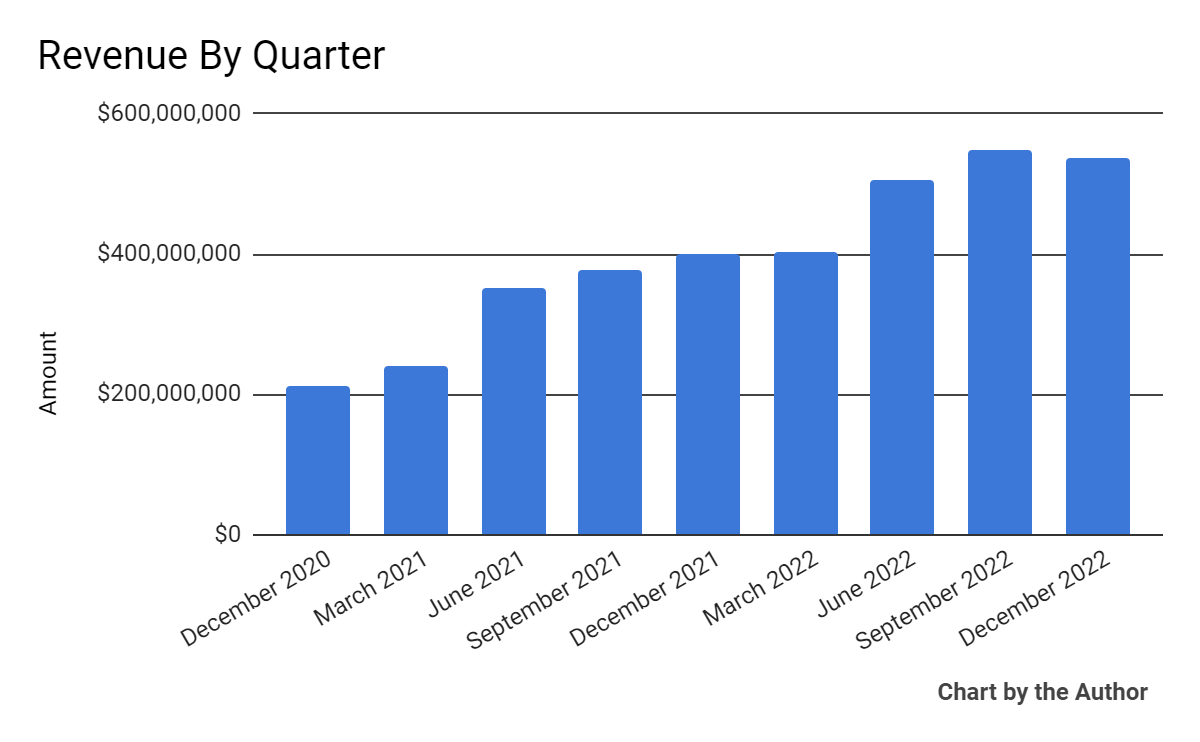

-

Total revenue by quarter has risen per the following chart:

{kind=link}

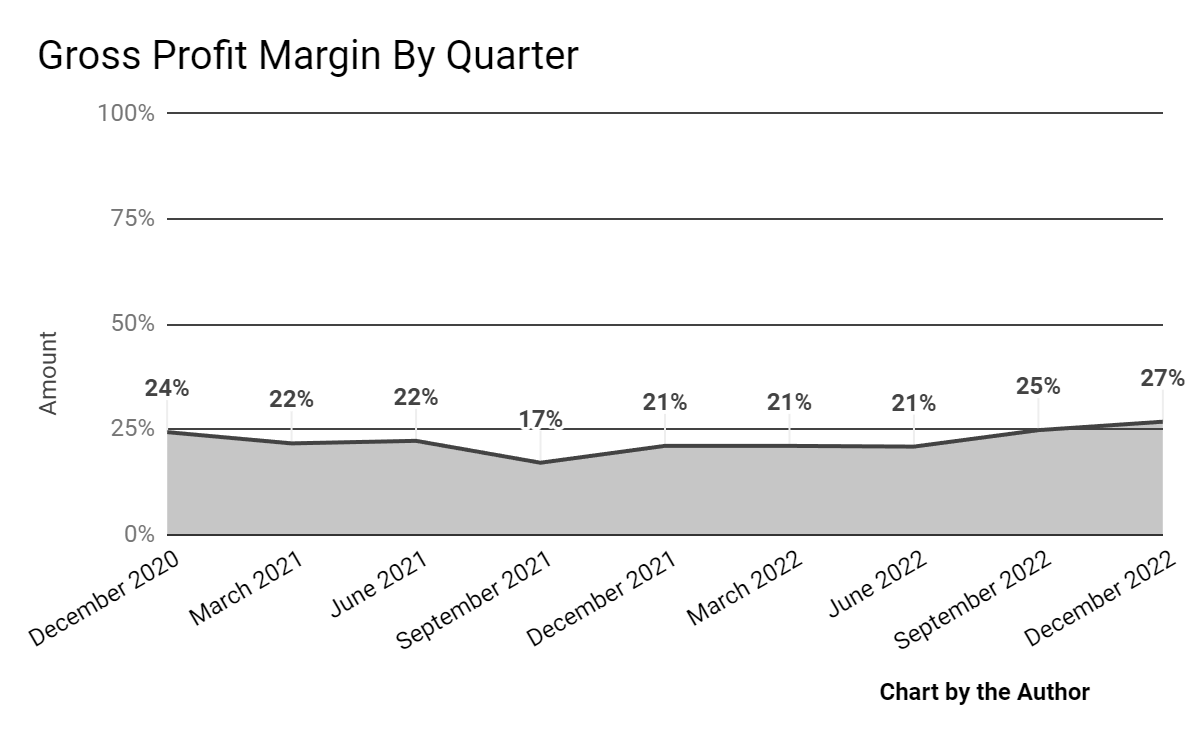

-

Gross profit margin by quarter has trended higher as the chart shows here:

{kind=link}

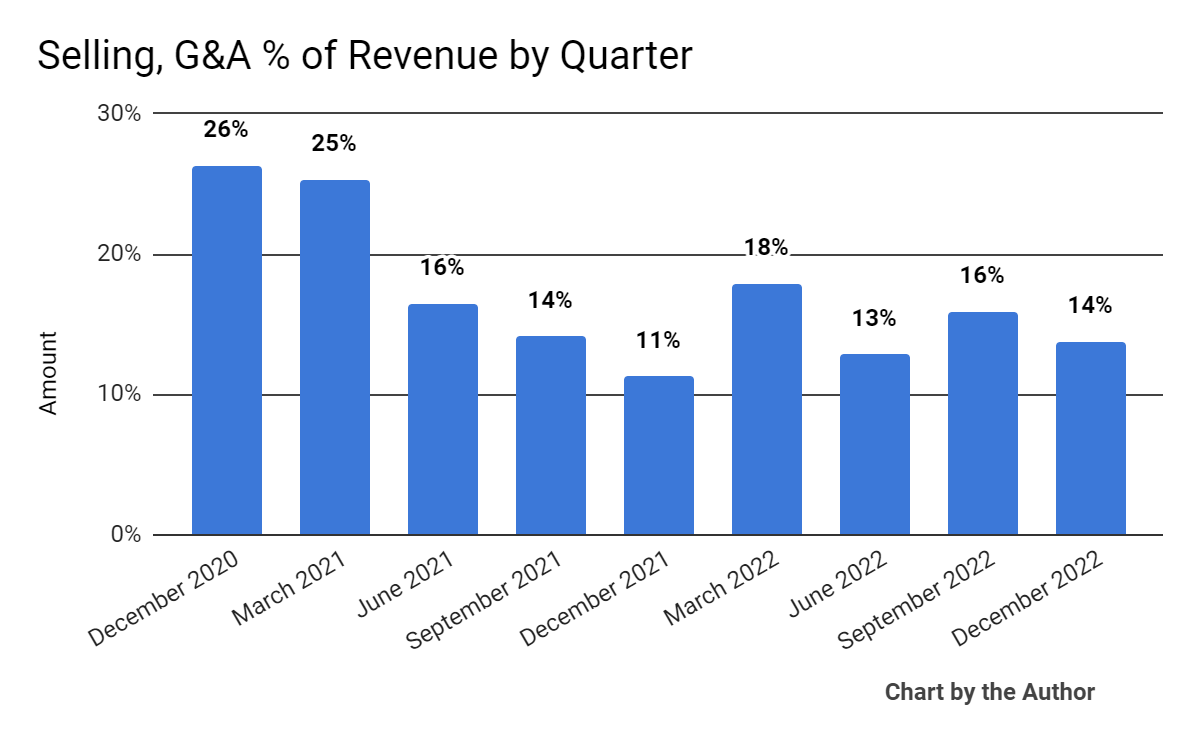

-

Selling, G&A expenses as a percentage of total revenue by quarter have dropped, a positive signal indicating the company is getting more efficient generating each incremental dollar of revenue:

