SHLS - Shoals Technologies: Well-Positioned For Growth In 2024

2023-12-29 03:00:45 ET

Summary

- Shoals’ current share price does not appropriately reflect its business fundamentals, enabling Shoals to outperform in 2024 with a 25% to 50% upside likely.

- Shoals is the leading EBOS provider in the United States with 50% market share, but they have only begun expanding into the international solar market.

- While other solar players have seen sales decline, Shoals' backlog set a record high at $633M, which is almost 5 quarters of revenue.

- Shoals recently opened a new manufacturing facility, increasing their production capacity by 75% to 35 GW. This factory will allow for significantly greater revenue while also providing production cost efficiencies.

- Shoals is well-positioned to handle the large warranty claims associated with the wire insulation shrinkback failure caused by their supplier. Additionally, they have begun litigation against the supplier to recover their warranty expenses.

Investment Thesis

Shoals Technologies Group (SHLS) is the leading utility scale electrical balance of systems (EBOS) manufacturer for solar, energy storage, and eMobility. Shoals has consistently achieved 50% to 60% year-over-year revenue growth since going public and is increasing their exposure to international markets. Shoals has incorrectly been sold off by the market alongside other solar stocks. While the general solar market sell-off is justified by lower sales and poor outlooks, Shoals has not experienced any sales pressure and their backlog has continued to increase; they even set a quarterly record in Q3.

Shoals faced pressure following the announcement of a large warranty expense associated with their BLA system. The issue stems from wire insulation shrinkback caused by defective wire made by their supplier. Shoals is well-positioned to manage the warranty claim and has begun litigation against the supplier to recover expenses.

Shoals can rally 25% to 50% next year from market improvement alone. In the long term, solar demand will continue to increase, and Shoals has a track record of producing high quality products and capturing increased market share.

