FOUR - Shift4 Payments: Strong Growth At 25-30% CAGR In 2024 Priced At 16x FCF

2023-11-16 12:19:06 ET

Summary

- Shift4 Payments, Inc. boasts impressive organic growth, projected at 25-30% CAGR in 2024.

- At less than 16x forward free cash flows, the stock's valuation presents a compelling opportunity.

- Despite recent volatility, Shift4 Payments remains resilient, supported by strategic acquisitions and a commitment to profitability.

Investment Thesis

Shift4 Payments, Inc. ( FOUR ) Q3 results demonstrate that this company continues to grow at a rapid rate. According to my estimates, its organic growth rates in 2024 should come in around 25% to 30% CAGR. And that's clearly a very attractive growth rate.

But what if I told you that not only Shift4 Payments is delivering very fast growth rates, but that it's priced less than 16x forward free cash flows?

I must say, it's difficult not to get excited about this company's prospects.

Rapid Recap,

In my previous bullish analysis , I argued:

[Shift4 Payments] is a cheaply valued stock with strong prospects, particularly now that its growth rates have stabilized.

Author's work on FOUR

Since I made that assertion, the stock has been very volatile. Although its stock's performance is now positive territory, the performance was challenging and investors would have needed an iron stomach to put up with its vicissitudes.

Nonetheless, as we look ahead to 2024, I find myself bullish on this name, particularly given just how profitable the business is.

Shift4 Payments' Near-Term Prospects

Shift4 Payments is poised for a solid near-term outlook, underscored by its reassuring financial performance in Q3 2023.

The diversified momentum across enterprise merchants, including ventures into new verticals, has proven fruitful. Notably, strategic decisions made in the prior year, such as in-sourcing a significant portion of the go-to-market distribution in connection with the SkyTab POS launch, have contributed to improved unit economics, particularly in the restaurant channel.

Furthermore, its acquisition of Finaro is a key highlight, not only removing uncertainties surrounding international expansion but also contributing positively to the company's overall prospects.

The synergies from the Finaro acquisition are expected to have a favorable impact on future quarters. Also, Shift4 Payments' strong balance sheet , boasting over $690 million in cash, coupled with financial flexibility and a commitment to disciplined investments, further solidifies its position for sustained growth in the dynamic market landscape. That being said, note that Shift4 Payments holds nearly $1.8 billion of debt, meaning that it's fairly leveraged, even though management asserts otherwise.

What's more, as you can see above, in the past 6 months its share price has been the best performer in its peer group.

Given this context, let's press ahead to analyze its 2024 financial outlook .