{kind=link}

-

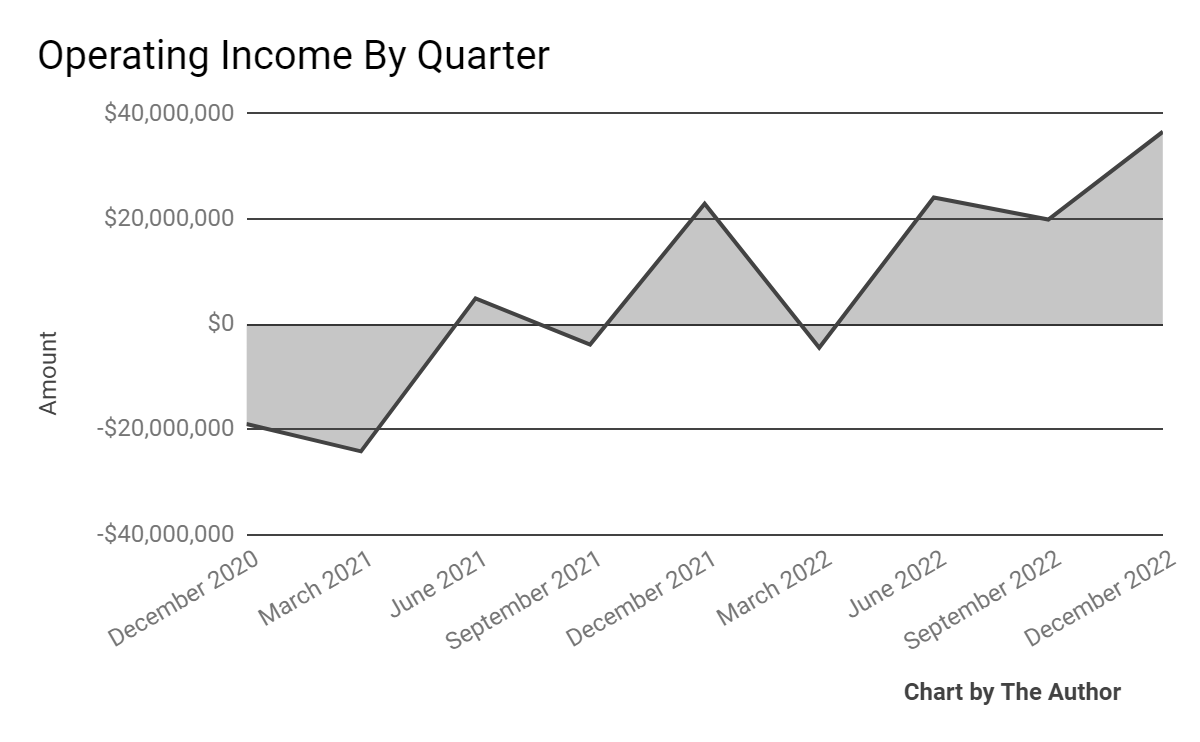

Operating income by quarter has trended higher in recent quarters:

{kind=link}

-

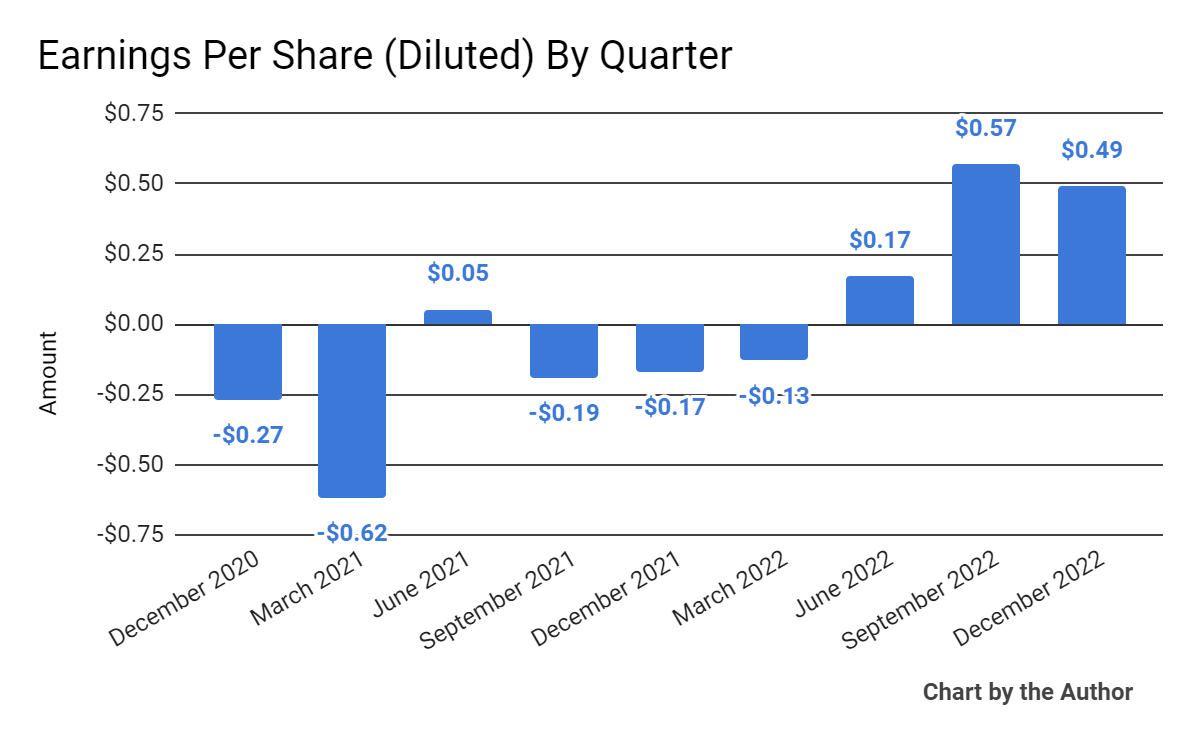

Earnings per share (Diluted) have jumped in recent quarters:

{kind=link}

(All data in the above charts is GAAP)