About Shoals

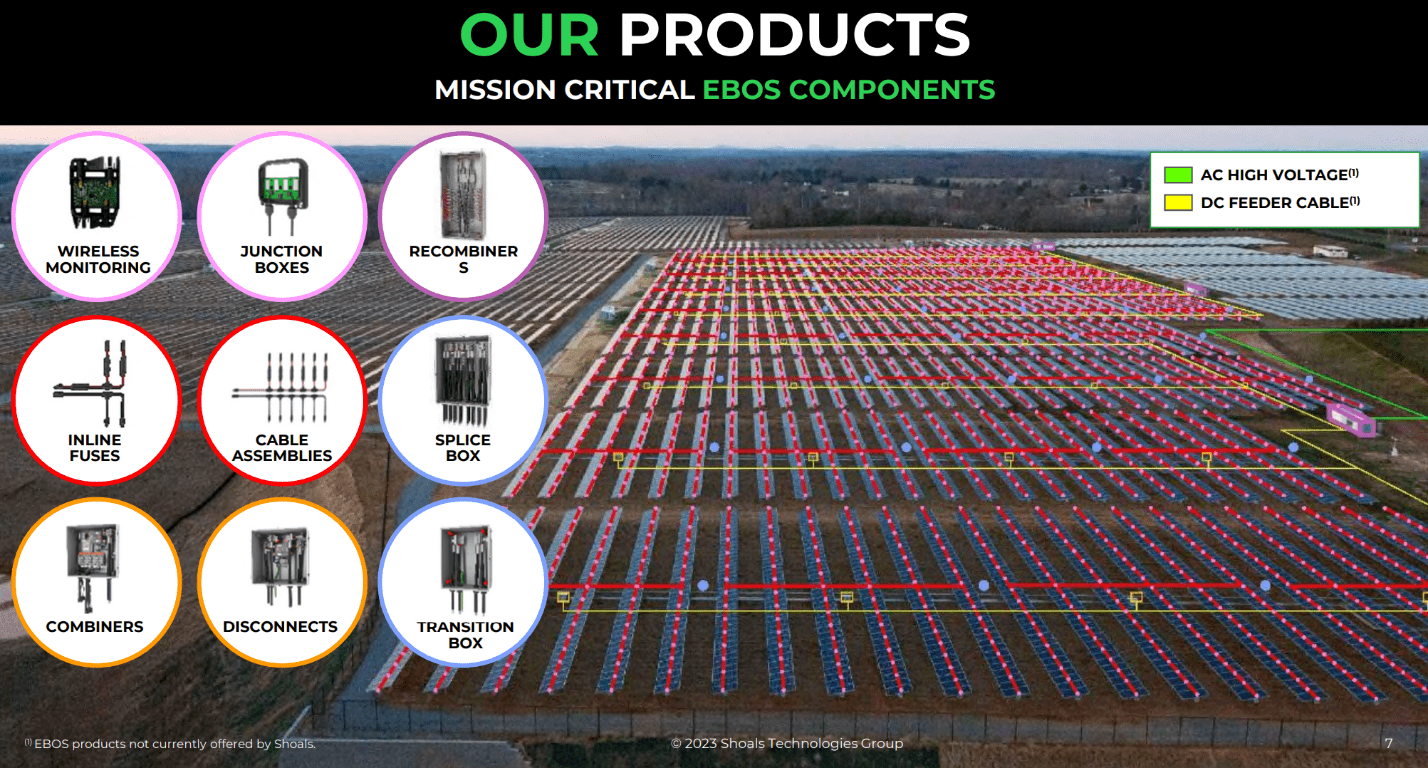

Shoals specializes in electrical balance of systems (EBOS) solutions. EBOS encompasses all the electrical components between the solar panels, inverters, batteries, and grid. This includes wiring, junctions, electrical disconnects, and monitoring systems. Shoals has also expanded into EV charging stations specifically designed for easy installation at commercial sites. Finally, in July they launched their PV health monitoring system, "Snapshot I-V" which enables remote monitoring and performance tracking on a per string level.

Shoals' product overview (Shoals - 2Q23 Earnings Presentation)

{kind=link}

Shoals started as an automotive component manufacturer before transitioning to the solar industry. They have continued to use automotive component quality control standards to ensure they produce high quality, durable parts. Shoals designs and manufactures their parts in the United States which gives them supply chain advantages and the potential to benefit from government incentives such as the Inflation Reduction Act.

Shoals' products are unique compared to industry alternatives because they can be installed above ground and their components are pushed to connect rather than custom made in the field. Traditional wiring for solar panels, called homerun wiring, entails running a wire from every row of panels to a combiner box which combines the power generated from multiple rows into a single wire. This uses lots of redundant wiring because many wires travel the same path from the combiner box. Additionally, the homerun system requires electricians to make thousands of custom connections. Shoals' system uses a push to connect connector that eliminates the need for field made connections, does not require electricians to install, and can connect many rows into a single wire by combining at the connector. Additionally, homerun systems are generally buried underground while Shoals' BLA and BLA plus are designed to be suspended above ground, making installation and maintenance faster and cheaper.

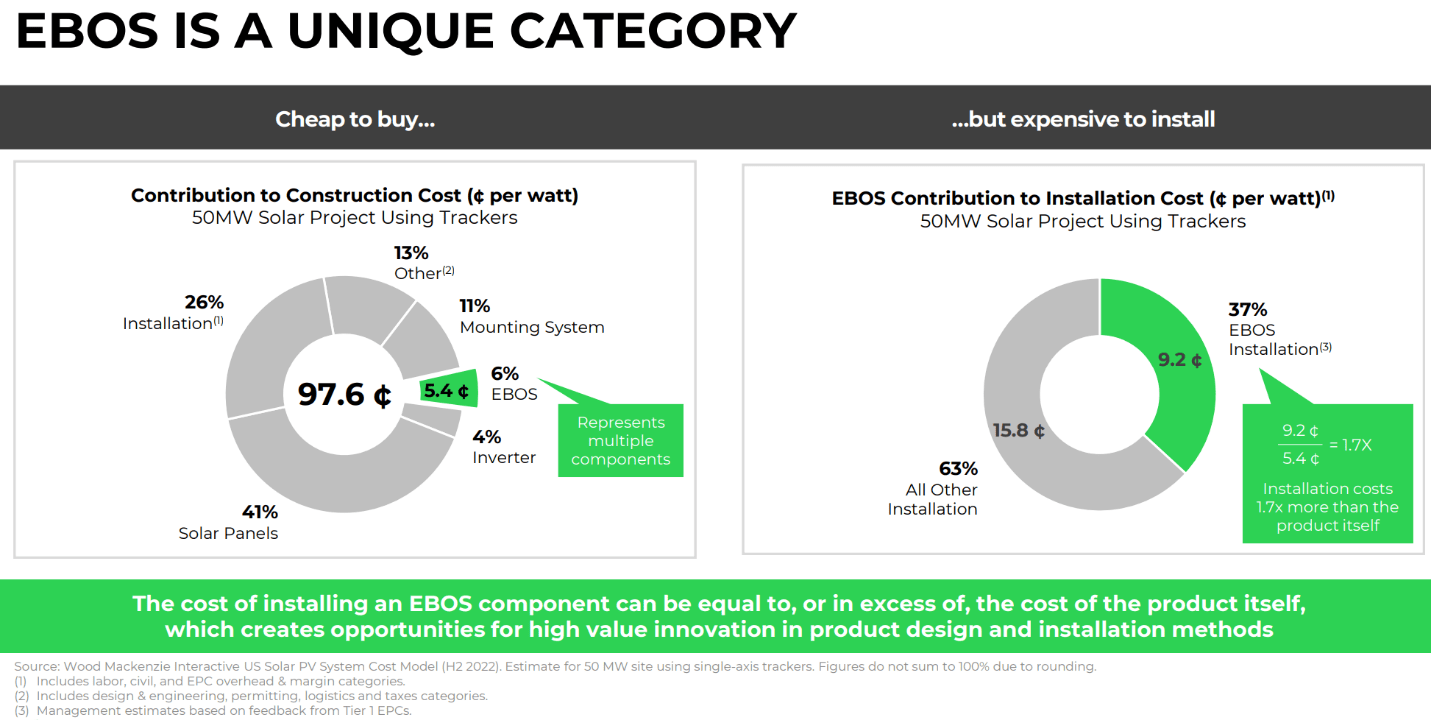

EBOS portion of total solar installation cost (Shoals - 2Q23 Earnings Presentation)

