SHLS - Shoals Technologies: High-Quality Business In A Promising Niche

2023-08-21 04:00:19 ET

Summary

- Shoals is a leading provider of electrical balance of system solutions and components for solar, battery storage, and EV charging applications.

- The company's revenue has tripled in the last five years and profitability metrics demonstrated a strong dynamic.

- SHLS stock has seen a 20% decline this year but is considered attractively valued given its revenue growth profile and positive FCF margin.

Investment thesis

Shoals Technologies Group ( SHLS ) operates in a promising electrical balance of system (EBOS) solutions niche in the clean energy industry. The company is a market leader in this new industry and demonstrates impressive profitability dynamics despite its relatively small scale. That makes the company well-positioned to reinvest in innovation and marketing to fuel aggressive revenue growth. With scaling up, it is highly likely that profitability metrics will expand notably. Despite a solid broader market year-to-date rally, SHLS stock price declined notably. While my valuation analysis suggests the stock trades are close to the fair value, I think market leaders with massive growth potential should trade at a premium. That said, I assign SHLS a "Buy" rating.

Company information

Shoals is a leading provider of EBOS solutions and components for solar, battery storage, and electric vehicle (EV) charging applications, selling to customers primarily in the U.S.

The company's fiscal year ends on December 31. SHLS disaggregates its revenue from contracts with customers based on product type. Revenue by product type is disaggregated between system solutions and components. According to the latest 10-K report, System solutions revenue represented about 78% of the total sales in FY 2022.

{kind=link}

Financials

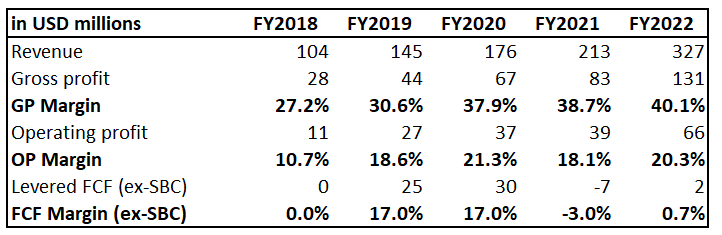

Shoals went public in January 2021, so we have a relatively short earnings history available. But a five-year period should be sufficient to see major trends in financial performance. The company's revenue more than tripled in the last five years, meaning a 33% CAGR. The gross and operating margins improved significantly as the business scaled up. The free cash flow ((FCF)) margin also looks healthy, though it has been volatile over the analyzed period.

{kind=link}

Having solid profitability metrics means the company can maintain a healthy financial position. The robust balance sheet has a low leverage ratio and strong liquidity metrics. SHLS is in a net debt position, though. But I do not think it is a problem, because the company consistently generates positive FCF, and the covered ratio looks comfortable at above 4. The company does not pay dividends, and share buybacks have been insignificant in recent years. I think that is reasonable because it would be more efficient to reinvest in innovation to fuel aggressive revenue growth and capture a more significant market share. That said, I do not expect any dividend to be distributed in the foreseeable future.

Seeking Alpha

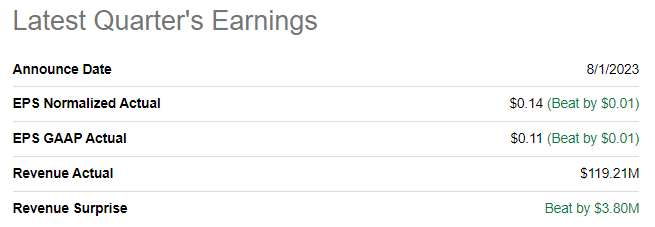

The latest quarterly earnings were released on August 1, when the company topped consensus estimates. Revenue growth demonstrated strong momentum, with a staggering 62% YoY increase. The adjusted EPS doubled, which is a solid sign, especially given low levels of share buybacks. The gross margin expanded from 39% to 42%, and the operating margin also demonstrated strength by expanding from 18% to 27%. Wider profitability was achieved by a more favorable revenue mix and enhanced operating efficiency. Shoals ended Q2 with a record $546 million backlog, which is a 67% YoY increase. During the earnings call , the management reiterated its full-year guidance, which is good amid the current uncertain macro environment. They also shared their vision regarding the new product pipeline, and I like that the company expands its offerings portfolio, which means more cross-selling opportunities and higher potential in gaining new customers.

