SHLS - Shoals: Expanding The EBOS Pie

Summary

- Demand for Shoals' EBOS solutions exceeded expectations in Q3.

- Backlog grew significantly demonstrating Shoals' unique proposition in EBOS.

- eMobility and storage provide exciting opportunities and are expanding the EBOS pie.

- I am excited about what's in store in 2023.

Shoals Technologies ( SHLS ) had a good year in 2022.

The stock price performance may not immediately suggest this, maintaining that Shoals-like volatility that holders have come to expect, but the underlying business strengthened.

The company delivered growth that exceeded aggressive expectations and is zoning in on new markets moving into 2023. With Shoals raising the lower end of Q4 guidance, a strong finish to FY22 is expected.

The business is proving to be a valuable enabler of the renewable transition as it moves into new verticals, this is arguably one of the biggest and most important trends of the coming decades. I am bullish on its prospects.

Q3 results recap

Although the Q3 results were delivered around two months ago now, I will give readers a refresher along with some of my thoughts.

Here is a summary of the key takeaways:

- Revenue of $90.8M (+52% Y/Y)

- Adjusted EBITDA of $26.6M (+57% Y/Y)

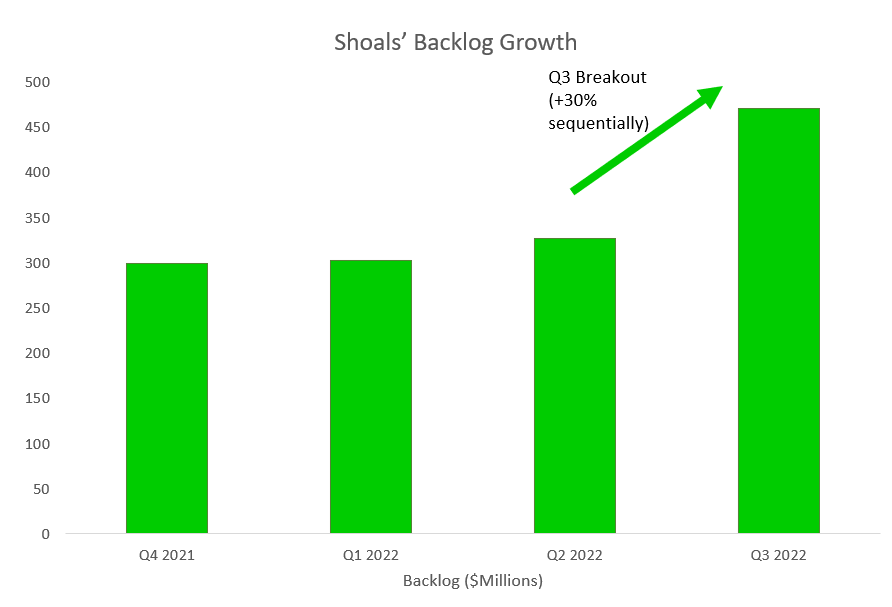

- Backlog of $471M ( +74% Y/Y )

I have highlighted the backlog growth because I believe it is the best indicator of demand for Shoals's products. The backlog underpins the EBOS (electrical balance of systems) providers' growth prospects, which is vital for a premium-priced solar name that is pulling forward a lot of future growth in today's prices. $144M of that backlog build came in Q3 alone, reinforcing Shoals as the go to provider of EBOS solutions. To compare, Shoals saw an increase of just $25M in Q2. This has given me greater confidence that Shoals has the best patented offerings in the market.

Compiled by author from company accounts

{kind=link}

Operating cash flow was $11.7M for the quarter, down around $8M sequentially. This decline can be attributed to a decrease in working capital, management expected to see a decline in OCF as they invest in expansion - Q2 was a one-off in that regard.

The strong demand for Shoals' suite of solutions allowed the company to raise the bottom end of their guidance, they now expect FY revenue to be between $310 to $325M with adjusted EBITDA at $80-$86m, this constitutes to a margin of 26.6%. The company based this on:

Current market conditions and input from our customers and team.

To grow revenue by 49% and EBITDA by 37% in 2022 is seriously impressive considering the considerable headwinds that Shoals had faced at the start of the year. Most notably, the significant reductions in solar installations seen as a result of price increases and supply chain constraints.

Shoals' stock price has remained volatile since the news, initially surging over $30 before pulling back to the low $20s and now recovering again. If an investor is looking for an argument against the efficient market hypothesis, I don't think they need to look much further than Shoals. It is volatile and susceptible to large stock price swings that are unrelated to any fundamental changes in the business. I remind investors that stock prices are generally a lot more volatile than the underlying business.

Move into eMobility

Growth stocks should have a large 'pie' ('TAM') and should be taking a large and increasing share of that pie. That's the strategy for Shoals and it's working so far. There are a lot of tailwinds in solar alone, the same applies to eMobility. There is no revenue segment breakdown at this point (likely because pure solar and America represent a significant part of revenue) but EV share is expected to make bigger contributions - it is already contributing to backlog according to Jason Whitaker on the conference call :

From an e-mobility perspective, obviously, very excited about what we've been able to accomplish, launching that product out. What I can tell you is, it is contributing to our backlog and awarded orders and expect that will continue to be the case over time. Feedback from customers has been nothing short of amazing and very excited that we've been able to accomplish not only a successful launch, but launch over 15 different states with validating that value proposition that we're able to bring with that 20% to 30% savings on installation time and cost while also maintaining our average corporate margin profile. So very, very, very exciting jobs from that perspective and only see that continue to grow.

