LEAT - Shimano: FY2022 Results Review Updated Valuation

Summary

- Shimano reported better-than-expected FY2022 results.

- The company’s corporate governance and capital allocation align more with shareholders than ever.

- FY2023 guidance is conservative, even compared to our worst-case scenarios.

- I update Shimano’s fair value valuation with the better-than-expected FY2022 results and FY2023 guidance.

Shimano's primer

Shimano ( SMNNY , SHMDF ) is the world's largest bicycle parts and second-largest fish tackle manufacturer, commanding about 70% of the bike market and 20% of the fishing tackle market. It's a rare company that benefits from scale and differentiation advantages over competitors by operating the most advanced manufacturing capability, the broadest product range, and the largest distribution network.

Free cash flow per share (FCF/share) has expanded at a 17% CAGR in the past decade (15% in the past 15 years) and returned 24% CAGR on invested capital (22% in the past 15 years).

Today, the company is still headed by the same family and driven by the same mission, 'focusing on customer happiness and bringing them closer to nature.' And the future looks bright as eco-friendly transportation and outdoor leisure activities become more central to our lives.

This article reviews Shimano's FY2022 results. Read here for a detailed company analysis, including the market position, competition, risks, and valuation.

Shimano's FY22 results

{kind=link}

Shimano reported better-than-expected results for the financial year ending 2022 on Feb 14th, 2023.

Revenue came in at JPY 628B ($4.7B in USD), an increase of 15% compared to the prior year. The positive results were driven by resilient demand in US and Japan, while Europe and China's markets were sluggish. The bike segment's demand remains higher than pre-Covid levels despite the prolonged supply disruption coming from the Ukraine-Russia war and central banks' fight against inflation. The fishing tackle segment was robust in all regions besides the North American market.

Operating income came in at JPY 169B ($1.2B), an increase of 14.1% compared to FY2021.

Compared to the management FY22 guidance issued in Q3'FY22 results, the actual FY22 results were much better. The company beat revenue guidance by 7% and exceeded operating margin guidance by 4%.

{kind=link}

FY 2022 actual result on Feb 14th, 2023

FY2022 results also beat analysts' revenue estimate of JPY 605B or 4%.

Shimano closed the year with a cash balance of JPY 417B ($3.1B), up from JPY 375B ($2.8B) in 2021. Its financial strength is looking stronger than ever.

Shimano's corporate governance and capital return

Besides beating revenue and earnings estimates, Shimano improved its corporate governance and increased share repurchases and dividends.

More independent directors

For FY2023, the board has proposed to increase the number of outside directors to four from three, and it's the first year they have a female director. The change is positive in the long term, showing the company is continuously adapting to the modern operating environment.

Shimano's ESG

Share Buyback

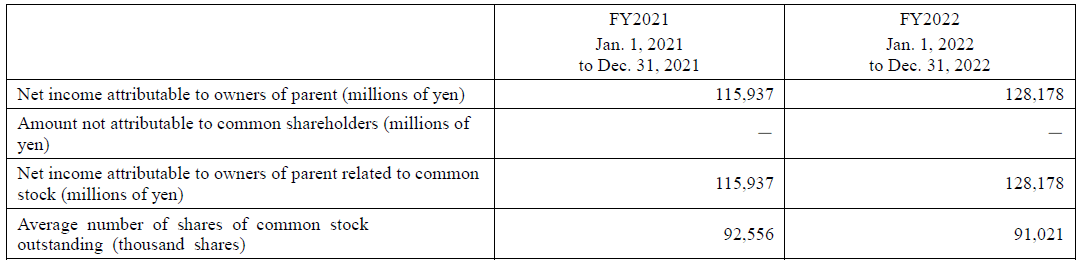

What is also positive is the company's growing appetite to buy back shares. FY2022, the company reduced share counts to 91M from 92.5M in FY2021. It spent JPY 34B ($257M) to repurchase 1.34B shares for an average of JPY 25,373/share.

At the current price of JPY 21,000 (or $16/ ADR share), that's a 2.2% buyback yield.

{kind=link}

It's a huge step, as the company barely bought back a meaningful amount of shares before 2019. The table below shows the company buyback activity in USD.

{kind=link}

Increased Dividends

The company also pays semi-annual dividends and has been increasing them since 2009. The FY2022 dividend continues the uptrend. The company proposed to pay a JPY 285 dividend per share in FY2023 or a 1.4% yield at the current price of JPY 21,000.

{kind=link}

If Shimano continues buying back shares (2.2% yield) and paying dividends (1.4% yield), shareholders could get roughly 3.6% in total in FY2023.