{kind=link}

The chart above shows the estimated costs associated with utility scale solar installations in H2 2022. EBOS materials are approximately 6% of the total project cost, but labor to install the components is 9% of total cost. This cost structure benefits Shoals because their product reduces costs in both categories, which allows them to charge higher prices. In their 2022 ESG report , Shoals reported their customers on average saw 43% lower installation costs and 20% lower material costs (due to less wiring and no trenching). The large savings potential has enabled Shoals to capture a 50% market share in US based solar projects and by the end of 2022, they were working with 14 of the 15 largest solar Engineering, Procurement, and Construction (EPCs) companies.

Strong and Growing Rapidly

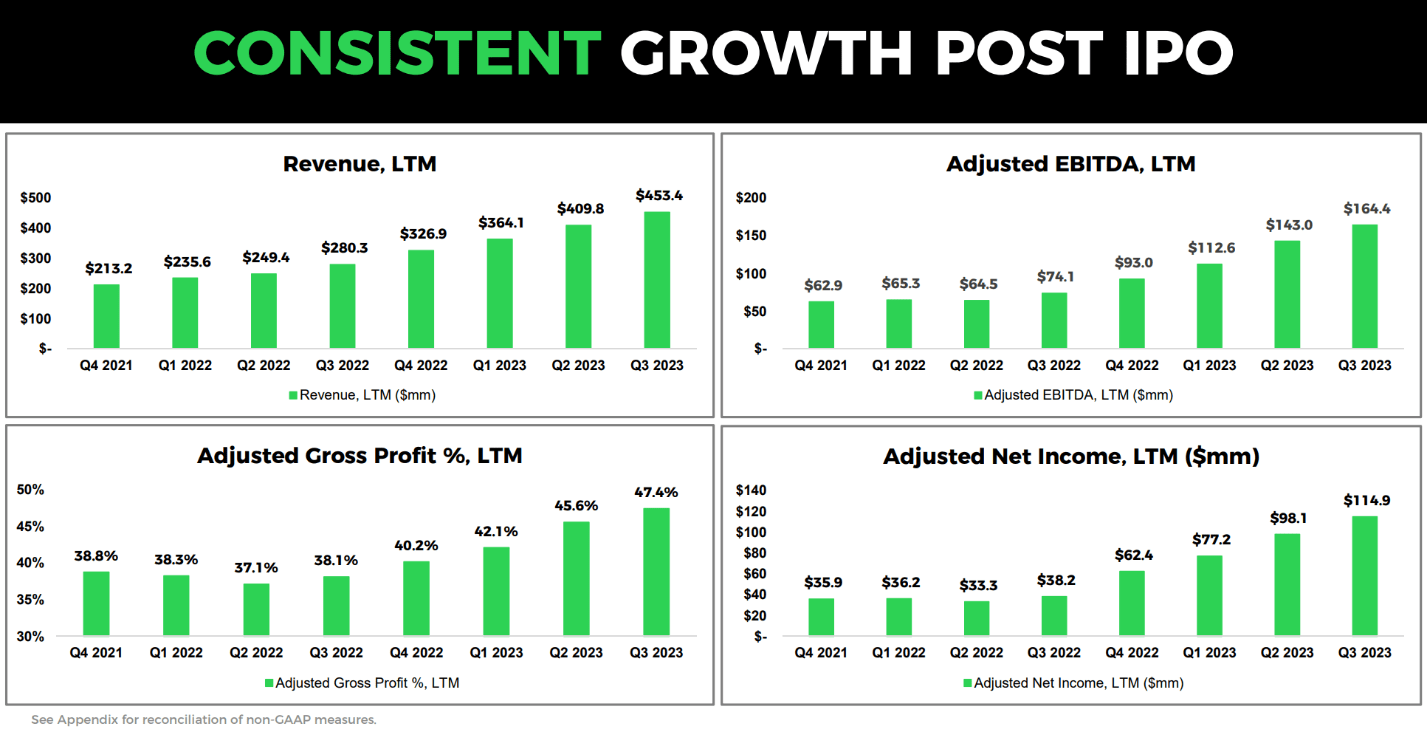

Shoals has consistently grown their business every quarter since their IPO. Their annualized revenue growth rate has been between 50% to 60%. At the same time, their profit margins have trended upward to 47% in the last quarter. Their revenue growth is backed by a strong order book and their margins have continued to improve as the company invests in new production capacity and better material usage efficiency.

At Q3 earnings, Shoals announced the completion of their third Tennessee based factory which adds 15 GW of new capacity for the production of BLA and BLA plus. The factory increases their capacity by 75% to 35 GW per year. Additionally, they can expand existing factories to 42 GW of annual production. Management believes their current capacity will be sufficient through 2025, while the new factory will boost efficiency and margins going forward.

