FOUR - Shift4 Payments Is Buying Economies Of Scale

2023-12-11 11:03:33 ET

Summary

- Shift4 Payments experienced significant growth in Q3'23, with end-to-end payment volumes increasing 36%.

- The company's acquisition of Appetize will add a host of stadiums for end-to-end revenue generation from ticketing to food & beverage.

- With a modest valuation and potential for further growth, Shift4 Payments is recommended as a buy with a price target of $97.94/share.

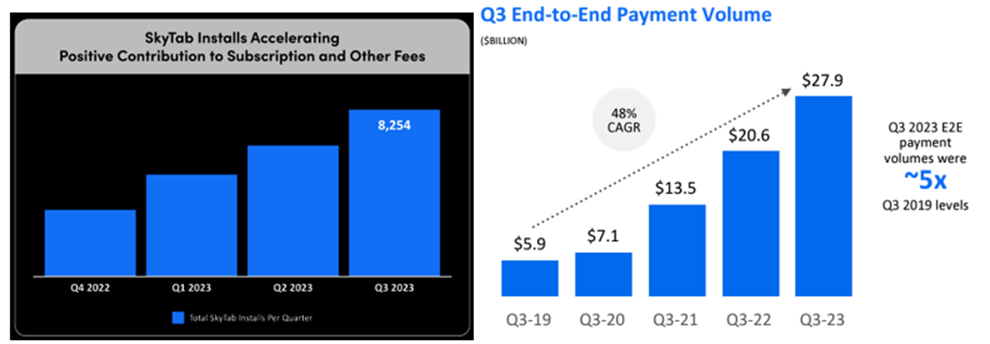

Shift4 Payments (FOUR) experienced significant growth in Q3'23 with end-to-end payment volumes increasing 36% with anticipation of higher volumes in Q4'23 inclusive of their in-year enterprise initiatives in resorts and stadiums resulting from the October 2, 2023 acquisition of SpotOn Technologies. Considering management's advantageous strategy of growth both organically and through M&A, I believe Shift4 Payments will ultimately become the powerhouse of transactions across payment systems. The firm currently trades at a modest 1.67x TTM Q3'23 sales with room for multiples expansion. Given this along with their potential growth trajectory, I provide FOUR a BUY recommendation with a price target of $97.94/share with an upside potential of 45%.

Operations & Macro

{kind=link}

Shift4 Payments experienced significant growth in Q3'23 with two significant tail-end acquisitions that will become accretive coming in Q4'23. At the top line, revenue grew 6% on a trailing basis, in line with the previous quarter, as the firm faces uncertainty in the macroeconomic environment. Management disclosed the acquisition of Finaro, pro forma would add 4% in topline revenue generation, realizing 27% growth. Looking forward, I believe much of the firm's growth for 2024 will be attributable to gateway conversions and M&A. I believe their M&A strategy has done well for the firm and continuing this growth strategy will bolster their land and expand strategy.

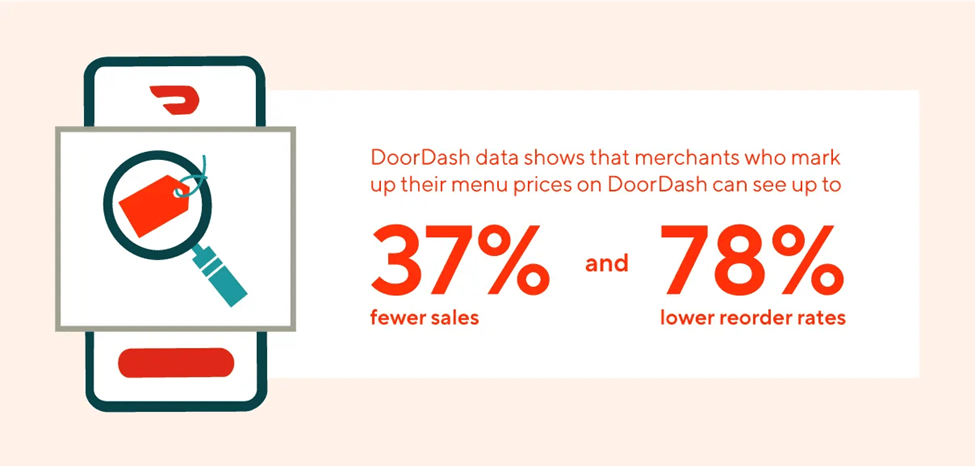

As the global economy teeters on the brink of a recession, the food and beverage industry appears to be relatively sensitive to price inflation. DoorDash reported that 37% of restaurants that raised their prices experienced fewer sales as well as 78% fewer repeat orders.

{kind=link}

Looking at both the nominal inflation index as well as the rate of y/y change for eating away from home, prices have continued to climb at exceptionally higher rates when compared to previous periods and don't appear to be slowing down.

