FOUR - Shift4 Payments: Still Valuable At 15.4x EV/EBITDA

2024-01-03 13:20:28 ET

Summary

- Shift4 Payments is a payment processor serving over 200,000 business locations across various industries.

- The stock has seen a significant increase lately fueled by acquisition rumors, but it remains reasonably priced compared to its peers.

- Analysts are estimating growth will accelerate in 2024 while the company generates increasing free cash flow.

Investment Thesis

Shift4 Payments ( FOUR ) is, plain and simple, a payment processor company. They have built the tech and software to allow companies to charge its clients. They serve more than 200,000 business locations across major industries like hospitality, restaurants, sports venues, and e-commerce. They have everything from the POS system, to the software and mobile payments.

The stock has been on a hot streak lately, rising +50% in less than two months. Although this increase was fueled by acquisitions rumors, the stock remains reasonably priced at 15.4x EV/EBITDA. Analysts are estimating that revenue growth will accelerate in 2024 and, when compared to its peers, the stock seems like a great opportunity for this new year.

What They Do

FOUR serves as an end-to-end payments processor primarily for enterprise clients. The term "end-to-end" means that FOUR handles the entire payment process, from collecting payment data to settling transactions.

Historically, FOUR focused on being a payments gateway, which is not the same as a payment processor. A payment gateway collects customer information for payment, and a payment processor that uses that information to contact the customer's bank and the merchant account, debiting one account and crediting the other. There are essentially two halves of the transaction.

However, much of the value in payment transactions typically goes to merchant acquirers, companies responsible for processing and settling payments. This is why, through several acquisitions, they expanded to provide end-to-end payment processing, covering the entire payment journey from data collection to settlement.

When a merchant starts using FOUR payment platform, they have two options: they can either use it as a gateway or as an end-to-end payment solution.

For those who opt for the end-to-end approach, they enjoy a unified solution for payment acceptance, devices, point-of-sale ((POS)) software, and a suite of business intelligence tools. This integrated solution simplifies their operations and allows them to cut costs on various payment acceptance solutions. Additionally, they gain access to gateway and technology solutions as extra features, adding further value to their overall offering.

On the other hand, merchants choosing the gateway option benefit from interoperability with third-party payment processors. To put it into numbers, FOUR has more than 500 different integrations with the kinds of legacy software solutions that big complex organizations might use. This flexibility allows them to connect and work seamlessly with different external payment processing services. Essentially, they have the freedom to integrate our gateway into their existing systems and utilize third-party processors of their choice.

Because of all this, FOUR is has been able to attract large enterprise clients and grow very quickly. Nowadays, they serve more than 200,000 business locations across major industries, primarily sports venues, hotels, casinos, and restaurants such as Ceasar's, Hilton, Levi's Stadium, etc.

Financials

FOUR earns revenue from fees paid by their costumers, which is basically a percentage of the end-to-end volume or a fixed per transaction. They also make money from licensing subscriptions to their POS software, business intelligence tools, payment device management and other technology solutions, for which they typically charge a flat subscription fees on a monthly basis.