Post IPO financial results (Shoals - 3Q23 Earnings Presentation)

{kind=link}

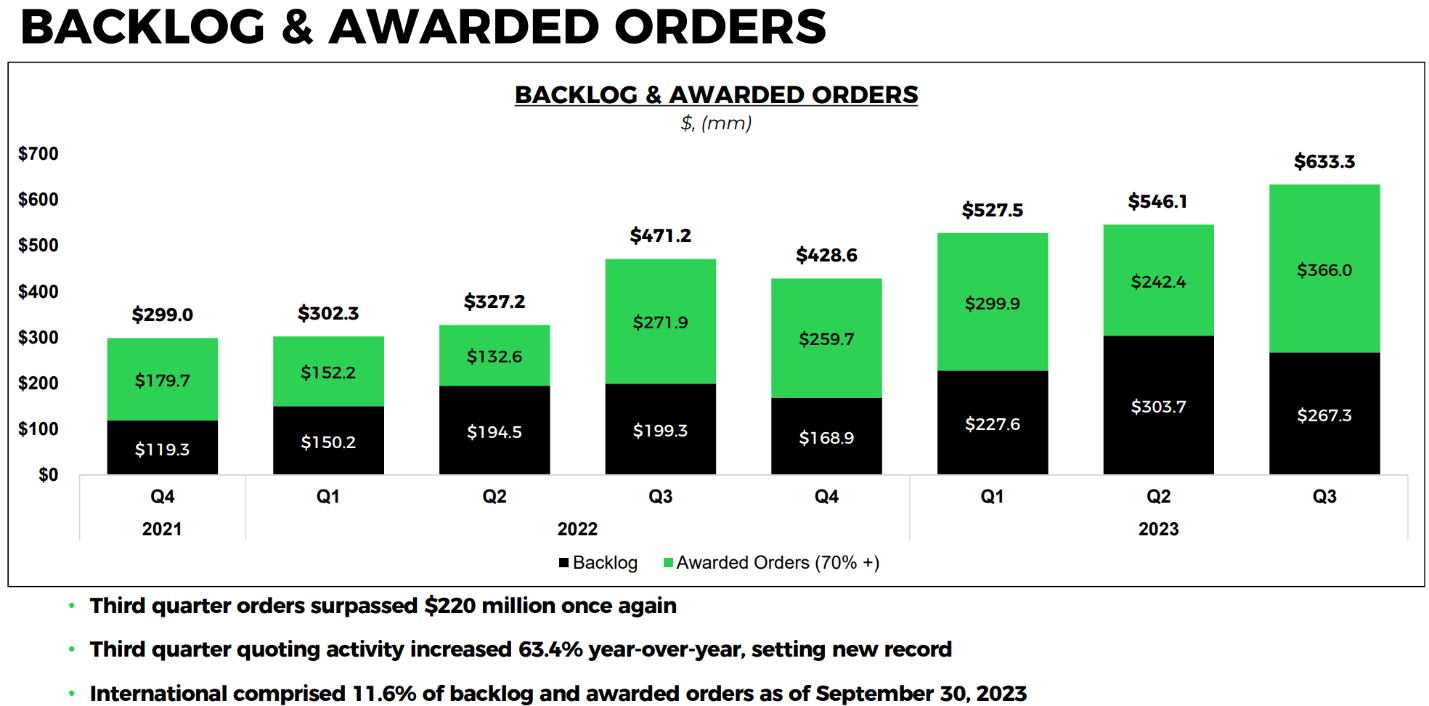

Shoals' backlog set a record last quarter at $633.3M after they added $220M in new orders and saw quoting volume increase 69% year over year. The new orders are equal to 164% of revenue ($134M) in the quarter. At their current production rate, it would take 5 quarters to produce products for all outstanding orders. With their new factory, I expect revenue to increase meaningfully through 2024 because there is ample demand for their products.

Shoals has historically focused on projects within the United States, while international projects were few and far between, largely driven by US based multinationals. Shoals has begun to get traction on international solar projects. For the first time, more than 10% of their backlog was international (11.6% as of September). Management is keen on growing international demand because the market is twice as large as the US market (where Shoals has a 50% market share ) and the market is predicted to grow at a 9% CAGR. Management believes they will be able to capture significant market share internationally, but they expect customers will require education on the benefits of Shoals above ground systems instead of buried systems which are standard.

Shoals is also looking to boost their domestic market penetration by expanding availability to smaller scale solar projects. Shoals has focused on grid scale installations greater than 75 MW. By serving smaller projects they expect to increase their TAM by 10%. Another growth driver will be energy storage. The global battery storage market is expected to increase 44x by 2030 from 2022 levels, to a total installed capacity of 680 GW of storage. Shoals doesn't make batteries, but their EBOS products include the components needed to connect batteries to the grid. Finally, in April, Shoals announced a partnership with Brookfield ( BEP , BEPC ) where Brookfield will provide charging as a service using Shoals' EV charging system.

