YAMHY - Shimano: Limited Recovery Profile Point To Expensive Valuations

2023-10-13 11:16:41 ET

Summary

- Shimano is the global market leader in cycling components with a 70% share in the mid to high-end market.

- Recent trading conditions have been difficult, with the company lowering its FY12/2023 guidance due to high market inventories and rising input costs.

- With no upside risk to earnings, the shares remain expensive on PER FY12/2024 24.3x on flattish growth, and we maintain our sell rating.

Investment thesis

Shimano ( SHMDF ) has experienced weak earnings to date in FY12/2023, due to high market inventories and limited demand recovery. We believe this situation will continue, with a very limited recovery profile into FY12/2024. With no upside risk to earnings, the shares remain expensive on PER FY12/2024 24.3x on flattish growth, and we maintain our sell rating.

Quick primer

Established in 1921 in Sakai City, Japan, Shimano is the global market leader in cycling components with an estimated 70% share in the mid to high-end market. The most significant geographic market is Europe, making up approximately 48% of total FY12/2022 sales. Shimano also manufactures fishing equipment such as rods, reels, and rowing equipment. It has 13,000 employees and President Taizo Shimano is a founding family member. Manufacturing is based in Japan, China, Singapore, Malaysia, and the Philippines. Its single largest customer in FY12/2022 was Germany's bike parts specialists Paul Lange & Co. Other customers include Taiwan's Merida Industry ( 9914.TW ) and Giant Manufacturing ( 9921.TW ). Key peers are SRAM of the US, Campagnolo of Italy, Yamaha Motor ( YAMHF ), and Bridgestone ( BRDCY ).

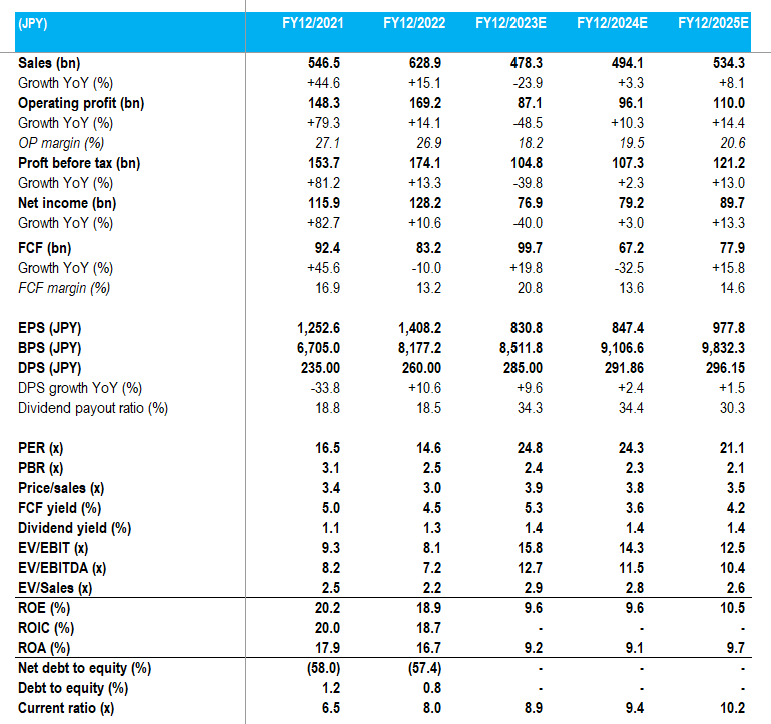

Key financials with consensus forecasts

Key financials with consensus forecasts (Company)

{kind=link}

Updating our view

We are updating our view from October 2022 where we rated Shimano as a sell, with the key concerns being cost inflation and expectations of negative earnings growth YoY for FY12/2023.

Recent trading conditions have been difficult, with the company lowering FY12/2023 guidance ( page 4 ) on the back of a slow start to the year; operating profit is expected to decline 59% YoY to JPY83 billion. The key concerns indicated by the company are high levels of market inventories, rising input costs, and the depreciating Japanese yen, which is pushing up domestic prices. High market inventories point to a relatively saturated market, following on from post-pandemic demand.

Despite the magnitude of the FY12/2023 downward revision, the shares have held up relatively well. We want to assess the demand outlook for the next 12–18 months, and whether the company has any available options to unlock shareholder value.

Limited recovery into FY12/2024

Global bicycle demand appears set to bottom in 2023 and enter a recovery phase in 2024 according to some commentators, and this sentiment appears to be echoed in current consensus forecasts (please see table above) indicating a small increase in sales YoY of 3% in FY12/2024. Whilst this is possible, we are currently cautious about all forms of discretionary consumer spending (including musical instruments ( Yamaha ) and travel ( Booking Holdings )) and believe that bicycle demand may bottom but remain relatively flat in FY12/2024 and FY12/2025. The reasoning is purely down to our negative stance on low consumer confidence, which will curtail any major recovery in non-staple items. Outdoor recreation demand has been strong post-pandemic, but we expect this to settle down into FY12/2024.

The rise in the cost of living could potentially drive bicycle demand as fuel and commuting costs increase - we are yet to see sustained evidence of this, although post-pandemic demand was in part attributed to this. Although secular drivers such as urbanization, environmental concerns, and traffic congestion should contribute to an increase in bicycle popularity, we believe consumption will generally remain focused on essential items. Financing costs have risen for consumer credit, making purchases more difficult, with U.S. average credit card interest rates being the highest since LendingTree began tracking rates monthly in 2019. There have been subsidies available for e-bikes in countries such as the US, France, Sweden, and Canada, but there appear to be no other major developments in major markets that would drive demand. Europe is the key market for the company, and recent economic sentiment indicators remain in a negative trend.

Positive developments for total shareholder returns

The company conducted a share buyback in March 2023 to the value of JPY13 billion, equivalent to a return of 0.7%. Although this does not appear to be particularly generous, the company has made strides in FY12/2023 by increasing the dividend per share from JPY260 to JPY285. The resultant payout ratio is 37%, a major increase from 18.5% in FY12/2022.

With an approximate net cash balance of JPY490 billion/USD3.3 billion, inevitably the market expects that capital will be allocated to improving shareholder returns, which in turn provides valuation support. However, at this current juncture, return on equity is expected to halve to 10% in the medium term compared to the recent 20% level with modest growth expectations.

Valuation

On consensus estimates, the shares are trading on PER FY12/2024 24.3x, and dividend yield of 1.4%. As a high-quality franchise, we expect to see relatively premium valuations and Shimano fits this billing, but the dividend yield is disappointingly low considering the cash-rich balance sheet and free-cash-flow generative nature of the business.

With limited earnings upside, suitable multiples for a quality business, and low shareholder returns, we believe the shares remain unattractive.

Thesis catalysts

We expect to see another downward revision to FY12/2023 company guidance, as demand continues to falter, particularly in Japan and emerging markets. There may be signs that market inventory levels remain elevated into FY12/2024.

Risks to the thesis

A combination of a strengthening Japanese yen, increasing consumer confidence, and falling credit costs drive demand. Special government subsidies for e-bikes could help with replacement and upgrade activity.

Conclusion

When an attractive market leader sees its operating margins fall from recent highs of 27% to below 20%, it would be expected that with normalizing business conditions, profitability will recover in the short to medium term. Our view is that demand remains relatively flat, placing pressure on valuations and denoting downside risk, despite the potential for increasing share buybacks. With our low expectations of a demand recovery, we maintain our sell rating on the shares.

For further details see:

Shimano: Limited Recovery Profile Point To Expensive Valuations