SUMCF - Shin-Etsu Chemical: Limited Downside But Earnings Visibility Appears Low

2023-10-10 04:55:22 ET

Summary

- Shin-Etsu Chemical's exposure to the housing and construction sector poses a downside risk, with limited upside risk from the semiconductor market.

- The company's Q1 FY3/2024 financial results showed a decline in sales and operating profit, with guidance pointing to continued weakness for FY3/2024.

- The US housing market remains stable, but falling consumer confidence and weak demand in China are negative factors for Shin-Etsu.

Investment thesis

Shin-Etsu Chemical's ( SHECF ) exposure to the housing and construction sector points to downside risk, with limited upside risk from the semiconductor market. Although a well-run business, we see no immediate reason to invest in the shares and reiterate our neutral rating.

Quick primer

Shin-Etsu Chemical is Japan's largest chemical company and the global leading manufacturer of PVC by volume (no. 2 is Formosa Plastics in Taiwan) used widely in the construction industry. It has a diversified product base covering Functional Materials (such as cellulose derivatives and synthetic pheromones), Electronics Materials (no. 1 global leader in substrate wafers with around 30% share, no. 2 is Sumco ( OTCPK: SUMCF )), and Processing and Specialized Services (wrapping films and wafer containers).

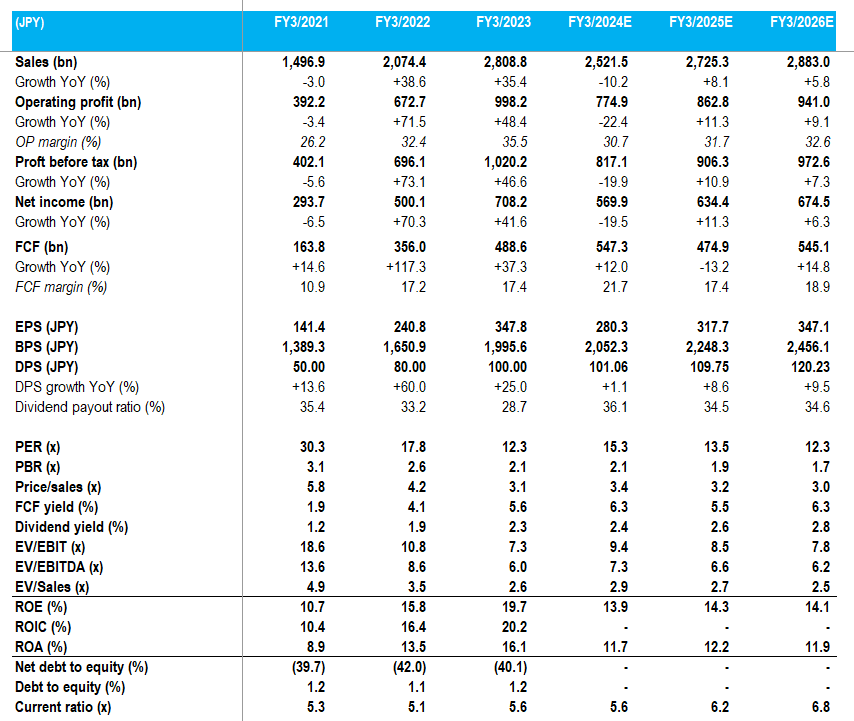

Key financials with consensus forecasts

Key financials with consensus forecasts (Company, Refinitiv)

{kind=link}

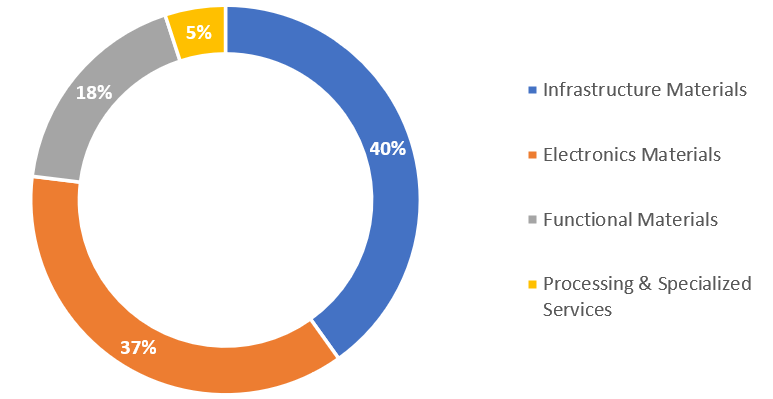

Q1 FY3/2024 sales by segment

Q1 FY3/2024 sales by segment (Company)