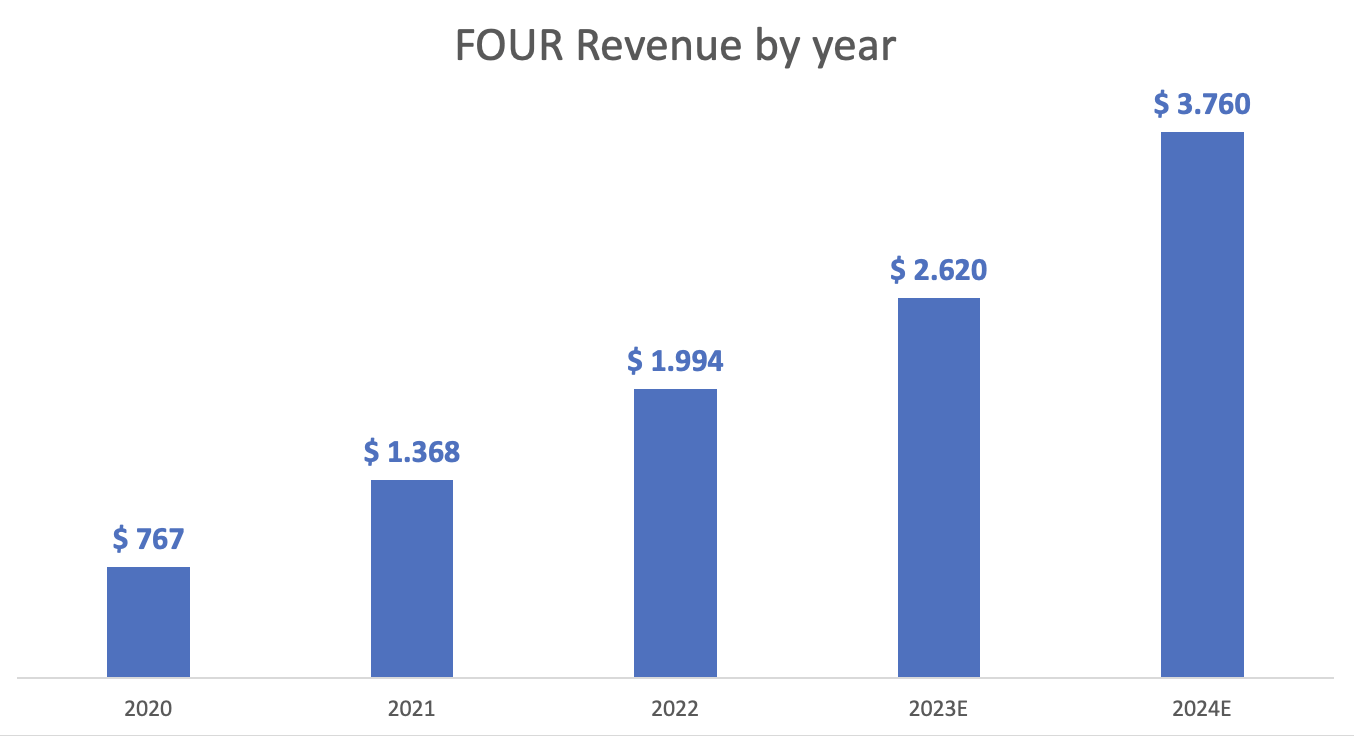

Revenue has increased at a 36% CAGR for the past 4 years and it is expected to grow an additional 43% in 2024. In other words, revenue growth will accelerate in 2024 vs. 2023.

