SSDOY - Shiseido: Switching From Defensive To Offensive Business Strategy

Summary

- Shiseido's Shift 2025 and beyond business strategy aims to enhance the company's brand equity globally through innovation and cost optimization.

- Shiseido seeks to increase its core operating profit in the Japanese beauty business alone to JPY50 billion ($380 million) by 2025.

- Over the next 3 years, Shiseido's CapEx will entail stronger marketing initiatives, innovation, and increased labor.

The multi-billion dollar Japanese cosmetic market is led by local brands that are also double up as multinational beauty companies. Major players include Shiseido Company, Ltd ( SSDOY ) Kao Corporation ( KAOCF ), KOSÉ Corporation ( KSRYY ), Pola Orbis Holdings ( PORBF ), and Fancl Corporation ( FACYF ). Shiseido announced its Q4 2022 earnings results where it reported revenues of $2.32 billion representing a decline of 7.59% (YoY). It missed Wall Street estimates by $45.65 million in the quarter while EPS missed forecasts by $0.09.

Thesis

In the execution of its medium-to-long-term strategy dubbed "Shift 2025 and Beyond" Shiseido seeks to conduct structural reforms including divestitures and an aim to grow sales motivated by brand values. The company is focused on increasing the number of app downloads in e-commerce while building a loyal user base in the online-merge-offline (OMO) platform. Shiseido is working to raise the sales ratio of skin beauty/ make-up products that respond to the dynamic market. Other measures include constructing new factories and deploying new logistical systems to increase profitability. However, the company has had to face the ever-growing challenge of new competitors, the varying cultural market, and trend dynamics including prolonged Covid19 restrictions such as mask rules in Japan and global inflationary pressures.

Structural Reforms

Shiseido seeks to increase its core operating profit in the Japanese beauty business alone to JPY50 billion ($380 million) by 2025. The company's net income in the quarter ending on September 30, 2022, stood at $88.4 million or about $260 million for the FY 2022 meaning that it seeks to grow its net profit by at least 1.5 times in less than 2 years. Coming from Japan alone will be a significant achievement considering it scored JPY50.4 billion as profit before tax from finance and investment share profit. SSDOY’s EBITDA stood at JPY 102.4 billion indicating a 10% (YoY) growth.

Shiseido's full-year sales grew 5.7% (YoY) for the FY ending on December 31, 2022, to about JPY1.07 trillion ($8.1 billion). Net profit declined 27.1% (YoY) to JPY34.2 billion ($260.6 million). Additionally, operating profit also dropped 53.7% (YoY) indicating the need to grow its Japanese business while prioritizing brand, innovation, and customers. Shiseido announced that it was working to attain a core operating margin of 12% by 2025 and 15% in 2027.

Since 2021, the behemoth beauty company has pursued the "Win 2023" initiative to concentrate on rich areas such as skincare to grow its profitability. Shiseido is intending to conduct structural reforms on sectors that denoted negative performances worth about JPY200 billion in the EMEA region and the Americas. In the US, it owns brands such as Drunk Elephant, NARS, and the global beauty license for Tory Burch. In a deal struck in 2021, Shiseido agreed to sell its personal care business (including Tsubaki) and skincare products brands such as Senka to private equity company, CVC Capital Partners. The deal worth about JPY160 billion (about $1.2 billion in today’s exchange rate) was supposed to lead to the creation of a spin-off company in a 35:65 joint venture. In its Q4 2022 earnings call. Shiseido explained that the divestiture led to improved consolidated results from the EMEA and the Americas that were deemed struggling since 2020. The sales ratio of skincare brands exceeded 70% (YoY) denoting better performance into 2023.

In my view, Shiseido should adopt features of artificial intelligence or AI and augmented reality or AR while expanding its Asian market to offer customized experiences to clients. This will give the new brands a cutting-edge and more competitive nature. It is all about customer acquisition and client conversions both online and in physical stores. For instance, Alibaba ( BABA ) owns Lazada ( LZDA ), a leading e-commerce platform in Southeast Asia. Back in September 2022, BABA injected an additional $912 million to not only grow Lazada’s valuation but also increase international sales. BABA’s online sales in China were slowing down into Q4 2022, and the investment in Lazada known for using AI and AR will strengthen sales.

"Through a strategic distribution partnership agreement with Global SS Beauty Brands Limited- a subsidiary of India’s Shoppers Stop Limited," Shiseido announced the launch of NARS Cosmetics in India. Through this venture, Shiseido aims to stabilize its skin beauty brand portfolio in the Asia-Pacific region. All these partnerships are under the medium-to-long-term banner of Shift 2025 and beyond supported by a new management structure.

Intended Cash flow and Marketing dynamics

Shiseido aims to generate a cash inflow exceeding JPY400 billion from this investment over the next three years. The company's CapEx will entail stronger marketing initiatives, innovation, and increased labor. I expect part of the cash generated to be allocated toward IT, e-commerce, and digital transformation mechanisms. We are looking at a swing from defense to offense with the four main brands: NARS, Drunk Elephant, Cle de Peau Beaute, and Shiseido all contributing directly to top-line growth.