{kind=link}

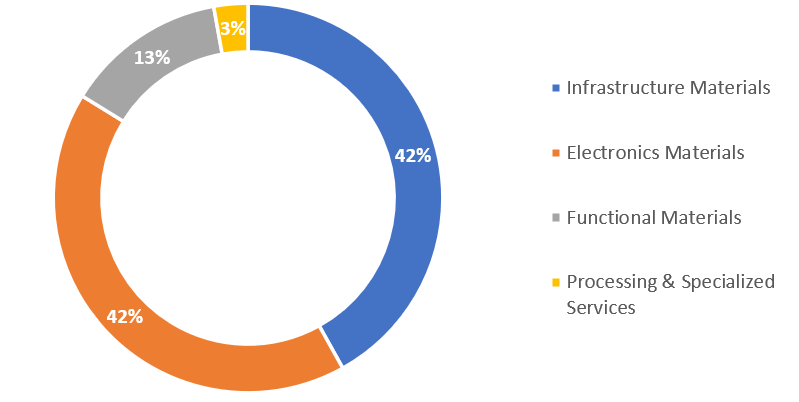

Q1 FY3/2024 operating profit by segment

Q1 FY3/2024 operating profit by segment (Company)

{kind=link}

Updating our view

We are updating our hold rating from July 2021 , where we felt that prospects would start to normalize into FY3/2023 after a bumper growth profile for FY3/2022 where operating profit grew by over 70% YoY.

Q1 FY3/2024 results presented a mixed picture, with sales declining 9% YoY and operating profit falling by 24% YoY. The company issued FY3/2024 guidance, pointing to FY sales dropping by 18% YoY and operating profit by 30% YoY - management commented that conditions are expected to be more challenging into the latter half of the year. However, with the yen depreciating from later summer, there is a tailwind for Shin-Etsu's earnings (company guidance is USDJPY 135 versus the current 149).

For the Infrastructure Materials segment, housing and construction demand has been stable in the US where price hikes have been introduced, but China has been weak. In the Electronic Materials segment, it would appear that the semiconductor industry remains in a state of inventory adjustment, with the company expecting growth to resume from 2024 to 2025, driven by AI.

We want to assess growth prospects into FY3/2025 and FY3/2026, given that current consensus forecasts show that recent earnings peaked in FY3/2023.

Housing shortage and consumer confidence

The US housing market may experience higher-for-longer interest rates, but housing stock remains at low levels prompting the need for construction. However, elevated credit costs and falling consumer confidence have led to builder sentiment falling in September 2023 . We expect this trend to persist into the second half of the year, which would be a negative development for building suppliers such as Shin-Etsu.

China's real estate market remains weak and with our expectations of falling completed floor space in 2023 as well as 2024, demand for PVC will continue to decline. The company has raised prices in China but we cannot see this trend being sustainable with weak underlying demand.

Whilst we have no edge on the outlook for interest rates worldwide, geopolitical risk has increased with heightened tensions in Israel and Gaza. Increasing energy prices could impact inflation again, similar to Russia's invasion of Ukraine in February 2022.

Semiconductor outlook

Recent comments from the company regarding the outlook for their semiconductor business are mixed. On a positive note, the wafer market is expected to turn positive YoY from around January 2024. On the other hand, EUV mask blank demand remains relatively limited, which is odd considering the increasing need for AI, and for high-end mobile chipsets. Wafer demand was also expected to weaken QoQ into Q2 FY3/2024, and there is currently no indication that demand will ramp into H2 FY3/2024. The consensus view is that the semiconductor industry will recover in CY2024, with electronic sales surpassing the peak seen in 2022 - we disagree, as we currently see no major drivers in the consumer electronics market.

Whilst the long-term outlook for Shin-Etsu's Electronics Materials business appears stable, we do not currently see any positive catalysts to indicate a demand recovery in the short to medium term.

Valuation

On consensus estimates, the shares are trading on PER FY3/2025 13.5x, and on a dividend yield of 2.6% (on a 34.5% payout ratio). With high profitability and strong market positioning, the company is a high-quality franchise and as such valuations do not look particularly expensive.

Management has been focused on total shareholder returns, with a current JPY100 billion/USD660 million share buyback program in place. However, this is equivalent to 1.2% of shares outstanding, resulting in a total return of 3.8% (including dividend yield) which is palatable but not that attractive.

We believe current valuations are fair for a quality cyclical business navigating difficult macro conditions.

Thesis catalysts

Despite the FX tailwind from a depreciating yen, the demand environment begins to weaken for Infrastructure Materials in H2 FY3/2024. With semiconductor demand experiencing a delay in an outright recovery, the company will miss FY3/2024 guidance.

Risks to the thesis

Central banks will start to telegraph that interest rates will begin to fall in early 2024, prompting increasing consumer and business confidence. Both consumption and business investment will recover in earnest.

Conclusion

Earnings visibility at Shin-Etsu does not appear particularly high at present, and this is to be expected given the rapidly changing external environment. Whilst we believe company management will navigate the business through this period without too much drama, their limited stance on shareholder returns makes us believe there is no immediate hurry to invest in the shares. There may be limited downside, but we reiterate our neutral rating.

For further details see:

Shin-Etsu Chemical: Limited Downside But Earnings Visibility Appears Low