{kind=link}

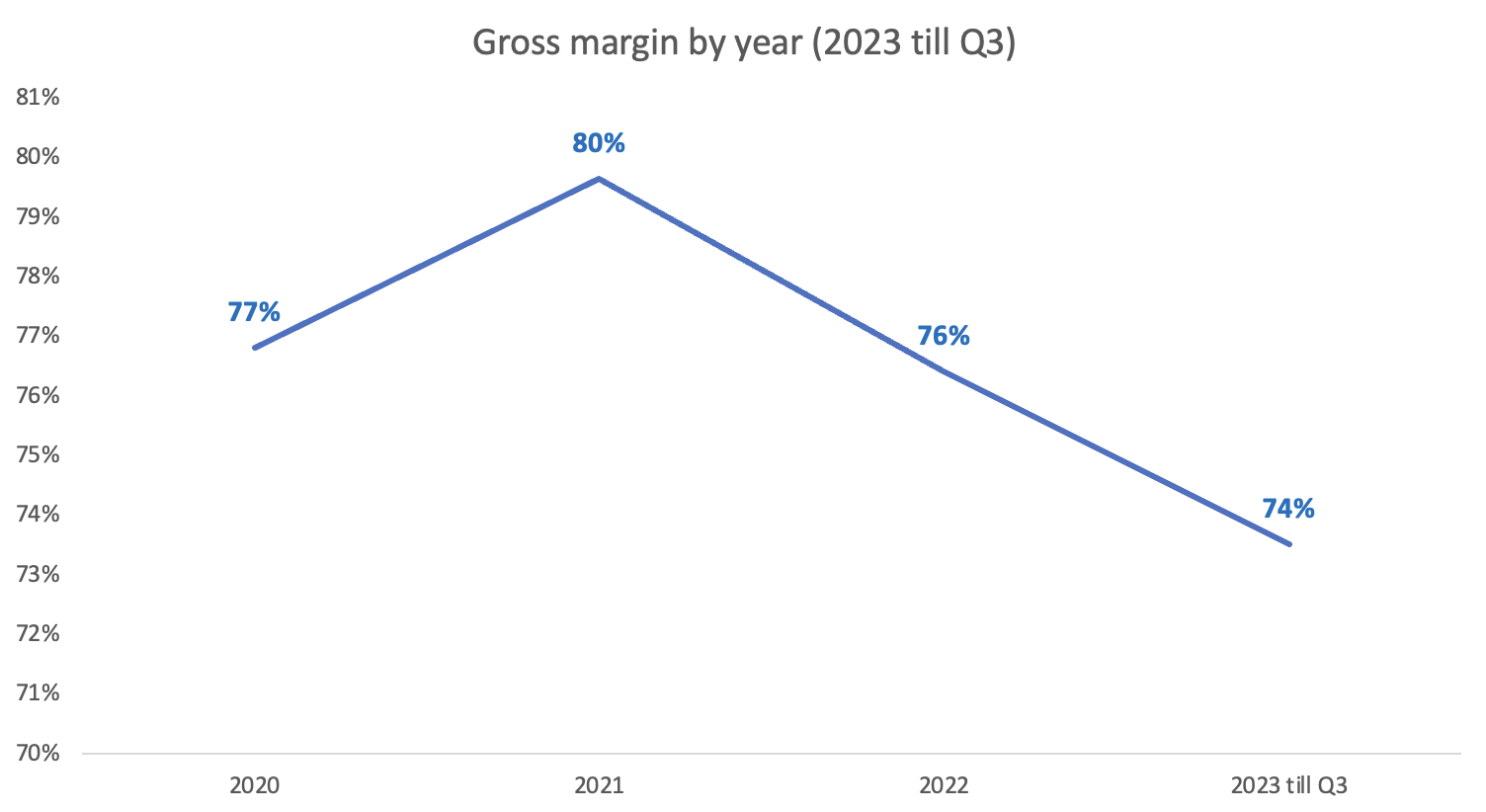

Although revenue has been increasing, the gross margin has been relatively stable around 80%-75%.