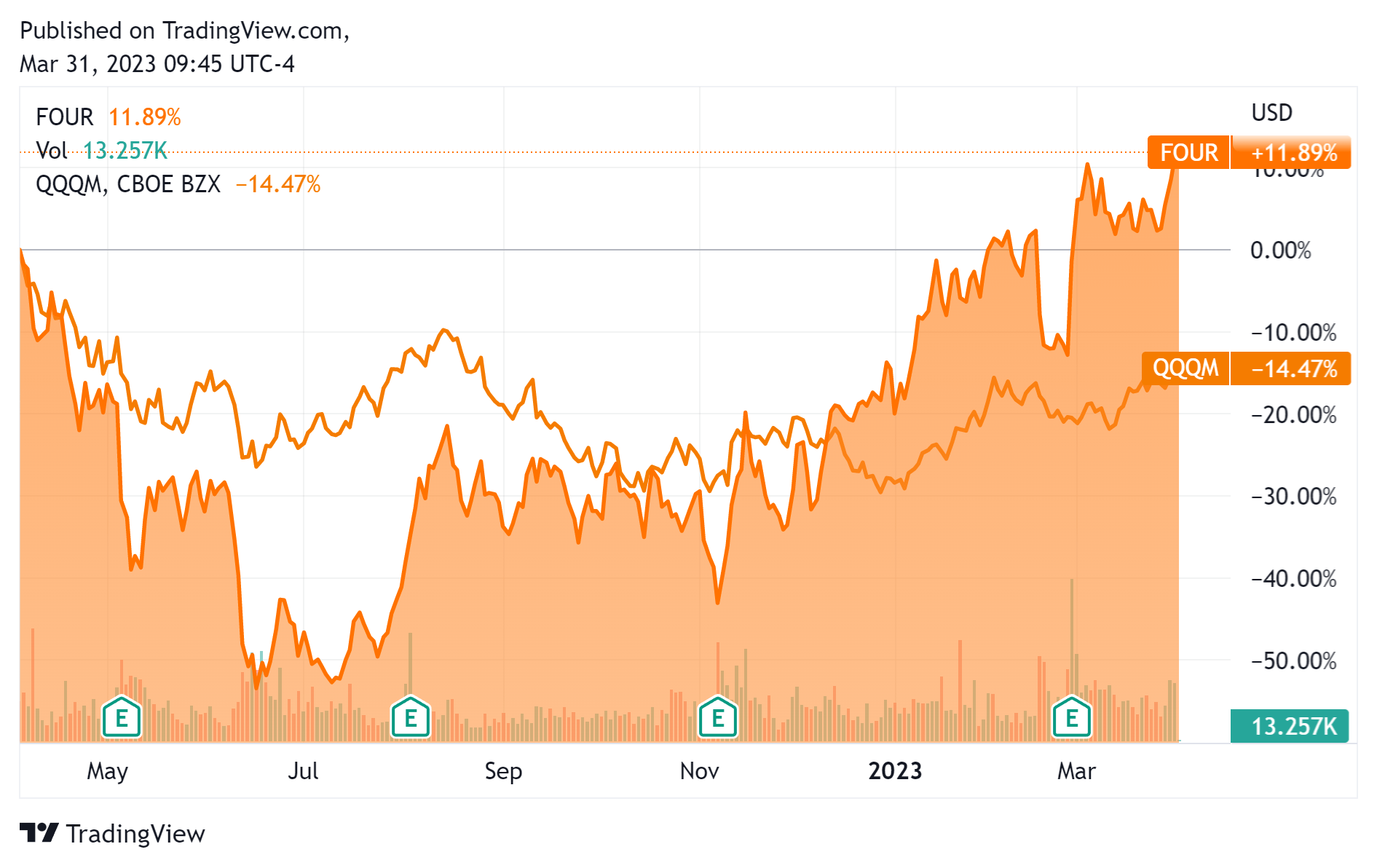

In the past 12 months, FOUR's stock price has risen 12% vs. that of the Nasdaq 100 Index's drop of 14.5%, as the chart indicates below:

{kind=link}

As to its Q4 2022 financial results, total revenue rose 34.6% year-over-year and gross profit margin increased 5.7 percentage points.

SG&A as a percentage of total revenue continued a sequential downward trend while operating income rose markedly year-over-year, as did earnings per share.

For the balance sheet, the firm ended the quarter with cash and equivalents of $776.5 million and total debt of $1.75 billion.

Over the trailing twelve months, free cash flow was an impressive $213.6 million, of which capital expenditures accounted for $61.8 million. The company paid $49.6 million in stock-based compensation in the last four quarters.

Valuation And Other Metrics For Shift4

Below is a table of relevant capitalization and valuation figures for the company:

| Measure [TTM] |

| Amount |

| Enterprise Value / Sales |

| 2.6 |

| Enterprise Value / EBITDA |

| 28.9 |

| Price / Sales |

| 2.0 |

| Revenue Growth Rate |

| 45.8% |

| Net Income Margin |

| 3.8% |

| GAAP EBITDA % |

| 9.0% |

| Market Capitalization |

| $5,840,000,000 |

| Enterprise Value |

| $5,180,000,000 |

| Operating Cash Flow |

| $275,400,000 |

| Earnings Per Share (Fully Diluted) |

| $1.10 |

(Source - Seeking Alpha)