Shimano's FY23 guidance

{kind=link}

Shimano's management is known to be conservative. Unsurprisingly, they guided for FY2023 revenue and operating income to drop by 20% and 38%, respectively.

If history is a guide, my model suggests FY2023 will be at least JPY 53B, 6% higher than estimates. The current situation of inventories for completed bicycles also means the worst is over. The management reports that high-end-class bikes remained low, followed by higher inventory levels of middle-class and entry-class bicycles. Recent reports from Thule (THUPY) and MIPS ( MIPS ) also suggest the same picture. Shimano's core offering is mid-to-high-end parts, so the inventory headwind should go away by 2024.

Updated valuation

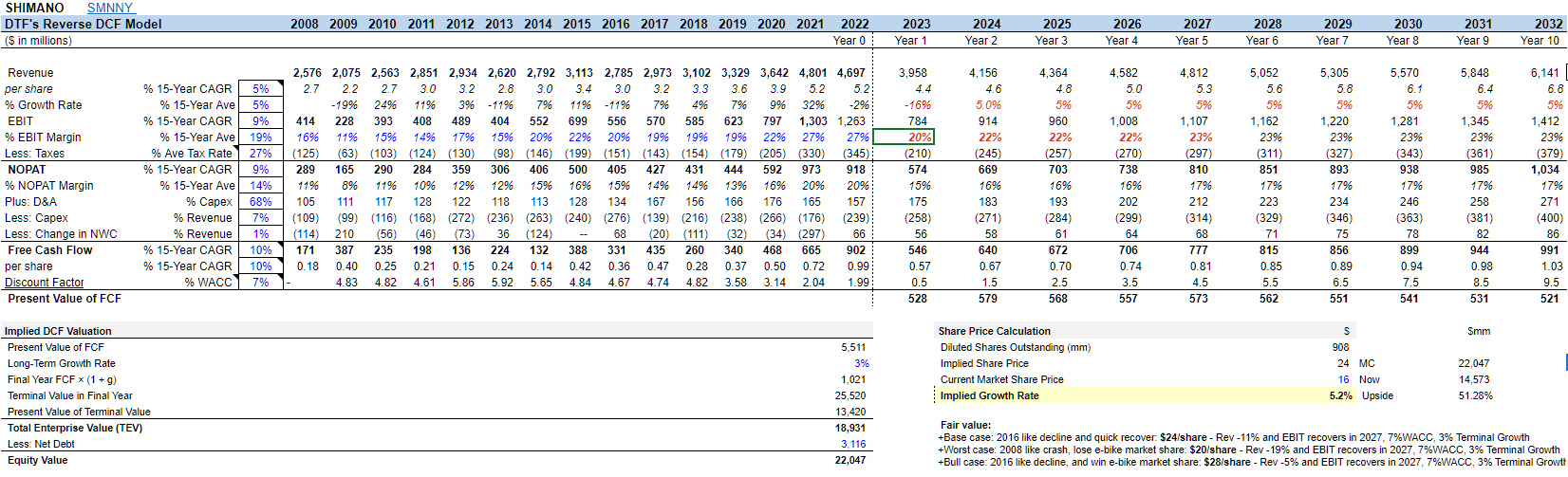

With the better-than-reported FY2022 and conservative FY2023 estimates, Shimano's fair value on a DCF valuation based on my estimates increased to $24/ ADR from $23/ ADR share.

Previously, I assumed the operating margin to be 18% for 2022 and 2023. However, actual results came in at 27% and guidance at 20%. Shimano's ability to maintain strong profitability convinced me to increase my operating margin assumption between 2023-2027.

{kind=link}

Reversing my DCF model to the current price of $16/ADR share shows that the market assumes Shimano doesn't grow until 2032.

Finally, its FY2032 PE multiple stands at 13x in the base case (maintaining market share and growing at the industry-wide rate). All methods point to a convincing buy at the current price.

Summary

The market was not excited by Shimano's FY2022 results. But I am. Fundamentally, everything has stayed the same. Shimano's FY2022 results showed improved sales of 15% vs. 8% expected and higher than bike-related peers, MIPS, THULPY, and LEATT, who saw their sales cratered during the year. Shimano's operating margin also performed much better than I expected, generating a 22% operating margin vs. 15%. Additionally, while inventory backlog remains a problem in the near term, the picture for Shimano's mid-to-high-end segment is already better.

Finally, investors are getting a slightly lower price today at JPY 21,000/share or $16/ADR share. I maintain my BUY rating and increase Shimano's fair price to $24/ADR share, representing a 50% upside.

For further details see:

Shimano: FY2022 Results Review, Updated Valuation