{kind=link}

Though this doesn't necessarily affect consumers as a whole, it appears to be adding pressure on the food and beverage industry to build a more dedicated customer base. As suggested in my previous article covering Chewy ( CHWY ), many consumers are stretching the buck as far as it can go and are seeking alternative products to manage their cost of living. Though that's comparing pet food to dining, I believe the theme remains that those eating out will seek more economical alternatives throughout the next year.

There could be a silver lining with their recent acquisition of Appetize and their stadium presence. The acquisition will add some major stadiums to the company's customer base, including Fenway Park, Yankee Stadium, Madison Square Garden, and Busch Stadium, amongst others. This integration will bring along a significant amount of benefits, including the integration onto the VenueNext platform, mobile payments, concessions, retail parking, and ticketing. The acquisition will be materially morphing Appetize's business model in which Shift4 Payments will be pivoting the model to payments, discontinuing hardware sales, and discontinuing the payment referral revenue. Though this will lower Appetize's revenue generation in the short term, this is a strategy Shift4 Payments has executed in prior deals and expects this to become a synergy-rich deal with reduced costs and higher revenue generation.

According to IWSR , consumers have a tendency to switch from beer to liquor during recessions. As more stadiums and venues focus their attention on craft cocktails and craft beer, alcohol sales may be less affected by an economic downturn at stadiums.

Goldman Sachs' analysts also suggested that beer and spirits tend to be recession- and inflation-proof. The only limiting factor is that consumers have the tendency to switch from restaurants and bars to eating and drinking at home.

Despite this trend, attendance at sporting events and concerts may be dampened if a recession were to arise, leading to overall lower sales volume and payments volume for Shift4 Payments.

Lower levels of disposable income could dampen leisure and entertainment spending in a tightened economic environment. This could translate to lower attendance for sporting events or concerts.

Aside from this, management discerned that the firm will meet consensus estimates with flat growth when annualizing the Q3'23 figures. With the addition of ticketing in their end-to-end payments within a stadium, management mentioned at the UBS Global Tech Conference that the addition of food and beverage would drive 4x the fees on top of just ticketing fees.

If you essentially annualize Q4 2023, including our adds in 2023 and what we anticipate from Appetize, you're already at consensus 2024 EBIT estimates. Similarly, you could also just annualize Q3's non-GAAP adjusted EPS and you're also at 2024 analyst EPS estimates.

Jared Isaacman, Founder & CEO

Management has ambitious goals through their Finaro acquisition with the target of adding over 10,000 restaurants and hotels across Europe and Canada.

Overall growth has remained stable through both gateway conversions and M&A activity.

{kind=link}

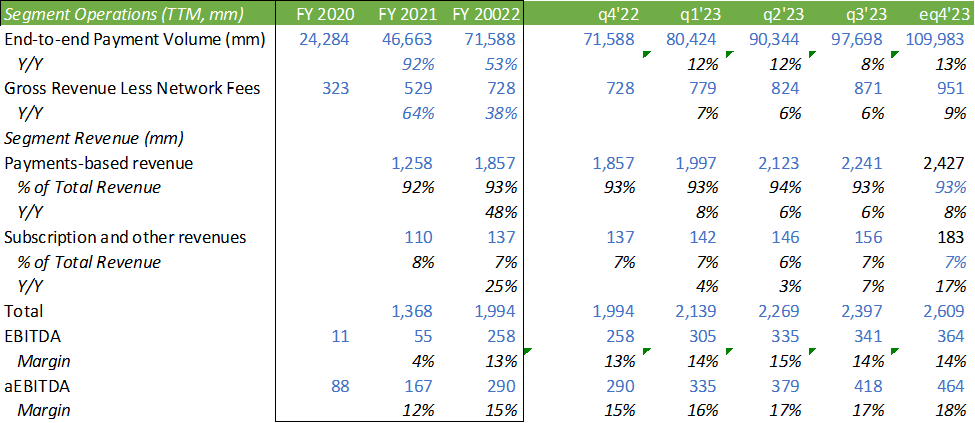

Management expects gross revenue less network fees to be between $274-$289mm for Q4'23, resulting in FY23 figures to be between $945-$960mm, resulting in a 9-10% increase on a year-to-year TTM basis. aEBITDA is expected to be between $132-$140mm for Q4'23, resulting in FY23 aEBITDA of $456-$464mm with a margin of 17.5-17.66%.

Based on their current positioning, I believe Shift4 Payments is in a good position throughout the duration of FY23 and may experience a slowdown in organic growth throughout FY24. That being said, I believe management will continue to remain opportunistic in the M&A market for additional deals as competitors' multiples fall. This inorganic growth should accommodate the slowing market and position the firm for a longer runway for success. I believe a company like Toast ( TOST ) that focuses on the restaurant industry payments and operations infrastructure may be the type of firm Shift4 Payments may target for a merger, despite the much higher market cap.