Backlog & awarded orders (Shoals - 3Q23 Earnings Presentation)

{kind=link}

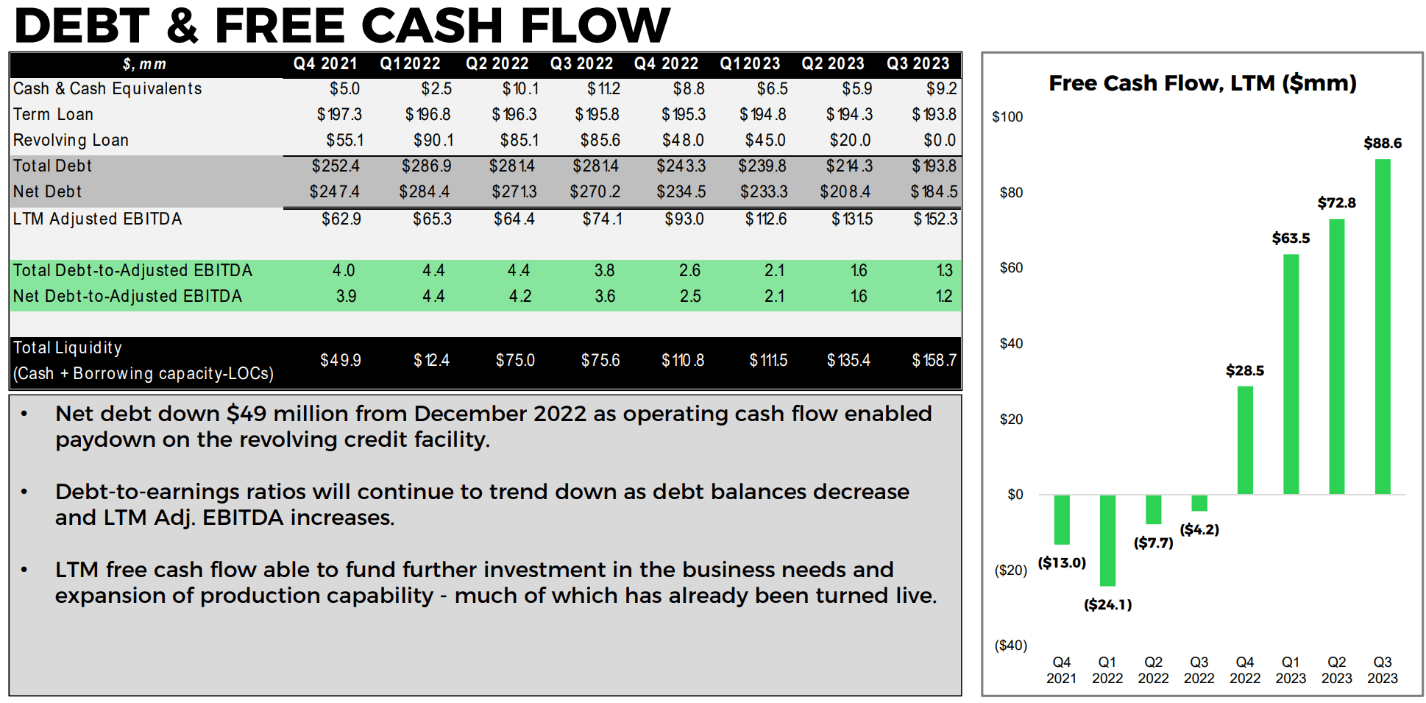

Balance Sheet

Shoals' balance sheet has improved over the past year as they deployed their free cash flow into debt reduction. In the last quarter they fully paid off their revolving line of credit and reduced their total debt to under $200M. Their remaining debt is associated with a term loan. The prepayment penalty for the loan expired in November and during the last earnings call the CFO mentioned that they are considering paying it off early and moving some of the debt to the LOC which has a lower interest rate.

Debt & free cash flow (Shoals - 3Q23 Earnings Presentation)

{kind=link}

Their total liquidity (cash + lines of credit) increased to $159M at the end of the quarter. The CFO stated that they may need to use their LOC for warranty expenses associated with wire insulation shrinkback.

Wire Insulation Shrinkback Litigation

On October 31st, Shoals filed a lawsuit against Prysmian Cables and Systems USA, LLC, the US arm of Prysmian Group ( PRYMF ). From the earnings call , the suit seeks to recover cost associated with the "identification, repair, and replacement of defective wire and is seeking full recovery from Prysmian for those, as well as future expenses related to the issue."

The suit is based on defective wire provided by Prysmian between 2020 and 2022. The wire insulation (plastic coating around the wire) was incorrectly applied, causing it to shrink over time. This results in failures near connectors as the insulation pulls back, exposing the wire. Shoals believes up to 300 sites are impacted and as many as 30% of all BLA harnesses produced during this time period used the Prysmian wire. The estimated warranty cost is between $59M and $185M. Shoals plans to cover this expense as it works with customers to ensure their solar farms continue to operate without interruption.

Prysmian is one of the largest wire providers for power systems with sales in excess of €10B per year and generated €729M in FCF in the last twelve months. If Shoals can prove their case, then Prysmian is capable of covering the costs associated with the failure. Shoals' management believes it will take several quarters for all warranty related remediation and expenses to pass.