{kind=link}

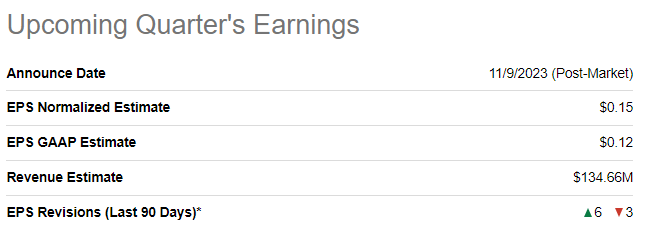

The upcoming quarter's earnings are scheduled on November 9. Revenue is projected by consensus to sustain a stellar growth rate, with an expected 48% YoY growth. The adjusted EPS is expected to be in line with revenue growth and expand from $0.10 to $0.15.

{kind=link}

According to the latest 10-K report, Shoals claims the company is significantly larger by revenue than its next largest competitor. It is difficult to assess because SHLS's main competitors are non-public companies, and their financial information is not disclosed. Being the market leader in a promising EBOS market makes Shoals well-positioned to benefit from secular tailwinds. The industry is expected to compound at about 19% CAGR by 2026, which is a bullish sign. The company's solid profitability gives it more opportunities to reinvest in innovation and marketing. It is also important to underline that EBOS is required for every solar, EV charging, or energy storage project regardless of size, location, or technology. Shoals is leading this market because of its "combine-as-you-go" system, which enables project owners to install the equipment faster, meaning less costs. Creating real financial value for its customers makes Shoals a good partner for project owners and EPC operators.

{kind=link}

Bears might argue that the company's technology might be replicated, but Shoals' intellectual property is very well protected legally by patents. The company works hard to expand its offerings to the EV charging niche. While the EV charging industry itself has very bright growth prospects due to the rapid EV adoption, we see governmental support to boost EV adoption, which is also a solid tailwind for SHLS. Another major growth opportunity for Shoals is international expansion. The company does not disaggregate its revenue by country, but financial statements suggest that a significant part of sales is generated in the U.S. That said, there is a vast potential for revenue growth if the company expands its sales internationally. All in all, I am optimistic about Shoals' growth prospects.