{kind=link}

Shift4 Payments does hold a bit of debt on the balance sheet, with a net debt/aEBITDA ratio of 2.52x. The firm has a relatively low cost of debt at just 1.81% and no maturities through 2025. The 2025 notes and 2027 notes are each convertible, with respective strike prices at $80.48/share and $122.66/share.

Valuation

Shift4 Payments has historically authorized share repurchase programs on an annual basis. The firm currently has a program to repurchase up to $250mm of Class A shares through December 31, 2023, with $153.2mm remaining as of Q3'23 reporting. Management noted on the call that they will remain opportunistic in repurchasing shares.

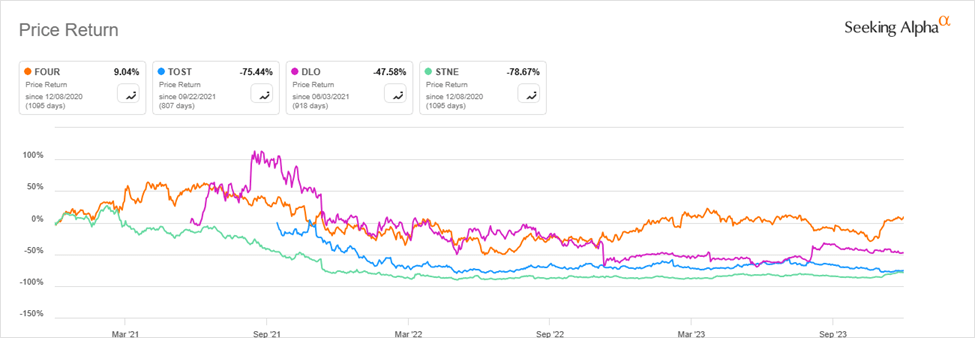

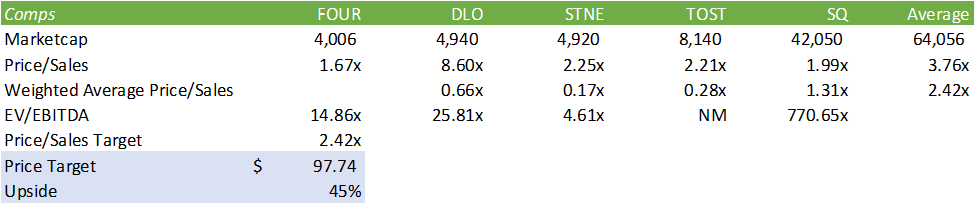

FOUR trades at a significant discount to their competitors in the market at 1.67x TTM sales.

{kind=link}

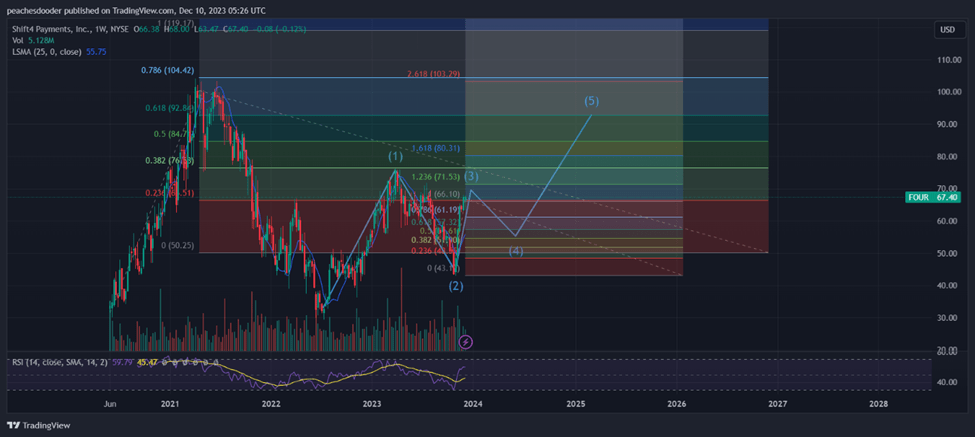

I used a weighted average price/sales multiple based on market cap for a target multiple of 2.42x TTM sales. I do believe there may be some near-term pullback in the stock price as shares remain in overbought territory since the recent run-up. As the stock retraces to 0.382% of the third wave when using Elliot Wave Theory, the technical pricing can potentially position the stock at or near my fundamental price target. With this, I give FOUR a BUY recommendation with a price target of $97.74/share.

{kind=link}

For further details see:

Shift4 Payments Is Buying Economies Of Scale