For instance, sales from NARS on a global level exceeded JPY1.2 billion with the company looking at a sellout of more than JPY150 billion in the medium-to-long-term range. In my view, Shiseido needs to target the men's market to increase sales of skincare and male skincare seeing the female market is already facing stiff competition. Over the next three years, the company allocated JPY100 billion towards marketing with further M&A opportunities needed to ensure it meets its ROI. Globally, the beauty and personal care industry was estimated to be worth $481.6 billion in 2022 with forecasts indicating it will rise to $787.8 billion by 2028. This industry is expected to grow by a CAGR of 5.12% from 2023 to 2028.

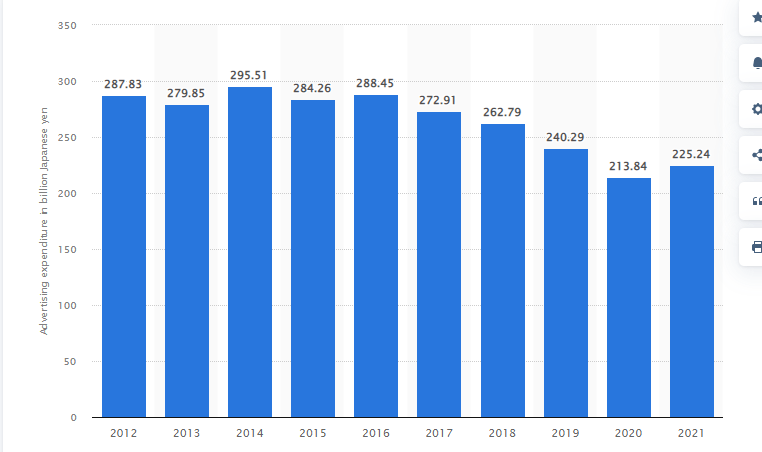

The advertisement expenses in the Japanese cosmetics industry (using traditional media) in 2021 reached JPY225.2 billion. This value represented an increase above JPY11 billion or an increase of 5.13% (YoY).

{kind=link}

Shiseido’s e-commerce sales in Q3 2022 registered a mid-single-digit growth. In September 2022, the company launched a member service app, Beauty Key that among other benefits rewards customers with a 5% cash back after registration and purchasing of a target product. This and more products are designed to expand Shiseido's loyalty base and maximize the gross profit margin.

Another aspect of the growing realization for Shiseido is that it will work towards cost reductions. The company hopes to lower its costs, especially on selling, General, and administrative (SG&A) by 60% (YoY). Shiseido hopes that with its marketing efforts, Japan will be proactive in its product launches and innovations. The user loyal base is also expected to expand from a medium and long-term perspective especially in China after its recovery from the lockdowns in 2022.

China’s skincare market was valued at $16.35 billion in 2022 and has been described as the fastest-growing segment in the country. Further, foreign cosmetic brands such as Shiseido are considered of higher quality as compared to local brands. The biggest trends include anti-aging, natural creams, and unisex brands.

Shiseido’s financial target

Under the “Shift 2025 and beyond” Shiseido aims to grow its net sales by 8% in the next three years with the 2022 sales excluding business transfers of JPY0.9 trillion as a starting point. It will then hope to move along the growth curve at a CAGR of 6% until 2027 (that is 2026 to 2027) before establishing a benchmark for growth efficiency. Additionally, Shiseido is looking towards attaining a free cash flow of JPY100 billion in 2025 after the structural reforms and construction of new factories. The company sees its EBITDA margin surge 18% (YoY) in 2025 and drop 20% by 2027 boosted by an expanded market share, optimization of fixed costs, and an improvement in marketing activities.

Risks to Consider

Shiseido stated that its net profit into FY 2023 is likely to drop by 18.1% (YoY) to JPY28 billion or $260 million. This decline will be reflected in the company's net sales which may decline 6.3% (YoY) to JPY1 trillion or $7.6 billion. Lower earnings may affect shareholder returns in the medium term.

The Japanese fashion business may take longer to recover. This delay is due to the impact of Covid19 that took two years more in this country as compared to others in EMEA or the Americas. Members of the public are still encouraged to wear masks with new guidelines requiring passengers to wear face masks on trains and buses or in congested public locations. Of note is that the Japanese central government is set to ease the Covid19 guidelines hopefully on March 13, 2023, a move that will boost economic and social activities. Research has shown that wearing protective face masks has directly affected the beauty industry by lowering sales. The most affected areas are color cosmetics like facial makeup and lipstick.

Bottom Line

Ahead of its next earnings date on May 12, 2023, Shiseido is enhancing its activities to ensure it reaps big in 2023. Under the Shift 2025 and beyond the program, SSDOY is looking to review its main brands, expand into new locations such as India, divest some of its subsidiaries, perform continuous market execution, and follow a cost structure to increase profit generation. However, I feel that the stock may face further downside owing to continued Covid19 restrictions in Japan and delayed economic recovery from China. Still, this stock has the potential to surge and therefore, I will suggest a hold rating for now.

For further details see:

Shiseido: Switching From Defensive To Offensive Business Strategy