2024 Valuation

The first part of my valuation analysis is for 2024. Solar stocks have had a rough 2023 as the impact from higher interest rates has led to reduced demand and missed sales targets. Solar companies had been priced for high growth but missed guidance and contracting sales have resulted in plummeting share prices. Shoals has traded in sympathy with the solar industry at large despite consistently improving sales and no negative guidance.

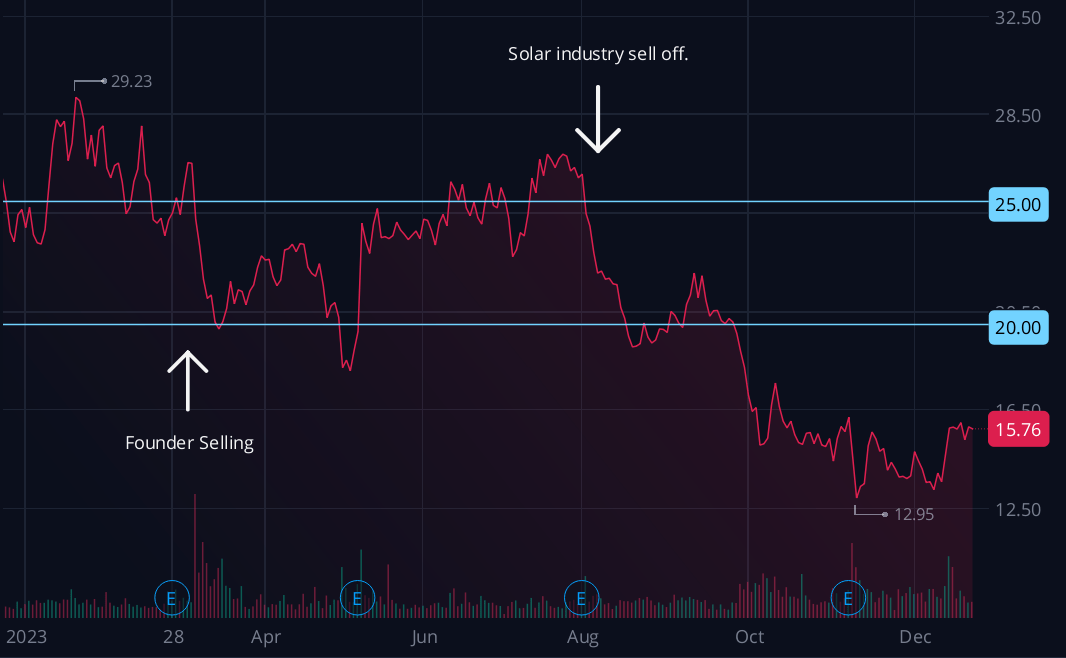

Shoals' share price over the past year has been defined by three events. First was the sale of 24.5M shares by the company's founder, Dean Solon, in March, representing 15% of shares outstanding. Shoals share price was also impacted by his selling in 2021 and 2022. The March offering represented all of his remaining shares. Therefore, the risk of large insider selling is no longer present. Second was the solar sell off beginning in August. Solar companies had been bleeding all year, but the rapid rise in treasury yields and spike in interest rates did the market in. Third was brief worry surrounding the wire insulation shrinkback warranty claim that was announced at Q3 earnings, but the share price has since recovered.

Shoals charting (By Author, Webull)

{kind=link}

Shoals charting (By Author, Webull)

I expect the share price to increase throughout 2024 due to improved economic conditions, lower interest rates, and continued revenue growth by the company. Shoals has a large backlog and longer lead times due to high demand. Orders placed in 2024 will most likely be fulfilled in 2025 or 2026. Therefore, when considering the impact economic conditions and interest rates will have, we must look forward several years. The Federal Reserve has indicated they expect to cut rates 3 times in 2024, and inflation continues to drop with CPI rising 3.1% and PPI rising only 0.9% for the last twelve months. I see no reason to expect runaway inflation ahead of us, and the ballooning government debt will incentivize the Federal Reserve to cut rates faster. This will result in lower interest rates, which will enable the construction of more solar projects leading to more opportunities for Shoals.

Prior to the solar market sell-off, Shoals was trading between $20 and $25 per share. Returning to this trading range will result in a 25% to 50% increase in the share price. Additionally, the upper end of this range is justified by my discounted cash flow analysis to come.