{kind=link}

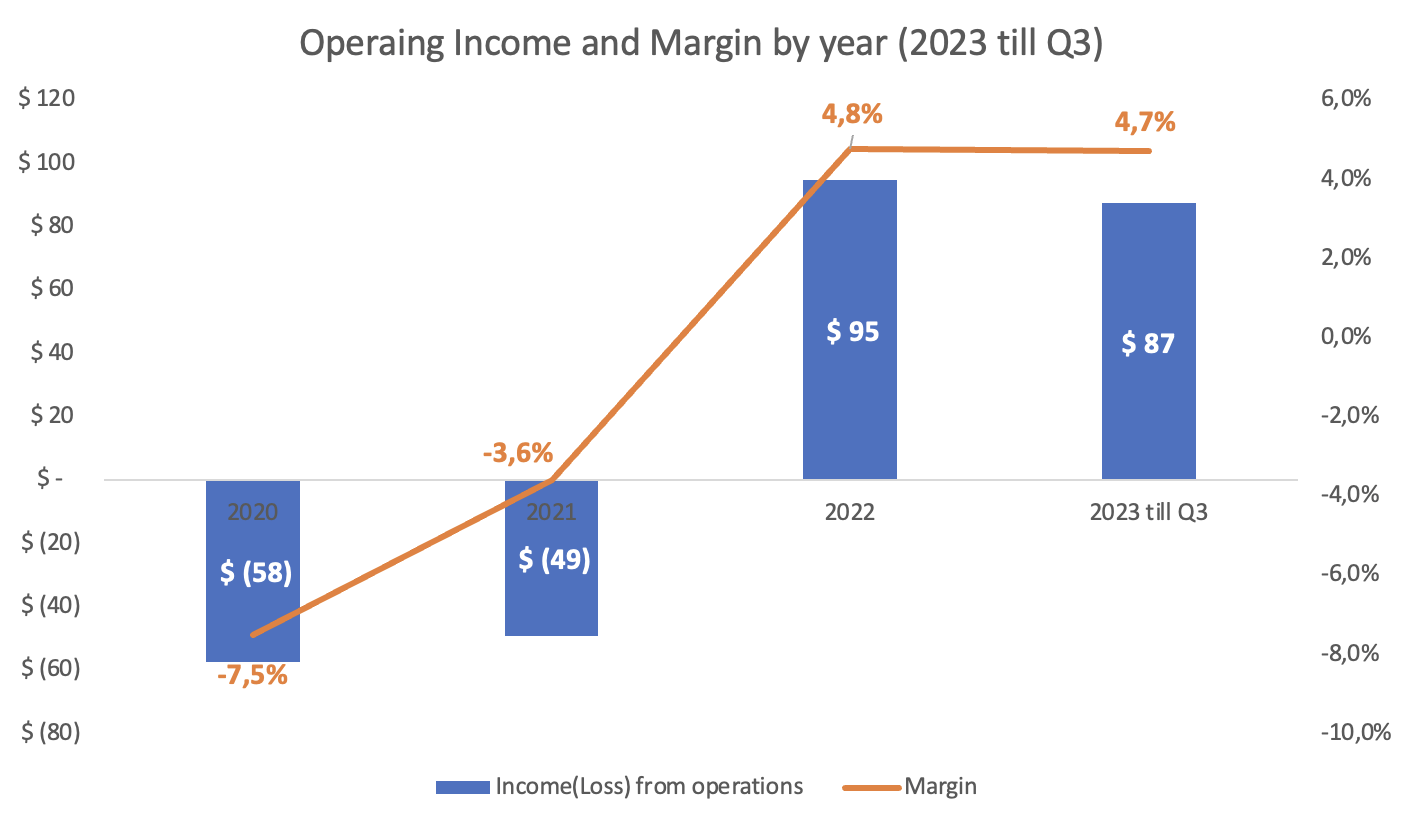

Moreover, the company has been profitable two years in a row now.