Valuation

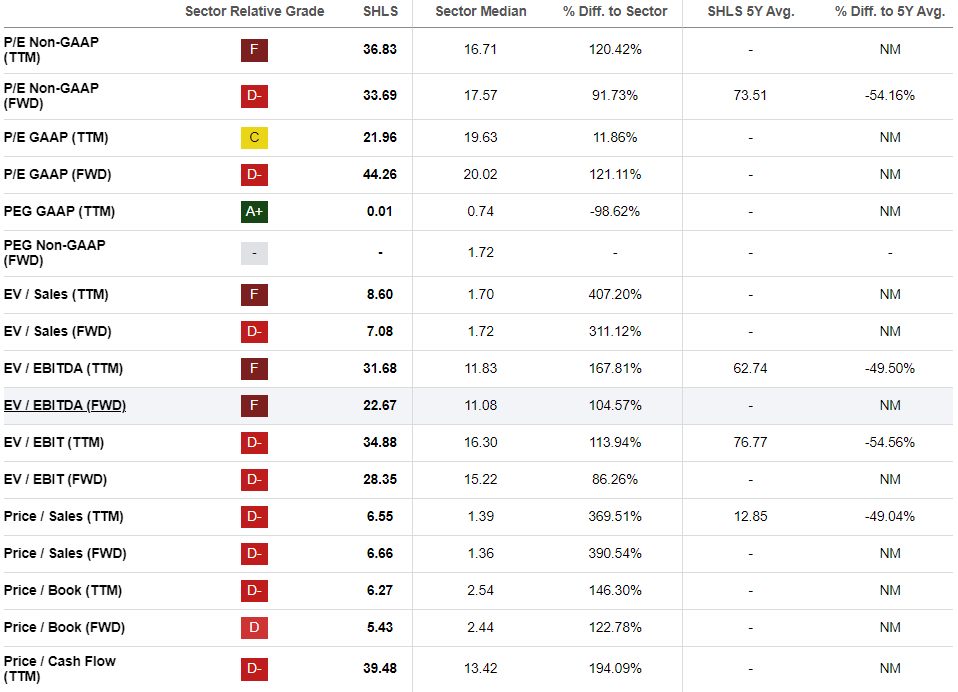

SHLS investors felt pain this year with a year-to-date 20% stock price decline, which is significantly worse than the broad market's dynamic. Seeking Alpha Quant assigns the stock a low "D+" valuation grade because SHLS's multiples are substantially higher than the sector median. On the other hand, current valuation ratios are much lower than the company's historical multiples. Though, I cannot say the stock is overvalued based on the multiples, especially given the revenue growth profile.

{kind=link}

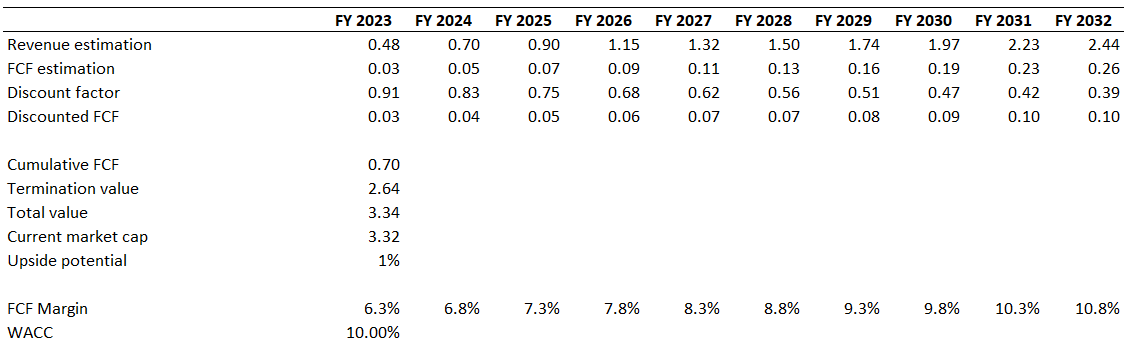

I now want to proceed with discounted cash flow ((DCF)) approach. I use a 10% WACC for discounting. I have revenue consensus estimates projecting a 20% CAGR for the next decade. I use the last five years' average FCF margin, which is 6.3%, and expect it to expand by 50 basis points yearly.

{kind=link}

The stock looks fairly valued, and the business's cumulative discounted cash flow is approximately equal to the current market cap. Revenue growth estimates are aggressive at 20% CAGR, so I balanced an optimistic revenue growth profile with a conservative FCF expansion. Overall, I think the stock is attractively valued, given the revenue growth profile and consistently positive FCF margin. Also, crucial to mention that the current stock price is substantially lower than the IPO price, which was $25 per share.

Risks to consider

Shoals mainly target the solar energy end market, which is subject to cyclicality and heavily depends on economic cycles. Economic conditions in the U.S. are now uncertain, with very mixed macroeconomic data. While we see that the unemployment rate is still low and consumption looks resilient, interest rates keep rising, and there is little evidence that the Fed will pivot soon. That said, there is a high probability that high-interest rates will eventually slow down the economy, affecting the solar energy industry as well. Though, it will be temporary and not secular.

As we have seen in the "Valuation" section, very optimistic revenue growth is projected. Consensus estimates forecast that Shoals' revenue will compound 20% annually over the next decade, which is very challenging. In case revenue growth projections are downgraded, it will have a massively adverse effect on the fair value. Also, even slight quarterly earnings misses or changes to near-term guidance might lead to massive volatility. In recent quarters, we saw many times that the stock price might drop about twenty percent intraday even after a slightly disappointing earnings release.

Bottom line

To conclude, Shoals is a "Buy" for long-term investors. I like the company's impressive profitability dynamic, especially given the relatively small scale of operations. The current stock price is close to its fair value, but I think market leaders with vast growth potential, like Shoals, should trade at a premium to its stock price.

For further details see:

Shoals Technologies: High-Quality Business In A Promising Niche