Long-term Valuation

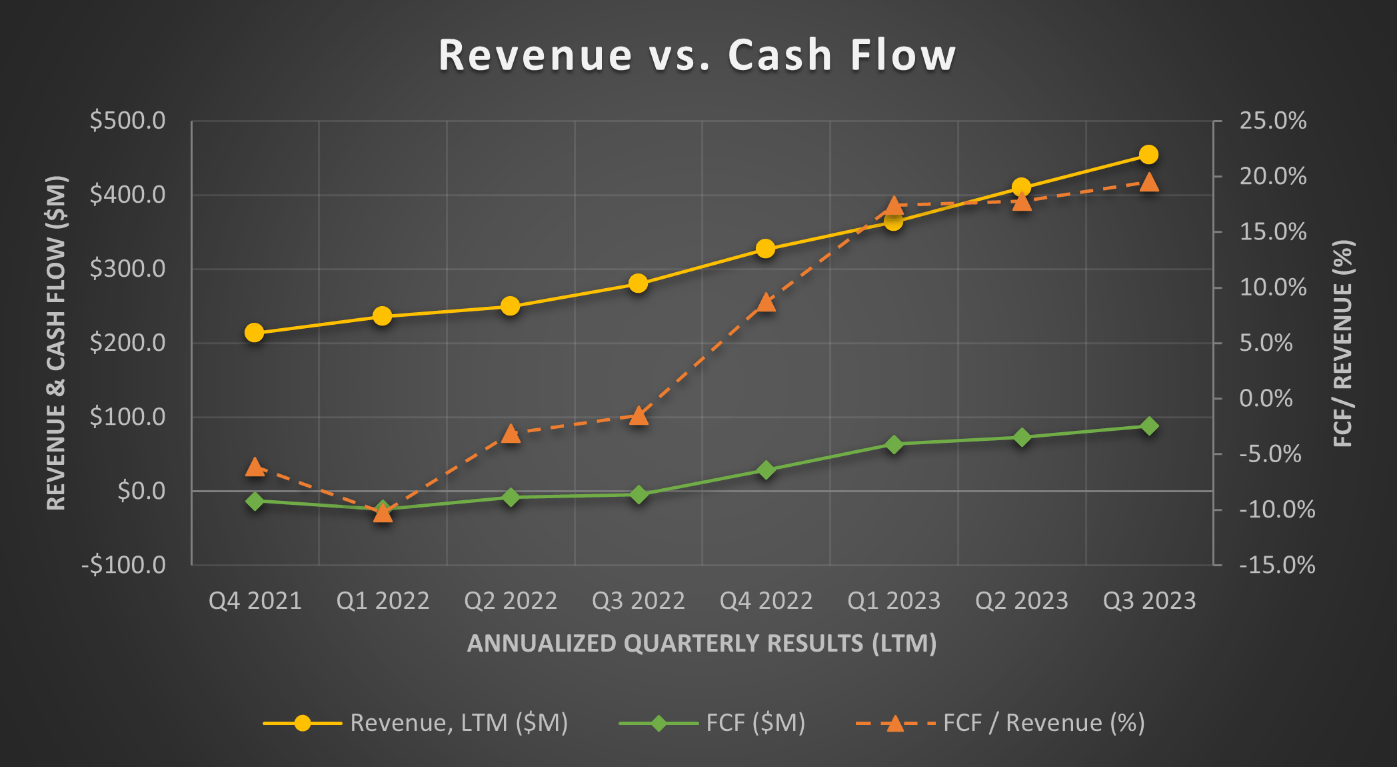

To determine a fair value for Shoals let's return to their performance and see how they have improved over time. As shown in the plot below, revenue has increased every quarter, but the key takeaway is the change in free cash flow. Shoals didn't have positive FCF until Q4 2022. Since then, FCF as a percentage of revenue has increased from a low of -10% to 19.5% in the latest quarter.

Revenue vs cash flow (By Author, Shoals - 3Q23 Earnings Presentation)