{kind=link}

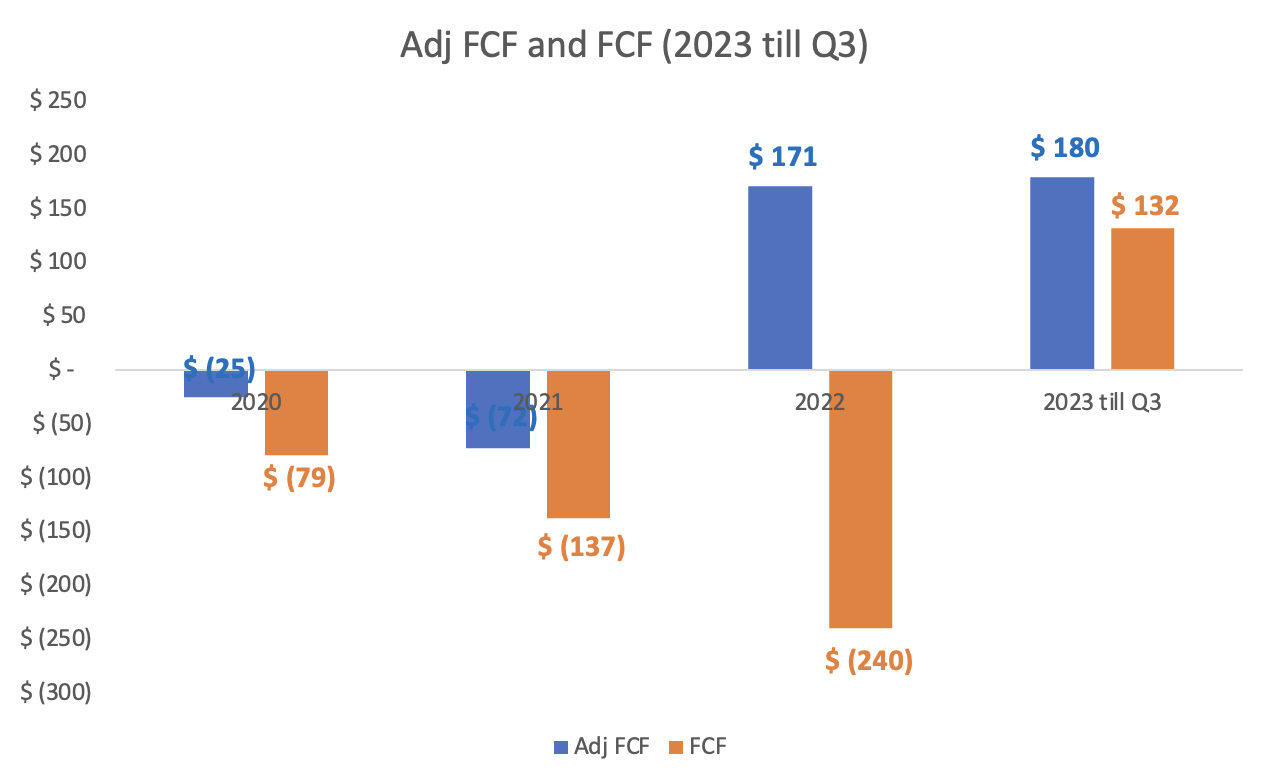

However, they have been spending most of their cash flow in acquisitions to fuel growth. Look at the following chart. FCF is just cash from operations minus capex, while adjusted FCF also takes into account acquisitions, buyout commissions, etc.

{kind=link}

This year, 2023, they expect to generate +$259 million in adjusted free cash flow vs. $147.2 million a year ago (the reconciliation they make is slightly different from the chart I did above).

Overall, they are growing fast and are profitable. They are in a solid financial position as well, without having a large amount of debt hanging over their shoulders relative to their cash.

Valuation

FOUR has a market cap of $6.12 billion. They have $783 million in cash and $1.74 billion of long term debt, so the enterprise value comes up to $7.07 billion.

FOUR made $2.4 billion in revenue the last twelve months, which translates into a 2.23 P/S ratio. Fiserv ( FI ) trades at 2.79x, Toast ( TOST ) at 2.76x, and Block ( SQ ) at 2.3x P/S ratio. Those are all very similar ratios, but FOUR remains the cheapest with the fastest grow.

Moreover, FOUR is highly profitable. They expect to make +$260 million in FCF in 2023 . Using just that number, it means that the stock trades at 23.5x P/FCF. That's not a very expensive multiple for a company expected to grow revenue 43% next year.

Moreover, adjusted EBITDA should come in between $456 million and $464 million. That would strike a 15.4x EV/EBITDA at the midpoint. Still, cheaper than its peers.

Overall, despite the rapid increase it had the last couple months, the common stock doesn't look expensive compares to its peers. In a potential takeover (given the rumors of the last couple weeks), some articles were saying the potential buyout price could be between $90 and $100 dollars per share.

Risks

There are several red flags with this investments (as with any):

- FOUR is a founder-led and majority owned company. James Isaacson, CEO, owns 31.7% of the shares outstanding and controls 82% of the voting power, allowing him to do, basically, whatever he wants.

- Blue Orca, a short seller, has raised concerns about Adj EBITDA and free cash flow being inflated in the past.

- FOUR operates in a high competitive industry and faces intense competition from companies like Toast ((TOST)), Block ((SQ)), Fiserv ((FI)) and Global Payments ( GPN ).

- As the company's growth slow, the stock will face multiple compression.

Takeaway

Although FOUR has risen a lot in the past two months, the stock remains reasonably priced while growth accelerates in the coming year. In the short term, I am concerned that the stock looks a little extended given that the RSI has been over 70 for the past 9 sessions. Right now I would wait for a pullback to initialize a new position, but I still rate it a BUY.

For further details see:

Shift4 Payments: Still Valuable At 15.4x EV/EBITDA