Gearing up for 2023 - an exciting year for Shoals

Backlog to delivery time (when they can actually record revenue) is generally 9-12 months, so backlog growth in Q4 is going to be an important indicator for the revenue growth we should expect to see in 2023. The market sees $506M in revenue with EBITDA of $154M, this would give Shoals an EBITDA margin of 30.4%, up 300bp Y/Y.

I am excited by the eMobility opportunity along with Shoals' move into battery storage. In both cases the opportunity afoot is very big, EV infrastructure and storage are both seeing large capital inflows and huge growth is expected. BloombergNEF forecasts say that the global energy storage market to grow 15-fold by 2023, yes that's correct - 1500%.

BloombergNEF

Shoals only developed their storage solutions in 2021, with what they called the launch of 'Shoals 2.0', so they are really at the start of their journey into the energy storage industry. Shoals has the benefit of using existing expertise with Solar EBOS and existing partnerships with large EPCs to develop a footprint in storage.

The company is focusing on both solar with storage and storage as a standalone - this will allow them to build up credibility in storage through agreements that provide a mix of solutions. The company announced in November that it would supply BLA and storage solutions to one of the largest solar plus projects in the U.S when complete. This is a significant milestone for Shoals in becoming a bigger competitor in the storage field.

This demand has come with a specific focus on Quality, which is really at the center of what Shoals' does and is its edge against competitors. Combining quality and an understanding of customer needs with efficiency is the company's specialty and I expect the 'quality gap' to continue to expand as the industry evolves and Shoals scales and onboards a larger number of partners.

The need to improve energy security in the western world has become a significant focus since the onset of the Ukrainian-Russian war and whilst 2022 was the year of oil and gas, it has also set the renewable industry up for accelerated growth in the future as countries look to increase energy capacity while also focusing on sustainability.

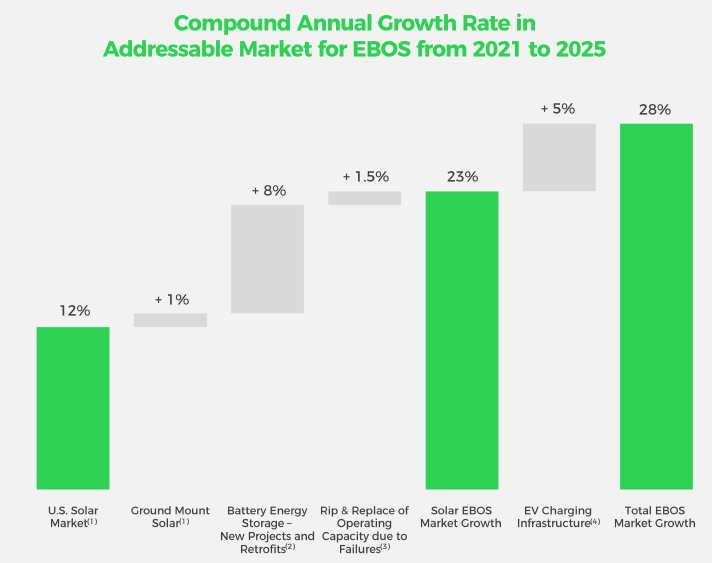

The renewable industry struggled in 2022 as a result of rising costs and supply chain disruptions but many of these issues started to alleviate at the end of the year. Even with these struggles, solar was the shining star and the same is expected in 2023 - growth is anticipated to come in at 20-30%. Solar energy is expected to surpass coal power by 2027 with EBOS, more specifically, growing even faster:

{kind=link}

Risks

CEO, Jason Whitaker, will be stepping down from his role in early 2023 due to health reasons. Mr. Whitaker has done a phenomenal job during his 13-year tenure at Shoals and I would like to wish him well in the future. This leaves some uncertainty regarding succession but I am confident they will find a suitable replacement before the end of March.

Shoals' stock is also expensive based on today's prices, the stock is trading on 32x '23 EBITDA, with First Solar ( FSLR ) as a comparison trading on 28x '23 EBITDA. I think the growth potential of Shoals is larger with the move into EV charging infrastructure and storage, Shoals' TAM has expanded significantly and I believe they can take a larger share of both of those markets through their innovative EBOS technology.

Finally, Shoals's debt stood at $274M at the end of Q3 while the cash position was just $10M. Shoals recently announced an equity offering of 2 million class A shares to help fund the termination of its Tax Receivable Agreement ($58.1M), this couldn't be funded by existing resources leading to the offering. The cash position is quite precarious but the operating cash flow is healthy and management have shown they can manage this cash position well.

The Bottom Line

Shoals is providing the critical 'plumbing infrastructure' for some of the largest solar projects in America. After building up its EBOS expertise over a long period, the company is now moving into new verticals; eMobility and storage, both of which I believe provide significant growth opportunities for the business.

Like much of the renewable industry, Shoals charges a premium, but I believe it's a premium worth paying. The solar enabler isn't the first stock that comes to mind when the renewable energy industry is discussed but its critical role in energy infrastructure will prove to be invaluable as the industry scales in my opinion. Long Shoals.

For further details see:

Shoals: Expanding The EBOS Pie