{kind=link}

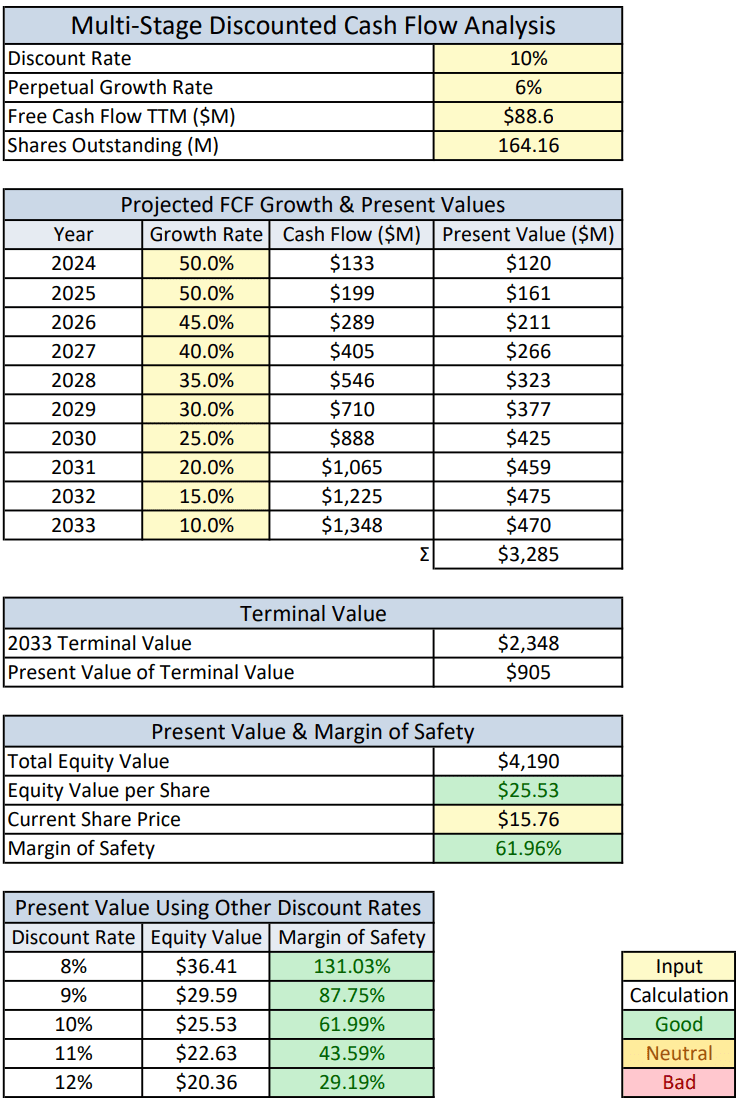

I have calculated a discounted cash flow analysis to determine a fair value and a market share analysis to validate the DCF. For the near-term growth rate, I am using 50%, which is consistent with the past two years, and is well supported by the existing backlog and increased production capacity. I am using a linear reduction in growth to the perpetual (long-term) growth rate because Shoals will eventually reach market saturation and their growth will be limited by the solar market. Management expects the solar market to grow at a 9% CAGR, while Wood Mackenzie (the leading data provider for energy and natural resources) expects the solar market to grow at an 8% CAGR. I am using a 6% perpetual growth rate because the rate of expansion will eventually decline, but replacements will help offset lower growth in new solar farms.

The DCF analysis yields a present value of $25.53 per share using a 10% discount rate. I have also included the present values using other discount rates in the table directly below the DCF calculation.

Discounted cash flow analysis (By Author)

{kind=link}

To validate the DCF analysis, I have estimated the total market share Shoals will have in 2030. Currently, Shoals' products are used in approximately 50% of all grid scale solar projects. Shoals sells their products as components or systems. The exact mix varies by quarter, but systems sales (all EBOS components) are larger than component sales (individual pieces). If the product mix trends toward more system sales, then my calculations below will be conservative; the calculations assume no change in product mix. Additionally, the analysis does not account for other growth factors such as electric car charging, battery storage, or future products.

Total revenue for the last twelve months was $453M. I am using a domestic market share of 50% and an estimated international market share of 1% (no information on the US/International split is provided). Shoals has consistently converted new clients to their products because of the value they provide. Their products are patent protected and cheaper than alternatives, therefore near monopoly market share is possible. I am forecasting three scenarios for their long-term market share, ranging from minimal growth to global market dominance.

Revenue generation calculates what Shoals' revenue would be at the forecast market share using today's solar market. To coordinate with the DCF analysis, the 2030 estimate adjusts total estimated revenue using a 9% CAGR. Finally, FCF/Revenue calculates what FCF percentage is required to match the $710M FCF estimated by the DCF at the end of 2029.

Market share forecast (By Author)

I believe the medium forecast is most likely to occur. Shoals will need FCF to be 31.3% of revenue for the DCF target to be valid. This is reasonable because they have increased the FCF rate from negative to 20% in the last two years, and their new factory is expected to increase efficiency while reducing costs.

Conclusion & Risks

Shoals faces competitor, demand, and warranty risks. Shoals remains largely unchallenged but the chance that competitors will be formed always exists. They are also suing two firms for producing knockoffs of their patented BLA systems. Shoals' growth will ultimately be limited by the solar market size. Eventually they will convert all willing EPCs, and their long-term growth necessitates expansion into international markets. The warranty costs associated with the wire insulation shrinkback will hurt earnings and cash flow for several quarters, but Shoals is looking to recover all costs associated with warranty issues from Prysmian. Investors who only read top line results are likely to miss the cause for lower earnings, leading to more selling pressure and a lower near-term stock price. For investors paying attention, this is an opportunity.

Shoals is well-positioned to benefit from the growing solar market. Despite industry headwinds caused by elevated interest rates, Shoals has continued to grow and avoided the demand declines of other industry players. Declining interest rates will lead to a recovery in solar demand. At the same time, the new factory will enable Shoals to increase their revenue significantly throughout 2024. Shoals is well-positioned for dip buyers to see outsized returns in 2024 while providing an opportunity for long-term exposure to a growing market with strong government support. I am rating Shoals a strong buy because their $15-$16 per share range provides substantial upside. I would shift to a buy rating once the stock price nears $18 per share and hold above $23 per share. In the event of a euphoric rally into the $30's, take your profits and move on.

Editor's Note: This article was submitted as part of Seeking Alpha's Top 2024 Long/Short Pick investment competition , which runs through December 31. With cash prizes, this competition -- open to all contributors -- is one you don't want to miss. If you are interested in becoming a contributor and taking part in the competition, click here to find out more and submit your article today!

For further details see:

Shoals Technologies: Well-Positioned For Growth In 2024