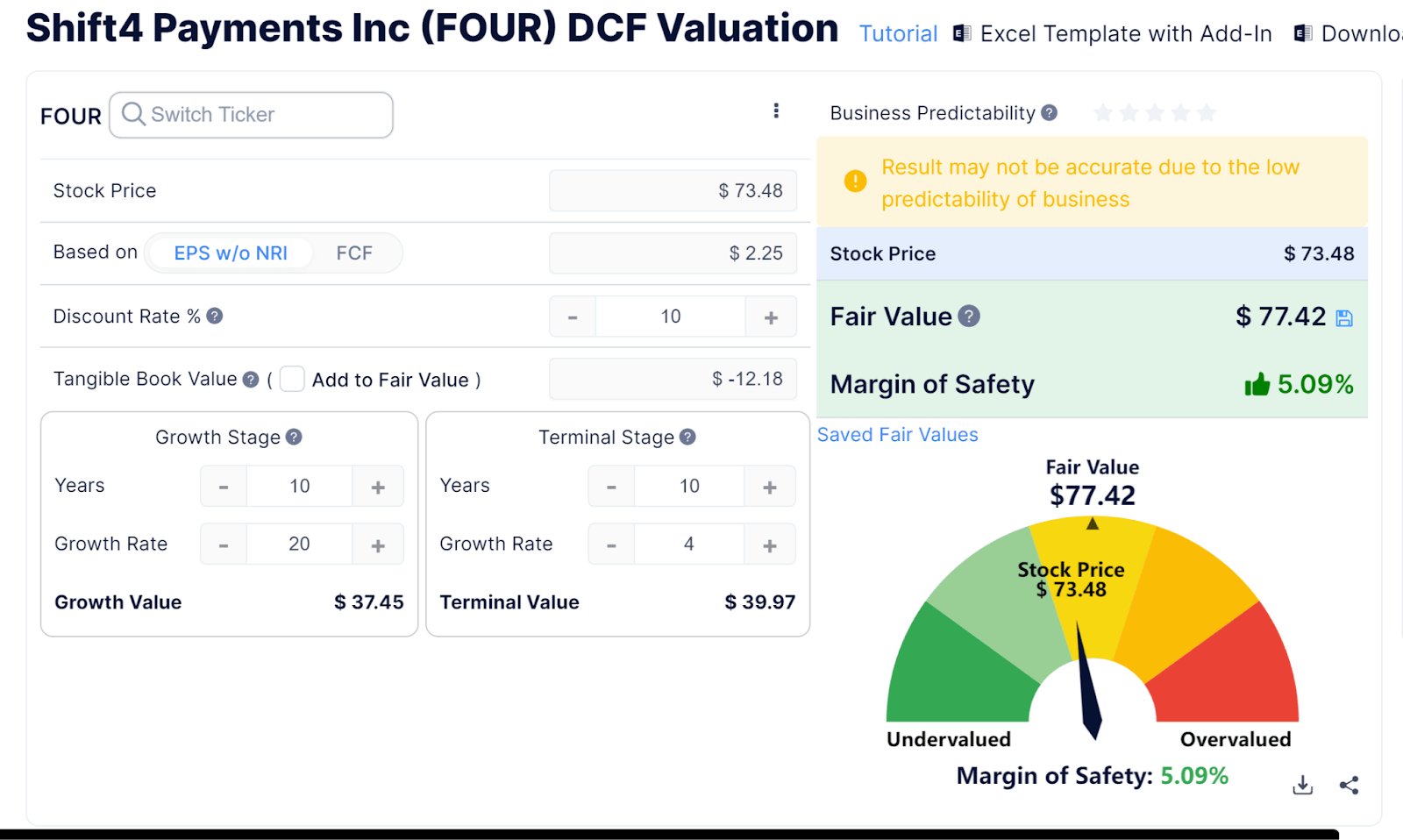

Below is an estimated DCF (Discounted Cash Flow) analysis of the firm's projected growth and earnings:

{kind=link}

Assuming generous DCF parameters, the firm's shares would be valued at approximately $77.42 versus the current price of $73.48, indicating they are potentially currently slightly undervalued, with the given earnings, growth, and discount rate assumptions of the DCF.

As a reference, a relevant partial public comparable would be Block (SQ); shown below is a comparison of their primary valuation metrics:

| Metric [TTM] |

| Block |

| Shift4 Payments |

| Variance |

| Enterprise Value / Sales |

| 2.3 |

| 2.6 |

| 11.6% |

| Enterprise Value / EBITDA |

| NM |

| 28.9 |

| --% |

| Revenue Growth Rate |

| -0.7% |

| 45.8% |

| --% |

| Net Income Margin |

| -3.1% |

| 3.8% |

| --% |

| Operating Cash Flow |

| $175,900,000 |

| $275,400,000 |

| 56.6% |

(Source - Seeking Alpha)

Future Prospects For Shift4 Payments

In its last earnings call (Source - Seeking Alpha), covering Q4 and full year 2022's results, management highlighted its record results for the full year, 'all in excess of [its] midterm outlook.'

2022 saw the beginning of its European and greater international expansion efforts and the launch of its SkyTab restaurant POS system.

However, the range of potential outcomes in 2023 is wider than management would have liked due to a Q4 moderation in payment volumes that was industry-wide, likely as consumers pulled back in the face of macroeconomic headwinds.

Looking ahead, management sees its European business propelled by its Finaro acquisition, which it expects approval for 'shortly'.

Regarding valuation, my discounted cash flow calculation indicates the stock may be slightly undervalued, but that assumes a generous growth estimate and flawless execution.

Risks to the company's outlook include a sagging global economy and remaining uncertainties with its Finaro acquisition which is central to its international expansion efforts.

Even with a softening Q4 payment volume backdrop, Shift4 has produced strong revenue and profit growth.

My outlook remains a Buy on FOUR.

For further details see:

Shift4 Continues Growth Ways In 2023