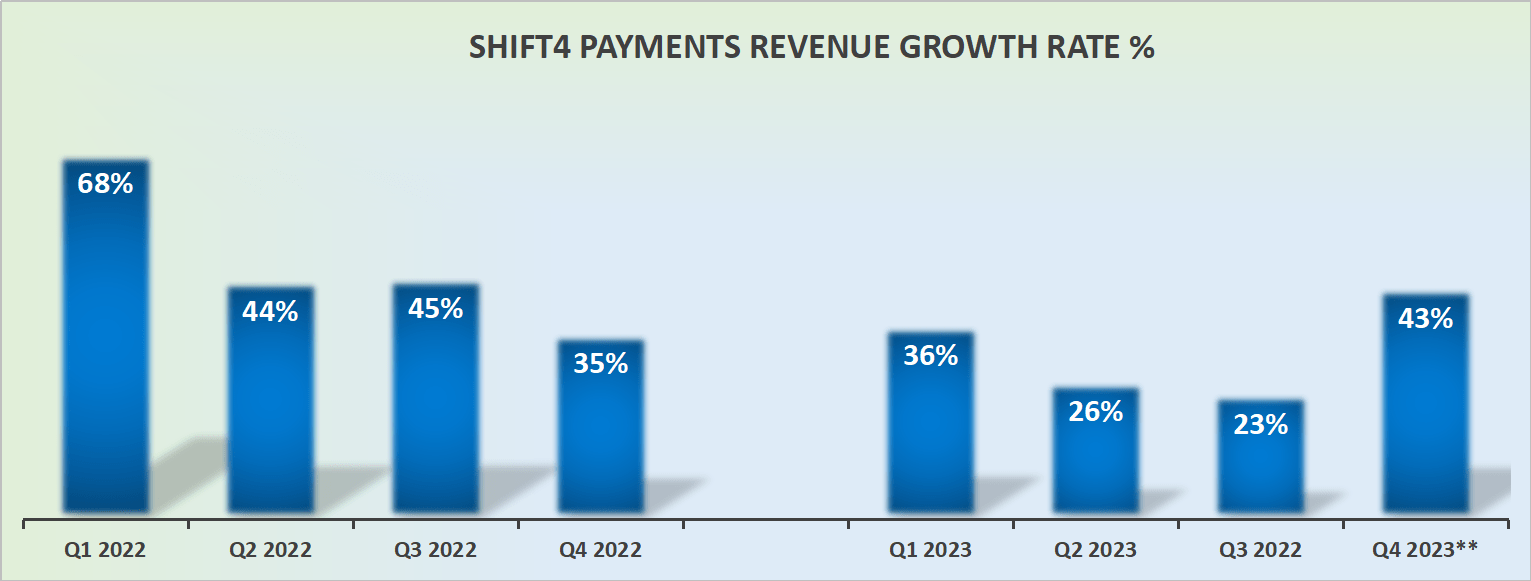

Revenue Growth Rates Require Interpretation

FOUR revenue growth rates; **includes acquisitions of Finaro

{kind=link}

Shift4 has made a large acquisition that will add substantial revenues to Q4. This implies that its nearly 45% CAGR revenue guidance is being meaningfully driven through several acquisitions, the most impactful being Finaro.

In fact, its organic growth rates are expected to come in closer to 28% CAGR. Consequently, it appears that for now Shift4's revenue growth rates have stabilized and we should not expect to see 2024 dipping down close to the low 20s% CAGR.

Profitability Profile in Focus

Shift4 Payments has demonstrated a commitment to profitability and margin enhancement. The company reported a robust gross profit margin of 70% for the quarter, marking a substantial improvement of over 550 basis points year-over-year.

This was complemented by an impressive 780 basis points increase in the adjusted EBITDA margin, reaching 51%. The prudent cost management strategy is evident in the consistent improvement in these margins.

That being said, while its legacy M&A, particularly the acquisition of Finaro, is expected to contribute positively to the business, it also introduces short-term challenges. The acquisition is anticipated to result in a temporary drag on adjusted EBITDA margins, emphasizing the complexity and transitional nature of integrating acquired entities.

FOUR shareholder letter

Putting aside the bumpiness in Shift4's share price, it appears that this business' free cash flows continue to tick higher with time.

What's more, management continues to not only reaffirm that it will reach close to $250 million of free cash flow in 2023, but they've actually upwards revised this figure slightly and it now points towards $260 million of free cash flow for 2023.

It now appears that without any heroics at all, simply from its ongoing momentum, Shift4 Payments could reach $350 million of free cash flow in 2024.

This would leave this stock priced at 15x forward free cash flows, which is perhaps one of the cheapest amongst its fintech cohort.

The Bottom Line

Shift4 Payments presents a compelling investment opportunity. The company's organic growth rates, estimated to be between 25% and 30% CAGR in 2024, underscore its dynamic presence in the market. What makes this investment even more enticing is the fact that this impressive growth is currently being undervalued, with the stock priced at less than 16 times forward free cash flows.

In a landscape where rapid growth often commands a premium, Shift4 Payments stands out as an anomaly, offering investors the chance to tap into a high-growth fintech sector at a remarkably attractive valuation. The company's commitment to profitability, evident in its strong financial performance and disciplined investments, further solidifies its position for sustained growth.

For further details see:

Shift4 Payments: Strong Growth At 25-30% CAGR In 2024, Priced At 16x FCF